The Tax POA WV-2848 form serves as a crucial tool for individuals seeking to appoint someone to represent them in tax matters before the West Virginia State Tax Department. This form allows taxpayers to designate an individual or organization, such as an attorney or accountant, to handle their tax-related issues, enabling them to communicate effectively with the authorities. Completing the form correctly involves providing essential information like the taxpayer's details, the representative's information, and specifying the scope of authority granted. The form is designed to ensure that the appointed representative can receive confidential information, file returns, and manage disputes. Consequently, taxpayers can maintain control over their tax affairs while benefiting from professional assistance. Understanding the nuances of the Tax POA WV-2848 form can significantly enhance the efficiency and effectiveness of tax representation in West Virginia.

Rev. 12/15

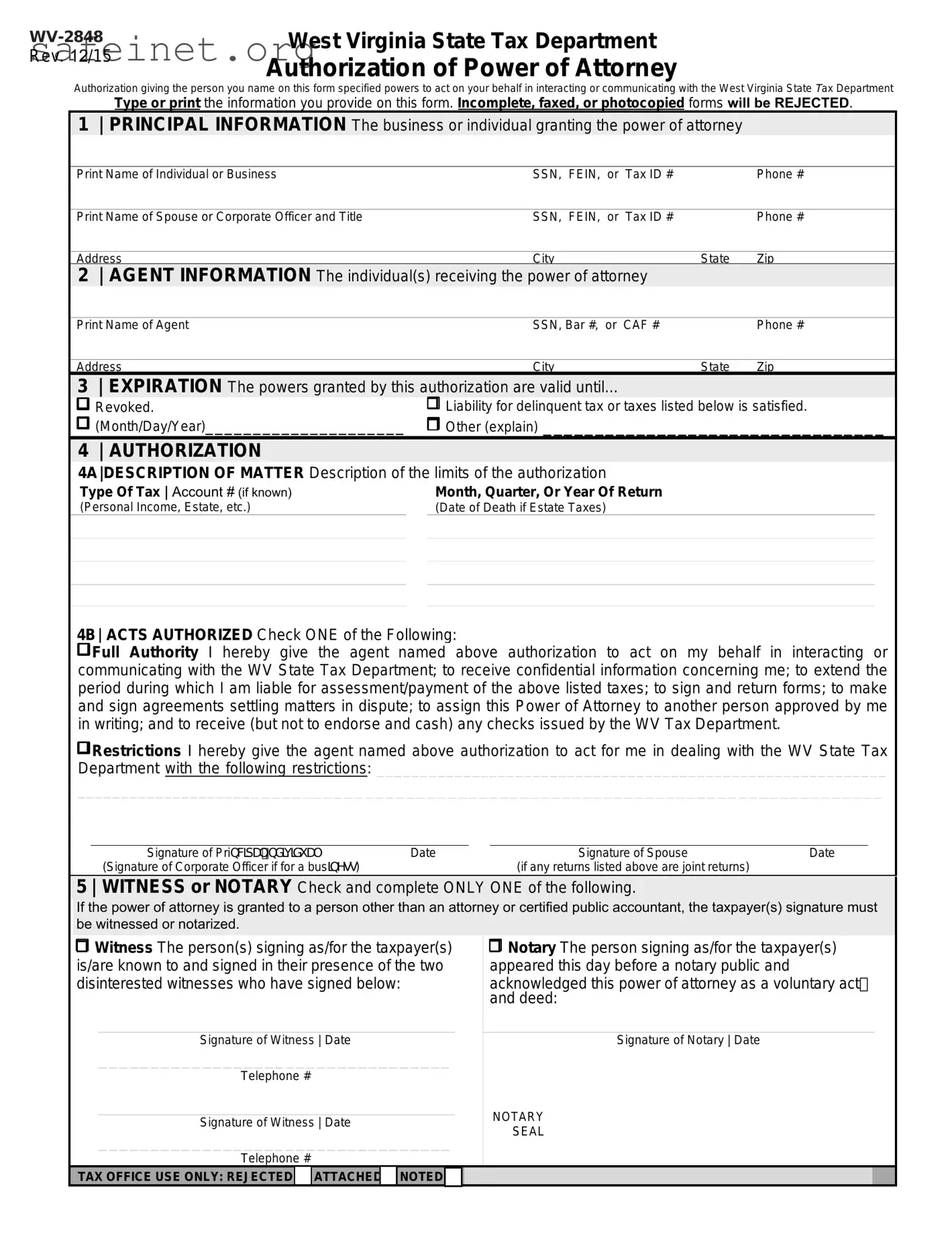

West Virginia State Tax Department

Authorization of Power of Attorney

Authorization giving the person you name on this form specified powers to act on your behalf in interacting or communicating with the West Virginia State Tax Department

Type or print the information you provide on this form. Incomplete, faxed, or photocopied forms will be REJECTED.

1| PRINCIPAL INFORMATION The business or individual granting the power of attorney

Print Name of Individual or Business |

SSN, |

FEIN, |

or |

Tax ID # |

|

Phone # |

|

|

|

|

|

|

|

Print Name of Spouse or Corporate Officer and Title |

SSN, |

FEIN, |

or |

Tax ID # |

|

Phone # |

|

City |

|

|

|

|

|

Address |

|

|

|

State |

Zip |

2| AGENT INFORMATION The individual(s) receiving the power of attorney

Print Name of Agent |

SSN, Bar #, or CAF # |

|

Phone # |

|

City |

|

|

Address |

State |

Zip |

3| EXPIRATION The powers granted by this authorization are valid until…

Revoked. |

Liability for delinquent tax or taxes listed below is satisfied. |

(Month/Day/Year)_____________________ |

Other (explain) _________________________________ |

4 | AUTHORIZATION

4A|DESCRIPTION OF MATTER Description of the limits of the authorization

Type Of Tax | Account # (if known)

(Personal Income, Estate, etc.)

Month, Quarter, Or Year Of Return

(Date of Death if Estate Taxes)

4B| ACTS AUTHORIZED Check ONE of the Following:

4B| ACTS AUTHORIZED Check ONE of the Following:

Full Authority I hereby give the agent named above authorization to act on my behalf in interacting or communicating with the WV State Tax Department; to receive confidential information concerning me; to extend the period during which I am liable for assessment/payment of the above listed taxes; to sign and return forms; to make and sign agreements settling matters in dispute; to assign this Power of Attorney to another person approved by me in writing; and to receive (but not to endorse and cash) any checks issued by the WV Tax Department.

Full Authority I hereby give the agent named above authorization to act on my behalf in interacting or communicating with the WV State Tax Department; to receive confidential information concerning me; to extend the period during which I am liable for assessment/payment of the above listed taxes; to sign and return forms; to make and sign agreements settling matters in dispute; to assign this Power of Attorney to another person approved by me in writing; and to receive (but not to endorse and cash) any checks issued by the WV Tax Department.

Restrictions I hereby give the agent named above authorization to act for me in dealing with the WV State Tax Department with the following restrictions: ___________________________________________________________

Restrictions I hereby give the agent named above authorization to act for me in dealing with the WV State Tax Department with the following restrictions: ___________________________________________________________

_________________________________________________________________________________

_____________________________________________________________________________

Signature of PriQFLSDO,QGLYLGXDO |

Date |

|

Signature of Spouse |

Date |

(Signature of Corporate Officer if for a busLQHVV) |

|

|

(if any returns listed above are joint returns) |

|

5 | WITNESS or NOTARY Check and complete ONLY ONE of the following.

If the power of attorney is granted to a person other than an attorney or certified public accountant, the taxpayer(s) signature must be witnessed or notarized.

Witness The person(s) signing as/for the taxpayer(s) is/are known to and signed in their presence of the two disinterested witnesses who have signed below:

Witness The person(s) signing as/for the taxpayer(s) is/are known to and signed in their presence of the two disinterested witnesses who have signed below:

Signature of Witness | Date

__________________________________

Telephone #

Signature of Witness | Date

__________________________________

Telephone #

Notary The person signing as/for the taxpayer(s) appeared this day before a notary public and acknowledged this power of attorney as a voluntary act and deed:

Notary The person signing as/for the taxpayer(s) appeared this day before a notary public and acknowledged this power of attorney as a voluntary act and deed:

Signature of Notary | Date

NOTARY

SEAL

TAX OFFICE USE ONLY: REJECTED  ATTACHED

ATTACHED NOTED

NOTED  ___________________________________________________________

___________________________________________________________

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA WV-2848 form is used to authorize an individual to represent a taxpayer before the West Virginia Department of Revenue. |

| Eligibility | Any individual or organization can be designated as a representative as long as they do not have a conflict of interest. |

| Form Components | The form includes sections for taxpayer information, representative details, and the scope of authority granted. |

| Governing Laws | The form is governed by West Virginia Code Chapter 11, and applicable regulations from the West Virginia Department of Revenue. |

| Submission | After completion, the form should be submitted to the West Virginia Department of Revenue either by mail or in person. |

| Revocation | Taxpayers can revoke the POA at any time by submitting a written notice to the Department of Revenue. |

| Duration | The authorization remains in effect until revoked or until the specific tax matter is resolved. |

| Signature Requirement | Taxpayers must sign the form, indicating their consent for the representative to act on their behalf. |

| Limitations | The representative cannot negotiate or enter into binding agreements unless explicitly authorized in the form. |

Filling out the Tax POA wv-2848 form is an important step in designating someone to represent you in tax matters. Once the form is completed, it should be submitted to the appropriate tax authority. Below are the step-by-step instructions to help you accurately fill out the form.

After submission, keep track of your application status and maintain communication with your representative to address any additional requirements or updates that may arise.

What is the Tax POA WV-2848 form?

The Tax POA WV-2848 form serves as a Power of Attorney document specifically used in West Virginia for tax matters. This form allows you to designate another person to represent you before the West Virginia State Tax Department. The chosen representative can handle various activities including filing returns, discussing your tax matters, receiving information, and signing documents on your behalf. This authority can be crucial for ensuring effective communication and action regarding your tax obligations.

Who can I appoint using the WV-2848 form?

You can appoint anyone to act on your behalf, provided they are qualified to represent you in tax matters. This typically includes licensed professionals such as attorneys, certified public accountants (CPAs), or enrolled agents. However, you may also choose a family member or friend who is not a professional, as long as they consent to the role. Ensure that the person you appoint is ready and willing to assist you with your tax situation.

How do I complete the WV-2848 form?

To complete the WV-2848 form, begin by downloading it from the West Virginia State Tax Department’s website. Fill in your personal information, including your name, address, and Social Security number. Next, provide the required information for the individual you are appointing, such as their name and contact details. Lastly, sign and date the form to validate your request. Make sure to keep a copy for your records, as it may be needed for future reference.

Where should I send the completed WV-2848 form?

You need to submit the completed WV-2848 form to the West Virginia State Tax Department. You can send it via mail or, in some instances, submit it electronically if the department allows. Checks need to be directed to the address specified on the form. Verify that you are following the most recent guidelines provided by the tax department to ensure timely processing of your Power of Attorney request.

Not Providing Complete Information - Many individuals fail to fill out all required fields, leading to processing delays. It's crucial to include your full name, address, and Social Security number.

Incorrect Signatures - Sometimes, people forget to sign the form or use a signature that doesn’t match the one on file with the IRS. Ensure you sign your name in the correct field before submitting.

Failing to Specify Authorization - Some filers neglect to clearly outline the extent of the representation. Be clear about what the appointed representative can handle, whether it's specific tax years or types of tax issues.

Not Keeping Copies - A common oversight is not making copies of the completed form for personal records. Always retain a copy so you can reference it if needed later.

The Tax POA WV-2848 form is essential for individuals who wish to authorize someone else to represent them in tax matters before the West Virginia State Tax Department. Alongside this form, several other documents can be necessary or beneficial. Below is a list of such forms and documents, each serving a specific purpose in the tax representation process.

Understanding these additional forms and documents is crucial for anyone engaged in tax matters in West Virginia. Having the right paperwork in order can simplify communication and facilitate smoother tax processes. Always consult with a professional if you have questions about your specific circumstances.

The IRS Form 2848 is known as the Power of Attorney and Declaration of Representative. This form grants an individual the authority to act on behalf of another person for federal tax matters. A similar document is the IRS Form 8821. This form allows an individual to receive and inspect confidential tax information. However, unlike Form 2848, Form 8821 does not permit the individual to represent the taxpayer before the IRS.

The Durable Power of Attorney (DPOA) is another related document. This legal document allows one person to act on behalf of another in financial matters, even if the principal becomes incapacitated. It differs from the Tax POA WV-2848 because it is broader in scope, covering all financial decisions, not just tax-related issues. This means that the DPOA remains effective even when the person who created it is unable to make decisions.

The Limited Power of Attorney is also similar in that it grants specific authority to another person. This document is limited to particular actions or situations and can be time-sensitive. While the Tax POA WV-2848 is used specifically for state and federal tax issues, a Limited Power of Attorney could cover a variety of situations, such as selling property or managing finances during a temporary absence.

A Medical Power of Attorney allows someone to make healthcare decisions on behalf of another person. Similar to the Tax POA WV-2848 in terms of granted authority, its focus is on medical matters rather than tax issues. This document is critical for situations where an individual cannot make their own medical decisions and needs a trusted person to advocate for them.

The Healthcare Proxy is another document that can be likened to the Tax POA WV-2848. This document specifically appoints a person to make healthcare decisions for someone else. Like the Medical Power of Attorney, it has specific applications, but its purpose is fundamentally different from the scope of tax-related duties assigned through the Tax POA.

The Financial Power of Attorney is broader and covers all aspects of managing someone’s financial affairs. This document empowers an agent to handle day-to-day financial transactions, and while it bears similarities to the Tax POA WV-2848, it applies to general financial matters rather than being limited strictly to tax responsibilities.

Finally, the Revocation of Power of Attorney is a document that terminates a previously granted power of attorney. It ensures that the appointed agent no longer has authority to act on one’s behalf. Although it serves a different purpose than the Tax POA WV-2848, it is directly related to the powers previously granted, allowing individuals to regain control when necessary.

Filling out the Tax POA WV-2848 form can be an important step in managing your tax matters. It allows you to grant someone the authority to act on your behalf in tax-related issues. To make sure you maximize the effectiveness of this form, here are some guidelines to follow.

Do's:

Don'ts:

By following these tips, you can ensure a smoother process when it comes to handling your tax affairs.

Understanding the Tax POA WV-2848 form is crucial for anyone involved in tax matters in West Virginia. Several misconceptions often arise regarding this form. Here are six common ones explained.

This is incorrect. The Tax POA WV-2848 form can be used by anyone who wishes to authorize an individual to represent them before the tax authorities, whether that individual is a professional or a relative.

This is not true. You can submit the WV-2848 form multiple times. Each submission can authorize different representatives or renew the authorization for an existing representative.

This misconception can lead to issues. While the representative can act on your behalf, you remain responsible for your tax obligations and should stay informed throughout the process.

Submitting the Tax POA WV-2848 form is free of charge. There are no fees associated with filing this authorization form with the tax authority.

This is misleading. The WV-2848 form specifically addresses state tax matters in West Virginia. It does not automatically cover federal tax issues, which require separate forms.

This is false. You have the right to revoke or modify the authorization at any point by submitting a new WV-2848 form or written notice to the tax authority.

Clarifying these misconceptions can help individuals navigate their tax situations more effectively and ensure they are utilizing the Tax POA WV-2848 form appropriately.