The Tax POA RV-F0103801 form is an essential document that grants a designated representative the authority to act on your behalf concerning tax matters. This form is particularly important for individuals and businesses navigating the complex landscape of tax obligations and communications with the state tax authority. By completing this form, you empower your representative to receive information, submit documents, and manage your tax files effectively, ensuring that you remain compliant while delegating necessary tasks. Knowing how to correctly fill out the POA can streamline the process of tax management, making it easier to handle audits, disputes, or inquiries. Furthermore, this form helps protect your rights by allowing someone you trust to advocate on your behalf, relieving you of some of the stress involved in tax matters. Whether you’re managing personal taxes or business dealings, understanding the nuances of the Tax POA RV-F0103801 form can make all the difference in easing the burdens of tax administration.

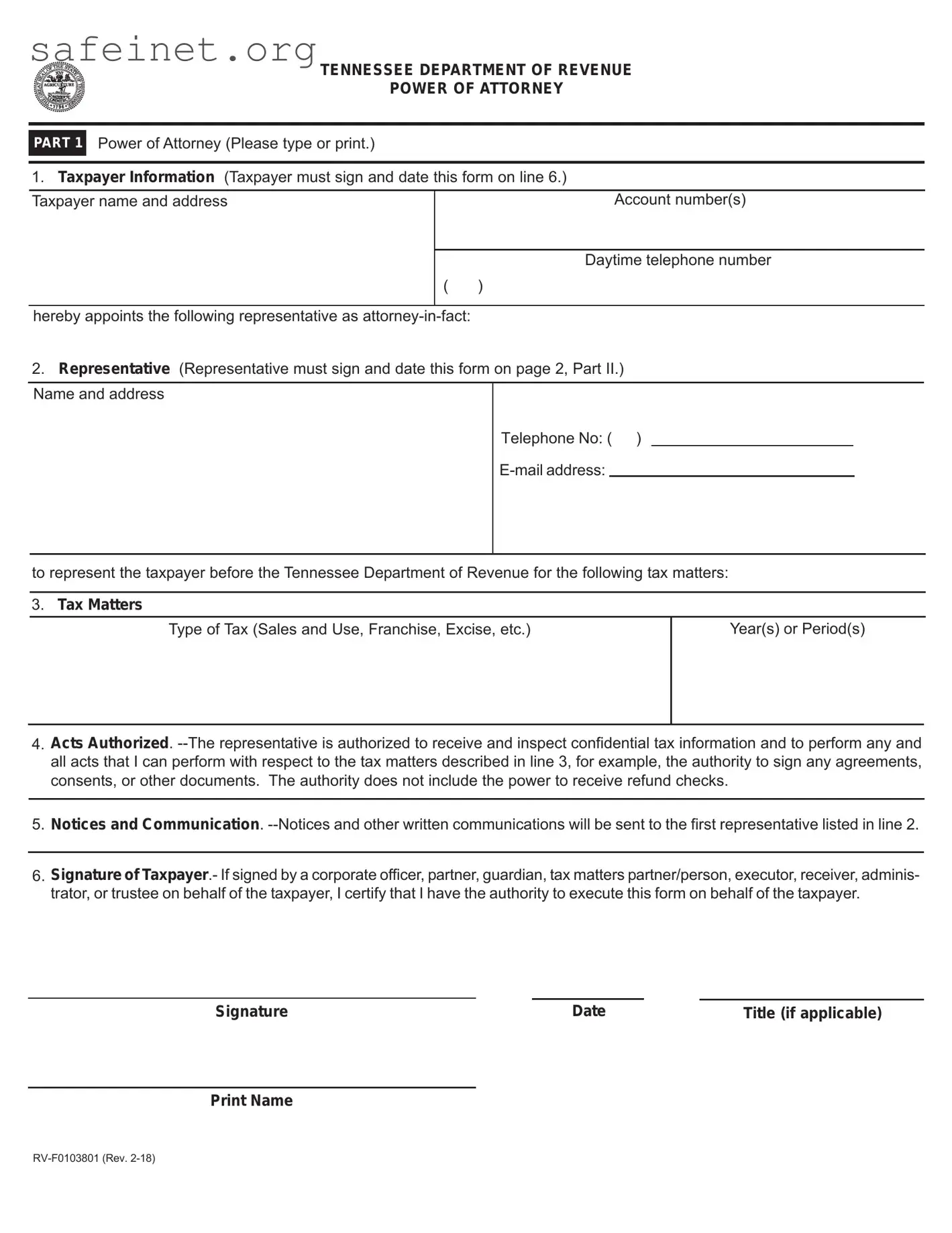

TENNESSEE DEPARTMENT OF REVENUE

POWER OF ATTORNEY

|

PART 1 |

Power of Attorney (Please type or print.) |

|

|

|

||||

|

||||

|

Taxpayer name and address |

Account number(s) |

||

|

|

|

|

|

|

|

|

|

Daytime telephone number |

( |

) |

|||

hereby appoints the following representative as

2.Representative (Representative must sign and date this form on page 2, Part II.) Name and address

Telephone No: ( )

to represent the taxpayer before the Tennessee Department of Revenue for the following tax matters:

3.Tax Matters

Type of Tax (Sales and Use, Franchise, Excise, etc.)

Year(s) or Period(s)

4.Acts Authorized.

5.Notices and Communication.

6.Signature of Taxpayer.- If signed by a corporate officer, partner, guardian, tax matters partner/person, executor, receiver, adminis- trator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

Signature |

Date |

Title (if applicable) |

Print Name

Under.penalties of perjury, I declare that:

. I am authorized to represent the taxpayer(s) identified in Part 1 for the tax matter(s) specified there; and I am one of the following designations:

a. Attorney or Certified Public Accountant

b. Officer or

c.Other

►If this declaration of representative is not signed and dated, the power of attorney will be returned.

Designation |

Jurisdiction (state) |

Signature |

|

above letter |

|||

|

|

||

|

|

|

Please mail this form to: Tennessee Department of Revenue Andrew Jackson Office Building 500 Deaderick Street

Nashville, Tennessee 37242

Date

| Fact Name | Description |

|---|---|

| Form Purpose | The Tax POA RV-F0103801 form is used to designate a Power of Attorney for tax matters with the state tax authority. |

| Governing Law | This form is governed by the laws of the state of Tennessee, specifically under the provisions by the Department of Revenue. |

| Signature Requirement | A valid signature from both the taxpayer and the designated representative is required for the form to be effective. |

| Filing Method | The form can be submitted either by mail or electronically, depending on the state tax authority's guidelines. |

Completing the Tax POA RV-F0103801 form is an important step to ensure your tax matters are handled appropriately. After filling out the form, be prepared to submit it according to the instructions provided by the appropriate agency. This will enable your designated representative to assist you with your tax affairs.

Once the form is complete, ensure that it is submitted to the appropriate tax authority in accordance with their guidelines. Keep a copy for your records.

What is the Tax POA RV-F0103801 form?

The Tax POA RV-F0103801 form is a Power of Attorney document specifically designed for tax matters in the United States. It allows an individual, known as the principal, to authorize someone else, known as the agent, to represent them before the tax authority. This representation can include filing tax returns, discussing issues related to the taxpayer’s account, and making decisions on behalf of the taxpayer regarding their tax liabilities and rights.

Who can be appointed as an agent using this form?

Any individual or entity can be designated as an agent on the Tax POA RV-F0103801 form. Common choices for agents include tax professionals such as certified public accountants (CPAs), enrolled agents, or attorneys. It is crucial for the principal to choose someone trustworthy who understands tax laws and can effectively manage their tax-related matters.

How do I complete the form?

To complete the Tax POA RV-F0103801 form, the principal must provide their personal information, including name, address, and tax identification number. The form also requires details about the appointed agent, including their name and contact information. The principal must sign and date the form to validate it. Ensure that all sections of the form are filled out accurately to avoid delays in processing.

How do I submit the Tax POA RV-F0103801 form?

After completing the Tax POA RV-F0103801 form, the principal should submit it to the appropriate tax authority. This is typically done by mailing the form to the address specified for submissions on the form or on the tax authority’s website. It may also be possible to submit the form electronically, depending on the jurisdiction's requirements. Check for any specific submission guidelines applicable to your state or local tax authority.

How long is the Power of Attorney effective?

The Power of Attorney granted by the Tax POA RV-F0103801 form remains effective as long as the principal is alive and has not revoked it. The principal can revoke the Power of Attorney at any time by providing written notice to the agent and the tax authority. Once the form is revoked, the agent no longer has the authority to act on behalf of the principal regarding tax matters.

When filling out the Tax Power of Attorney (POA) RV-F0103801 form, individuals often encounter a range of mistakes that can lead to delays or complications. Below is an expanded list of some common errors:

Many individuals overlook the necessity of filling in all required fields, such as names, addresses, and Social Security numbers of both the taxpayer and the representative. Incomplete information can lead to rejection of the form.

Individuals sometimes forget to sign the form. A signature is crucial, as it verifies that the taxpayer agrees to the authority granted to the representative.

Incorrect names, especially variations or abbreviations, can create confusion. It is important that the names match exactly with those on the tax records.

Some people overlook checking the right boxes that indicate the level of authority being granted to the representative, which can lead to misunderstandings about the powers conveyed.

Many forget to specify when the power of attorney becomes effective and when it will terminate. This omission can affect the representation.

Incorrect phone numbers or addresses for the representative can hinder communication between the taxpayer, the representative, and the tax authorities.

Sometimes, individuals assume that they can only appoint one representative. However, the form allows for multiple representatives if needed. Not listing all relevant representatives may limit their ability to act.

Each state may have specific instructions or additional forms that accompany the RV-F0103801. Failing to check these can lead to complications.

Individuals sometimes confuse where to send the completed form. It is crucial to ensure that the completed form reaches the appropriate tax authority.

Waiting until the last minute to submit the form can lead to issues, especially if the deadline for sending in related tax documents approaches.

Being aware of these common mistakes can help ensure a smoother experience when submitting the Tax POA RV-F0103801 form. Double-checking all entries and seeking guidance if necessary can mitigate potential issues.

The Tax POA RV-F0103801 form is an essential document for individuals who wish to grant authority to someone else to represent them in tax matters. Along with this form, several other documents may be used to ensure compliance and establish clear communication with tax authorities. Below is a list of commonly associated forms and documents that can facilitate this process.

By using these documents in conjunction with the Tax POA RV-F0103801 form, taxpayers can navigate their tax responsibilities more effectively. Each form serves a unique purpose and contributes to a comprehensive approach toward managing tax representation and compliance.

The Tax Power of Attorney (POA) form RV-F0103801 serves a crucial role in allowing individuals to authorize others to handle their tax matters. An analogous document is the IRS Form 2848, Power of Attorney and Declaration of Representative. Similar to the RV-F0103801, Form 2848 allows taxpayers to appoint someone to represent them before the IRS. Both forms enable authorized representatives to access confidential tax information and to take specific actions on behalf of the taxpayer, such as signing documents and negotiating tax liabilities. By utilizing these forms, taxpayers can ensure their interests are effectively managed by trusted individuals.

Another related document is the IRS Form 8821, Tax Information Authorization. Like the RV-F0103801 and Form 2848, this form allows taxpayers to reveal their tax information to a chosen representative. However, the main difference lies in the powers granted; while Form 8821 permits access to information, it does not authorize the representative to act on the taxpayer’s behalf. This distinction is significant, as it serves specific needs depending on whether a taxpayer wants their representative to obtain information or to take action regarding tax matters.

A third comparable document is the Durable Power of Attorney. This document provides a broader authority than the RV-F0103801, allowing an agent to manage financial and legal affairs, not limited to taxes. While a Durable Power of Attorney remains valid even if the principal becomes incapacitated, it does not specifically address tax-related responsibilities. Therefore, individuals often employ both the Durable Power of Attorney for general matters and the RV-F0103801 for tax-related issues, ensuring a comprehensive approach to managing their affairs.

Lastly, the state-specific tax Power of Attorney forms also share similarities with the RV-F0103801. Each state generally offers its own version that allows taxpayers to appoint someone to handle their tax matters at the state level. These forms mirror the purpose of the RV-F0103801 in facilitating tax assistance, but they are tailored to comply with state laws and regulations. Taxpayers may prefer to utilize state forms alongside the RV-F0103801 to effectively address their fiscal responsibilities across different jurisdictions.

When filling out the Tax POA RV-F0103801 form, it is important to follow some guidelines to ensure that everything is completed correctly. Here are some things you should and shouldn't do.

The Tax POA RV-F0103801 form, used for granting Power of Attorney for tax matters, is often misunderstood. Below are some common misconceptions and clarifications regarding this form.

Understanding these misconceptions can help taxpayers make informed decisions regarding their representation in tax matters.

Filling out the Tax POA RV-F0103801 form allows individuals to designate a representative to act on their behalf regarding tax matters, ensuring that communication with tax authorities occurs through this designated agent.

It is important to include accurate and complete information about both the taxpayer and the representative to prevent delays or issues in processing the designation.

Submitting this form does not relieve the taxpayer from their obligation to ensure all tax responsibilities are met; the designated representative merely acts as an intermediary.

Once filed, the form remains valid until revoked by the taxpayer or until the specified termination date, providing ongoing authority for the representative in tax matters.