The Tax POA gen-58 form is an important document for anyone seeking to authorize another individual to act on their behalf in matters related to tax. This form facilitates communication between the taxpayer and the IRS, allowing a designated representative to receive tax information, make inquiries, and represent the taxpayer during audits or reviews. Completing the form requires specific information, such as the taxpayer’s details, the representative’s information, and the scope of authority granted. It is crucial to ensure that all sections of the form are filled out accurately to avoid delays or issues with the IRS. Additionally, knowing the limitations and responsibilities of both the taxpayer and the representative is essential for a smooth process. This form plays a vital role in managing tax affairs, making it easier for individuals who may not be comfortable navigating tax complexities on their own.

|

Power of Attorney |

|

4 |

|

✖ |

||||

|

and Declaration of Representative |

|

|

|

|

||||

|

|

|

|

|

CLEAR |

||||

|

|

|

|

|

North Carolina Department of Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

P. O. Box 25000, Raleigh, NC |

|

|

|

|

|

|

|

|

|

Fax: |

|

|

|

|

|

|

|

|

I |

Power of Attorney (Please type or print.) |

|

|

|

|

I Part 1. |

|

|

|

|

|

||||

|

|

|

|

|

|

||||

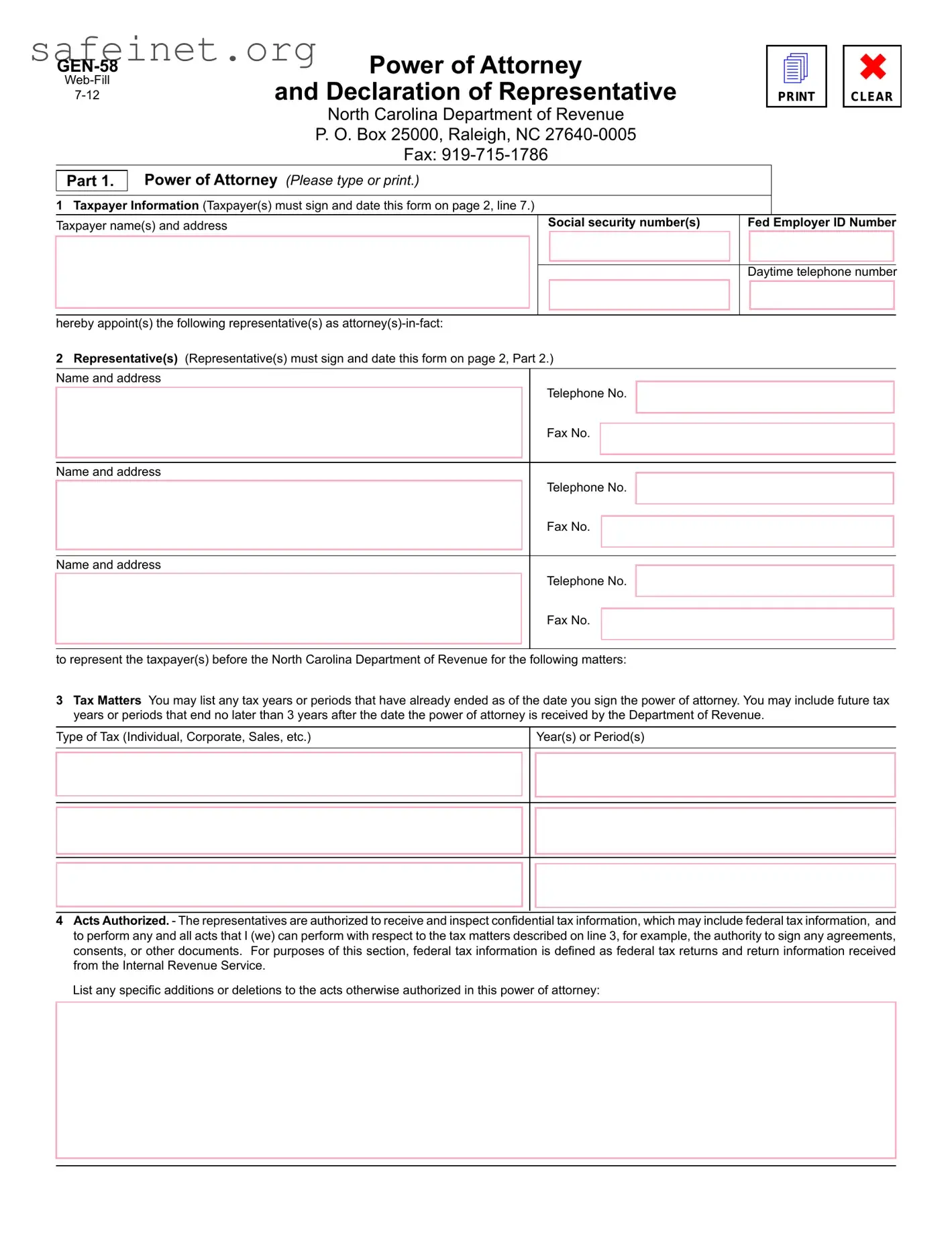

1Taxpayer Information (Taxpayer(s) must sign and date this form on page 2, line 7.)

Taxpayer name(s) and address |

Social security number(s) |

Fed Employer ID Number |

||

|

|

|

|

|

Daytime telephone number

hereby appoint(s) the following representative(s) as

2Representative(s) (Representative(s) must sign and date this form on page 2, Part 2.)

Name and address

Telephone No.

Fax No.

Name and address

Telephone No.

Fax No.

Name and address

Telephone No.

Fax No.

to represent the taxpayer(s) before the North Carolina Department of Revenue for the following matters:

3Tax Matters You may list any tax years or periods that have already ended as of the date you sign the power of attorney. You may include future tax years or periods that end no later than 3 years after the date the power of attorney is received by the Department of Revenue.

Type of Tax (Individual, Corporate, Sales, etc.)

Year(s) or Period(s)

4Acts Authorized. - The representatives are authorized to receive and inspect confidential tax information, which may include federal tax information, and to perform any and all acts that I (we) can perform with respect to the tax matters described on line 3, for example, the authority to sign any agreements, consents, or other documents. For purposes of this section, federal tax information is defined as federal tax returns and return information received from the Internal Revenue Service.

List any specific additions or deletions to the acts otherwise authorized in this power of attorney:

Page 2

Gen. 58

5

Department’s homepage for a list of the online services for businesses that require login to the |

|

PLEASE CHECK THIS BOX IF YOUR REPRESENTATIVE WILL CREATE AN |

|

SERVICES ON YOUR BEHALF |

|

|

|

6Retention/Revocation of Prior Power(s) of Attorney. - The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Department of Revenue for the same tax matters and years or periods covered by this document. If you do not

want to revoke a prior power of attorney, check here |

►□ |

|

|

|

|

YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT. |

|

|

7Signature of Taxpayer(s). - If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested.

If signed by a corporate officer, partner, guardian, tax matters partner/person, executor, representative, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

►IF NOT SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED.

Signature |

Date |

Title (if applicable) |

Print Name |

|

|

Signature |

Date |

Title (if applicable) |

Print Name |

|

|

Part 2.

Declaration of Representative

Under penalties of perjury, I declare that:

• |

I am authorized to represent the taxpayer(s) identified in Part 1 for the tax matter(s) specified there; and |

• |

I am one of the following: |

|

a Attorney - a member in good standing of the bar of the highest court of the jurisdiction shown below. |

bCertified Public Accountant - duly qualified to practice as a certified public accountant in the jurisdiction shown below.

cEnrolled Agent - Enrolled as an agent under the requirements of Treasury Department Circular No. 230.

dOfficer - a bona fide officer of the taxpayer’s organization.

e

fFamily Member - a member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

gOther (explain) -

►IF THIS DECLARATION OF REPRESENTATIVE IS NOT SIGNED AND DATED, THE POWER OF ATTORNEY WILL BE RETURNED.

Designation - Insert

above letter

Jurisdiction (state) or Enrollment Card No.

Signature

Date

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA Gen-58 form is used to authorize someone to represent you in tax matters before the IRS. |

| Eligibility | Any individual taxpayer can use this form to designate a representative for tax purposes. |

| Governing Law | The use of this form is governed by IRS regulations under the Internal Revenue Code. |

| Signature Requirement | A valid taxpayer signature is necessary for the form to be effective. |

| Expiration | This authorization remains in effect until revoked or until the tax matters are resolved. |

| Submission Method | The completed form can be submitted electronically or via mail to the appropriate IRS office. |

| Additional Information | Additional guidance on filling out the form can be obtained through the IRS website. |

After gathering the necessary information, the next steps involve carefully completing the Tax POA gen-58 form. This form is essential for granting someone the authority to act on your behalf regarding tax matters. Ensuring accuracy in each section is crucial to avoid any potential issues. Below are the steps to follow for filling out the form correctly.

What is the Tax POA gen-58 form?

The Tax POA gen-58 form is a Power of Attorney document specifically used for tax-related matters. This form allows an individual, referred to as the "principal," to designate another person, called the "agent," to act on their behalf in dealings with the IRS or state tax authorities. It grants the agent the authority to handle certain tax matters, such as filing returns, responding to inquiries, and receiving sensitive tax information.

Who can use the Tax POA gen-58 form?

Any individual or business entity who needs assistance with tax matters can use the Tax POA gen-58 form. This includes individuals who may want to authorize a tax professional, such as an accountant or an attorney, to handle their tax affairs. Businesses may also use this form to designate someone to manage tax filings and communications.

How do I complete the Tax POA gen-58 form?

To complete the Tax POA gen-58 form, start by providing your personal information as the principal, including your name, address, and taxpayer identification number (TIN). Next, provide the agent's information, including their name and address. You'll also need to select the specific tax matters and tax years for which you are granting authority. Lastly, sign and date the form to make it official.

Do I need to have my signature notarized?

No, the Tax POA gen-58 form does not require notarization. However, it must be signed by you as the principal. It’s important that all information is accurate to ensure the form is processed correctly.

How does the Tax POA gen-58 form affect my rights?

By using the Tax POA gen-58 form, you grant specific rights to your agent to act on your behalf. This means that the agent can communicate with tax authorities and handle certain tax matters. However, the principal still retains ultimate responsibility for their tax obligations. You can revoke this authority at any time if needed.

What should I do if I want to revoke the Tax POA gen-58 form?

If you wish to revoke the Tax POA gen-58 form, you must submit a written notice of revocation to the agent and the relevant tax authority. This notice should include your name, the agent’s name, and a statement that you are revoking the Power of Attorney. Additionally, submitting another POA form that does not list the agent will also serve to revoke the previous authority.

How long is the Tax POA gen-58 form valid?

The Tax POA gen-58 form remains valid until you revoke it, or until the specific tax matters and years indicated on the form have been resolved. If you choose to cancel the POA or if the agent no longer needs the authority, the form can be terminated at any time.

Can I designate more than one agent using the Tax POA gen-58 form?

The Tax POA gen-58 form allows you to designate one primary agent. However, you can include additional agents if you wish to grant shared authority. It is important to clearly outline the roles each agent will play in the management of your tax matters.

Where can I find the Tax POA gen-58 form?

You can find the Tax POA gen-58 form on the official website of the IRS or state tax authority. It is often available as a downloadable PDF that you can fill out and print. Make sure to use the most recent version of the form to ensure compliance.

Is there a fee associated with filing the Tax POA gen-58 form?

There is typically no fee associated with filing the Tax POA gen-58 form. However, if an agent is a tax professional, they may charge for their services in preparing and submitting the form, as well as for their assistance in handling your tax matters.

Incorrect Identification Information: Often, individuals fail to provide accurate details such as their name, address, or Social Security number. This can lead to delays in processing the form.

Choosing the Wrong Authorizations: The form allows for specific authorizations. Misunderstanding which sections to complete can lead to a limited scope of representation.

Missing Signatures: Some people forget to sign the form. Without a signature, the IRS cannot accept it, and the intended authority won’t be granted.

Improperly Completed Dates: Providing incorrect dates or failing to include the date can create acceptance issues. This simple mistake can render the whole form invalid.

Failure to Specify the Duration of Authority: Not indicating how long the representative should have authority can lead to future confusion and potential complications.

Neglecting Additional Representatives: If you want more than one person to handle your tax matters, forgetting to list all representatives can restrict access to your information.

Forgetting to Keep a Copy: After submission, it’s vital to keep a copy of the completed form for your own records. This can help in resolving any future disputes about authority.

Using Outdated Forms: The IRS periodically updates forms. Ensuring you’re using the latest version of the Tax POA gen-58 form is essential for compliance.

Ignoring State-Specific Requirements: Some states have their own rules and requirements for tax power of attorney forms. Always verify if additional state forms or information are needed.

The Tax Power of Attorney (POA) Gen-58 form allows individuals to designate another person to handle their tax matters with the IRS or state tax authorities. Several other documents often accompany this form to ensure comprehensive representation and compliance. Below are four key documents that are frequently used alongside the Tax POA Gen-58 form.

Including these documents with the Tax POA Gen-58 form can help ensure that all necessary permissions and information are in order, facilitating a smoother tax representation experience. Always consider consulting with a professional to ensure compliance and proper procedure.

The Tax Power of Attorney (POA) form, often referred to as the Gen-58 form, allows an individual to authorize someone else, typically a tax professional, to represent them before the IRS regarding tax matters. A document similar to this is the Durable Power of Attorney. This form grants an agent the authority to manage a person's financial matters, not just limited to taxes but will remain effective even if the person becomes incapacitated. Its broad scope of authority distinguishes it from the Tax POA, which is specifically for tax-related issues.

Another closely related document is the Limited Power of Attorney. This variation grants agents specific powers for certain situations, such as handling tax filings for a defined period or circumstance. Unlike the Tax POA Gen-58, which is closely tied to federal tax matters, a Limited Power of Attorney can encompass other areas such as real estate or banking, but the authority granted can be tailored to suit particular needs.

The IRS Form 2848 is inherently similar to the Gen-58 form as it is also a power of attorney specific to tax matters. This IRS form allows taxpayers to appoint someone to represent them in tax matters before the IRS. What sets it apart is its ability to specify the exact type of tax matters in which representation is authorized, creating a more detailed outline of the responsibilities and limits of the appointed representative.

The Authorization to Release Information form is important for those dealing with entities like the IRS or state tax agencies. Though it does not formally authorize someone to represent a taxpayer, it allows those agencies to share information about the taxpayer's account with their designated individual. This form helps facilitate communication but lacks the full representation authority offered by the Tax POA Gen-58.

A Revocation of Power of Attorney is crucial when an individual wants to withdraw the authorization that was previously granted. When using a Tax POA like the Gen-58, understanding that this revocation process exists is essential. It ensures that the appointed representative can no longer act on behalf of the taxpayer, giving them control over who represents them in tax matters.

The Health Care Power of Attorney often comes up in different contexts but is noteworthy for its role in medical decision-making. While it does not directly relate to tax matters, its importance in ensuring that an individual’s health care preferences are followed highlights the broader concept of empowering another individual to act on one's behalf. This document is limited specifically to health care decisions, offering a clear contrast to the tax-focused authority found in the Gen-58.

Additionally, the Business Power of Attorney serves businesses in a similar fashion. It allows an appointed individual to act on behalf of a business in various dealings, including tax matters. Unlike the Tax POA, which primarily focuses on an individual’s tax concerns, the Business POA addresses broader commercial activities beyond tax representation.

The Consent to Representation form, while not a power of attorney, allows taxpayers to provide their consent for their representatives to act in a specific instance, such as dealing with audits or assessments. This can be essential for communication but does not provide the same extensive authority as the Tax POA, which grants rights more comprehensively to handle a wide range of tax issues.

Next is the General Power of Attorney, which provides sweeping authority for the agent to act in legal and financial matters on behalf of an individual. It covers many areas of law, not just taxes. This broad range can lead to confusion if specific tax matters are the main concern, which is where the focused nature of the Tax POA Gen-58 becomes particularly advantageous.

Finally, the Non-Disclosure Agreement (NDA) shares a connection in that both documents deal with sensitive information. An NDA focuses on protecting confidential information between parties, while the Tax POA Gen-58 focuses on granting authority to discuss and handle tax matters. Understanding both can be essential for those who manage tax and financial information responsibly.

When filling out the Tax POA Gen-58 form, it’s important to follow certain guidelines to ensure your application is accurate and complete. Here are some things you should and shouldn’t do:

Following these guidelines can help prevent issues and ensure that your Tax POA Gen-58 form is processed smoothly.

The Tax Power of Attorney (POA) Gen-58 form is essential for anyone who needs to allow someone else to manage their tax matters with the IRS. However, there are several misconceptions surrounding this form that can lead to confusion. Here’s a list of some common misunderstandings about the Tax POA Gen-58 form:

Understanding these misconceptions can help individuals make more informed decisions about their tax representation options.

When dealing with tax matters, understanding how to fill out and use the Tax Power of Attorney (POA) Gen-58 form is essential. Below are key takeaways that can simplify the process for you.

Using the Tax POA Gen-58 form wisely can alleviate stress during tax season. Knowing the procedures can empower you with confidence when navigating your tax responsibilities.