The Tax Power of Attorney (POA) M-5008-R form serves as a vital document for individuals and entities navigating the complexities of tax representation. This form empowers a designated representative to act on behalf of the taxpayer in front of tax authorities, streamlining communication and potentially easing the burden of tax-related processes. It is crucial for tax professionals, including accountants and attorneys, who must manage their clients' tax affairs efficiently. Signing this form establishes a legal relationship where the representative can handle audits, appeals, and other interactions with tax agencies. Moreover, the M-5008-R includes specific sections requiring both the taxpayer and the representative to provide accurate information, reinforcing accountability. By understanding the purpose and requirements of this form, taxpayers can ensure they have the necessary support during potentially overwhelming tax matters, promoting transparency and clarity throughout the tax preparation and filing phases.

Appointment of Taxpayer Representative (Form

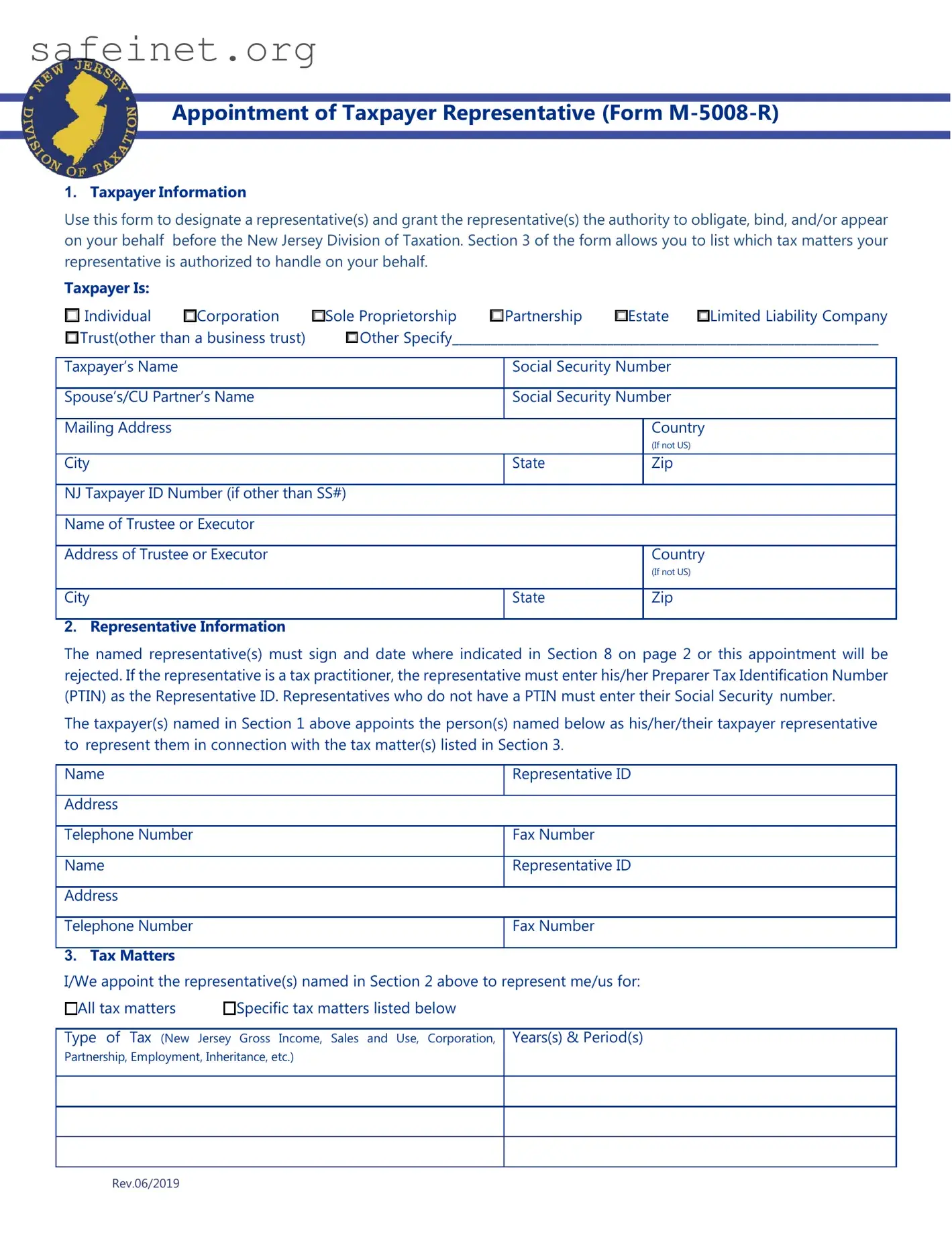

1.Taxpayer Information

Use this form to designate a representative(s) and grant the representative(s) the authority to obligate, bind, and/or appear on your behalf before the New Jersey Division of Taxation. Section 3 of the form allows you to list which tax matters your representative is authorized to handle on your behalf.

Taxpayer Is:

☐Individual ☐Corporation ☐Sole Proprietorship ☐Partnership ☐Estate ☐Limited Liability Company ☐Trust(other than a business trust) ☐Other Specify__________________________________________________________________

Taxpayer’s Name |

Social Security Number |

|

|

|

|

Spouse’s/CU Partner’s Name |

Social Security Number |

|

|

|

|

Mailing Address |

|

Country |

|

|

(If not US) |

City |

State |

Zip |

|

|

|

NJ Taxpayer ID Number (if other than SS#) |

|

|

|

|

|

Name of Trustee or Executor |

|

|

|

|

|

Address of Trustee or Executor |

|

Country |

|

|

(If not US) |

|

|

|

City |

State |

Zip |

|

|

|

2.Representative Information

The named representative(s) must sign and date where indicated in Section 8 on page 2 or this appointment will be rejected. If the representative is a tax practitioner, the representative must enter his/her Preparer Tax Identification Number (PTIN) as the Representative ID. Representatives who do not have a PTIN must enter their Social Security number.

The taxpayer(s) named in Section 1 above appoints the person(s) named below as his/her/their taxpayer representative to represent them in connection with the tax matter(s) listed in Section 3.

Name

Address

Telephone Number

Name

Address

Telephone Number

3.Tax Matters

Representative ID

Fax Number Representative ID

Fax Number

I/We appoint the representative(s) named in Section 2 above to represent me/us for: ☐All tax matters ☐Specific tax matters listed below

Type of Tax (New Jersey Gross Income, Sales and Use, Corporation, Partnership, Employment, Inheritance, etc.)

Years(s) & Period(s)

Rev.06/2019

4.Acts Authorized

The representative(s) is/are authorized to receive and inspect confidential tax records and is/are granted full power to act with respect to the tax matters described in Section 3 above, and to do and perform all such acts as I/we could do or perform. The authority granted by this appointment does not include the power to endorse a refund check.

☐If you want the representative(s) to have limited power, provide an explanation on the lines below and check this box. You may attach additional information as well.

5.Notices and Communications (audit correspondence only)

We will send original notices and other written communications to you and a copy (other than automated computer notices) to the first representative listed in Section 2 unless you check one or more of the boxes below.

☐I/We do not want the Division to send any notices or communications to my representative(s).

☐I/We want the Division to send a copy of notices and/or communications (other than automated computer notices) to both representatives listed in Section 2.

6.Retention/Revocation of Prior Appointment(s) or Power(s)

The filing of this form automatically revokes all earlier Appointment(s) of Taxpayer Representative and/or Power(s) of Attorney on file with the Division of Taxation for the tax matters and years or periods listed in Section 3 unless you check the box below.

☐I/We do not want to revoke any prior Appointment(s) of Taxpayer Representative and/or Power(s) of Attorney. If you check this box, you must attach copies of the previous Appointment(s) and/or Power(s) that you do not want to revoke.

7.Signature of Taxpayer(s)

If the tax matters covered by this appointment concern a joint Gross Income Tax return and the representative(s) is/are being appointed to represent both spouses/CU partners, both must sign below.

If a corporate officer, partner, guardian, tax matter partner, executor, administrator, or trustee signs the appointment on behalf of the taxpayer, the signature below certifies that they have the authority to execute this form on behalf of the taxpayer(s).

This Appointment of Taxpayer Representative Is Void if not Signed and Dated

Taxpayer Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

Taxpayer Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

8.Acceptance of Representation and Signature

I/ We accept the appointment as representative(s) for the taxpayer(s) who has/have executed this Appointment of Taxpayer Representative.

Representative Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

Representative Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

Rev.06/2019

Instructions for Form

Use this form to designate a representative(s) and grant the representative(s) the authority to obligate, bind, and/or appear on your behalf before the New Jersey Division of Taxation. Section 3 of the form allows you to list which tax matters your representative is authorized to handle on your behalf.

You may authorize the representative(s) to receive your confidential tax information. Unless otherwise indicated, the representative(s) may also perform any and all acts that you can perform regarding your taxes. This includes consenting to extend the time to assess tax or agreeing to a tax adjustment. Representatives may not sign returns or delegate authority unless specifically authorized to do so on this form.

Form

•When an individual appears with you or with a representative who is authorized to act on your behalf. For example, this form is not required if a representative appears on behalf of a corporate taxpayer with an authorized corporate officer;

•If a trustee, receiver, or attorney has been appointed by a court that has jurisdiction over a debtor;

•If an individual merely furnishes tax information or prepares a report or return for you;

•When a fiduciary stands in the position of, and acts as, the taxpayer. However, if a fiduciary wishes to authorize an individual to represent or act on behalf of the taxpayer, the fiduciary must sign and file Form

Limitations

Appointing a representative does not relieve you of tax responsibilities or obligations. This form allows another person to represent you in most matters concerning tax administration, tax investigations, examinations/audits, and other meetings with the Division. Because you remain responsible for your tax obligations, a representative’s authority does not extend to some aspects of the collection process. Examples of the collection process are: judgments, levies, liens, and seizures. In these instances, we may require telephone communication, direct contact, and/or interaction with the taxpayer.

Who Can Execute the Appointment of Taxpayer Representative?

•An individual, if the request pertains to a personal Income or individual Use Tax return filed by that individual (or by an individual and his or her spouse/CU partner if the request pertains to a joint Income Tax return and joint representation is requested). If joint representation is not requested, each taxpayer must file his or her own form.

•If the taxpayer is a limited liability company (LLC), a manager of the LLC. If there is no manager, a member of the LLC authorized to act on tax matters on behalf of the entity.

•A sole proprietor.

•A general partner of a partnership or limited partnership.

•The administrator or executor of an estate.

•The trustee of a trust.

•If the taxpayer is a corporation, a principal officer or corporate officer who is authorized to act on tax matters and has legal authority to reach agreements on behalf of the corporation; any person who is designated by the board of directors or other governing body of the corporation; any officer or employee of the corporation upon written request signed by a principal officer of the corporation and attested by the secretary or other officer of the corporation; or any other person who is authorized to receive or inspect the corporation’s return or return information under I.R.C. §6103(e)(1)(D).

Tax Matters

You may enter more than one tax type and indicate the tax year(s) and/or tax period(s) applicable in Section 3. If you designate a specific tax but no tax year or period, the

Rev.06/2019

Retention/Revocation of Prior Powers of Attorney and/or Appointments of Taxpayer Representative

By executing and filing the

You may not partially revoke a previously filed Form

Signature of Taxpayer(s)

You, or an individual you authorize to execute the Form

Individuals. If the matter for which the appointment is prepared involves a joint Income Tax return and the same individual(s) will represent both spouses/CU partners, both must sign Form

Corporations. The president,

Partnerships. All partners must sign Form

Limited Liability Companies (LLC). A member or manager must sign Form

Fiduciaries. In matters involving fiduciaries under agreements, declarations, or appointments, Form

Estates. The administrator or executor of an estate may execute Form

Others. Form

Instructions for Submission

Completion and submission of this form is only required when you are communicating – either in person or in writing – with the Division on behalf of another person.

In Person

If you are planning to visit a Regional Information Center on behalf of another individual, you must bring:

•The completed form, signed by both the representative and the taxpayer; and

•One form of

In Writing

If you are responding to a notice sent by the Division, submit your documentation to the PO Box on the notice. You must include with your correspondence:

•The completed form, signed by both the representative and the taxpayer;

•A copy of the notice; and

•Any corresponding documentation.

Rev.06/2019

| Fact Name | Details |

|---|---|

| Form Title | Tax Power of Attorney (POA) M-5008-R |

| Purpose | This form allows taxpayers to authorize someone to act on their behalf regarding tax matters. |

| Governing Law | This form is governed under the state tax laws of Michigan. |

| Eligibility | Any individual or entity responsible for paying taxes may use this form to designate a representative. |

| Required Information | The form requires the taxpayer's identification, the representative's details, and the scope of authority. |

| Submission Process | This form must be submitted to the Michigan Department of Treasury for it to be valid. |

| Revocation | A taxpayer can revoke this authorization at any time by submitting a written notice to the Department of Treasury. |

| Duration of Authority | Authority granted through this form remains effective until revoked or until the tax matter is resolved. |

| Updates and Changes | Taxpayers should check for updates to the form and instructions periodically to ensure compliance. |

Filling out the Tax POA M-5008-R form requires careful attention to detail. Once you have all the necessary information at hand, follow these steps to ensure accuracy and compliance.

Once submitted, allow time for processing and follow up if you don't receive confirmation within a reasonable period. It’s essential to keep communication lines open for any updates or requests for more information.

What is the Tax POA M-5008-R form?

The Tax POA M-5008-R form is a Power of Attorney document specific to tax matters in certain jurisdictions. It allows an individual or entity to designate someone else, often a tax professional, to act on their behalf concerning tax issues. This may include handling communications with the tax authority, submitting documents, and making decisions regarding tax filings. Essentially, it empowers the designee to represent you officially in tax-related matters.

Who can file the Tax POA M-5008-R form?

Any individual or business entity that needs representation in tax matters can file the M-5008-R form. This includes individuals who may not have the time or expertise to deal with tax issues themselves, as well as businesses needing to delegate administrative duties. The form can be signed by the taxpayer or an authorized representative, ensuring that the designated person has the proper authority to act.

How do I fill out the Tax POA M-5008-R form?

Filling out the Tax POA M-5008-R form involves providing specific information about both the taxpayer and the person being authorized. You will need to include names, addresses, Social Security numbers, and potentially other identification details. Clear instructions often accompany the form, guiding you on each section. Accuracy is crucial, as any errors might delay processing or result in miscommunication regarding your tax matters.

What happens after I submit the Tax POA M-5008-R form?

After submission, the tax authority will review the form to ensure it meets the necessary requirements. If approved, the designated individual or entity can begin acting on your behalf immediately. You may receive a confirmation of acceptance, but it’s wise to follow up to ensure everything is in order. Keep in mind that you can revoke the power of attorney at any time by submitting a revocation form, should your circumstances change.

When individuals fill out the Tax POA m-5008-r form, common mistakes often hinder the process. It is essential to be aware of these errors to ensure a smooth experience in delegating tax responsibilities. Below is an expanded list of mistakes frequently made during this process:

Many filers fail to provide accurate details such as their name, social security number, or address. Inconsistencies can lead to delays and complications in processing the form.

Some individuals neglect to specify the extent of the authority granted to the representative. Clearly defining the scope of power can prevent misunderstandings later on.

Omitting a signature is a common oversight. Without an appropriate signature, the form is considered incomplete and, thus, not valid.

The use of outdated forms can result in rejections. Always ensure you are filling out the most current version of the Tax POA m-5008-r form.

Individuals sometimes submit the form through improper channels. It is crucial to follow the specified guidelines for mailing or electronic submission to avoid complications.

Some may forget to include essential documents that support the authority granted. Lack of necessary documentation can lead to delays in processing the request.

Awareness of these mistakes allows individuals to take proactive steps, ensuring that their Tax POA m-5008-r form is completed accurately and efficiently.

When dealing with tax matters, it's crucial to have all the necessary documentation to ensure a smooth process. Alongside the Tax Power of Attorney (Tax POA M-5008-R) form, there are several other forms and documents you may find useful. Here’s a list of commonly used documents that can support your tax-related needs:

Having these documents on hand can greatly simplify the tax preparation process. Each form serves a specific purpose and contributes to a more organized and efficient experience. Whether you are filing your taxes, reporting income, or communicating with the IRS, understanding these forms will empower you to navigate your tax responsibilities with confidence.

The IRS Form 2848, known as the Power of Attorney and Declaration of Representative, is a crucial document for tax-related matters. Like the Tax POA m-5008-r form, it allows taxpayers to designate an individual to act on their behalf regarding tax matters. Both forms authorize representation in dealing with the Internal Revenue Service, ensuring that the appointed representative can negotiate, sign documents, and perform other tax-related activities for the taxpayer. This allows for smoother communication and record management between the IRS and the taxpayer's chosen representative.

The IRS Form 8821, Tax Information Authorization, is another document sharing similarities with the Tax POA m-5008-r form. Instead of granting full authority for representation, the Form 8821 permits a designated individual to obtain a taxpayer's confidential information. While both forms facilitate communication with tax authorities, the 8821 limits the representative's power, allowing them only to receive information but not to act on the taxpayer's behalf in the same way that a Power of Attorney does.

The California Form FTB 3520, Power of Attorney, mirrors the structure and purpose of the Tax POA m-5008-r form, but this document is specific to the California state tax system. It allows taxpayers to appoint someone to represent them before the California Franchise Tax Board. Similar to the federal form, it enables the designated representative to conduct tax matters, ensuring that the taxpayer can have local representation that understands state-specific tax laws and requirements.

The New Jersey Division of Taxation Form 548, also titled Power of Attorney, allows taxpayers to authorize a representative to handle state tax issues. Much like the Tax POA m-5008-r form, it enables the appointed person to communicate with tax authorities, sign returns, and make decisions related to New Jersey tax obligations. Both forms reflect the need for taxpayers to manage their tax affairs through trusted individuals who are knowledgeable in the respective laws.

The Florida Department of Revenue Form DR-835, Power of Attorney, shares a similar purpose with the Tax POA m-5008-r form. This document grants authority to a representative to act on behalf of a taxpayer concerning matters with the Florida Department of Revenue. Both forms ensure that taxpayers have the capacity to delegate their tax responsibilities, facilitating a smoother resolution of tax issues at both state and federal levels.

When filling out the Tax POA M-5008-R form, it's crucial to adhere to specific guidelines to ensure accuracy and compliance. Here are ten essential dos and don'ts to consider:

Understanding the Tax POA m-5008-r form is crucial for taxpayers looking to grant power of attorney to someone else regarding their tax matters. However, several misconceptions surround this form, leading to confusion among individuals. Below are four common misconceptions, along with clarifications to dispel any misunderstandings.

This is not true. While business owners often use this form, any taxpayer can designate an agent to handle their tax affairs. Individuals, regardless of their employment status, can benefit from having someone represent them during tax matters.

Many believe that only licensed attorneys can be appointed as agents on the Tax POA m-5008-r form. In reality, the agent can be a family member, friend, or any individual trusted to handle tax-related issues. The key requirement is that the appointed person is reliable and knowledgeable about tax processes.

This misconception can lead to complications. Submitting a new Tax POA m-5008-r form does not inherently void previous agreements unless specifically stated. It is important to communicate clearly if the intention is to revoke former powers of attorney.

This is inaccurate. While the agent does have the authority to act on the taxpayer's behalf in tax matters specified within the form, the taxpayer retains the right to monitor and manage the relationship. Oversight can help ensure that the agent acts in the best interest of the taxpayer.

The Tax POA (Power of Attorney) M-5008-R form is an important document for tax-related matters in the U.S. Below are key takeaways regarding its completion and use.

Understanding these key aspects will help in effectively utilizing the Tax POA M-5008-R form.