The Tax Power of Attorney (POA) form serves as a crucial tool for individuals wishing to delegate authority to someone else regarding their tax matters. This form allows a designated representative to act on behalf of the taxpayer in interactions with the Internal Revenue Service (IRS). It encompasses several key aspects, including the identification of the taxpayer and the individual granted the authority, the specific types of tax matters included, and the duration for which this authority is valid. A properly completed Tax POA form ensures that the representative has the legal capacity to receive confidential information, sign documents, and negotiate on behalf of the taxpayer. Understanding the different sections of this form is essential, as it outlines the powers granted and the responsibilities involved, ultimately providing a clear framework for managing tax obligations without direct involvement from the taxpayer. For individuals seeking assistance with their taxes, properly utilizing the Tax POA form can streamline the process, facilitating efficient communication with tax authorities.

mil OFDEPARTMENTREVENUE

Form REV184b, Business Power of Attorney

Read instructions before completing this form.

To grant authority for an individual or sole proprietor, complete Form REV184i, Individual or Sole Proprietor Power of Attorney.

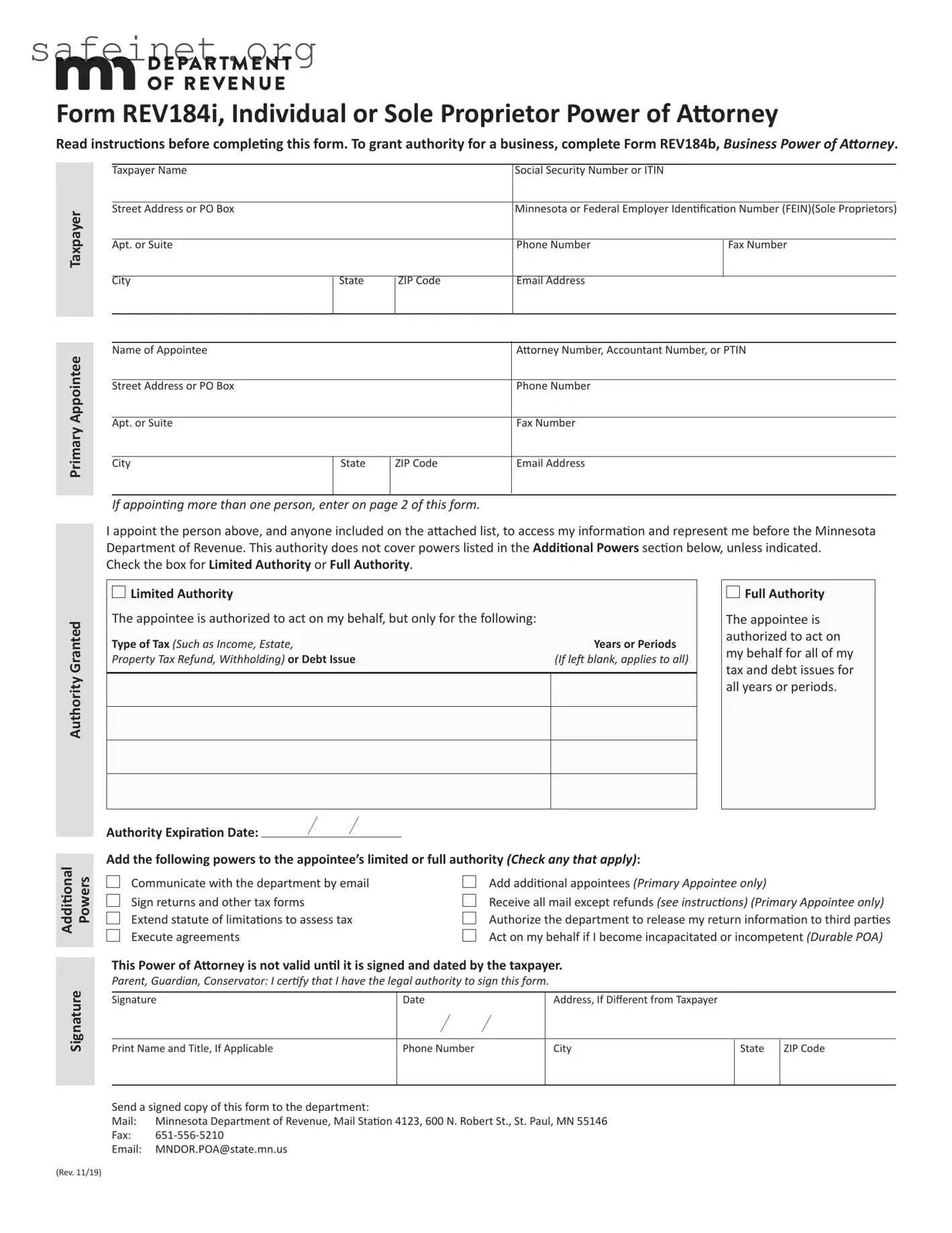

Business Taxpayer

Primary Appointee

Business Taxpayer Name |

|

|

Minnesota or Federal Employer Identification Number (FEIN) |

|

Street Address or PO Box |

|

|

Phone Number |

Fax Number |

Apt. or Suite |

|

|

|

I |

|

|

Combined Business Returns: Filing entity name (if different) |

||

City |

State |

ZIP Code |

Filing Entity FEIN or Taxpayer Identification Number |

|

I |

|

I |

|

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

|

Street Address or PO Box |

|

|

Phone Number |

|

Apt. or Suite |

|

|

Fax Number |

|

City |

State |

ZIP Code |

Email Address |

|

I |

|

I |

|

|

If appointing more than one person, enter on page 2 of this form. |

|

|

||

The person named above, and anyone included on the attached list, is appointed to access the taxpayer’s information and represent it be- fore the Minnesota Department of Revenue. Check the box for Limited Authority or Full Authority. (This authority does not cover powers listed in the Additional Powers section below, unless indicated.)

Authority Granted

□

Limited Authority

Limited Authority

The appointee is authorized to act on behalf of the taxpayer, but only for the following:

Type of Tax (Such as Business Income, |

Tax Form Name or Number |

Years or Periods |

Sales, Withholding) or Debt Issue |

(If applicable) |

(If left blank, applies to all) |

□

Full Authority

Full Authority

The appointee is authorized to act on behalf of the taxpayer for all tax and debt issues for all years or periods.

Authority Expiration Date: |

I |

I |

|

|

Signature Powers

Additional

(Rev. 11/19)

Add the following powers to the appointee’s limited or full authority (check any that apply):

□ |

Communicate with the department by email |

□ |

Add additional appointees (Primary Appointee only) |

□ |

Sign returns and other tax forms |

□ |

Receive all mail except refunds (see instructions) (Primary Appointee only) |

□ |

Extend statute of limitations to assess tax |

□ |

Authorize the department to release return information to third parties |

□ |

Execute agreements |

|

|

This Power of Attorney is not valid until it is signed and dated by someone with legal authority to sign agreements on behalf of the business taxpayer.

I certify that I have the legal authority to sign this form.

Signature |

Date |

Address, If Different from Taxpayer |

|

I |

I |

|

|

Print Name and Title |

Phone Number |

City |

State |

ZIP Code |

|

|

|

|

|

Send a signed copy of this form to the department:

Mail: |

Minnesota Department of Revenue, Mail Station 4123, 600 N. Robert St., St. Paul, MN 55146 |

Fax: |

|

Email: |

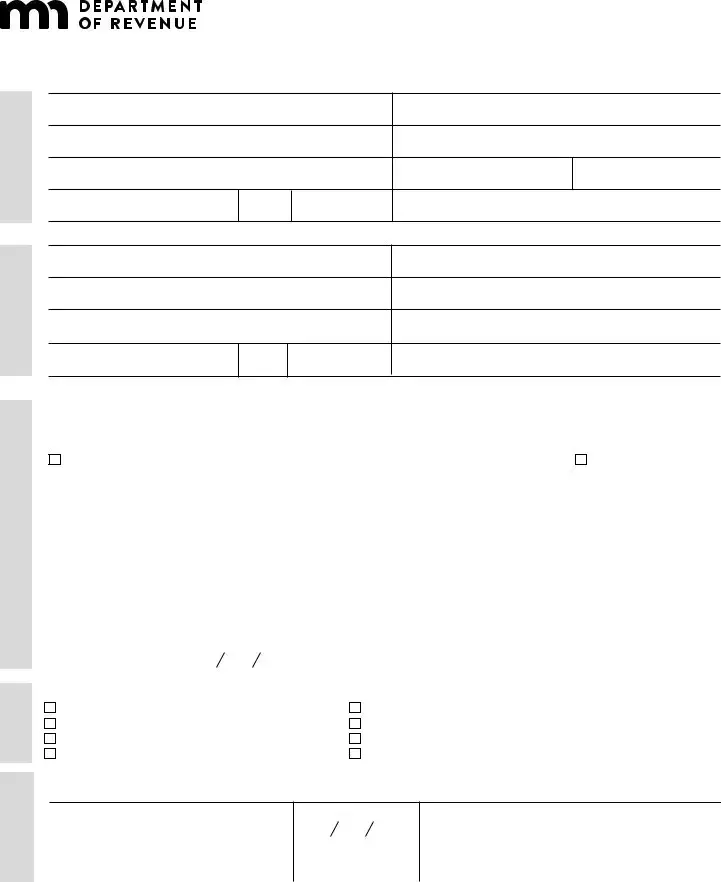

Form REV184b, Page 2 — Additional Appointees

Name of Business Taxpayer

MN ID or FEIN

Include any additional appointees below. Additional appointees only have authority over matters chosen in the Authority Granted and Additional Powers sections on page 1.

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Attach additional copies of this page, as needed.

Form REV184b Instructions

What is a Power of Attorney (POA)?

A power of attorney (POA) is a legal document that grants an attorney, accountant, agent, tax return preparer, or other person authority to access the business taxpayer’s account information and represent the taxpayer before the Minnesota Department of Revenue.

Use of Information

The information you enter on this form may be private or nonpublic under state law. We use it to allow the appointee to access the taxpay- er’s account and take actions on its behalf. We may share it with other government entities for tax administration if allowed by law. You are not required to provide the information requested; however, we are unable to process the appointment unless the form is complete.

How do I complete this form?

Business Taxpayer

Step 1

Enter the business taxpayer’s name and contact information.

Note: This form does not cover personal tax issues or sole proprietorships. Complete Form REV184i, Individual Power of Attorney.

Step 2

Enter the Federal Employer ID number (FEIN), or Minnesota Tax ID number.

Step 3

For businesses filing combined business returns, enter the name and ID number for the entity responsible for filing returns.

Primary Appointee

Eligibility: The appointee must be eligible to represent the business with the department.

The taxpayer may not appoint:

•A person barred or suspended from practice as an attorney or accountant

•A person barred or suspended from practice before the IRS

•An employee of the department

•A former department employee within one year of leaving the department

For details, go to www.revenue.state.mn.us and enter Preparer Enforcement in the Search box.

Step 4

Enter the appointee’s name and contact information. An appointee is a person selected to represent the taxpayer before the department. The taxpayer may have more than one appointee, but only the primary appointee can be selected to receive mailed correspondence from the department.

For additional appointees, complete page 2 of Form REV184b. Include additional pages, if needed. Note: The taxpayer is responsible for keeping the appointees informed of changes to its account.

Authority Granted

Step 5

Choose whether to grant the appointee full authority or to limit authority to specific issues.

Limited Authority allows the appointee to act on specific tax or debt issues.

•By tax type or issue

•By year or filing period is optional. If no year is provided, authority applies to all periods.

Full Authority allows your appointee to act on your behalf for your tax and debt issues.

Choose an expiration date for the POA if applicable. To have the POA end on a specific date, enter the month, day, and year (enter as MM/ DD/YY). If no date is provided, the POA and additional powers will remain in effect until removed.

Continued

Form REV184b Instructions, cont.

Additional Powers

Step 6

Choose additional powers to give the appointee.

•Communicate by email

Allows the appointee to communicate with the department by email.

Note: Transmit return information at your own risk. Email is not secure. The department is not liable for damages caused by interception of emails.

•Sign returns and other forms

This does not authorize the appointee to endorse or negotiate any checks or other payments issued by the department.

•Add additional appointees

Allows the primary appointee to authorize additional appointees.

Note: The appointee may only grant authority over tax types or issues authorized in the Authority Granted section.

•Execute agreements

Allows the appointee to enter into contracts and other binding agreements on behalf of the taxpayer.

•Authorize disclosure to third parties

Allows the appointee to authorize the department to share return information with people outside the department. Appointees may discuss the taxpayer’s account with people they employ or supervise, even if this box is not checked.

•Receive all mail except refunds

Authorizes the department to mail letters, legal notices, and tax information directly to the primary appointee only. Any refunds or letters relating to refunds will be sent directly to the business.

Note: The business may still receive copies of some mail from the department in certain circumstances.

This power is effective only for the tax types or issues granted to the primary appointee. If the business is only granting authority for spe- cific years or periods, this option is not available. All mail will go directly to the business.

Mail will go to the most recently designated person, replacing designations from a prior POA.

Signature

Step 7

Owners, officers, or authorized agents:

Sign, date, print your name and title, and enter your contact information. This POA is not valid until it is signed and dated by someone with legal authority to sign it

We reserve the right to request additional information as needed to verify identity and authority to sign.

Step 8

Send the form to the department using only one of the following:

•Mail: Minnesota Department of Revenue, Mail Station 4123, 600 N. Robert St., St. Paul, MN 55146

•Fax:

•Email: [email protected]

How do I revoke an appointee?

To revoke an appointee, the taxpayer or the appointee must send the department a signed and dated statement terminating the appointee’s authority or a completed Form REV184r, Revocation of Power of Attorney.

No POA form is necessary to access a taxpayer’s

Questions?

Website: www.revenue.state.mn.us

Email: [email protected]

Phone:

| Fact Name | Details |

|---|---|

| Purpose | The Tax Power of Attorney (POA) form allows someone to act on your behalf regarding tax matters. |

| Authorization | It grants authority for handling tax filings, representing the taxpayer in discussions with tax authorities. |

| Confidentiality | The form maintains confidentiality of the taxpayer's information between the taxpayer and the representative. |

| State-Specific Forms | Different states may require their own versions of the Tax POA. For example, California follows the California Revenue and Taxation Code Section 21018. |

| Duration of Authority | The authority granted by the POA does not expire unless revoked by the taxpayer. |

| Filing Requirements | Submit the form to the appropriate tax authority, either at the federal, state, or local level. |

| Notarization | Some states require notarization or witness signatures for the POA to be valid. |

| Revocation | A taxpayer can revoke the Power of Attorney at any time by submitting a specific revocation form. |

| Limitations | The representative's authority may be limited to particular tax matters or tax periods as specified in the form. |

Filling out the Tax Power of Attorney (POA) form is an important step in allowing someone to represent you regarding your tax matters. The following steps provide guidance on how to correctly complete the form, ensuring that it meets the necessary requirements for submission.

After you submit the form, your authorized representative will be able to act on your behalf regarding the designated tax matters. Be sure to keep a copy for your records.

What is a Tax POA form?

A Tax Power of Attorney (POA) form is a legal document that authorizes one person to act on another person's behalf in matters related to taxes. This form allows someone, often a tax professional, to represent the taxpayer before the Internal Revenue Service (IRS) or state tax authorities. The individual granting this authority is referred to as the principal, while the person given the authority is known as the agent or representative.

Why would I need to fill out a Tax POA form?

You might need to fill out a Tax POA form if you want someone else to handle your tax matters, such as filing tax returns, negotiating with the IRS, or responding to IRS inquiries on your behalf. This is especially useful if you do not have the time, expertise, or confidence to manage your tax situations alone. It can also help ensure that important deadlines and communications are managed promptly and correctly.

How do I complete the Tax POA form?

To complete the Tax POA form, gather all relevant information about yourself and the individual you wish to designate as your representative. You will need your identifying information, such as your Social Security number and contact details, along with similar information about your agent. Clearly indicate the scope of authority you wish to grant—this can range from general authority to specific actions. Finally, sign and date the form, as your signature will validate the document.

Do I need to submit the Tax POA form to the IRS?

After completing the Tax POA form, you typically do not need to submit it to the IRS immediately. However, you or your representative should retain a copy for your records. In certain situations, you may need to provide the form to the IRS upon request or if they require it for any ongoing issues concerning your tax account.

Can I revoke a Tax POA form?

Yes, you can revoke a Tax POA at any time. To do so, you will need to provide a written notice to your agent and any relevant tax authorities, such as the IRS. It is advisable to complete and submit a formal revocation form, which ensures that your previous agent can no longer act on your behalf. Keeping a copy of the revocation for your records is also beneficial.

Is there a fee associated with the Tax POA form?

Generally, there is no fee for completing a Tax POA form itself. However, if you choose to hire a tax professional to assist you with the form or to represent you, that professional may charge a fee for their services. Always clarify any potential costs with your representative beforehand to avoid surprises.

Where can I find the Tax POA form?

The Tax POA form can be obtained directly from the IRS website or through various state tax authority websites. Many tax professionals also provide copies of the form to their clients. Ensure you’re using the most current version of the form to avoid any issues with your submission.

Ignoring Basic Information: Some people forget to include essential personal details such as their name, address, or Social Security number. This can lead to delays or rejection of the form.

Incorrect Agent Designation: It's crucial to accurately identify the person or entity you are authorizing. A common error is failing to correctly list the agent’s name or using outdated information.

Failing to Specify Tax Matters: Many overlook the importance of clearly defining the tax matters for which the Power of Attorney (POA) applies. This could result in your agent having limited authority.

Not Using the Correct Form: Different tax situations require different forms. Filling out the wrong Power of Attorney form can result in complications or rejection.

Omitting Signatures: Completing the form without the necessary signatures is a frequent mistake. Both the taxpayer and the agent must sign for the form to be valid.

Neglecting to Date the Form: Some individuals forget to date their signatures. A missing date can complicate the validity of the POA, leading to unintended consequences.

Not Keeping Copies: Failing to make copies of the completed form can be a critical oversight. Retaining copies is important for your records and future reference.

Overlooking State-Specific Requirements: Some people assume that the Power of Attorney form is uniform across all states. Each state may have unique requirements, and ignoring these can create issues.

Inadequate Understanding of Limits: Individuals may not fully comprehend the scope of authority granted to their agent. Misunderstanding what the agent can and cannot do can lead to conflicts later.

When navigating tax responsibilities, the Tax Power of Attorney (POA) form is frequently accompanied by several other documents. These additional forms can help streamline the process and ensure all necessary permissions and information are properly handled. Below is a list of common forms and documents that you may encounter alongside a Tax POA form.

Each of these documents serves a unique purpose in managing your tax obligations and authorizing others to act on your behalf. Being familiar with them can help ensure that you are prepared for any situation that may arise during tax season or when dealing with tax authorities.

The Tax Power of Attorney (POA) form allows individuals to authorize someone else to act on their behalf in tax matters. This document shares similarities with the Limited Power of Attorney. Like the Tax POA, a Limited POA grants specific powers to an agent, but it is not restricted to tax issues. Instead, it can cover various legal and financial tasks, enabling the principal to delegate authority while maintaining control over specific areas of their affairs.

Another document akin to the Tax POA is the Durable Power of Attorney. This form allows a person to appoint an agent to manage their affairs in the event they become incapacitated. Unlike the Tax POA, which is specific to tax matters, the Durable POA can encompass a range of responsibilities, ensuring that the agent can act in financial or healthcare decisions even when the principal is unable to do so.

The Healthcare Proxy mirrors some aspects of the Tax POA by allowing individuals to appoint someone to make medical decisions on their behalf. While the Tax POA focuses solely on tax-related decisions, the Healthcare Proxy is concerned with health and medical care, thus emphasizing the importance of having trusted individuals represent one's interests in critical situations.

A Financial Power of Attorney specializes in granting authority to oversee financial matters. This document, like the Tax POA, allows for specific tasks to be managed by an agent. However, the Financial Power of Attorney encompasses a broader range of financial decisions, beyond just tax filings and obligations, offering comprehensive oversight of an individual’s financial affairs.

The Living Will also shares a functional similarity to the Tax POA in that both documents guide decision-making under specific circumstances. A Living Will provides instructions on healthcare preferences, particularly at the end of life, much like the way a Tax POA outlines decisions regarding tax representation. Both documents ensure that an individual's wishes are respected when they cannot express them directly.

A Will, as a legal document outlining how a person wishes to distribute their assets upon death, is related to the Tax POA in that both involve a designated individual acting on behalf of another. The executor named in a Will has the responsibility to manage the deceased's financial obligations, similar to how an agent uses a Tax POA to manage tax-related duties for the principal.

The Authorization for Release of Information form is another document comparable to the Tax POA. This form permits third parties, often institutions like banks or healthcare providers, to access specific information on behalf of an individual. In both cases, the scope is limited, but the intention remains to allow an agent to manage responsibilities that the principal cannot handle personally.

Lastly, the Guardianship Designation form parallels the Tax POA, as both involve appointing someone to act in a representative capacity. While the Tax POA addresses only tax matters, a Guardianship Designation takes a broader view and can be crucial in situations where an individual is unable to manage their personal affairs due to age or incapacity, ensuring that someone is legally empowered to act in their best interest.

When filling out the Tax Power of Attorney (POA) form, it's essential to approach the task carefully. Here are six helpful tips to keep in mind, including what to do and what to avoid.

When it comes to the Tax Power of Attorney (POA) form, there are a few common misconceptions that people often have. Understanding these can help you navigate your tax responsibilities more effectively.

By debunking these myths, you can approach your tax matters with greater clarity and confidence. Being informed is key when dealing with anything related to taxes!

Filling out the Tax Power of Attorney (POA) form allows you to authorize another person to act on your behalf regarding tax matters. This is essential for ensuring that someone you trust can handle your tax-related issues, especially if you are unable to do so yourself.

It's important to provide accurate information in the form, including your full name, address, and Social Security number, as well as those of the person you are authorizing. Any discrepancies can lead to delays or rejections.

Review the specific authorizations you grant carefully. You can specify the areas in which the authorized person can act, ranging from general tax matters to specific years or types of tax returns.

Understand that submitting the Tax POA form does not relieve you of your tax obligations. You remain responsible for all tax liabilities even if someone else handles communications or filings.

The IRS requires that a signed POA be submitted whenever you want to give someone the authority to discuss your tax issues. Ensuring the signature is properly executed is crucial.

Once the Tax POA form is processed and accepted, it generally remains in effect until you revoke it or the authorized individual can no longer serve. Always keep a copy for your records.