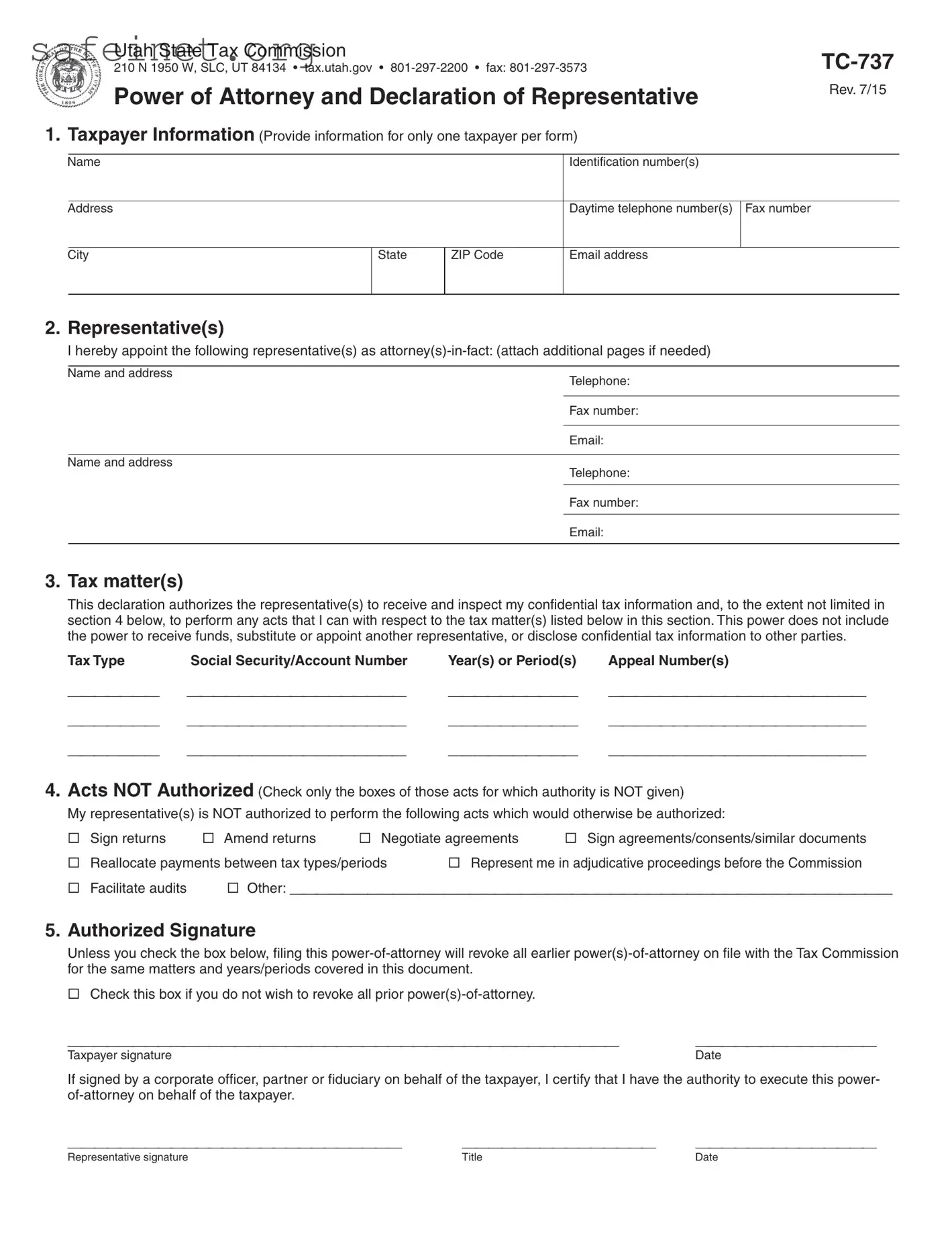

The Tax Power of Attorney (POA) form TC-737 is an essential document used by taxpayers in the United States to authorize another individual or representative to handle their tax affairs with the relevant tax authority. This form allows the designated person, often a tax professional or attorney, to perform various tasks on behalf of the taxpayer, including responding to inquiries, accessing tax records, and signing documents related to tax matters. The TC-737 form provides a streamlined approach for taxpayers who may find it challenging to manage their taxes due to time constraints or lack of expertise. It ensures that the appointed representative can act on behalf of the taxpayer without the need for direct involvement in every interaction with the tax authority. PHAs can also revoke this authorization at any time, offering flexibility and control over tax-related representation. Knowing how to properly fill out the TC-737 form and understanding its implications is crucial for anyone seeking assistance with their tax situation.

Utah State Tax Commission |

|

210 N 1950 W, SLC, UT 84134 tax.utah.gov |

|

Power of Attorney and Declaration of Representative |

Rev. 7/15 |

|

|

1. Taxpayer Information (Provide information for only one taxpayer per form) |

|

Name

Identification number(s)

Address

Daytime telephone number(s) Fax number

City

State

ZIP Code

Email address

2. Representative(s)

I hereby appoint the following representative(s) as

Name and address

Name and address

Telephone:

Fax number:

Email:

Telephone:

Fax number:

Email:

3. Tax matter(s)

This declaration authorizes the representative(s) to receive and inspect my confidential tax information and, to the extent not limited in section 4 below, to perform any acts that I can with respect to the tax matter(s) listed below in this section. This power does not include the power to receive funds, substitute or appoint another representative, or disclose confidential tax information to other parties.

Tax Type |

Social Security/Account Number |

Year(s) or Period(s) |

Appeal Number(s) |

_______ |

_________________ |

__________ |

____________________ |

_______ |

_________________ |

__________ |

____________________ |

_______ |

_________________ |

__________ |

____________________ |

4.Acts NOT Authorized (Check only the boxes of those acts for which authority is NOT given)

My representative(s) is NOT authorized to perform the following acts which would otherwise be authorized:

|

Sign returns |

Amend returns |

Negotiate agreements |

Sign agreements/consents/similar documents |

|

|

Reallocate payments between tax types/periods |

Represent me in adjudicative proceedings before the Commission |

|||

Facilitate audits Other: _______________________________________________

5.Authorized Signature

Unless you check the box below, filing this

Check this box if you do not wish to revoke all prior

___________________________________________ |

______________ |

Taxpayer signature |

Date |

If signed by a corporate officer, partner or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power-

__________________________ _______________ ______________

Representative signature |

Title |

Date |

| Fact Name | Details |

|---|---|

| Form Purpose | The Tax POA Form TC-737 allows a taxpayer to designate another individual or entity to represent them in tax matters before the state tax authority. |

| Governing Law | This form is governed by the Utah Code Title 59, specifically the Tax Administration Act. |

| Required Information | Taxpayers must provide their name, address, Social Security number or Tax ID number, and the representative’s details. |

| Submission Process | The completed TC-737 form should be submitted to the Utah State Tax Commission, either by mail or electronically, depending on the current regulations. |

| Validity Period | This form remains valid until revoked by the taxpayer or upon the conclusion of the designated tax matters. |

Completing the Tax POA Form TC-737 is a straightforward process that allows individuals to authorize someone to act on their behalf regarding tax matters. Once this form is filled out correctly, it can facilitate communication with tax authorities and ensure that the appointed representative can handle necessary tax obligations effectively.

What is the Tax POA form TC-737?

The Tax POA form TC-737, or Power of Attorney, allows an individual to appoint someone else to handle their tax matters on their behalf. This form gives the designated representative the authority to speak with the tax authorities, access tax records, and take actions related to the taxpayer's accounts.

Who can be appointed as a representative using TC-737?

The representative can be a trusted friend, family member, accountant, or attorney. The key is that the person you choose should be knowledgeable about tax matters and trustworthy, as they will have access to sensitive financial information.

How do I fill out the TC-737 form?

You will need to enter your personal information, such as your name, address, and Social Security number. Then, provide the same information for the person you are appointing. Lastly, you must sign and date the form to make it valid.

Is there a fee for submitting the TC-737 form?

Typically, there is no fee for submitting the TC-737 form. However, it is advisable to check with your local tax authority, as procedures and policies can vary by state.

How long does it take for the TC-737 to become effective?

The TC-737 generally becomes effective as soon as the tax authority processes it. This can vary in timeframe depending on the specific tax agency's workload, so it's best to submit the form well in advance of any deadlines.

Can I revoke a Power of Attorney submitted on the TC-737?

Yes, you can revoke the Power of Attorney at any time by submitting a new form that clearly states your intention to revoke the previous authorization. Make sure the new document is properly signed and dated.

What if I need to make changes to the TC-737 form after submitting it?

If changes are needed, you should submit a new TC-737 form with the updated information. It's essential to clearly indicate that this new form replaces the previous one. Communicating this to the tax authorities can prevent confusion.

Can I use the TC-737 form for corporate tax matters?

The TC-737 form is primarily designed for individual taxpayers. If you need to appoint a representative for a business, you may need to use a different form specific to corporate tax matters. Check with the relevant tax authority for guidance.

What happens if my representative makes a mistake?

If your representative makes a mistake, you may still be held liable for any tax obligations. It's essential to choose a knowledgeable representative to avoid potential issues. You may want to periodically review their actions to ensure everything is handled correctly.

How can I check the status of the TC-737 after submission?

To check the status of your submission, it's best to contact the tax authority directly. Provide them with the relevant identification details so they can assist you. They will let you know whether your form has been processed and if your representative has the authority to act on your behalf.

By paying attention to these common errors, you can ensure that your Tax POA form TC-737 is completed correctly. This, in turn, aids in a smoother interaction with the IRS and your chosen representative.

The Tax Power of Attorney (POA) form TC-737 allows you to authorize someone else to represent you before tax authorities. Often, this form accompanies other important documents that facilitate tax representation and compliance. Each document serves a specific purpose, ensuring that both the taxpayer's rights and the process of tax representation are protected.

Incorporating these documents alongside the TC-737 form ensures a smoother process when dealing with tax matters. Clarity and precision are crucial in tax representation, protecting both the taxpayer and their chosen representative.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is one such document that shares similarities with the Tax POA form TC-737. Both forms allow individuals to designate someone to represent them in tax matters. With Form 2848, a taxpayer can authorize an individual to communicate with the IRS on their behalf. This document is crucial for those seeking to ensure that their representative can receive confidential information and handle various tax-related queries effectively.

Another closely related document is IRS Form 8821, Tax Information Authorization. This form permits an individual to authorize a representative to receive and inspect confidential tax information without granting the same level of authority as a power of attorney. Unlike TC-737, which allows broader representation, Form 8821 is geared towards easier access and review of specific tax records, making it ideal for individuals who want to limit the scope of authority delegated to their representative.

The California Form FTB 3520, Power of Attorney, provides a similar function within the state tax context. Like TC-737, this California form allows taxpayers to appoint someone to act on their behalf in matters concerning the Franchise Tax Board. It similarly maintains the confidentiality of the taxpayer's information, ensuring that the designated agent can secure necessary documentation and communicate concerning taxes owed or due.

Texas also has its version of a power of attorney through the Texas Power of Attorney Form, which serves a comparable purpose. This document allows individuals to delegate authority to someone else to handle personal and financial affairs, including tax matters. While TC-737 focuses on state tax issues, the Texas Power of Attorney Form may encompass a broader range of responsibilities beyond taxation.

The New York State Form POA-1 is yet another similar document that functions similarly to TC-737. This form allows New York residents to appoint someone to act on their behalf for tax-related matters. Like the TC-737, the POA-1 grants the representative the authority to access confidential information regarding the taxpayer’s state-related tax obligations.

There is also the IRS Form 8822, Change of Address. Though not a power of attorney form, it is related in that it permits taxpayers to authorize another person to notify the IRS of address changes on their behalf. While it serves a different purpose, it emphasizes the shared goal of facilitating communication between taxpayers and tax authorities with the necessary representation.

Lastly, the Durable Power of Attorney is another relevant document that contains elements similar to the Tax POA form TC-737. While it primarily focuses on healthcare and financial decisions, it can extend to tax matters as well. In this way, individuals can ensure that their appointed agent can make decisions and represent them in various circumstances, including tax-related issues, if necessary. This broader authority may appeal to those wanting comprehensive management over their financial and tax obligations.

When filling out the Tax POA form TC-737, consider these important dos and don'ts:

The Tax Power of Attorney (POA) form TC-737 has several misconceptions associated with it. Understanding these misconceptions can help taxpayers navigate their tax matters more effectively.

This is not accurate. The TC-737 form can be used by both individuals and businesses, allowing representatives to act on behalf of various entities in tax matters.

There is no fee associated with the submission of the TC-737 form. Taxpayers can file this form without incurring additional costs.

While the form does grant authority, the scope of this power is defined by the specifics outlined on the form itself. Taxpayers should clearly detail what actions their representatives can take.

This is incorrect. Taxpayers can revoke a previously submitted TC-737 form at any time by submitting a new form or a written notice to the tax agency. Revocation will restore the taxpayer’s control over their tax matters.

The Tax POA Form TC-737 is an important document for individuals requiring assistance with their tax matters. Here are some crucial points to consider when filling out and utilizing this form:

By understanding these key points, individuals will be better equipped to navigate the process related to the Tax POA Form TC-737 efficiently.