When it comes to managing tax matters, the Tax Power of Attorney (POA) form RD-1061 serves as an essential tool for individuals and businesses alike. This form allows taxpayers to designate an authorized representative, granting them the power to act on their behalf in dealings with the tax authorities. Understanding the significance of the RD-1061 involves recognizing its ability to facilitate communication between taxpayers and the Department of Revenue, streamline the resolution of tax disputes, and ensure that tax-related decisions are made efficiently. It is crucial to be aware of the specific information required, such as the taxpayer's details, representative's information, and the scope of authority being granted. Furthermore, knowing how and when to submit the RD-1061 can significantly impact one’s tax filing process, ensuring compliance while protecting taxpayer rights. As federal and state tax laws continue to evolve, the RD-1061 remains a vital resource in navigating these complexities, making informed tax decisions easier and more accessible for everyone involved.

Form

CLEAR

Page 1

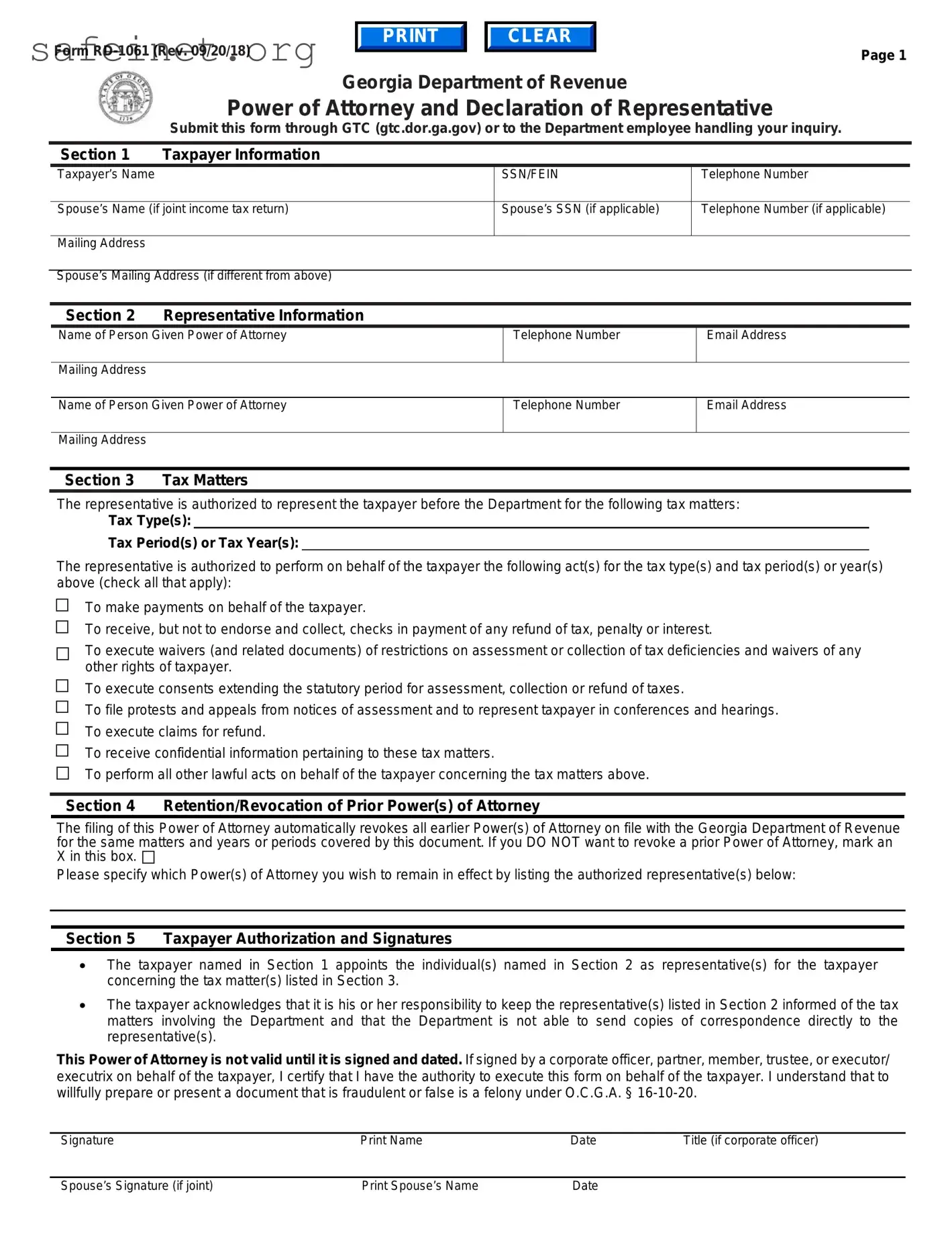

Georgia Department of Revenue

Power of Attorney and Declaration of Representative

Submit this form through GTC (gtc.dor.ga.gov) or to the Department employee handling your inquiry.

Section 1 |

Taxpayer Information |

|

|

|

Taxpayer’s Name |

|

SSN/FEIN |

Telephone Number |

|

|

|

|

|

|

Spouse’s Name (if joint income tax return) |

Spouse’s SSN (if applicable) |

Telephone Number (if applicable) |

||

Mailing Address

Spouse’s Mailing Address (if different from above)

Section 2 Representative Information

Name of Person Given Power of Attorney

Mailing Address

Telephone Number

Email Address

Name of Person Given Power of Attorney

Mailing Address

Telephone Number

Email Address

Section 3 |

Tax Matters |

The representative is authorized to represent the taxpayer before the Department for the following tax matters:

Tax Type(s):

Tax Period(s) or Tax Year(s):

The representative is authorized to perform on behalf of the taxpayer the following act(s) for the tax type(s) and tax period(s) or year(s) above (check all that apply):

To make payments on behalf of the taxpayer.

To receive, but not to endorse and collect, checks in payment of any refund of tax, penalty or interest.

To execute waivers (and related documents) of restrictions on assessment or collection of tax deficiencies and waivers of any other rights of taxpayer.

To execute consents extending the statutory period for assessment, collection or refund of taxes.

To file protests and appeals from notices of assessment and to represent taxpayer in conferences and hearings.

To execute claims for refund.

To receive confidential information pertaining to these tax matters.

To perform all other lawful acts on behalf of the taxpayer concerning the tax matters above.

Section 4 Retention/Revocation of Prior Power(s) of Attorney

The filing of this Power of Attorney automatically revokes all earlier Power(s) of Attorney on file with the Georgia Department of Revenue for the same matters and years or periods covered by this document. If you DO NOT want to revoke a prior Power of Attorney, mark an X in this box.

Please specify which Power(s) of Attorney you wish to remain in effect by listing the authorized representative(s) below:

Section 5 Taxpayer Authorization and Signatures

•The taxpayer named in Section 1 appoints the individual(s) named in Section 2 as representative(s) for the taxpayer concerning the tax matter(s) listed in Section 3.

•The taxpayer acknowledges that it is his or her responsibility to keep the representative(s) listed in Section 2 informed of the tax matters involving the Department and that the Department is not able to send copies of correspondence directly to the representative(s).

This Power of Attorney is not valid until it is signed and dated. If signed by a corporate officer, partner, member, trustee, or executor/ executrix on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer. I understand that to willfully prepare or present a document that is fraudulent or false is a felony under O.C.G.A. §

Signature |

Print Name |

Date |

Title (if corporate officer) |

Spouse’s Signature (if joint) |

Print Spouse’s Name |

Date |

|

Form |

Page 2 |

Section 6 Acknowledgment of the Power of Attorney

This Power of Attorney must be acknowledged by the taxpayer before a notary public, unless the appointed representative(s) is licensed to practice as an

Acknowledgement of Power of Attorney. The person(s) signing as the taxpayer in Section 5 above appeared this day before a notary public and acknowledged this Power of Attorney as a voluntary act and deed.

Sworn and subscribed before me this __________ day of ______________________, 20_______.

Signature of Notary

Notary Seal

Date

Section 7 Declaration of Representative

Under penalties of perjury, I declare that:

• I am authorized to represent the taxpayer identified in Section 1 for the matter(s) specified in Section 3 of this form; and

•I am one of the following (indicate all thatapply):

1.An

2.A certified public accountant duly qualified to practice in the jurisdiction indicated below.

3.Enrolled as an agent to practice before the Internal Revenue Service under the requirements of Circular 230.

4.A registered public accountant.

Designation – use number(s) from above list

(1 - 4)

Licensing jurisdiction (state) or other licensing authority (if applicable)

Bar, license, certification,

registration, or enrollment number

Signature

Date

Form |

Page 3 |

Purpose of Form

A taxpayer may use Form

Filing Instructions

Taxpayers should submit Form

To upload to GTC: (1) Login, (2) Under “I Want To” select “See More Links”, (3) Select “Submit Power of Attorney", and (4) Follow the prompts to upload the Form

Revocation

If you have a valid Form

If the taxpayer or representative merely wants to revoke an existing authorization, upload a copy of the previously executed Form

Specific Instructions

Section 1 – Taxpayer Information

Enter the name, address, and contact information of the taxpayer. If the taxpayer is an individual, enter the full Social Security number (SSN). If the taxpayer is a business entity, enter the Federal Employer Identification Number (FEIN). If the taxpayer is granting access to a joint return, enter the spouse’s name, address, and full SSN.

Section 2 – Representative Information

Enter the representatives’ names, addresses and any applicable contact information. A representative must be an individual, not a business entity. If designating authority to more than two representatives, please attach a schedule similar in form to Section 2 signed by the taxpayer.

Section 3 – Tax Matters

Enter the tax type(s) and specific period(s) or year(s) for which the authorization is being granted. The Department will only discuss and/or disclose taxpayer information for the type(s) and period(s) listed. Notices and communications will be sent to the taxpayer, not the representative. The representative may access copies of taxpayer notices and communications via third party access to the taxpayer’s account through GTC.

Form |

Page 4 |

Section 4 – Retention/Revocation of Prior Power(s) of Attorney

All existing Form

Section 5 – Taxpayer Authorization and Signature

The taxpayer must sign in Section 5 for Form

Taxpayer |

Who Must Sign |

|

|

|

|

Individuals |

The individual/sole proprietor must sign (if granting access to a joint return, |

|

spouse must also sign). |

||

|

||

Corporations |

A corporate officer with authority to sign. |

|

|

|

|

Partnerships |

A partner having authority to act in the name of the partnership must sign. |

|

|

|

|

Limited Liability |

A member having authority to act in the name of the company must sign. |

|

Companies |

||

|

||

Trusts |

A trustee must sign. |

|

|

|

|

Estates |

An executor/executrix or the personal representative of the estate must sign. |

|

|

|

Section 6 – Acknowledgment of the Power of Attorney

This POA must be acknowledged by the taxpayer before a notary public, unless an appointed representative is an

Section 7 – Declaration of Representative

If an appointed representative is licensed to practice as an

| Fact Name | Description |

|---|---|

| Form Purpose | The Tax POA Form RD-1061 is used to authorize a representative to act on your behalf in tax matters before the Georgia Department of Revenue. |

| Eligibility | Any individual or business entity can designate an authorized representative, provided they fill out the form correctly. |

| Governing Law | This form is governed by the Georgia Department of Revenue regulations, specifically under O.C.G.A. § 48-2-23. |

| Required Information | To complete the form, you need to provide information about both the taxpayer and the representative, including contact details. |

| Submission Process | The completed RD-1061 form can be submitted by mail or electronically through the Georgia Department of Revenue's online portal. |

| Revocation of Authority | You can revoke the power of attorney at any time by submitting a new RD-1061 form or a written notice to the Department of Revenue. |

After obtaining the Tax POA form RD-1061, you are ready to proceed with filling it out. This form allows you to designate someone to represent you in tax matters with the state. Follow these steps carefully to ensure all required information is provided accurately.

Once you have completed all these steps, review the form for any errors. After confirming the accuracy, submit it to the appropriate tax authority. Keep a copy for your records.

What is the Tax POA Form RD-1061?

The Tax Power of Attorney (POA) Form RD-1061 is an official document that allows a taxpayer to appoint another individual, often a tax professional, to represent them before the taxing authorities. This form grants the designated person authority to handle a range of tax matters on behalf of the taxpayer, ensuring that the needs of the taxpayer are managed effectively and efficiently.

Who can I appoint using the RD-1061 form?

Taxpayers can appoint anyone they trust using the RD-1061 form. This includes certified public accountants, tax attorneys, or any qualified individual. However, keep in mind that this trusted individual must be willing to accept the role and responsibilities that come with it. It’s vital to choose someone who is knowledgeable about your specific tax situation.

What authority does the appointed representative have?

The representative authorized by the RD-1061 form can engage with tax authorities on your behalf. This includes the ability to access your tax records, discuss your tax situation, and even make decisions regarding your tax filings. Essentially, they can act in your stead to ensure that any issues are resolved and any obligations are fulfilled.

How do I fill out the RD-1061 form?

Filling out the RD-1061 form requires careful attention to detail. Start by entering your personal information, including your name, Social Security number, and contact information. Next, provide details about the representative you wish to appoint, such as their name and address. Make sure to sign and date the form, as this step confirms your authorization.

Where should I send the completed RD-1061 form?

The completed RD-1061 form should be sent to the appropriate tax authority. Depending on your location, this could be a state or federal tax office. Be sure to check the specific instructions that accompany the form, as they will provide guidance on the correct mailing address to ensure that your submission is received promptly.

How long does it take for the RD-1061 form to be processed?

Processing times can vary depending on the tax authority's workload. Generally, however, you can expect to wait anywhere from a few days to several weeks. It’s wise to follow up with the relevant agency if you haven't received confirmation of your authorization after a reasonable period.

Can I revoke the POA once I’ve submitted the RD-1061 form?

Yes, you can revoke the Power of Attorney at any time. If you decide to do so, it is crucial to submit a written notice of revocation to the tax authority. This action ensures that your previous representative no longer has the authority to act on your behalf. Be sure to communicate with both the tax authority and your former representative regarding the revocation to avoid any misunderstandings.

Inaccurate Information: Individuals often provide incorrect personal information, such as Social Security numbers or addresses. This can lead to delays and complications in processing the form.

Failure to Sign: Not signing the form is a common oversight. Without a signature, the form is considered incomplete and cannot be processed.

Improperly Specifying Powers: Many people do not clearly indicate the specific powers granted to the tax representative. This ambiguity can create confusion regarding the authority of the representative.

Neglecting to Check Boxes: Certain boxes must be checked to indicate which types of tax matters the power of attorney covers. Failing to do this can limit the authority of the representative.

The Tax Power of Attorney (POA) Form RD-1061 allows you to designate someone to handle your tax matters on your behalf. This document works alongside several other forms and documents that may be necessary in various tax-related situations. Below is a list of commonly used forms that you might encounter.

Understanding these forms will help ensure that your tax-related processes run smoothly. Each document serves a specific purpose and can be integral to managing your financial responsibilities effectively.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is similar to the Tax POA form RD-1061 as both enable taxpayers to authorize someone to act on their behalf before the IRS. Both forms require the taxpayer's information and the representative’s details, including their qualifications. They allow the representative to receive and inspect confidential information, helping streamline communication between the IRS and the taxpayer.

Another comparable document is the IRS Form 8821, Tax Information Authorization. While the POA focuses on granting authority to represent, Form 8821 allows an individual to receive tax information without the power to act on behalf of the taxpayer. Both forms serve to facilitate communication with the IRS, but they differ in the level of authority provided to the representative.

The California Franchise Tax Board’s FTB 3520 form, Power of Attorney, works similarly by allowing taxpayers to designate an agent for tax-related matters. Like the RD-1061, it includes sections for both taxpayer and representative information. The FTB 3520 grants rights specific to California tax situations, making it a regional equivalent that still follows the general principles of taxpayer representation.

The New York State Department of Taxation and Finance has its own Power of Attorney Form, POA-1, which offers similar functions. It allows individuals to appoint representatives for state tax matters. Similar to the RD-1061, this form requires both parties' details and is essential for dealing with New York tax issues, illustrating how state-level practices mirror federal procedures.

The IRS Form 56, Notice Concerning Fiduciary Relationship, is another document related to taxpayer representation. While it specifically deals with fiduciaries and their authority over a taxpayer’s affairs, it shares the essence of enabling authorized representation. It informs the IRS about the fiduciary’s position, facilitating communication in tax matters.

The Department of Veterans Affairs Form 21-22, Appointment of Veteran Service Organization as Claimant’s Representative, is similar in the context of handling benefits. It allows veterans to designate representatives for assistance with claims, demonstrating how different organizations create processes for representation, akin to tax matters.

The Social Security Administration’s SSA-11, Request for a Representative Payee, serves a related purpose for individuals who require help managing their Social Security benefits. While its focus is on financial management rather than tax representation, both forms emphasize the importance of having an authorized individual to navigate complex processes on behalf of another.

In the realm of healthcare, the Durable Power of Attorney for Healthcare is akin to a tax power of attorney but for medical decisions. This form allows an individual to appoint someone to make healthcare choices if they become unable to do so. Similarities include the requirement for signatures and the necessity to outline the authority granted, though the focus shifts from financial to health decisions.

The Financial Power of Attorney document grants comprehensive rights over an individual's financial affairs, similar to a tax POA in its role of designating authority. Both forms require clear delineation of what the representative can and cannot do, although the financial power of attorney encompasses broader responsibilities.

Lastly, the General Power of Attorney facilitates broad legal authority. While the Tax POA form RD-1061 is specific to tax matters, a General Power of Attorney allows for various kinds of legal decisions and actions on behalf of the principal. This may include tax-related authority but extends much further, highlighting the varying levels of representation that documents can provide.

When filling out the Tax POA form (RD-1061), it's important to follow certain guidelines to ensure the process goes smoothly. Here’s a list of dos and don’ts to keep in mind:

Many individuals have misconceptions about the Tax POA (Power of Attorney) form RD-1061. Below is a list of these common misunderstandings and clarifications that can help demystify the process.

Understanding these misconceptions can empower you to make informed decisions about your tax representation. Always seek clarity and assistance when navigating tax forms.

The Tax POA (Power of Attorney) form RD-1061 is an important document used in tax matters. Understanding how to fill out and utilize this form can help ensure proper communication with tax authorities.