The IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, is an essential tool for taxpayers who need assistance in managing their tax matters. This form allows individuals to designate an authorized representative, such as an attorney, accountant, or tax professional, to act on their behalf when dealing with the IRS. By completing Form 2848, taxpayers grant their representatives the authority to receive and inspect their tax information, communicate with the IRS, and represent them during audits or appeals. It also specifies the types of tax matters the representative can address, ensuring that all necessary permissions are clearly outlined. Understanding how to fill out this form correctly and the implications of granting power of attorney is critical, as improper use can lead to complications in tax representation. Consequently, using Form 2848 can ensure that your tax concerns are handled effectively and that you have the right support through potentially complex situations.

REVENUe ____________________

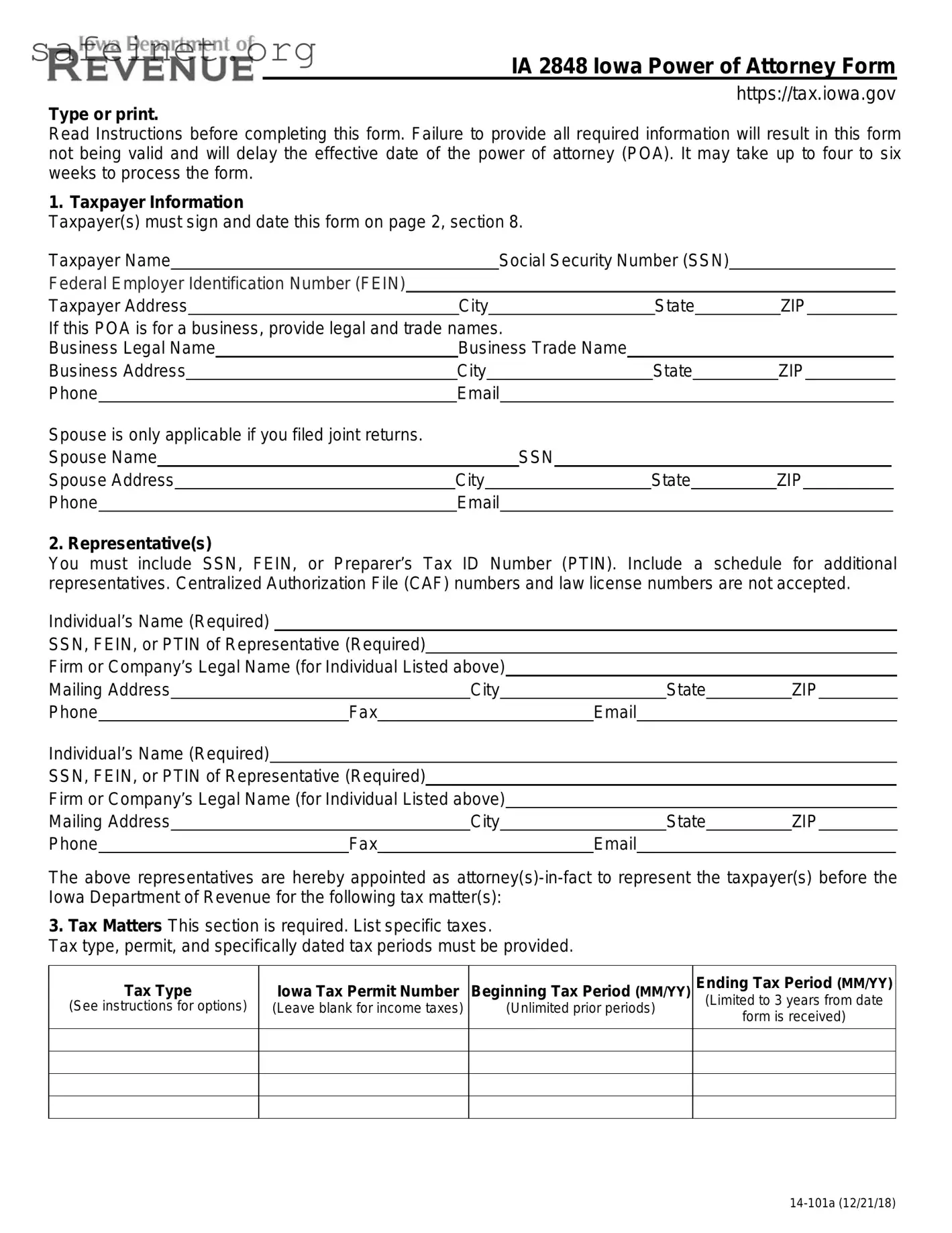

IA 2848 Iowa Power of Attorney Form

https://tax.iowa.gov

Type or print.

Read Instructions before completing this form. Failure to provide all required information will result in this form not being valid and will delay the effective date of the power of attorney (POA). It may take up to four to six weeks to process the form.

1. Taxpayer Information

Taxpayer(s) must sign and date this form on page 2, section 8.

Taxpayer Name |

|

|

Social Security Number (SSN) |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Federal Employer Identification Number (FEIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Taxpayer Address |

City |

State |

|

ZIP |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

If this POA is for a business, provide legal and trade names. |

|

|

|

|

|

|

|||||||||||||

Business Legal Name |

Business Trade Name |

|

|

|

|

|

|

||||||||||||

Business Address |

|

City |

|

State |

|

ZIP |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Phone |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Spouse is only applicable if you filed joint returns. |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Spouse Name |

|

|

SSN |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Spouse Address |

City |

State |

|

ZIP |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. Representative(s)

You must include SSN, FEIN, or Preparer’s Tax ID Number (PTIN). Include a schedule for additional representatives. Centralized Authorization File (CAF) numbers and law license numbers are not accepted.

Individual’s Name (Required)

SSN, FEIN, or PTIN of Representative (Required)

Firm or Company’s Legal Name (for Individual Listed above)

Mailing Address |

|

|

|

City |

|

|

State |

ZIP |

||||

Phone |

|

Fax |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Individual’s Name (Required)

SSN, FEIN, or PTIN of Representative (Required)

Firm or Company’s Legal Name (for Individual Listed above)

Mailing Address |

|

|

|

City |

|

|

State |

ZIP |

||||

Phone |

|

Fax |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

The above representatives are hereby appointed as

3.Tax Matters This section is required. List specific taxes.

Tax type, permit, and specifically dated tax periods must be provided.

Tax Type |

Iowa Tax Permit Number |

Beginning Tax Period (MM/YY) |

(See instructions for options) |

(Leave blank for income taxes) |

(Unlimited prior periods) |

|

|

|

Ending Tax Period (MM/YY) (Limited to 3 years from date form is received)

IA 2848 Iowa Power of Attorney Form, page 2

4.Acts Authorized (Do not name additional representatives in this section.)

Representatives are authorized to receive and inspect confidential tax information and to perform any and all acts with respect to the tax matters described in section 3. For example, the representative may negotiate, sign any agreements, consents, or other documents, and represent the taxpayer(s) in any informal and formal proceeding involving the Department. See Instructions for full list of authorized activities. The authority does not include the power to receive refund checks, unless specifically added in section 5 below. List any specific additions or deletions to the acts otherwise authorized in this power of attorney:

Additions:

Deletions:

5. Receipt of Refund Checks

If you want to authorize a representative named in section 2 to receive, but not to endorse or cash, refund

checks, initial here |

|

and list the name of that representative below. |

Name of representative to receive refund check(s)

6. Notices and Communications

Original notices and other written communications will be sent to you and the taxpayer. A copy will be sent to the first representative listed in section 2.

7. Retention or Revocation of Prior Power(s) of Attorney

The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Iowa Department of Revenue for the same tax matters and tax periods covered by this document.

If you do not want to revoke a prior power of attorney, check here □

You must attach a copy of any power of attorney you want to remain in effect.

8. Signature of Taxpayer(s)

If a tax matter concerns a joint individual income tax return, both spouses are required to sign this form, if represented by the same individual(s).

If signed by a corporate officer, partner, member, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer: I certify that I have the authority to execute this form on behalf of the taxpayer.

If the taxpayer is an entity with more than one owner or member, a second signature of a person authorized to legally bind the entity is required.

If this form is not signed and dated, this power of attorney will not be valid. The form will be returned to you.

Signature ______________________________ |

Date |

____________________________________ |

|

Print Name |

____________________________ |

Title _____________________________________ |

|

Signature ______________________________ |

Date |

____________________________________ |

|

Print Name |

____________________________ |

Title _____________________________________ |

|

Mail to:

Registration Services

Iowa Department of Revenue

PO Box 10470

Des Moines IA

Or fax to:

Purpose of form

Taxpayer information is confidential. The Iowa Department of Revenue will discuss confidential tax information only with the taxpayer, unless the taxpayer has a valid power of attorney form on file with the Department.

A power of attorney is required by the Department when the taxpayer wishes to authorize another person to perform one or more of the following on behalf of the taxpayer:

a. To receive copies of notices or documents sent by the Department, its representatives, or its attorneys.

b. To receive (but not to endorse and collect) checks in payment of any refund of Iowa taxes, penalties, or interest.

c. To request waivers (including offers of waivers) of restrictions on assessment or collection of tax deficiencies and waivers of notice of disallowance of a claim for credit or refund.

d. To request extensions of time for assessment or collection of taxes.

e. To fully represent the taxpayer(s) in any formal or informal meeting with the Department, hearing, determination, final or otherwise, or appeal.

f.To enter into any compromise with the Department.

g.To execute any release from liability required by the Department before divulging otherwise confidential information concerning taxpayer(s).

h.Other acts as expressly stipulated in writing by the taxpayer.

3.Tax Matters

Tax type options

Enter tax type in section 3 and include beginning and ending dates for each. Valid tax types are: Individual Income, Partnership, Corporation, Sales, Use, Withholding, Franchise, Inheritance, Fiduciary, or Other (specify).

Tax periods

Specific tax periods must be identified. Each tax period must be separately stated.

Beginning tax period

An unlimited number of prior tax periods is allowed.

Ending tax period

An

7.Retention / Revocation of prior Power(s) of Attorney Canceling a power of attorney

A power of attorney may be revoked by a taxpayer at any time by filing a statement of revocation with the Department. The statement must indicate that the authority of the previous power of attorney is revoked and must be signed and dated by the taxpayer. Also, the name and address of each representative whose authority is revoked must be listed or a copy of the power of attorney must be included. Revocation of the authority to represent the taxpayer before the Department will be effective on the date received by the Department.

IA 2848 Iowa Power of Attorney Instructions

Submitting a new power of attorney

A new power of attorney for a particular tax type(s) and tax period(s) revokes a prior power of attorney for those tax type(s) and tax period(s), unless the taxpayer indicates on the new power of attorney form that a prior power of attorney is to remain in effect. The effective date of a new power of attorney is the date it is received by the Department.

For a

Withdrawing as a representative

A representative may withdraw from representing a taxpayer by filing a statement with the Department. The statement must be signed and dated by the representative and must identify the name and address of the taxpayer(s) and the matter(s) from which the representative is withdrawing.

8.Signature of Taxpayer(s) Who must sign?

Individual taxpayer. A power of attorney form must be signed by the individual.

Joint returns. If a tax matter concerns a joint individual income tax return, both taxpayers must sign and date.

Corporation. An officer of the corporation having authority to legally bind the corporation must sign the power of attorney form. The corporation must certify that the officer has such authority.

Association. An officer of the association having authority to legally bind the association must sign the power of attorney form. The association must certify that the officer has such authority.

Partnership. A power of attorney must be signed by all partners, or if executed in the name of the partnership, by the partner or partners duly authorized to act for the partnership, who must certify that the partner(s) has such authority.

Federal Power of Attorney

The Federal Power of Attorney form or a Military Power of Attorney is accepted by the Iowa Department of Revenue. To be valid, the federal or military form must include a statement that it is applicable for Iowa purposes at the time it is executed. In the case of a previously executed Federal or Military Power of Attorney subsequently revised to apply for Iowa purposes, it must contain a written statement that indicates it is being submitted for use with State of Iowa forms and the statement needs to be initialed by the taxpayer. Iowa allows married taxpayers to file one Iowa Power of Attorney form on behalf of both spouses. The IRS requires separate Power of Attorney forms for each spouse. If the Federal Power of Attorney is being used for Iowa purposes by married taxpayers, both federal forms must be submitted to Iowa.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 2848, Power of Attorney and Declaration of Representative, allows individuals to designate an attorney-in-fact to represent them before the IRS. |

| Requirements | To complete the form, the taxpayer and the representative must provide identifying information, including names, addresses, and Taxpayer Identification Numbers (TINs). |

| Scope of Authority | Form 2848 grants the designated representative authority over various tax matters, including but not limited to audits, appeals, and claims for refunds. |

| State-Specific Forms | Some states have their own Power of Attorney forms, such as California’s Form FTB 3520 or New York’s Form POA-1, governed by state laws. |

| Signature Requirement | The form requires signatures from both the taxpayer and the appointed representative to be considered valid. |

| Submission | Taxpayers must submit the completed form to the IRS, and it may also be necessary to retain a copy for their records. |

Once you've gathered the necessary information, filling out the IRS Form 2848, also known as the Tax Power of Attorney, becomes straightforward. You'll need to ensure that each section is completed accurately and thoroughly, as this will dictate the authorizations given. Follow the steps below to effectively complete the form.

Following these steps closely will help ensure that the form is completed accurately. After filling out the form, make sure to submit it to the IRS, as specified in their guidelines. This will allow your designated representative to act on your behalf regarding the tax matters you’ve indicated.

What is Form 2848, the Tax Power of Attorney?

Form 2848, the Tax Power of Attorney, allows a taxpayer to authorize another individual to represent them before the IRS. This can include the power to receive confidential tax information, sign documents, and act on behalf of the taxpayer in certain matters. This designation is crucial for those who cannot manage their tax affairs personally.

Who can be appointed as a representative on Form 2848?

The form allows taxpayers to designate an individual, like an attorney, accountant, or any other person, as their representative. The appointee must hold a valid tax identification number and may need to be a professional with tax-related qualifications in some situations. Non-professionals can also be designated if they serve as a trustworthy representative.

How do I complete Form 2848?

To complete Form 2848, taxpayers must fill out their information, including their name, address, and taxpayer identification number. The taxpayer must then list the representative’s information, including their name, address, and preparer tax identification number (PTIN). The form requires signatures from both parties. Make sure all information is accurate to avoid delays.

Do I need to submit Form 2848 each year?

Form 2848 does not need to be submitted annually. Once it is filed and accepted, it remains in effect until the authority is revoked, the taxpayer cancels the appointment, or the IRS determines the representative is no longer eligible. However, it is important to update the form if there are any changes in circumstances or representatives.

How is Form 2848 submitted to the IRS?

Form 2848 can be submitted to the IRS by mailing, faxing, or in some cases, electronically filing it. The appropriate submission method depends on the type of authorization and specific IRS guidelines. Always check the latest instructions provided by the IRS to ensure proper submission and to avoid any processing issues.

Can I revoke a Power of Attorney granted via Form 2848?

Yes, revocation of power granted through Form 2848 is possible. The taxpayer can revoke the authority granted by submitting a written statement indicating the revocation to the IRS. It's essential to also inform the representative of the revocation to prevent any misunderstandings regarding authority.

What if my representative doesn't follow my instructions?

In a situation where a representative does not adhere to the taxpayer’s instructions, the taxpayer retains the right to revoke the Power of Attorney. This should ideally be done in writing. Taxpayers should keep careful records of all communications with their representatives to address potential disputes effectively.

Is there a fee for using Form 2848?

Filing Form 2848 with the IRS does not require a fee. However, if the representative providing assistance is a professional, they may charge for their services per their standard rates. Taxpayers should discuss any potential fees with their representatives upfront to avoid unexpected costs.

Not Specifying the Correct Tax Year(s) - It’s essential to indicate the specific tax years for which the Power of Attorney (POA) is valid. Leaving this section blank can lead to confusion and may limit the representative's authority.

Failing to Sign the Form - A common oversight is forgetting to sign the form. Without a signature, the IRS won't accept the Power of Attorney, rendering it ineffective.

Selecting Incorrect Representation Types - When filling out the form, the individual needs to choose the right type of representation. One should understand the differences between individuals and entities to ensure the right box is checked.

Providing Incomplete Contact Information - It's vital to ensure that all contact information for both the taxpayer and the representative is fully completed. Missing phone numbers or addresses can lead to delays or miscommunications.

Neglecting to Include Additional Representatives - If there are multiple representatives, failing to list them can cause issues. The form allows space for more than one representative, so it’s important to include everyone who will assist in handling the tax matters.

When individuals or businesses are seeking representation in tax matters, particularly when using the Tax POA (Power of Attorney) Form 2848, there are several other documents and forms that may be required or beneficial. Each of these documents serves a specific purpose in the tax process, helping to clarify responsibilities or streamline communication with tax authorities. Below is a list of commonly used forms associated with the Tax POA Form 2848.

Understanding the purpose of these documents can greatly enhance your ability to navigate tax-related issues effectively. By preparing the necessary forms in advance, you can foster open communication with your tax representative and the IRS, ultimately leading to a smoother resolution process.

The IRS Form 2848, officially known as the Power of Attorney and Declaration of Representative, allows an individual to designate another person to act on their behalf in tax matters. This document is similar to many other power of attorney forms used in different contexts. Each serves a specialized purpose but shares the fundamental principle of granting authority to a representative.

One comparable document is the General Power of Attorney (GPOA). This form allows an individual to grant broad powers to another person, typically for financial or legal decisions. Like the Form 2848, it enables the agent to act on behalf of the principal, but the GPOA covers a wide range of issues beyond taxation, including managing bank accounts and executing contracts.

Another similar document is the Durable Power of Attorney. This form remains in effect even if the principal becomes incapacitated. While the Form 2848 is specifically for tax matters, the Durable Power of Attorney can cover various areas, ensuring that decisions can still be made for the individual even when they are unable to do so themselves.

The Medical Power of Attorney is a critical document that grants someone the authority to make healthcare decisions for another person. It differs from the Form 2848 in that its focus is on medical care rather than financial matters. However, both documents emphasize the importance of having a trusted representative to act in the best interest of the principal.

A Limited Power of Attorney is another related document. This form gives an agent limited authority to act for a specific purpose, such as managing property during a specific transaction. Like the Form 2848, the Limited Power of Attorney is often used for specific situations, but its scope is narrower than the general authority of the GPOA.

The Financial Power of Attorney is tailored for financial matters, allowing the agent to manage the principal’s finances, including paying bills and handling investments. This document shares similarities with Form 2848 as both empower someone to act on behalf of another. However, the Financial Power of Attorney does not limit itself to tax issues.

The Will can also be compared to Form 2848, though its purpose is quite different. A will outlines how a person’s assets should be distributed after their death. While the two documents do not serve the same function, they both reflect a desire to have a trusted individual make decisions in accordance with the individual's wishes.

The Trust document is relevant here as well. A Trust allows a person to transfer their assets into a managed account for the benefit of beneficiaries. While Form 2848 is strictly about tax representation, both documents involve a third party managing the affairs of another, albeit in different contexts.

The Sales Agreement, while primarily a contract, can have elements similar to the Form 2848 when it involves appointing an agent to execute specific sales on behalf of an individual. Both require a principal to grant specific authority to the representative, emphasizing trust and reliability in action.

Finally, the Living Will is similar in that it captures a person's wishes regarding healthcare but is focused on end-of-life care decisions. While different in intent and application from Form 2848, both emphasize the importance of having a representative act in alignment with the principal’s wishes, even when specific circumstances arise.

When filling out the Tax Power of Attorney (POA) Form 2848, consider the following dos and don'ts to ensure accuracy and compliance:

Understanding the Tax Power of Attorney (POA) Form 2848 is essential for taxpayers and their representatives. However, several misconceptions can lead to confusion. Below are five common misconceptions explained.

This is not true. While many individuals choose to authorize certified tax professionals, taxpayers can also designate a family member or friend to act on their behalf using Form 2848.

Actually, Form 2848 must be submitted each time there is a change in representative or if the taxpayer requires a new POA for a different tax issue. It is not a permanent authorization.

The authority granted by this form is limited. It specifies the tax matters and tax years covered, meaning representatives can only access the information relevant to those areas.

In reality, the IRS must first acknowledge receipt and accept the form, which can take time. It's important to check in with the IRS to confirm that the form has been processed.

This is incorrect. Taxpayers have the right to revoke a POA at any time by submitting a written notice to the IRS. It's a simple process that provides flexibility in representation.

The IRS Form 2848, also known as the Power of Attorney (POA) form, is an important document for individuals seeking to authorize someone else to represent them before the IRS. Understanding how to fill out and use this form effectively can streamline the process of tax representation. Here are six key takeaways: