In the realm of financial transactions, a promissory note serves as a vital instrument that outlines the terms of a loan agreement between a borrower and a lender. In Vermont, this document is essential for establishing clear expectations regarding repayment schedules, interest rates, and any applicable fees. The Vermont Promissory Note form typically includes essential details such as the names of the parties involved, the principal amount borrowed, and the specific repayment terms. Additionally, it may address the consequences of default, ensuring that both parties understand their rights and obligations. This form not only provides legal protection but also fosters transparency in financial dealings. By utilizing the Vermont Promissory Note, individuals can confidently navigate their lending arrangements while safeguarding their interests.

Vermont Promissory Note Template

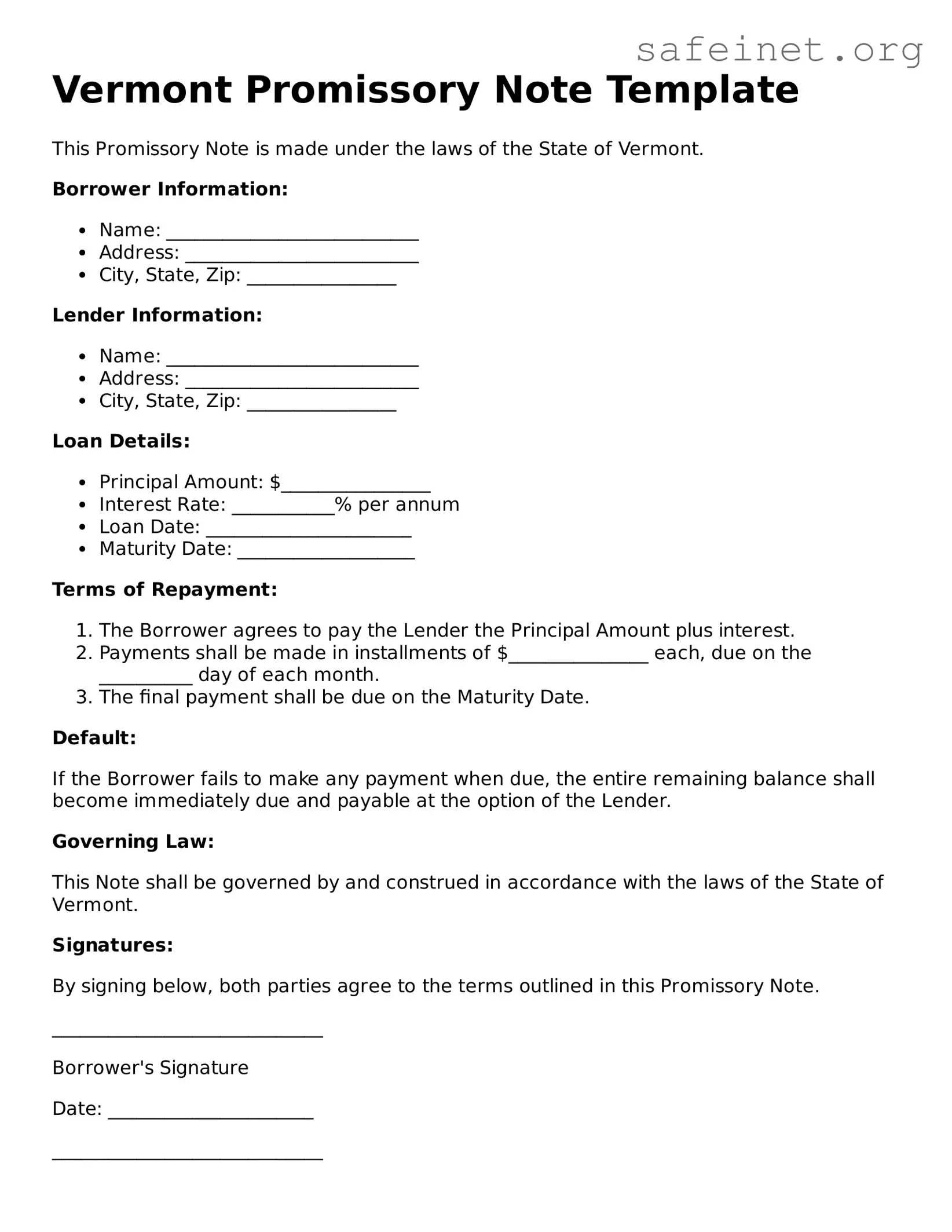

This Promissory Note is made under the laws of the State of Vermont.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Default:

If the Borrower fails to make any payment when due, the entire remaining balance shall become immediately due and payable at the option of the Lender.

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of Vermont.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

_____________________________

Borrower's Signature

Date: ______________________

_____________________________

Lender's Signature

Date: ______________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a specified time. |

| Governing Law | The Vermont Promissory Note is governed by Vermont Statutes Title 9, Chapter 3, which covers negotiable instruments. |

| Parties Involved | Typically, there are two parties: the maker (borrower) and the payee (lender). |

| Interest Rate | The note can specify an interest rate, which must comply with Vermont usury laws. |

| Payment Terms | Payment terms, including the due date and installment amounts, should be clearly outlined in the note. |

| Signatures Required | The maker must sign the note, and it is advisable for the payee to sign as well for clarity. |

| Enforceability | A properly executed promissory note is legally enforceable in court, provided it meets all legal requirements. |

| Default Consequences | If the maker defaults, the payee has the right to pursue legal action to recover the owed amount. |

| Amendments | Any changes to the terms of the note must be made in writing and signed by both parties to be valid. |

After obtaining the Vermont Promissory Note form, it is essential to fill it out accurately to ensure it meets all necessary requirements. This document will serve as a written promise to pay a specified amount under agreed terms. Follow these steps to complete the form correctly.

What is a Vermont Promissory Note?

A Vermont Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender. This note includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payment. It serves as a binding agreement between the parties involved.

Who can use a Vermont Promissory Note?

Any individual or business can use a Vermont Promissory Note. It is commonly used in personal loans, business loans, and real estate transactions. Both lenders and borrowers should understand the terms outlined in the note before signing.

What are the key components of a Vermont Promissory Note?

A typical Vermont Promissory Note includes the following components: the names and addresses of the borrower and lender, the principal amount, the interest rate, the repayment schedule, and any late fees or penalties. Additionally, it may specify the governing law and any collateral involved in the loan.

Is a Vermont Promissory Note legally binding?

Yes, once both parties sign the Vermont Promissory Note, it becomes a legally binding contract. This means that if the borrower fails to repay the loan as agreed, the lender has the right to pursue legal action to recover the owed amount.

Do I need to notarize a Vermont Promissory Note?

While notarization is not required for a Vermont Promissory Note to be legally binding, it is often recommended. Having the note notarized can provide an extra layer of protection for both parties and may help in enforcing the agreement if disputes arise.

Can I modify a Vermont Promissory Note after it has been signed?

Yes, modifications can be made to a Vermont Promissory Note, but they must be documented in writing and signed by both parties. Verbal agreements or informal changes are not enforceable, so it's essential to keep a clear record of any amendments.

What should I do if the borrower defaults on the note?

If the borrower defaults on the Vermont Promissory Note, the lender should first review the terms of the note to determine the appropriate course of action. Options may include sending a demand letter, negotiating a payment plan, or pursuing legal remedies such as filing a lawsuit. Consulting with a legal professional is advisable in such situations.

Inaccurate Borrower Information: People often provide incorrect or incomplete details about the borrower. This includes missing names, addresses, or contact information. Ensuring all information is accurate is crucial for enforceability.

Failure to Specify Loan Amount: Some individuals neglect to clearly state the total amount of the loan. This can lead to confusion later. Clearly indicating the principal amount helps avoid disputes.

Omitting Interest Rate: Many people forget to include the interest rate on the loan. This omission can create misunderstandings regarding repayment terms. Always specify the interest rate, if applicable.

Not Defining Repayment Terms: Some individuals do not outline how and when payments should be made. This includes missing details about payment frequency or due dates. Clear repayment terms help both parties understand their obligations.

Ignoring Signatures: A common mistake is failing to obtain the necessary signatures from both the borrower and the lender. Without signatures, the note may not be legally binding. Always ensure both parties sign and date the document.

When entering into a loan agreement, various forms and documents may accompany the Vermont Promissory Note. Each of these documents serves a specific purpose and helps clarify the terms and conditions of the agreement. Below is a list of commonly used forms that can enhance the clarity and security of a lending arrangement.

Understanding these documents can significantly enhance the lending experience for both parties. Each form plays a vital role in establishing clear expectations and protecting the interests of everyone involved. When navigating the complexities of a loan, having the right documentation in place is essential.

The Vermont Promissory Note form bears similarities to a Loan Agreement, which is a broader document outlining the terms of a loan between a borrower and a lender. While a promissory note focuses primarily on the borrower's promise to repay the borrowed amount, a loan agreement encompasses additional details such as interest rates, repayment schedules, and collateral requirements. This comprehensive nature of a loan agreement provides both parties with a clearer understanding of their obligations and rights throughout the lending process.

Another document akin to the Vermont Promissory Note is the Mortgage. A mortgage serves as a security instrument that ties a loan to real property. When a borrower takes out a mortgage, they agree to repay the loan while the lender retains a claim on the property until the debt is settled. Similar to a promissory note, a mortgage involves a promise to pay, but it also includes the legal framework for foreclosure in case of default. Thus, both documents are critical in the lending landscape, yet they serve different purposes in securing and documenting the loan.

The Secured Note is another document that shares characteristics with the Vermont Promissory Note. Like a promissory note, a secured note represents a borrower's commitment to repay borrowed funds. However, a secured note is backed by collateral, which provides the lender with additional security. If the borrower defaults, the lender has the right to claim the collateral to recover their losses. This added layer of protection distinguishes secured notes from standard promissory notes, making them a popular choice for lenders seeking to mitigate risk.

Lastly, the Demand Note is similar to the Vermont Promissory Note in that it involves a promise to pay a specified amount of money. The key difference lies in the repayment terms. A demand note does not have a fixed repayment schedule; instead, the lender can request repayment at any time. This flexibility can be advantageous for lenders who want to maintain control over the timing of repayment. While both documents establish a debtor-creditor relationship, the demand note’s unique feature allows for more immediate access to funds when needed.

When filling out the Vermont Promissory Note form, it’s important to approach the task with care. Here’s a straightforward list of things you should and shouldn't do to ensure the process goes smoothly.

By following these guidelines, you can help ensure that your Vermont Promissory Note is filled out correctly and effectively. A little attention to detail can go a long way in avoiding potential issues down the road.

When it comes to the Vermont Promissory Note form, several misconceptions can lead to confusion among borrowers and lenders alike. Understanding these misconceptions can help ensure that all parties involved are adequately informed and protected. Here are nine common misconceptions:

While notarization can add an extra layer of authenticity, a promissory note is legally binding as long as it is signed by the parties involved, regardless of notarization.

Many people believe that promissory notes are reserved for substantial amounts. In reality, they can be used for any loan amount, large or small.

Some assume that a promissory note must always specify an interest rate. However, it can be created as an interest-free loan if both parties agree.

This is not true. Individuals and businesses can issue promissory notes, allowing for flexibility in lending arrangements.

While both documents serve to outline agreements, a promissory note specifically focuses on the promise to repay a debt, whereas contracts can encompass a broader range of obligations.

In fact, parties can modify the terms of a promissory note if both agree to the changes and document them appropriately.

Defaulting can lead to serious repercussions, including legal action or damage to credit scores, depending on the terms outlined in the note.

Promissory notes can vary significantly in terms of structure and content. Each note should be tailored to the specific agreement between the parties.

While the note may no longer be active, it is important to keep it as a record of the transaction for future reference or in case of disputes.

Understanding these misconceptions can empower both lenders and borrowers to engage in more informed financial transactions, ultimately fostering clearer communication and better outcomes.

Filling out and using the Vermont Promissory Note form is an important process for both lenders and borrowers. Here are some key takeaways to keep in mind:

By following these key points, individuals can navigate the process of creating and using a Vermont Promissory Note more effectively.