The Tax Power of Attorney (POA) Form SC2848 is an essential document for individuals who wish to grant another person the authority to act on their behalf in tax matters. This form enables taxpayers to designate an authorized representative to communicate directly with the IRS, ensuring that their interests are adequately represented without requiring their physical presence. Key features of the SC2848 include the ability to specify the scope of the representative's authority, whom they can communicate with, and the duration of their appointment. Furthermore, the form includes sections where taxpayers can input their personal information, such as names, Social Security numbers, and other identifying details, making it straightforward for the IRS to process requests efficiently. It must be duly signed and submitted to the IRS to be effective. Taxpayers often utilize this form when they face complex tax issues or when they wish to receive assistance with tax preparation and filing. Understanding the implications and proper use of the SC2848 is crucial for ensuring that one's tax affairs are managed effectively and in compliance with regulations.

|

|

|

PRINT FORM |

|

RESET FORM |

|

1350 |

|

|

|

|

|

|

|

STATE OF SOUTH CAROLINA |

|

|

|

||

|

|

|

|

|||

|

|

DEPARTMENT OF REVENUE |

|

SC2848 |

||

|

|

POWER OF ATTORNEY AND |

|

|||

|

|

|

(Rev. 2/2/18) |

|||

dor.sc.gov |

|

DECLARATION OF REPRESENTATIVE |

3307 |

|

||

|

|

|

|

|

|

|

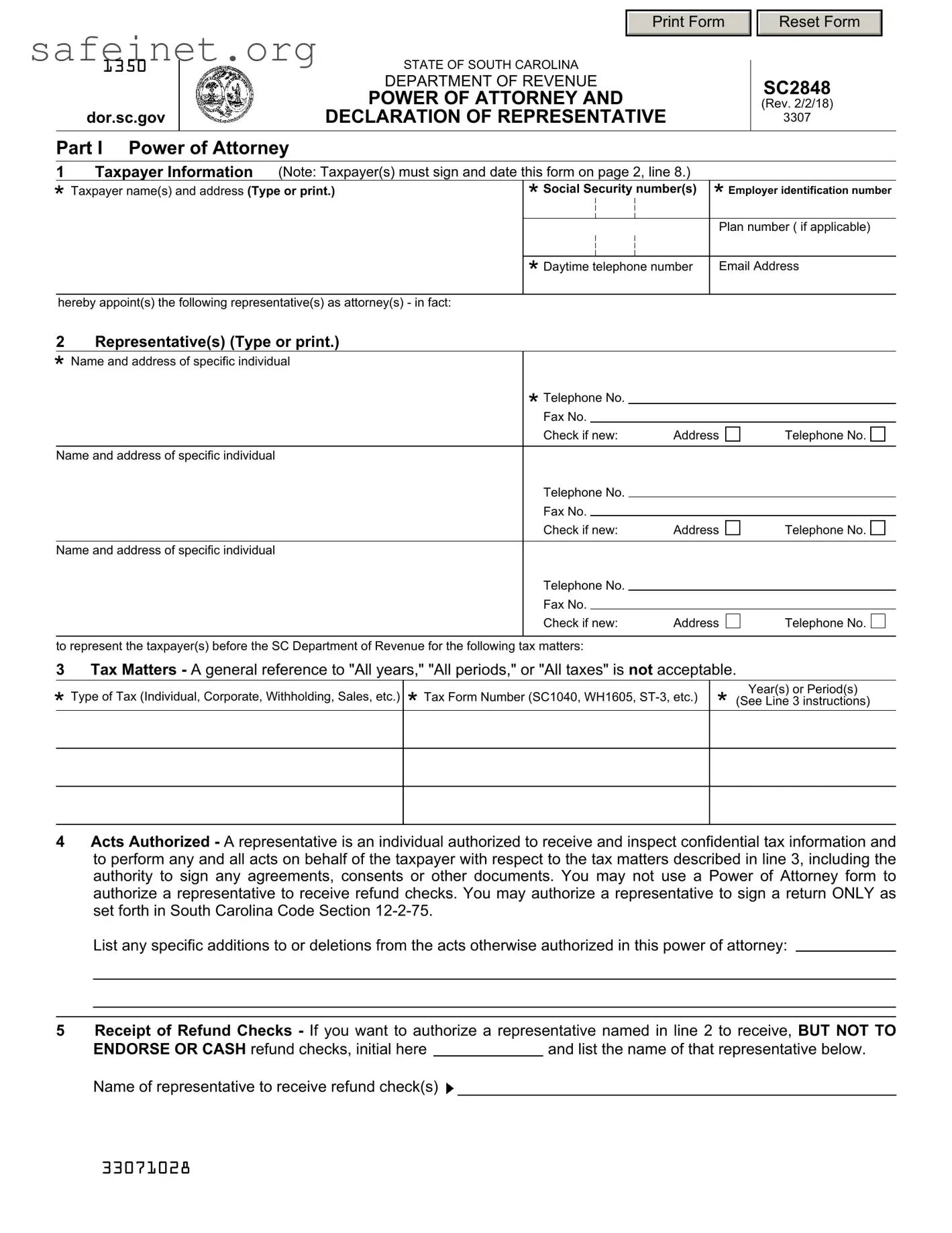

Part I Power of Attorney

1Taxpayer Information (Note: Taxpayer(s) must sign and date this form on page 2, line 8.)

|

|

|

|

|

|

|

|

* Taxpayer name(s) and address (Type or print.) |

*Social |

Security |

|

number(s) |

* Employer identification number |

||

|

|

|

|||||

|

|

|

|||||

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Plan number ( if applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* Daytime telephone number |

Email Address |

||||

|

|

|

|

|

|

|

|

|

hereby appoint(s) the following representative(s) as attorney(s) - in fact: |

|

|

|

|

|

|

2Representative(s) (Type or print.)

*Name and address of specific individual

* Telephone No. |

|

|

|

|

|

||

Fax No. |

|

|

|

Check if new: |

Address |

Telephone No. |

|

|

|

|

|

Name and address of specific individual |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

|

Check if new: |

Address |

Telephone No. |

|

|

|

|

|

Name and address of specific individual |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

|

Check if new: |

Address |

Telephone No. |

|

|

|

|

|

to represent the taxpayer(s) before the SC Department of Revenue for the following tax matters: |

|

|

|

3Tax Matters - A general reference to "All years," "All periods," or "All taxes" is not acceptable.

*Type of Tax (Individual, Corporate, Withholding, Sales, etc.)

*Tax Form Number (SC1040, WH1605,

Year(s) or Period(s)

*(See Line 3 instructions)

4Acts Authorized - A representative is an individual authorized to receive and inspect confidential tax information and to perform any and all acts on behalf of the taxpayer with respect to the tax matters described in line 3, including the authority to sign any agreements, consents or other documents. You may not use a Power of Attorney form to authorize a representative to receive refund checks. You may authorize a representative to sign a return ONLY as set forth in South Carolina Code Section

List any specific additions to or deletions from the acts otherwise authorized in this power of attorney:

5Receipt of Refund Checks - If you want to authorize a representative named in line 2 to receive, BUT NOT TO

ENDORSE OR CASH refund checks, initial here |

|

and list the name of that representative below. |

Name of representative to receive refund check(s)

33071028

6Retention/Revocation of Prior Power(s) of Attorney - The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the South Carolina Department of Revenue for the same tax matters for years or periods covered by this document .

If you do not want to revoke a prior power of attorney, check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

7Signature of Taxpayer(s) - If a tax matter concerns a joint return, both taxpayers must sign if joint representation is requested; otherwise, see the instructions for SC2848 concerning signature of taxpayer(s). If signed by a corporate officer, partner, guardian, tax matters partner/person, LLC members, executor, receiver, personal representative, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

The Department will not accept a Power of Attorney that is not signed.

*

*

|

* |

|

|

|

|

Signature |

Date |

|

Title (if |

applicable) |

|

|

|

||||

Print Name |

|

|

|

|

|

|

|

|

|

|

|

Signature |

|

Date |

|

Title (if |

applicable) |

Print Name |

|

|

|

|

|

NOTICES AND COMMUNICATIONS

All Notices and Communications will be sent to the taxpayer only. However, if you are unable to forward a copy to your named representative, you may contact our office for assistance.

Part II Declaration of Representative

I declare that:

I am authorized to represent the taxpayer(s) identified in Part I for the tax matter(s) specified; and

I am authorized to represent the taxpayer(s) identified in Part I for the tax matter(s) specified; and  I am one of the following:

I am one of the following:

aAttorney - a member in good standing of the bar of the highest court of the jurisdiction shown below.

bCertified Public Accountant - duly qualified to practice as a certified public accountant in the jurisdiction shown below.

cEnrolled Agent - enrolled as an agent under the Requirements of the US Treasury Department Circular No. 230. d Officer - a bona fide officer of the taxpayer organization.

e

f Family Member - a member of the taxpayer's immediate family (i.e., spouse, parent, child, brother, or sister). g Return Preparer.

h Other, please explain.

The Department will not accept a Declaration of Representative that is not signed.

The Department will not accept a Declaration of Representative that is not signed.

I declare that this return and all attachments are true, correct and complete to the best of my knowledge and belief. To wilfully furnish a false or fraudulent statement to the Department is a crime.

*Designation - Insert

above letter

*Jurisdiction (state)

*Signature

*Date

*indicates required field.

33072026

Instructions for SC2848

General Instructions

Purpose of Form

Use SC2848 to grant authority to an individual to represent you before the South Carolina Department of Revenue and to receive tax information. See the instructions for Part I, line 4 for limitations that may apply for certain representatives.

A fiduciary (trustee, executor, administrator, receiver, or guardian) stands in the position of a taxpayer and acts as the taxpayer. Therefore, a fiduciary does not act as a representative and should not file a power of attorney. If a fiduciary wishes to authorize an individual to represent or perform certain acts on behalf of the entity, a power of attorney must be filed and signed by the fiduciary acting in the position of the taxpayer.

Authority Granted

This power of attorney authorizes the individual(s) named to perform any and all acts you can perform, such as signing consents extending the time to assess tax, recording the interview, or executing waivers agreeing to a tax adjustment. However, authorizing someone as your power of attorney does not relieve you of your tax obligations. Delegating authority or substituting another representative must be specifically stated on line 4. However, the authority granted to a power of attorney may not exceed that allowed under SC Code Section

Filing the Power of Attorney

File the original or a photocopy or facsimile transmission (fax) with the applicable office (main or taxpayer service center). The applicable office is the office from which you request information or before which a matter, such as an audit, is pending. Paper forms can be mailed to P.O. Box 125 Columbia, SC

Substitute SC2848

Federal Form 2848 may be substituted for SC2848 even though the instructions for the two forms differ somewhat. Be sure to note the differences and complete the Federal Form 2848 accordingly.

Specific Instructions

Part I - Power of Attorney

Line 1 - Taxpayer Information

Individuals. Enter your name, SSN (and/or EIN, if applicable), and address in the space provided. If a joint return is involved, and you and your spouse are designating the same representative(s), also enter your spouse's name and SSN, and your spouse's address if different from yours.

Social Security Privacy Act

It is mandatory that you provide your social security number on this tax form. 42 U.S.C 405(c)(2)(C)(i) permits a state to use an individual's social security number as means of identification in administration of any tax. SC Regulation

Corporations, partnerships, or LLC's. Enter the name, EIN, and business address. If this form is being prepared for corporations filing a consolidated tax return (SC1120), do not attach a list of subsidiaries to this form. Only the parent corporation information is required on line 1. Also, line 3 should only list SC1120 in the Tax Form Number column. However, a subsidiary must file its own SC2848 for returns that are required to be filed separately from the consolidated return, such as

Trust. Enter the name, title, and address of the trustee, and the name and EIN number of the trust.

Estate. Enter the name, title, and address of the decedent's executor/personal representative, and the name and identification number of the estate. The identification number for an estate includes both the EIN, if the estate has one, and the decedent's SSN.

Line 2 - Representative(s)

Enter the name of your representative(s). Only individuals may be named as representatives. Use the identical name on all submissions. If you want to name more than three representatives, indicate so on this line and attach a list of additional representatives to the form. Be sure to sign and date all attachments.

Line 3 - Tax Matters

You must enter the type of tax, the tax form number, and the year(s) or period(s) in order for the power of attorney to be valid. For example, you may list "income tax, SC1040" for calendar year "2016" and "Sales tax,

You may list the current year/period and any tax years or periods that have already ended as of the date you sign the power of attorney. However, you may include on a power of attorney only future tax periods that end no later than 3 years after the power of attorney is received by the Department of Revenue. The 3 future periods are determined starting after December 31 of the year the power of attorney is received by the department. You must enter the type of tax, the tax form number, and the future year(s) or period(s).

Line 4 - Acts Authorized

If you want to modify the acts that your named representative(s) can perform, describe any specific additions or deletions in the space provided. The authority to substitute another representative or to delegate authority must be specifically stated on line 4.

Certain Limitations:

If any representative you name is someone other than an attorney, CPA or enrolled agent, the acts that person can perform on your behalf may be limited by SC Code Section

Line 5 - Receipt of Refund Checks

If you want to authorize your representative to receive, but not endorse refund checks on your behalf, you must initial and enter the name of that person in the space provided. Treasury Department Circular No. 230 (31 CFR, Part 10) prohibits an attorney, CPA, or enrolled agent, any of whom is an income tax return preparer, from endorsing or otherwise negotiating a tax refund check. If you are in a licensed attorney/client relationship, your refund may be sent to your licensed attorney.

Line 6 - Retention/Revocation of Prior Power(s) of Attorney

If there is any existing power(s) of attorney you do not want to revoke, check the box on this line and attach a copy of the power(s) of attorney. If you want to revoke an existing power of attorney and do not want to name a new representative, send a copy of the previously executed power of attorney to each office where the power of attorney was filed. The copy of the power of attorney must have a current signature of the taxpayer under the signature on line 8. Write "REVOKE" across the top of the form. If you do not have a copy of the power of attorney you want to revoke, send a statement of revocation to each office where you filed the power of attorney. The statement must indicate that the authority of the power of attorney is revoked and must be signed by the taxpayer. Also, the name and address of each recognized representative whose authority is revoked must be listed. A representative can withdraw from representation by filing a statement with each office where the power of attorney was filed. The statement must be signed by the representative and identify the name and address of the taxpayer(s) and tax matter(s) from which the representative is withdrawing.

Line 7 - Signature of Taxpayer(s)

Individuals. You must sign and date the power of attorney. If a joint return has been filed and both taxpayers will be represented by the same individual(s), both must sign the power of attorney unless one spouse authorizes the other, in writing, to sign for both. In that case, attach a copy of the authorization. However, if a joint return has been filed and both taxpayers will be represented by different individuals, each taxpayer must execute his or her own power of attorney on a separate SC2848.

Corporations or associations. An officer having authority to bind the taxpayer must sign.

Partnerships. All partners or members of an LLC must sign unless one partner or member is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if, under state law, the partner has authority to bind the partnership. A copy of such authorization must be attached. For purposes of executing SC2848, the tax matters partner is authorized to act in the name of the partnership. For dissolved partnerships, see US Treasury Regulations section 601.503(c)(6).

Other. If the taxpayer is a dissolved corporation, deceased, insolvent, or a person for whom or by whom a fiduciary (a trustee, guarantor, receiver, executor, or administrator) has been appointed, see US Treasury Regulations section 601.503(d).

PART II - Declaration of Representative

The representative(s) you name must sign and date this declaration and enter the designation (i.e., items

aAttorney - Enter the

bCertified Public Accountant - Enter the

d Officer - Enter the title of the officer (i.e., President, Vice President, or Secretary). e

f Family Member - Enter the relationship to taxpayer (i.e., spouse, parent, child, brother, or sister).

g Tax Return Preparer - Enter the

Note: If the representation is outside the United States, conditions

| Fact Name | Details |

|---|---|

| Purpose | The Tax Power of Attorney (POA) Form 2848 allows individuals to authorize another person to represent them before the IRS in tax matters. |

| Who Can Use It | Any individual or business entity that must manage tax issues with the IRS can use Form 2848. |

| Information Required | To complete the form, you'll need to provide personal information, including names, addresses, and taxpayer identification numbers. |

| Validity Period | The authority granted through Form 2848 remains valid until it is revoked, or the taxpayer passes away. |

| Filing Process | The completed form can be submitted by mail or fax to the IRS, depending on the specific circumstances. |

| Governing Law | This form is governed by the Internal Revenue Code Sections 601 and 6103. |

Once you have the Tax POA SC2848 form on hand, it’s essential to complete it accurately to ensure proper representation. Follow the steps outlined below for a smooth completion process.

What is the SC2848 form and what is its purpose?

The SC2848 form, also known as the Tax Power of Attorney, allows individuals to appoint someone else to act on their behalf regarding tax matters. This could include dealings with the IRS or state tax agencies. By completing this form, the taxpayer permits the appointed representative to receive confidential information and handle tax-related issues, ensuring that their financial affairs are managed effectively and in compliance with tax laws.

Who can I designate as my representative on the SC2848 form?

You can designate an individual or a business as your representative on the SC2848 form. This could be a trusted family member, friend, accountant, or tax attorney. It is important to choose someone who is knowledgeable about your tax situation and can represent your interests competently. Make sure that the person you select understands their responsibilities and is willing to take on this role.

How do I complete the SC2848 form correctly?

Completing the SC2848 form requires you to provide specific information about yourself, the representative, and the scope of authority you wish to grant. Begin by entering your personal information, including your name, address, and Social Security number. Next, provide the representative's details along with any specific tax matters or years you wish to include. Double-check that all information is accurate before submitting the form to avoid delays in processing.

Can I revoke the SC2848 form once it has been submitted?

Yes, you can revoke the SC2848 form at any time, as long as you follow the proper procedures. To do so, you must notify the IRS or the relevant state tax agency in writing that you wish to revoke the power of attorney. It's advisable to also inform your designated representative of your decision. By doing this, you ensure that your tax matters are handled according to your current preferences.

Failing to provide complete information:

Not signing the form:

Using outdated forms:

Incorrectly identifying the representative:

The Tax Power of Attorney (POA) Form SC2848 is an important document that allows individuals to appoint someone to represent them in tax matters. However, several other forms and documents often accompany it to ensure comprehensive representation and compliance. Here’s a look at these essential documents.

Using these forms and documents in conjunction with the Tax POA SC2848 can help streamline the process of tax management and representation. Proper documentation ensures that all bases are covered, leading to effective communication and resolution in tax matters.

The IRS Form 2848, commonly referred to as the Power of Attorney and Declaration of Representative, authorizes an individual to act on behalf of a taxpayer. There are several similar documents that serve the purpose of granting powers to representatives in various contexts.

One such document is the Durable Power of Attorney (DPOA). This form allows an individual to designate a trusted person to make financial or health decisions on their behalf should they become incapacitated. Like the IRS Form 2848, the DPOA enables an appointed agent to perform actions on behalf of the principal, but it encompasses broader powers that extend beyond tax matters.

A Medical Power of Attorney is another comparable document. This specific type of power of attorney is used to grant authority to someone to make healthcare decisions if the individual becomes unable to do so. The underlying principle of appointing a representative is similar to that of the IRS Form 2848; both documents aim to ensure that the principal's wishes are upheld, whether in tax matters or medical emergencies.

The Limited Power of Attorney (LPOA) is designed for specific situations or tasks. Individuals often use it for real estate transactions or vehicle sales, where the scope of authority is confined to particular actions. While the IRS Form 2848 provides a broad range of tax-related powers, the LPOA restricts authority to defined actions, demonstrating the flexibility of power of attorney documents.

A Corporate Resolution is similar in that it authorizes an individual to act on behalf of a corporation or business entity. Typically approved by the company’s board, this document designates responsibilities in financial or legal transactions. Like the IRS Form 2848, it empowers another to represent the interests of an entity, but is structured around organizational governance rather than individual tax matters.

The Healthcare Proxy serves a purpose akin to that of a Medical Power of Attorney, specifically focusing on making healthcare decisions on behalf of someone who is unable to communicate their preferences. This document shares foundational similarities with IRS Form 2848; it underscores the necessity for representation when the individual cannot advocate for themselves, albeit in the realm of healthcare.

In addition to these, the Tax Authorization Form (state-specific) allows tax professionals to represent clients before state tax authorities. This document typically mirrors the IRS Form 2848 but operates within the context of specific state laws and regulations, streamlining communication between taxpayers and state agencies.

Moreover, the General Power of Attorney is a comprehensive form that grants extensive authority to an agent to handle a wide range of affairs, including financial, legal, and health-related matters. While the IRS Form 2848 is narrowly focused on tax issues, the General Power of Attorney provides broad-ranging authority, thus offering flexibility in the management of one’s affairs.

The Trust document, which specifies the management and distribution of a person’s assets during their lifetime and after death, presents similarities in its purpose of appointing a representative. While the IRS Form 2848 specifically pertains to tax representation, both documents reflect the importance of entrusting responsibilities to an authorized individual.

Lastly, the Beneficiary Designation form allows individuals to designate a representative to manage their assets upon their passing. This document, often used in insurance and retirement accounts, emphasizes the notion of representation and authority, similar to the way the IRS Form 2848 enables a tax representative to act on a taxpayer’s behalf.

When filling out the Tax POA SC2848 form, taking care to follow guidelines can make the process easier. Here are some do's and don'ts to keep in mind:

The Tax Power of Attorney (POA) form SC2848 is often misunderstood. This document allows individuals to appoint someone to represent them before the Internal Revenue Service (IRS). Here are ten common misconceptions about this form, along with clarifications to help you better understand its purpose and function.

Understanding the realities of the SC2848 can empower taxpayers to navigate their tax representation options confidently. If considering using this form, ensure you review the instructions carefully and consider seeking assistance if needed.

When dealing with tax matters, filling out and using the IRS Power of Attorney (POA) Form 2848 can be crucial. Here are some key takeaways to understand its usage effectively:

Understanding how to fill out and use Form 2848 effectively can help minimize complications when dealing with your taxes.