The IRS Form 2848, often referred to as the Power of Attorney (POA) for taxes, plays a crucial role in tax representation. This form enables individuals to designate a trusted representative to act on their behalf regarding matters that involve the Internal Revenue Service. By completing the 2848, taxpayers can authorize their chosen representative—be it an attorney, accountant, or other qualified individual—to receive confidential information and communicate with the IRS. It covers various tax matters, including individual income tax, business taxes, and estate taxes. One of the major benefits of Form 2848 is its ability to streamline communication between the IRS and the representative, reducing the burden on the taxpayer while ensuring that their interests are adequately represented. Additionally, it is essential to understand the form's expiration and revocation procedures, as well as any specific limitations on the powers granted. Whether you're facing an audit, need assistance with filing, or require help navigating complex tax laws, the 2848 form is your gateway to authoritative representation during the tax process.

Form

Power of Attorney and

Declaration of Representative

Rev. 7/14

Massachusetts

Department of

Revenue

See separate instructions. Please print or type.

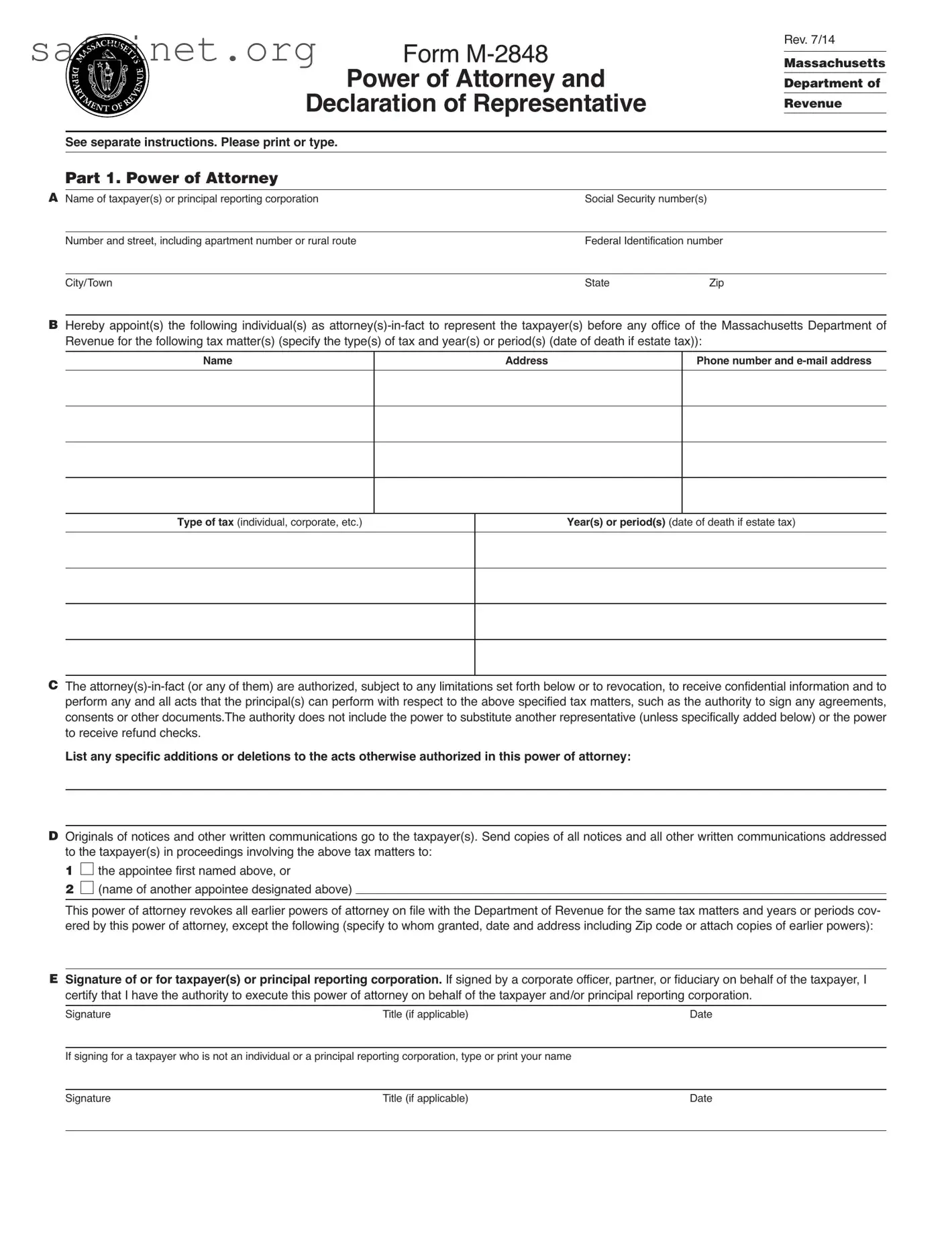

Part 1. Power of Attorney

A Name of taxpayer(s) or principal reporting corporation |

Social Security number(s) |

|

|

|

|

|

|

|

Number and street, including apartment number or rural route |

Federal Identification number |

|

|

|

|

|

|

City/Town |

State |

Zip |

BHereby appoint(s) the following individual(s) as

Name

Address

Phone number and

Type of tax (individual, corporate, etc.)

Year(s) or period(s) (date of death if estate tax)

CThe

List any specific additions or deletions to the acts otherwise authorized in this power of attorney:

DOriginals of notices and other written communications go to the taxpayer(s). Send copies of all notices and all other written communications addressed to the taxpayer(s) in proceedings involving the above tax matters to:

1 □

the appointee first named above, or

the appointee first named above, or

2 □

(name of another appointee designated above)

(name of another appointee designated above)

This power of attorney revokes all earlier powers of attorney on file with the Department of Revenue for the same tax matters and years or periods cov- ered by this power of attorney, except the following (specify to whom granted, date and address including Zip code or attach copies of earlier powers):

ESignature of or for taxpayer(s) or principal reporting corporation. If signed by a corporate officer, partner, or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney on behalf of the taxpayer and/or principal reporting corporation.

Signature |

Title (if applicable) |

Date |

If signing for a taxpayer who is not an individual or a principal reporting corporation, type or print your name

Signature |

Title (if applicable) |

Date |

|

|

|

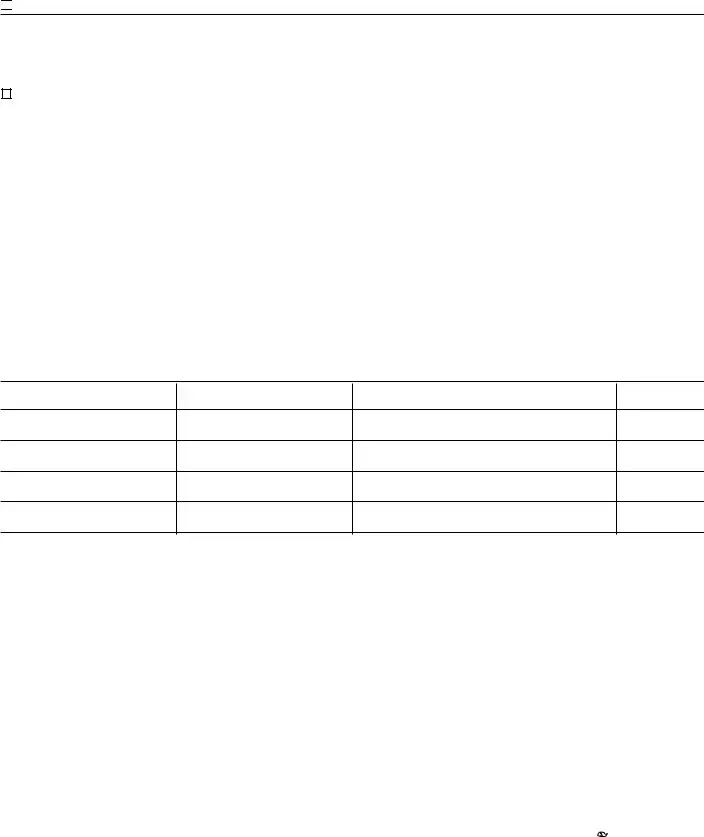

F If the power of attorney is granted to a person other than an attorney, certified public accountant, public accountant or enrolled agent, the taxpayer(s) signature must be witnessed or notarized below.

The person(s) signing as or for the taxpayer(s) (check and complete one):

D

is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

Signature of witness |

Date |

|

|

Signature of witness |

Date |

|

|

D appeared this day before a notary public and acknowledged this power of attorney as a voluntary act and deed. |

|

|

|

Signature of notary |

Date |

|

|

Part 2. Declaration of Representative. All representatives must complete this section.

I declare that I am not currently under suspension or disbarment from practice within the Commonwealth or in any jurisdiction, that I am aware of regula- tions governing the practice of attorneys, certified public accountants, public accountants, enrolled agents and others, and that I am one of the following:

1a member in good standing of the bar of the highest court of the jurisdiction shown below;

2duly qualified to practice as a certified public accountant or public accountant in the jurisdiction shown below;

3enrolled as an agent under the requirements of Treasury Department Circular No. 230;

4a bona fide officer of the taxpayer organization or principal reporting corporation;

5a

6a member of the taxpayer’s immediate family (spouse, parent, child or sibling);

7a fiduciary for the taxpayer;

8other (attach statement)

and that I am authorized to represent the taxpayer identified in Part 1 for the tax matters specified there.

Designation (insert appropriate

number from above list)

Jurisdiction (state, etc.)

or enrollment card number

Signature

Date

Made fillable by FormsPal.

printed on recycled paper

printed on recycled paper

Form

General Information

To protect the confidentiality of tax records, Massachusetts law generally prohibits the Department of Revenue from disclosing information contained in tax returns or other documents filed with it to persons other than the tax- payer or the taxpayer’s representative. For your protection, the Department requires that you file a power of attorney before it will release tax information to your representative. The power of attorney will also allow your represen- tative to act on your behalf to the extent you indicate. Use Form

You may use Form

For certain corporate excise matters under MGL ch 63. By executing this agreement an officer of a principal reporting corporation filing under MGL ch 63, § 32B represents that the principal reporting corporation is authorized to execute this agreement as agent for all corporations that par- ticipated in, or were required to participate in, such filing for any component of the corporate excise reported or required to be reported under any sec- tion of MGL ch 63 by any such corporation whether relating to the income measure,

A principal reporting corporation acts on behalf of all corporations that partic- ipated in, or were required to participate in, a filing under MGL ch 63, § 32B, as stated in the preceding paragraph. Consequently, in the case of such a filing by a principal reporting corporation, the references in this agreement to “taxpayer(s)” shall include all such corporations.

Filing the Power of Attorney. You must file the original, a photocopy or facsimile transmission (fax) of the power of attorney with each DOR office in which your representative is to represent you. You do not have to file another copy with other DOR officers or counsel who later have the matter under consideration unless you are specifically asked to provide an addi- tional copy.

Revoking a Power of Attorney. If you previously filed a power of attorney and you want to revoke it, you may use Form

If you want to revoke a power of attorney without executing a new one, send a signed statement to each office of DOR in which you filed the earlier power of attorney you are now revoking. List in this statement the name and address of each representative whose authority is being revoked.

How to Complete Form

Part 1. Power of Attorney

A. Taxpayer’s name, identification number and address.

a.For individuals.Enter you name, social security number and address in the space provided. If joint returns involved, and you and your spouse are designating the same representative(s), also enter your spouse’s name and social security number and your spouse’s address (if different).

b.For a corporation, partnership or association.Enter the name, federal identification number and business address. If the Power of Attorney for a partnership will be used in a tax matter in which the name and social secu- rity number of each partner have not previously been sent to DOR, list the name and social security number of each partner in the available space at the end of the form or on an attached sheet.

c. For a principal reporting corporation. Enter the name, federal identifi- cation number and business address of the principal reporting corporation.

d. For a trust. Enter the name, title and address of the fiduciary, and the name and federal identification number of the trust.

e. For an estate. Enter the name, title and address of the decedent’s per- sonal representative, and the name and identification number of the estate. The identification number for an estate is the decedent’s social security number and includes the federal identification number if the estate has one.

B.Appointee(s) and tax matters and years or periods.Enter the name(s), address(es) and telephone number(s) of the individual(s) you appoint. Your representative must be an individual and may not be an organization, firm or partnership.

Consider each tax imposed by the Commonwealth for each tax period as a separate tax matter. In the columns provided, clearly identify the type(s) of tax(es) and the year(s) or period(s) for which the power is granted. You may list any number of years or periods and types of taxes on the same power of attorney. If the matter relates to estate tax, enter the date of the taxpayer’s death instead of the year or period.

If the power of attorney will be used in connection with a penalty that is not related to a particular tax type, such as personal income or corporate, enter the section of the General Laws which authorizes the penalty in the “type of tax” column.

C. Powers granted by Form

If you do not want your representative to be able to perform any of these or other specific acts, or if you want to give your representative the power to delegate authority or substitute another representative, insert language ex- cluding or adding these acts in the blank space provided.

D. Where you want copies to be sent. The Department of Revenue rou- tinely sends originals of all notices to the taxpayer. You may also have copies of all notices and all other written communications sent to your rep- resentative. Please check box 1 if you want copies of all notices or all com- munications sent to the first appointee named at the top of the form. Check box 2 if you want copies sent to one of your other appointees. In this case, list the name of the appointee.

E. Signature of taxpayer(s). For individuals: If a joint return is involved and both spouses will be represented by the same individual(s), both must sign the power of attorney unless one authorizes the other (in writing) to sign for both. In that case, attach a copy of the authorization. However, if the spouses are to be represented by different individuals, each may execute a power of attorney.

For a partnership: All partners must sign unless one partner is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if under state law the partner has authority to bind the partnership.

For a corporation or association: An officer having authority to bind the en- tity must sign.

For a principal reporting corporation: An officer having authority to bind the principal reporting corporation of a combined group.

If you are signing the power of attorney for a taxpayer who is not an indi- vidual, such as a corporation or trust, please type or print your name on the line below the signature line at the bottom of the form.

F. Notarizing or witnessing the power of attorney. A notary public or two individuals with no stake in the tax matter must witness a power of at- torney unless it is granted to an attorney, certified public accountant, public accountant or enrolled agent.

Part 2. Declaration of Representative

Your representative must complete Part 2 to make a declaration containing the following:

1.A statement that the representative is authorized to represent you as a certified public accountant, public accountant, attorney, enrolled agent, member of your immediate family, etc. If entering “eight” in the “designation” column, attach a statement indicating your relationship to the taxpayer.

2.The jurisdiction recognizing the representative, if applicable. For an attor- ney, certified public accountant or public accountant: Enter in the “jurisdic- tion” column the name of the state, possession, territory, commonwealth or District of Columbia that has granted the declared professional recogni- tion. For an enrolled agent: Enter the enrollment card number in the “juris- diction” column.

3.The signature of the representative and the date signed.

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Form 2848, known as Power of Attorney and Declaration of Representative, allows individuals to authorize someone to represent them before the IRS. |

| Eligibility | Any taxpayer who needs assistance with tax matters can use this form to designate a representative. This could be a lawyer, CPA, or other authorized individual. |

| State-Specific Needs | In addition to the IRS Form 2848, some states may have their own Power of Attorney forms. For instance, California’s Form FTB 3520 allows for tax representation under the California Revenue and Taxation Code. |

| Revocation | A taxpayer can revoke the Power of Attorney at any time by submitting a written statement to the IRS, ensuring that no further actions are taken by the representative. |

| Representation Scope | The form can grant broad access to a representative, allowing them to handle various tax matters or can be limited to specific issues or forms by the taxpayer’s choice. |

When preparing to fill out the IRS Form 2848, Power of Attorney and Declaration of Representative, it is essential to gather your information and any necessary documents beforehand. This ensures a smoother process and can help avoid potential issues. After submitting the completed form, the IRS will process it and recognize the designated representative to act on your behalf regarding tax matters.

After submission, monitor for communication from the IRS. This includes confirmation that the power of attorney has been accepted and any further actions required on your part. Maintaining open lines of communication with your representative is also highly advisable throughout the process.

What is the IRS Form 2848?

IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, allows you to authorize someone to represent you before the IRS. This person can be an attorney, a certified public accountant, or an enrolled agent. By filling out this form, you empower them to handle your tax matters, communicate with the IRS, and receive information on your behalf.

Who can I appoint as my representative on Form 2848?

You can appoint an individual or individuals to represent you, including attorneys, CPAs, or enrolled agents. However, each representative must have a valid PTIN (Preparer Tax Identification Number) or an active enrollment status with the IRS. Be sure to verify that your chosen representative meets these criteria before submitting the form.

How do I fill out Form 2848 correctly?

To complete Form 2848, provide your name, address, and Social Security Number (or Employer Identification Number). Next, list the representative's name, address, and PTIN or CAF (Centralized Authorization File) number. Finally, specify the tax matters for which you’re granting authority and sign the form at the bottom. Make sure all information is accurate to avoid any delays or issues.

How long is the authorization valid?

The authorization granted by Form 2848 generally remains in effect until you revoke it, withdraw it, or when the representative is no longer able to act on your behalf. Additionally, the IRS retains the right to revoke any authorization if deemed necessary. You may also state a specific expiration date if you wish to limit the duration of the authorization.

Where do I send Form 2848?

Form 2848 can be submitted to the IRS by mailing it to the appropriate address indicated in the instructions of the form. Alternatively, you may fax the completed form to the IRS, depending on your specific situation. Be sure to check the latest IRS guidelines to confirm you are sending it to the correct location.

Can I revoke a previously granted Power of Attorney?

Yes, you can revoke a Power of Attorney at any time. To do so, you must submit a written statement to the IRS that clearly indicates your intent to revoke the previous Form 2848. You should also provide a copy of the previous authorization for reference. Keeping a record of your revocation is important for your own records.

Can I submit Form 2848 electronically?

Currently, Form 2848 is not eligible for electronic submission directly to the IRS. It must be printed and mailed or faxed. However, if you are working with a tax professional, they may be able to submit the form on your behalf using their own processes. Always confirm with your representative if additional steps are necessary.

Inaccurate information: Many individuals mistakenly provide incorrect personal information, such as Social Security numbers, addresses, or dates of birth. This can lead to the rejection of the form or delays in processing.

Omitting signatures: Some people fail to sign the form. Without the necessary signatures, the document is considered incomplete and cannot be processed by the IRS.

Choosing the wrong type of Power of Attorney: It's crucial to select the appropriate type of authority. Many applicants do not clearly understand the differences between limited and unlimited powers, leading to potential issues in representation.

Incorrectly designating the representative: Appointing a representative who does not meet the IRS qualifications is a common mistake. Make sure the chosen person is eligible and capable of handling the tax matters effectively.

The IRS Form 2848, known as the Power of Attorney and Declaration of Representative, allows individuals to designate a representative to handle their tax matters. While Form 2848 is essential for authorizing someone to act on your behalf, several other forms and documents often accompany it to streamline the process and ensure comprehensive representation. Below is a list of such documents, each playing a crucial role in managing tax-related matters.

Understanding these forms can significantly enhance communication with the IRS and facilitate efficient resolution of tax issues. Being prepared with the appropriate documentation empowers individuals to navigate their tax obligations effectively.

The IRS Form 8821, Tax Information Authorization, allows taxpayers to authorize others to receive confidential tax information. Unlike the Form 2848, which also grants power of attorney, Form 8821 does not permit the designated individual to represent the taxpayer before the IRS. Instead, it serves primarily to allow third parties, such as accountants or tax preparers, to obtain information about the taxpayer’s tax accounts, facilitating communication with the IRS without granting full decision-making capabilities.

Another document to consider is the IRS Form 4506, Request for Copy of Tax Return. While this form does not serve as a power of attorney or information authorization, it allows taxpayers to request copies of their past tax returns or other tax documents directly from the IRS. This form is useful for those who need to provide proof of income or tax filings for various purposes, including loan applications or audits, but does not grant authority to another party to act on the taxpayer's behalf.

Form 1040-X, Amended U.S. Individual Income Tax Return, is another related document, but it serves a different purpose. Taxpayers can use this form to correct errors on their original tax returns. While it does not provide anyone with the authority to act for the taxpayer, submitting a 1040-X may often require the taxpayer's representative to communicate with the IRS, especially if adjustments or clarifications are needed after the amendment.

Form 2848 is also comparable to the IRS Form 9465, Installment Agreement Request, which allows taxpayers to set up a payment plan for any taxes owed. This form does not provide authority to others but is an important document for those facing financial difficulties. It facilitates tax compliance by enabling taxpayers to manage their payments over time while addressing their tax liabilities.

Another similar document is the IRS Form 8971, Information Regarding Beneficiaries Acquiring Property from a Decedent. This form requires executors of estates to provide information to beneficiaries about the property being transferred. While Form 8971 primarily deals with estate taxes and property transfers, it shares a commonality with Form 2848 in terms of being a formal document that outlines specific authorizations and information transmissions between parties.

Lastly, the IRS Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return, is significant for estate tax purposes. This form requires detailed reporting of a deceased person's estate and often involves third-party representation. Similar to Form 2848, it necessitates clear authorization and representations regarding estate financial matters, allowing executors to act on behalf of beneficiaries in estate tax matters but differs in its legal focus and requirements.

When filling out the Tax POA Form 2848, it’s important to get it right. Here’s a list to help you navigate the process.

By following these guidelines, the process of filling out Form 2848 can go more smoothly. Always double-check your information to avoid any delays in handling your tax matters.

Many people have misconceptions about the Tax Power of Attorney (POA) form, known as Form 2848. Here are ten common misunderstandings:

This is not true. Form 2848 only allows specific powers related to tax matters, such as signing documents or handling IRS communications on your behalf.

While the form allows someone to represent you, it does not protect you from audits or guarantee favorable outcomes during an audit.

You only need to file Form 2848 when you want to designate a representative. It does not need to be submitted annually unless you want to change representatives.

Form 2848 is limited to tax-related matters. Your representative cannot make broader financial decisions without separate authorization.

You can revoke Form 2848 at any time. Simply submit a written notice to the IRS stating that you wish to withdraw the power granted.

Currently, Form 2848 must be printed and mailed to the IRS. Electronic submission is not available unless you use specific tax software that supports such a feature.

Anyone, including individuals, can file Form 2848. It’s not limited to tax professionals.

This form can also be used by corporations and entities to appoint a representative for tax matters.

A Form 2848 remains valid until the IRS receives a revocation or the representative no longer meets the qualifications.

This form does not transfer your rights to any refunds. Your representative can help you claim refunds, but they do not get them on your behalf without proper authorization.

When considering the Tax Power of Attorney (POA) form, known as Form 2848, there are several important points to keep in mind. This document allows individuals to authorize someone else to represent them before the Internal Revenue Service (IRS). Below are key takeaways to help you understand this process better.

Being informed about these aspects of the Tax POA Form 2848 can help you navigate the complexities of tax representation more effectively. Always consider seeking additional guidance if you have further questions or uncertainties.