The Tax Power of Attorney (POA) Form R-7006 is an essential document that facilitates communication between taxpayers and the Michigan Department of Treasury. This form allows individuals to appoint someone they trust—such as a family member, accountant, or attorney—to act on their behalf regarding tax matters. By giving this authority, taxpayers ensure that their chosen representatives can handle issues related to income tax, sales tax, and property tax liabilities effectively. The completion of the R-7006 form is straightforward but requires careful attention to detail, including both the taxpayer’s and the representative’s information. Furthermore, this form can be used for temporary or ongoing representation, making it adaptable to various situations, from simple tax inquiries to more complex issues like audits. It’s important to note that submitting this form does not relieve the taxpayer of their obligations to pay taxes; instead, it enhances their ability to manage those responsibilities efficiently. Understanding how the Tax POA Form R-7006 works can empower individuals to navigate the complexities of the tax system while maintaining control over who assists them in their financial affairs.

LOUISIANA

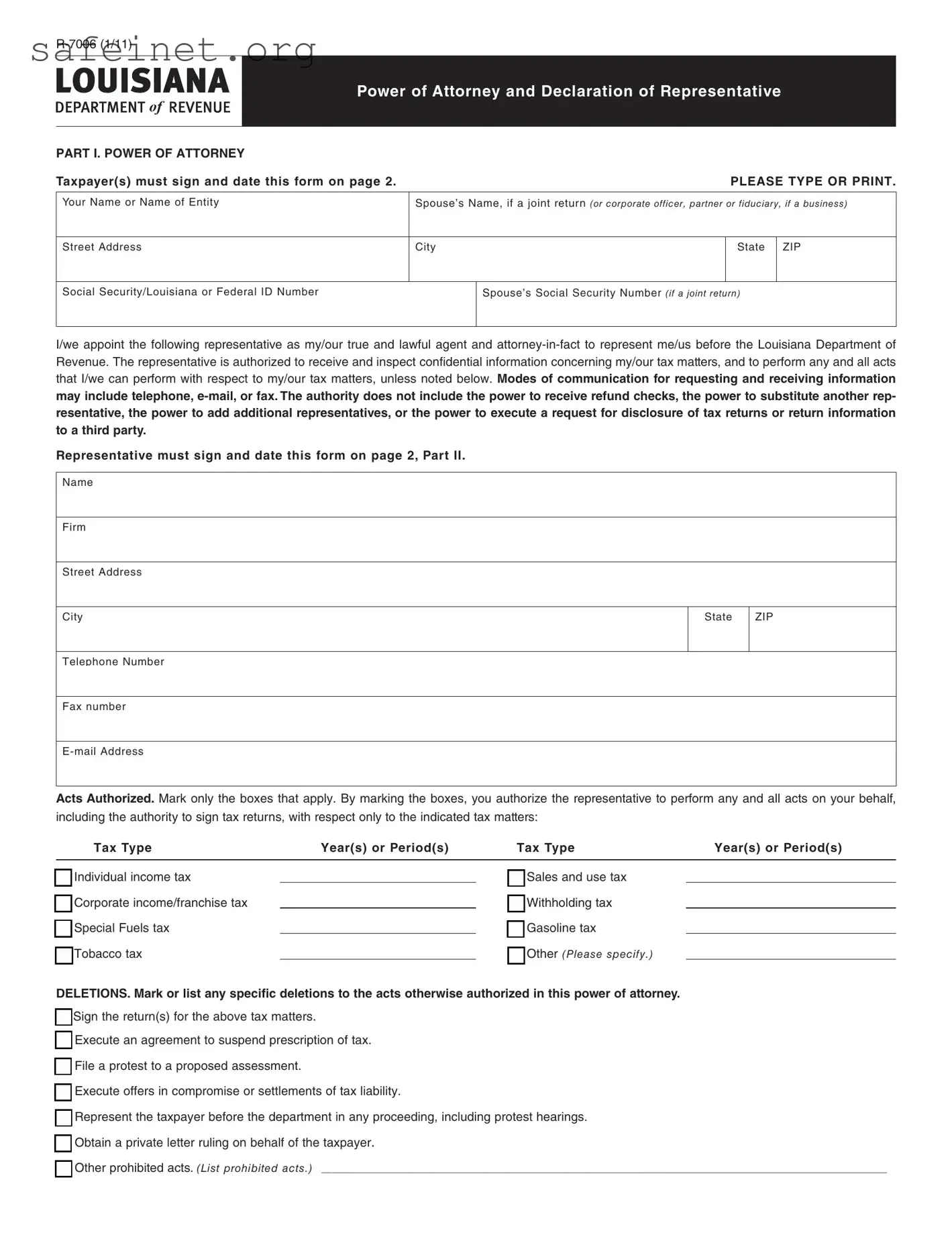

Power of Attorney and Declaration of Representative

DEPARTMENT of REVENUE

PART I. POWER OF ATTORNEY |

|

|

|

|

Taxpayer(s) must sign and date this form on page 2. |

|

|

PLEASE TYPE OR PRINT. |

|

|

|

|

|

|

Your Name or Name of Entity |

Spouse’s Name, if a joint return (or corporate officer, partner or fiduciary, if a business) |

|||

|

|

|

|

|

Street Address |

City |

|

State |

ZIP |

|

|

I |

|

I |

Social Security/Louisiana or Federal ID Number |

Spouse’s Social Security Number (if a joint return) |

|||

I

I/we appoint the following representative as my/our true and lawful agent and

Representative must sign and date this form on page 2, Part II.

Name

Firm

Street Address

City |

State |

ZIP |

|

I |

I |

Telephone Number |

|

|

( |

) |

|

|

|

|

Fax number |

|

|

( |

) |

|

Acts Authorized. Mark only the boxes that apply. By marking the boxes, you authorize the representative to perform any and all acts on your behalf, including the authority to sign tax returns, with respect only to the indicated tax matters:

Tax Type |

Year(s) or Period(s) |

Tax Type |

Year(s) or Period(s) |

■ Individual income tax |

|

■ Sales and use tax |

|

□ |

|

□ |

|

■ Corporate income/franchise tax |

|

■ Withholding tax |

|

□ |

|

□ |

|

■ Special Fuels tax |

|

■ Gasoline tax |

|

□ |

|

□ |

|

■ Tobacco tax |

|

■ Other (Please specify.) |

|

□ |

|

□ |

|

DELETIONS. Mark or list any specifc deletions to the acts otherwise authorized in this power of attorney.

□■ Sign the return(s) for the above tax matters.

□■ Execute an agreement to suspend prescription of tax. □■ File a protest to a proposed assessment.

□■ Execute offers in compromise or settlements of tax liability.

□■ Represent the taxpayer before the department in any proceeding, including protest hearings. □■ Obtain a private letter ruling on behalf of the taxpayer.

□■ Other prohibited acts. (List prohibited acts.) _____________________________________________________________________________________________________________

Page 2 |

NOTICES AND COMMUNICATIONS. Original notices and other written communications will be sent only to you, the taxpayer. Your representative may request and receive information by telephone,

REVOCATION OF PRIOR POWER(S) OF ATTORNEY. Except for Power(s) of Attorney and Declaration of Representative(s) fled on Form

Signature of Taxpayer(s). If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

IF THIS POWER OF ATTORNEY IS NOT SIGNED AND DATED, IT WILL BE RETURNED.

_______________________________________________________________________________________________________________________________________ |

______________________________ |

|

Taxpayer signature |

|

Date (mm/dd/yyyy) |

____________________________________________________________________________________________________________________________________________ |

_________________________________ |

|

Spouse signature |

|

Date (mm/dd/yyyy) |

_________________________________________________________________________________ |

_______________________________________________________ |

_________________________________ |

Signature of duly authorized representative, if the taxpayer |

Title |

Date (mm/dd/yyyy) |

is a corporation, partnership, executor or administrator |

|

|

Part II. DECLARATION OF REPRESENTATIVE

Under penalties of perjury, I declare that:

•I am not currently under suspension or disbarment from practice before the Internal Revenue Service.

•I am authorized to represent the taxpayer(s) identified in Part I for the tax matters specified there; and

•I am one of the following: (insert applicable letter in table below)

a.

b.Certified Public

c.Enrolled

d.

e.

f.Family

g.Other (state the relationship, i.e., bookkeeper or friend)

h.Former Louisiana Department of Revenue Employee. As a representative, I cannot accept representation in a matter with which I had direct involvement while I was a public employee.

IF THIS DECLARATION OF REPRESENTATIVE IS NOT SIGNED AND DATED, THE POWER OF ATTORNEY WILL BE RETURNED.

State Issuing

License

State License Number

Signature

Date

(mm/dd/yyyy)

I |

I |

I |

I |

I |

| Fact Name | Description |

|---|---|

| Form Purpose | The Tax Power of Attorney (POA) form R-7006 allows individuals to authorize a representative to handle their tax affairs on their behalf. |

| Governing Law | This form is governed under the tax laws and regulations established by the Internal Revenue Service and state tax agencies. |

| Eligibility | Any individual or business entity can complete the R-7006 form to designate another person as their authorized representative for tax matters. |

| Required Information | The form requires personal information about both the taxpayer and the designated representative, including names and identification numbers. |

| Filing Method | There are several ways to file the R-7006 form, including mailing it to the appropriate tax office or submitting it electronically in some jurisdictions. |

| Duration of Authority | The authority granted to the representative remains in effect until revoked by the taxpayer or upon the taxpayer's death. |

| Revocation | A taxpayer can revoke the POA at any time by submitting a written notice to the tax authority along with the R-7006 revocation form, if applicable. |

| Multiple Representatives | Taxpayers may designate more than one representative on the form, but each must be listed clearly to avoid confusion. |

After obtaining the Tax Power of Attorney (POA) form R-7006, it is essential to ensure that all required information is filled out accurately. This will facilitate the processing of the form by the relevant authorities. Here are the steps to complete the form correctly.

Once submitted, the form will be reviewed and processed by the designated authority. A follow-up may be required to confirm that the POA has been accepted and is in effect.

What is the Tax POA form R-7006?

The Tax POA form R-7006 is a Power of Attorney form specifically designed for individuals or entities who wish to authorize someone else to handle their tax matters with the state tax agency. By completing this form, you allow an appointed representative to act on your behalf in tax-related situations, such as filings, inquiries, and negotiations with tax authorities.

Who can I designate as my representative on the R-7006 form?

You may designate an attorney, certified public accountant, or any other individual you trust to represent you. This person should be knowledgeable about tax matters and will be empowered to act in your best interests. It’s essential to choose someone reliable and whom you feel comfortable granting this authority.

What information is required to complete the R-7006 form?

To complete the R-7006 form, you'll need to provide basic information about yourself, including your name, address, and taxpayer identification number. Additionally, you must include the representative's details, such as their name and contact information. Lastly, a signature is required to validate the form, confirming your consent to appoint this individual.

Do I need to submit the R-7006 form every year?

No, you do not need to submit the Tax POA form R-7006 annually. Once the form is accepted, it remains in effect until you revoke it in writing or until the representative is no longer authorized to act on your behalf. However, if you wish to change representatives or if your circumstances change, you will need to file a new form.

How long does it take for the R-7006 form to be processed?

The processing time for the R-7006 form varies by agency and their current workload. Generally, you can expect a confirmation of your submission within a few weeks. However, some situations might require additional review, which could take longer. It’s always a good idea to follow up if you haven’t received confirmation in a reasonable time frame.

What should I do if I change my mind about my representative?

If you change your mind about your representative, you have the option to revoke the power of attorney. To do this, you will need to submit a written notice to the tax agency, specifying that you are revoking the authority granted to your previously designated representative. Once the agency processes this revocation, your former representative will no longer have any authority to act on your behalf.

Failure to Sign the Form: One of the most common mistakes is neglecting to sign the form. Without a signature, the IRS will not acknowledge the Power of Attorney (POA) request. It is essential to ensure that all necessary signatures are provided.

Incorrect Taxpayer Information: Inaccuracies in the taxpayer’s name, Social Security number, or address can lead to significant delays. Double-checking this information against official documents is crucial for accuracy.

Not Specifying Tax Matters: The form allows for specific tax matters to be designated. Failing to clearly state which tax matters the POA covers can complicate the authority granted to the representative. It's important to be detailed in this section.

Missing Dates: Dates are vital for the validity of the form. Omitting the date of signature or the effective date of the POA can lead to confusion or rejection of the document. Always include relevant dates to maintain clarity.

By avoiding these common mistakes, individuals can ensure that their Tax POA form is processed smoothly and efficiently. Always review the completed form before submission to mitigate potential errors.

The Tax Power of Attorney form, known as R-7006, is an important document that allows individuals to designate someone else to handle their tax matters. Alongside this form, several other documents may be necessary to ensure that all aspects of tax representation are covered. Below is a list of five commonly used forms and documents in conjunction with the R-7006 form, each with a brief description.

Being aware of these related documents can aid in preparing for tax representation effectively. Having the right forms completed and submitted helps ensure that all necessary authorizations are in place for a smooth tax handling process.

The Tax Power of Attorney (POA) form, commonly known as R-7006, shares similarities with the IRS Form 2848, known as the Power of Attorney and Declaration of Representative. Both forms allow individuals to appoint someone else to act on their behalf concerning tax matters, ensuring that the designated person can communicate directly with tax authorities. They outline the specific rights and powers granted to the representative, permitting them to receive confidential tax information and represent the taxpayer in various tax situations, thus facilitating efficient resolution of tax-related issues.

Another similar document is the IRS Form 8821, known as the Tax Information Authorization. While this form does not grant the same level of authority as a POA, it provides permission for someone to receive tax information on behalf of the taxpayer. The key difference lies in representation; Form 8821 permits access to information without allowing the appointee to represent the taxpayer in dealings with the IRS, making it a more limited tool in terms of authority and capabilities.

State-specific Power of Attorney forms often resemble the R-7006 in that they grant individuals the ability to represent others in various legal and tax matters. Different states have different versions, but the fundamental purpose remains the same: to legally empower someone to act on another person’s behalf. These state POA forms can cover general representation or be tailored specifically to tax matters, emphasizing the necessity of ensuring the document adheres to state-specific requirements.

The IRS Form 706, the United States Estate (and Generation-Skipping Transfer) Tax Return, also shares some similarities in specific circumstances. When handling estate taxes, executors often need to delegate authority to handle tax responsibilities, paralleling the authority granted in a Tax POA. Although primarily a tax return form, the intentions surrounding the delegation of tax-related responsibility are akin, highlighting the need for proper representation during the estate settlement process.

The IRS Form 4506, titled Request for Copy of Tax Return, showcases another connection by allowing an individual to authorize someone else to obtain copies of their tax returns. This resemblance lies in the premise of granting permission, although the scope is limited to retrieving documents rather than representing the taxpayer in communications with the IRS. The authorization process in both scenarios aims to streamline communication regarding tax matters.

The Limited Power of Attorney form often used in financial matters, while different in focus, is similar in function. It allows an individual to delegate specific rights, which can include tax-related decisions. While this form might not always be directed strictly towards tax issues and remains more broad in scope, the fundamental idea of delegating authority empowers individuals to manage their financial and tax-related affairs more efficiently.

Durable Power of Attorney forms are another closely related document. They allow individuals to designate a person to make decisions on their behalf if they become incapacitated. This breadth of authority can extend to tax matters, just like the Tax POA, but the durable aspect provides a safeguard for continuing the appointee's role even when the principal can no longer manage their affairs, ensuring that tax obligations are met without interruption.

Finally, the medical POA form serves as a related document by illustrating how specific powers can be granted for particular situations. Just as the Tax POA empowers someone to act in tax-related contexts, a medical POA empowers an individual to make healthcare decisions for another. Both documents highlight the significance of agency and trust in allowing appointed representatives to act effectively on behalf of someone else, albeit in distinctly different areas of responsibility.

When filling out the Tax Power of Attorney (POA) Form R-7006, it is essential to follow the correct procedures to ensure your form is accepted without issues. Here are ten things you should and shouldn't do:

Following these guidelines will help ensure that your Tax POA form is processed smoothly and that you can effectively manage your tax matters.

The IRS Form R-7006 is a Power of Attorney (POA) form used to grant authority to an individual or organization to represent a taxpayer before the IRS. However, various misconceptions exist about this form. Here are ten common misconceptions:

Understanding these misconceptions can help taxpayers navigate the process more effectively and ensure that they leverage the R-7006 form appropriately.

When filling out and using the Tax POA (Power of Attorney) form R-7006, it is crucial to follow specific guidelines to ensure that the submission is correct and effective. Here are some key takeaways:

Following these guidelines can help streamline the process and enhance communication between the taxpayer and the IRS.