The Tax Power of Attorney Legal Form, commonly referred to as the Tax POA LGL 001 form, serves as a vital tool for individuals seeking to designate an authorized representative to act on their behalf in matters related to federal tax obligations. This form allows taxpayers to grant specific powers to another person, such as an attorney or a tax professional, enabling them to handle communications with the Internal Revenue Service (IRS). When completing this form, individuals must be mindful of the various sections, which outline the specific powers being granted and the duration of authority. Additionally, the form requires clear identification of both the taxpayer and the appointed representative, minimizing the potential for confusion and ensuring that all parties involved understand their roles and responsibilities. It is essential for taxpayers to consider the implications of granting such authority, including the access their representative will have to sensitive financial information. By properly utilizing the Tax POA LGL 001 form, taxpayers can ensure that their interests are represented accurately and effectively in addressing their tax matters.

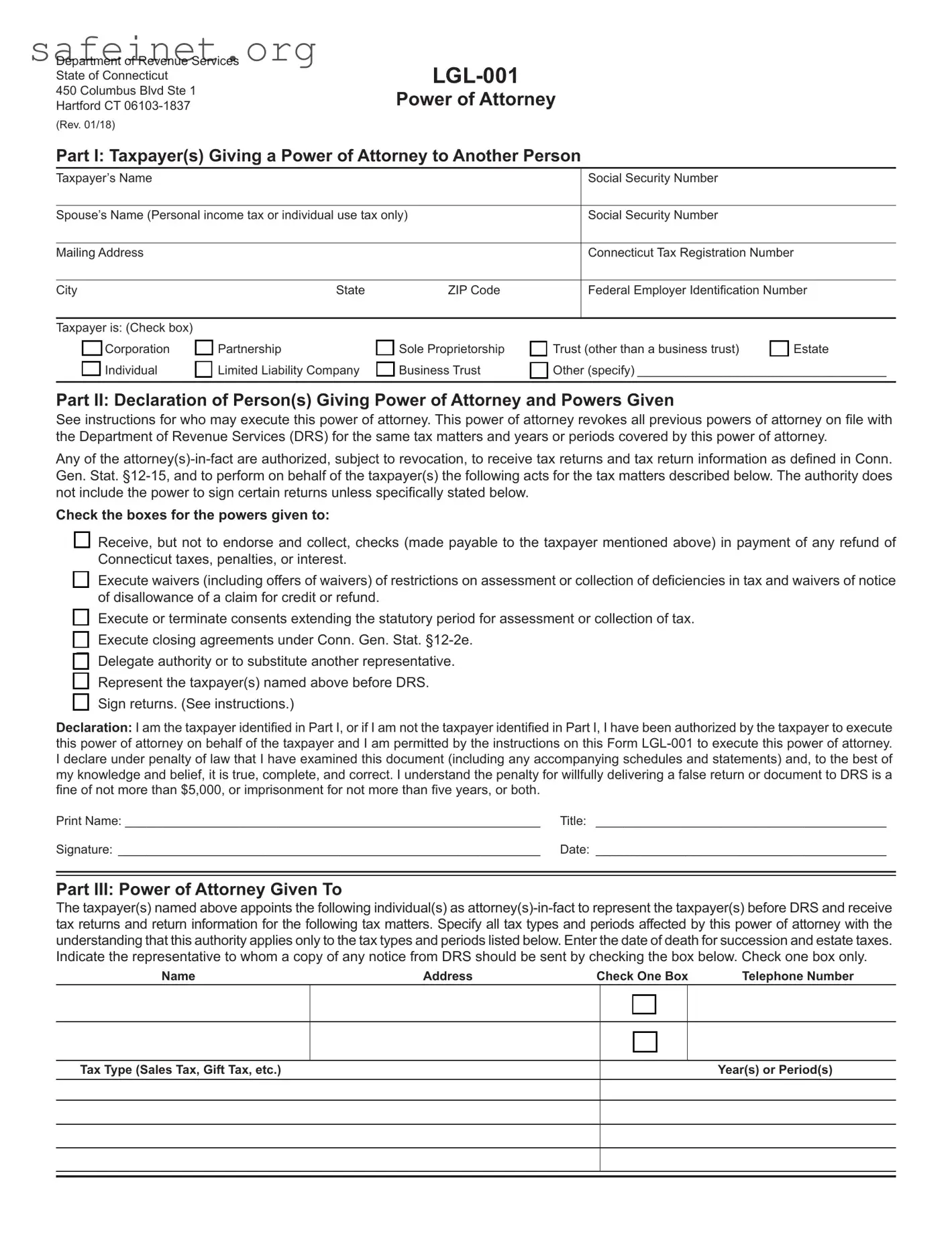

Department of Revenue Services State of Connecticut

450 Columbus Blvd Ste 1 Hartford CT

(Rev. 01/18)

Power of Attorney

Part I: Taxpayer(s) Giving a Power of Attorney to Another Person

Taxpayer’s Name |

|

|

Social Security Number |

|

|

|

|

Spouse’s Name (Personal income tax or individual use tax only) |

|

Social Security Number |

|

|

|

|

|

Mailing Address |

|

|

Connecticut Tax Registration Number |

|

|

|

|

City |

State |

ZIP Code |

Federal Employer Identification Number |

|

|

|

|

Taxpayer is: (Check box) |

|

|

|

|

Corporation |

Partnership |

Sole Proprietorship |

Trust (other than a business trust) |

Estate |

Individual |

Limited Liability Company |

Business Trust |

Other (specify) ____________________________________ |

|

|

|

|

|

|

Part II: Declaration of Person(s) Giving Power of Attorney and Powers Given

See instructions for who may execute this power of attorney. This power of attorney revokes all previous powers of attorney on file with the Department of Revenue Services (DRS) for the same tax matters and years or periods covered by this power of attorney.

Any of the

Check the boxes for the powers given to:

Receive, but not to endorse and collect, checks (made payable to the taxpayer mentioned above) in payment of any refund of Connecticut taxes, penalties, or interest.

Execute waivers (including offers of waivers) of restrictions on assessment or collection of deficiencies in tax and waivers of notice of disallowance of a claim for credit or refund.

Execute or terminate consents extending the statutory period for assessment or collection of tax. Execute closing agreements under Conn. Gen. Stat.

Delegate authority or to substitute another representative. Represent the taxpayer(s) named above before DRS. Sign returns. (See instructions.)

Declaration: I am the taxpayer identified in Part I, or if I am not the taxpayer identified in Part I, I have been authorized by the taxpayer to execute this power of attorney on behalf of the taxpayer and I am permitted by the instructions on this Form

Print Name: ____________________________________________________________ |

Title: __________________________________________ |

Signature: _____________________________________________________________ |

Date: __________________________________________ |

Part III: Power of Attorney Given To

The taxpayer(s) named above appoints the following individual(s) as

Name |

Address |

Check One Box |

|

Telephone Number |

||

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

Tax Type (Sales Tax, Gift Tax, etc.) |

|

|

|

|

|

Year(s) or Period(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Instructions

Use

Connecticut law stipulates that all official mailings will be sent to the taxpayer of record at the address on file with DRS. As a matter of policy, DRS also provides taxpayers with the right to have a copy of any notice sent to its counsel or other qualified representative who has properly executed and filed this power of attorney with DRS for the type of tax and tax period that is the subject of the notice. This power of attorney does not change the requirement that DRS send all official mailings directly to the taxpayer.

Part I: Taxpayer(s) Giving a Power of Attorney to Another Person

Provide the taxpayer’s name and address and either your Social Security Number (SSN) or Connecticut Tax Registration Number and Federal Employer Identification Number. If you are a sole proprietor, enter your name and SSN. Do not enter your trade name. Do not use your representative’s address as your own.

Your spouse’s name is not required except for joint personal income tax or individual use tax returns.

If you are filing a joint personal income tax return and you and your spouse have the same representative(s), include your spouse’s name and SSN in the space provided. Otherwise, each spouse must file a separate

Check the box that describes the taxpayer.

Part II: Declaration of the Person Giving Power of Attorney And Powers Given

Any person giving a power of attorney to another person(s) must sign this declaration and must check the box for each act being granted to the

Who may execute this power of attorney?

Any individual if the request is for an income tax return filed by that individual (or filed by that individual and his or her spouse if the request is for a joint income tax return);

Conn. Agencies Regs.

A limited liability company (LLC) member if the taxpayer is an LLC and has no manager or a manager if the taxpayer is an LLC and has managers

The sole proprietor if the taxpayer is a sole proprietorship;

A general partner if the taxpayer is a partnership or a limited partnership;

The administrator or executor if the taxpayer is an estate;

The trustee if the taxpayer is a trust;

If the taxpayer is a corporation, a principal officer or corporate officer (who has legal authority to bind the corporation), any

person who is designated by the board of directors or other governing body of the corporation, any officer or employee of the corporation upon written request signed by a principal officer of the corporation and attested to by the secretary or other officer of the corporation, or any other person who is authorized to receive or inspect the corporation’s return or return information under I.R.C. §6103(e)(1)(D);

The successor, receiver, guarantor, or any assignee of the taxpayer; or

The authorized representative of any of the above.

Part III: Power of Attorney Given To

Provide the name, address, and telephone number of the person(s) designated by you to be your

Enter the tax type and the tax periods or tax years that are the subject of this power of attorney. Be specific about the type of tax at issue (refer to the following examples):

Withholding tax;

Income tax;

Sales and use taxes;

Corporation business tax;

Admissions and dues tax;

Estate tax;

Gift tax;

Motor vehicle fuels tax;

Gross earnings tax (petroleum, gas, hospital, community antenna);

Cigarette tax distributor; and

Individual use tax.

The terms years and periods can indicate various time frames.

A tax year may be a calendar year of 1/1/06 through 12/31/06 or a fiscal year of 7/1/06 through 6/30/07 for corporation tax. A tax period may have one or more monthly or quarterly periods.

Example: A sales and use tax period of 1/1/04 through 12/31/06 may contain 36 monthly or 12 quarterly periods.

Indicate the tax year(s) or tax period(s) to be covered by the power of attorney.

Where to File

Do not send an

Mail, fax, or deliver

| Fact Name | Details |

|---|---|

| Purpose | The Tax POA LGL 001 form is used to authorize an individual to represent another person in tax matters. |

| Governing Law | In many states, the Tax POA form is governed by the state's tax code and regulations. |

| Signatures Required | The form typically requires signatures from both the taxpayer and the representative. |

| Filing Process | Once completed, the form must be filed with the state tax authority to be effective. |

| Duration of Authority | The authority granted by this form usually remains in effect until revoked or the tax matter concludes. |

| Revocation | Taxpayers can revoke the authority at any time by submitting a revocation notice to the relevant tax authority. |

| State Variations | Different states may have their own versions of the Tax POA form, with specific requirements outlined in their taxation laws. |

| Representation Scope | The form typically specifies the extent of authority and areas of tax matters the representative may cover. |

| Importance of Accuracy | Ensuring that all information is accurate and complete on the form is crucial to avoid delays in processing. |

Filling out the Tax POA lgl 001 form is an important step in designating someone to act on your behalf regarding tax matters. Carefully following the instructions ensures that the form is submitted correctly and that your representative can help you efficiently.

Once you have submitted the form, you should be on the lookout for any confirmation or communication from the tax authority. This may take some time, but following up can help ensure everything is processed smoothly.

What is the Tax POA lgl 001 form?

The Tax Power of Attorney (POA) lgl 001 form is a legal document that allows a designated person, often referred to as an agent or representative, to act on behalf of another individual regarding tax matters. This form grants authority to the agent to receive information from the IRS, file tax returns, and handle any tax-related issues that may arise. It streamlines communication between taxpayers and the IRS, ensuring that the appointed individual has the ability to manage specific tax responsibilities effectively.

Who should consider using the Tax POA lgl 001 form?

This form is particularly useful for individuals who may find it challenging to manage their tax affairs due to various reasons. For instance, people with complex tax situations, those who are out of the country, or individuals who simply prefer having a trusted friend, family member, or professional to handle their taxes could benefit from using the Tax POA lgl 001 form. It ensures that the appointed representative can act according to the taxpayer’s best interests and provide efficient management of tax responsibilities.

How do I fill out the Tax POA lgl 001 form?

Filling out the Tax POA lgl 001 form involves a few clear steps. First, provide your personal details, including your name, address, and taxpayer identification number. Next, specify the information regarding the individual you are appointing as your representative, including their name and contact information. It’s crucial to outline the extent of authority you are granting—whether it is for all tax matters or limited to specific issues. Finally, both you and your designated representative will need to sign and date the form. Make sure to keep a copy for your records after submitting it to the IRS.

How long is the Tax POA lgl 001 form valid?

The validity of the Tax POA lgl 001 form generally remains in effect as long as you have not revoked it or until the representative ceases to act on your behalf due to another reason, such as passing away or ceasing to represent you. Remember, you can also revoke a Tax POA at any time by notifying the IRS and submitting a revocation statement. It’s important to review and update this form when your life circumstances change or when you wish to designate a different representative.

Inaccurate Information: One common mistake is providing incorrect or incomplete information. Ensure that your name, address, and taxpayer identification number are accurate. Even minor discrepancies can lead to delays in processing.

Neglecting Signatures: Signatures are essential. Some individuals forget to sign the form or fail to provide the date. Without a signature, the form is invalid and may not be accepted by the IRS.

Incorrect Power of Attorney Designation: It is important to specify who you are granting power of attorney. Mistakes can occur in selecting the right representative or not including the necessary details about the individual authorized to act on your behalf.

Not Keeping Copies: After submitting the form, it is vital to retain a copy for your records. This can prevent confusion later regarding the powers granted and confirm that your submission was made.

The Tax Power of Attorney (POA) form, often referred to as Tax POA lgl 001, allows individuals to designate someone else to handle their tax matters with the Internal Revenue Service (IRS). Several other forms and documents commonly accompany this POA form, enhancing its effectiveness or fulfilling specific IRS requirements. Here is a list of such documents:

Utilizing these forms in conjunction with the Tax POA lgl 001 provides comprehensive support in managing tax-related responsibilities. Each document serves a specific purpose that enhances communication and authority between taxpayers and their representatives.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is a widely recognized document that allows taxpayers to appoint an individual to represent them before the IRS. Similar to the Tax POA lgl 001, this form grants authority to the representative to receive confidential tax information, enabling them to act on behalf of the taxpayer in communications with the IRS. The standardized format and specific instructions help ensure clarity in what powers are granted to the representative.

Another document related to this process is the IRS Form 8821, Tax Information Authorization. This form is used for authorizing an individual to receive tax information, but unlike the Tax POA lgl 001, it does not allow the designee to represent the taxpayer before the IRS. Instead, it focuses solely on granting access to information, making it a more limited option for those who need assistance without needing full representation.

The Durable Power of Attorney form extends beyond the tax realm, allowing individuals to grant legal authority to another person to manage their affairs should they become incapacitated. This document shares a similar intent with the Tax POA lgl 001 in that it involves the delegation of authority, but it covers a broader range of personal and financial matters rather than being restricted to tax issues alone.

The Limited Power of Attorney, often used in real estate transactions, allows individuals to give specific powers to another person for a defined timeframe or task. This document is akin to the Tax POA lgl 001 as both are intended to grant authority, but the Limited Power of Attorney focuses on particular transactions while the Tax POA lgl 001 centers on tax-related matters, maintaining a narrower scope.

The Federal Employer Identification Number (EIN) application, Form SS-4, requires entities to authorize individuals or representatives to act on their behalf. Like the Tax POA lgl 001, it allows for the designation of a point person who can handle specific tasks regarding federal tax obligations. Both forms facilitate efficient communication with the IRS, streamlining processes for the taxpayer or business entity.

The Health Care Power of Attorney form shares a similar framework in that it designates a representative to make health-related decisions on someone’s behalf. Although focused on medical decisions, like the Tax POA lgl 001, it establishes trust in the appointed representative to act according to the wishes of the individual, showing an excellent parallel in the nature of personal agency in both tax and healthcare contexts.

The Non-Disclosure Agreement (NDA), while primarily about confidentiality, can sometimes intersect with tax-related matters, particularly when discussing financial information. Similar to the Tax POA lgl 001, which protects and controls access to sensitive information, an NDA provides a legal framework for safeguarding proprietary information shared between parties, ensuring that trust is maintained during financial discussions or negotiations.

The Revocable Living Trust allows individuals to designate a trustee to manage their assets, including tax obligations, during their lifetime or after death. Much like the Tax POA lgl 001, it enables the appointed person to act in the best interests of the individual, ensuring that tax matters are handled efficiently and in accordance with the individual's wishes.

The General Power of Attorney form permits individuals to grant comprehensive authority to another person to manage a broad spectrum of affairs, including financial and tax-related matters. This document aligns with the Tax POA lgl 001 in terms of assigning power but provides a significantly broader scope of authority, allowing the designated agent to make decisions across various aspects of the principal's life.

Lastly, the Form 4506-T, Request for Transcript of Tax Return, can be submitted by a designated representative to obtain tax return information. This form is analogous to the Tax POA lgl 001 in that it facilitates the access of tax information, but unlike the POA forms, it does not authorize representation. Both forms support taxpayers' needs for information but differ in the level of authority granted to the representatives.

When filling out the Tax POA (Power of Attorney) lgl 001 form, there are some important things to keep in mind. Here is a helpful list of dos and don’ts to ensure the process goes smoothly.

Following these guidelines will help in avoiding common pitfalls and ensure that the form is completed correctly.

The Tax Power of Attorney (POA) form, specifically the legal form lgl 001, is often surrounded by misunderstandings. Below are several common misconceptions regarding this form, along with clarifications to provide a more accurate understanding.

This is not true. While individuals with complicated tax affairs benefit from this form, it is available for anyone needing assistance in managing their tax responsibilities.

In reality, the Tax POA allows designated individuals to handle specific tasks on your behalf, but you retain ultimate control over your affairs.

This is incorrect. The Tax POA can be revoked at any time, provided you notify the designated representative and the relevant tax authorities.

This form is not limited to instances of incapacity; individuals can authorize others to act on their behalf for convenience, regardless of their health status.

While the form itself is essential, you may need to supply supplementary documents depending on the individual circumstances involved in the tax matters.

This is not accurate. While attorneys are commonly appointed, you can choose anyone you trust to represent you, including family members or friends.

Using the Tax POA lgl 001 form effectively requires attention to detail and understanding of its purpose. Below are key takeaways to consider: