When navigating the complexities of tax matters, understanding the Tax Power of Attorney (POA) Form 101 is essential for both individuals and businesses. It serves as a crucial tool that grants authorized representatives the ability to communicate with the Internal Revenue Service (IRS) on your behalf. This form ensures that your designated agent has the power to handle various tax-related issues, including filing returns, making payments, and discussing personal tax information. Furthermore, it helps streamline processes like audits and appeals, making them more manageable, especially during stressful situations. The Tax POA Form 101 is not just a one-size-fits-all document; it requires specific details such as the taxpayer’s information, the representative’s details, and the scope of authority granted. Additionally, it's important to understand that signing this form does not relinquish your rights or responsibilities regarding your taxes, and you can revoke the power granted at any time. By using the Tax POA Form 101 effectively, you can facilitate communication with the IRS, ensure compliance, and ease the burden of tax-related tasks.

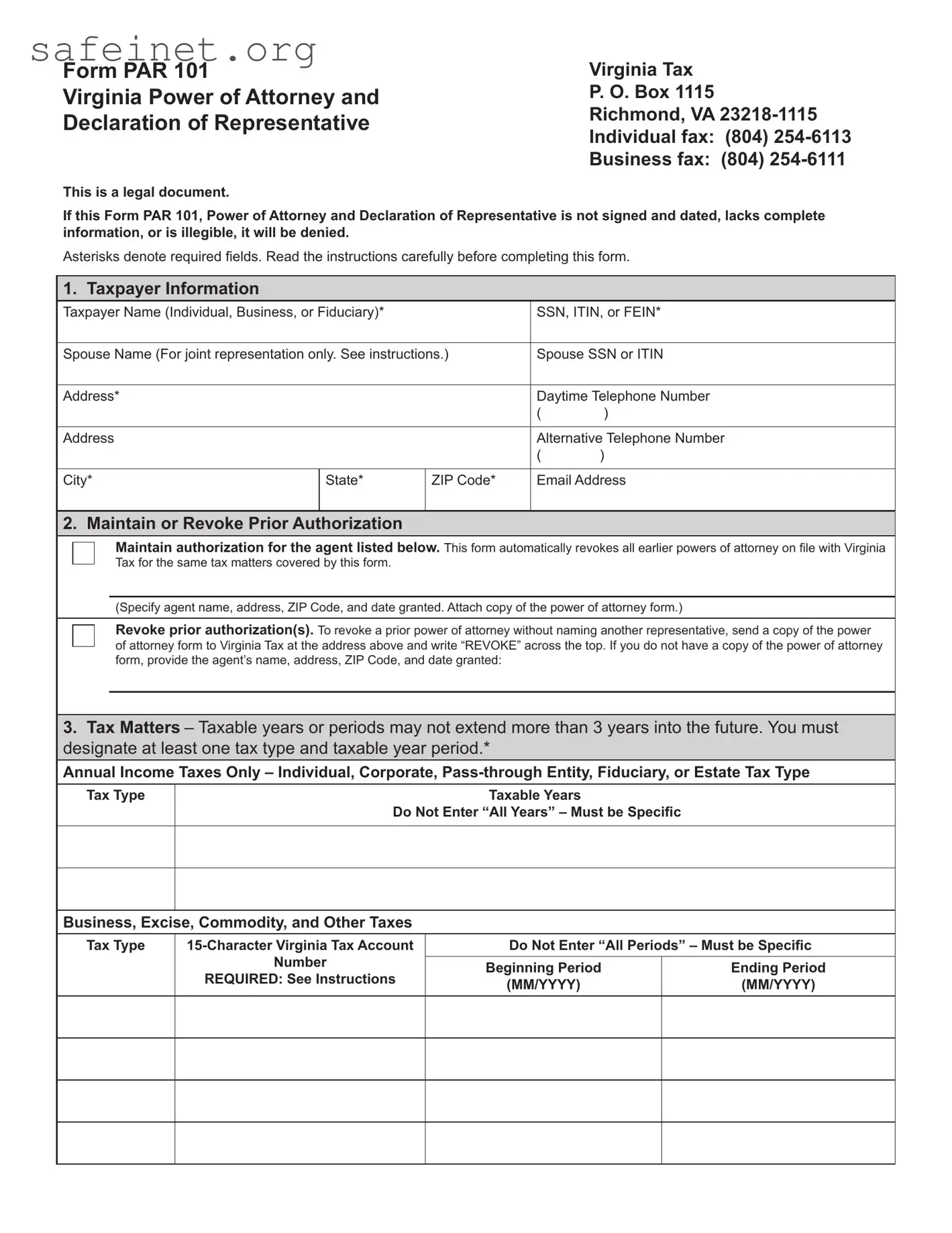

Form PAR 101

Virginia Power of Attorney and

Declaration of Representative

Virginia Tax P. O. Box 1115

Richmond, VA

This is a legal document.

If this Form PAR 101, Power of Attorney and Declaration of Representative is not signed and dated, lacks complete information, or is illegible, it will be denied.

Asterisks denote required fields. Read the instructions carefully before completing this form.

1. Taxpayer Information

Taxpayer Name (Individual, Business, or Fiduciary)* |

|

SSN, ITIN, or FEIN* |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Spouse Name (For joint representation only. See instructions.) |

Spouse SSN or ITIN |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address* |

|

Daytime Telephone Number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

Alternative Telephone Number |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City* |

|

State* |

ZIP Code* |

Email Address |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

2. Maintain or Revoke Prior Authorization |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

Maintain authorization for the agent listed below. This form automatically revokes all earlier powers of attorney on file with Virginia |

||||

|

|

|

|

□ |

|

|

|

|

||||||

|

|

|

|

|

|

|

Tax for the same tax matters covered by this form. |

|

|

|

||||

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

(Specify agent name, address, ZIP Code, and date granted. Attach copy of the power of attorney form.) |

||||

|

|

|

|

|

|

|

|

|

|

Revoke prior authorization(s). To revoke a prior power of attorney without naming another representative, send a copy of the power |

||||

|

|

|

□ |

|

|

|

|

|

||||||

|

|

|

|

of attorney form to Virginia Tax at the address above and write “REVOKE” across the top. If you do not have a copy of the power of attorney |

||||||||||

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

form, provide the agent’s name, address, ZIP Code, and date granted: |

|

|

||

3. Tax Matters – Taxable years or periods may not extend more than 3 years into the future. You must designate at least one tax type and taxable year period.*

Annual Income Taxes Only – Individual, Corporate,

Tax Type |

Taxable Years |

Do Not Enter “All Years” – Must be Specific

Business, Excise, Commodity, and Other Taxes

Tax Type |

Do Not Enter “All Periods” – Must be Specific |

||

|

Number |

|

|

|

Beginning Period |

Ending Period |

|

|

REQUIRED: See Instructions |

||

|

(MM/YYYY) |

(MM/YYYY) |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.Authorized Agent /Representative Information. Additional representatives should be listed on an attached list and may not receive copies of correspondence.

Primary Representative – Must be a person; cannot be a business |

|

Automatic Correspondence |

|||||

First Name* |

Last Name* |

An Authorized Agent will automatically be mailed |

|||||

copies of correspondence regarding the tax |

|||||||

|

|

|

|

|

|||

|

|

|

|

|

|

matters. |

|

Address |

|

|

|

|

|

||

|

|

|

|

A - |

Authorized Agent Number |

||

|

|

|

|

|

_________________________ |

||

Address |

|

|

|

|

|||

|

|

|

|

|

Do NOT mail copies of any correspondence |

||

|

|

|

|

|

□ to agent. |

||

City |

|

State |

|

ZIP Code |

|

Mail copies of email communications to |

|

|

|

|

|

|

□ agent. |

||

Daytime Telephone Number |

Fax Number |

Email Address |

|||||

( |

) |

( |

) |

|

|

|

|

|

|

|

|

||||

Additional Representative – Must be a person; cannot be a business |

|

Automatic Correspondence |

|||||

First Name |

Last Name |

An Authorized Agent will automatically be mailed |

|||||

copies of correspondence regarding the tax |

|||||||

|

|

|

|

|

|||

|

|

|

|

|

|

matters. |

|

Address |

|

|

|

|

|

||

|

|

|

|

A - |

Authorized Agent Number |

||

|

|

|

|

|

_________________________ |

||

Address |

|

|

|

|

|||

|

|

|

|

|

Do NOT mail copies of any correspondence |

||

|

|

|

|

|

|

||

|

|

|

|

|

□ to agent. |

||

City |

|

State |

|

ZIP Code |

|

Mail copies of email communications to |

|

|

|

|

|

|

□ agent. |

||

Daytime Telephone Number |

Fax Number |

Email Address |

|||||

( |

) |

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

5. Signature of Taxpayer(s) and Acknowledgment of Authorized Acts

By signing this form, I am granting the representative(s) listed in Section 4 the authority to:

•Receive and inspect my confidential tax information for the tax matters listed in Section 3,

•Perform all acts that I can perform with respect to the specified tax matters, and

•Represent me before Virginia Tax, including consenting to extend the time to assess tax and executing consents that agree to a tax adjustment.

•In addition, I understand that the acts of my Authorized Agent may increase or decrease my tax liabilities and legal rights.

The authority does not, however, include the power to receive refund checks, substitute another representative, request a copy of a tax return, sign certain returns, or consent to a disclosure of tax information.

For joint representation, both the taxpayer and the spouse listed in Section 1 must sign and date this form. If this form is signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, they certify that they have the authority to execute this form on behalf of the taxpayer. This power of attorney will remain in effect until it is revoked by either the taxpayer or the agent.

Print Name*

Print Name

Signature* |

Title |

Date* |

Signature |

Title |

Date |

|

|

|

6.Representative Signature: Under penalties of perjury, I declare I am authorized to represent the taxpayer(s)

listed in Section 1.

A.) Attorney B.) Certified Public Accountant C.) Enrolled Agent D.) Family member or Other (provide relationship below):

Relationship: ____________________________________________________________________________________

|

Designation |

|

|

|

Representative |

Letter from |

Print Name * |

Representative Signature* |

Date* |

|

Above List |

|

|

|

Primary |

|

|

|

|

|

|

|

|

|

Additional |

|

|

|

|

|

|

|

|

|

INSTRUCTIONS FOR VIRGINIA FORM PAR 101

POWER OF ATTORNEY AND DECLARATION OF REPRESENTATIVE

Form Purpose

Use Form PAR 101 to:

•Authorize a person to represent you before Virginia Tax with respect to the tax matters you specify, or

•Revoke a prior power of attorney authorization.

THIS IS A LEGAL DOCUMENT: When you submit Form PAR 101, you are authorizing the person you name in Section 4 to be your representative. For the tax matters you specify in Section 3, your representative will be able to receive and inspect your confidential tax information and perform any and all acts you can perform, including consenting to extend the time to assess tax or executing consents that agree to a tax adjustment. The acts of your representative may increase or decrease your tax liabilities and legal rights. Certain exceptions apply. See below.

When to submit Form PAR 101:

The following are examples of when you need to complete and submit Form PAR 101:

1.You are disputing an assessment of tax and a third party is representing you before Virginia Tax,

2.You have been notified that we will be conducting an audit of your account and you have engaged the services of a third party to assist with the audit, or

3.You are the administrator of a deceased individual’s estate and you need to grant access to the decedent’s confidential tax information to a third party in order to perform your duties.

The above list is not

When a Form PAR 101 is NOT required:

Form PAR 101 is not required when a person merely furnishes information or prepares a report or return for you or your business. For example, you do not need to submit Form PAR 101 to:

1.Authorize a tax professional (CPA, Enrolled Agent, tax preparer, or payroll service provider) to discuss routine issues regarding return filings and payments the tax professional submitted on your behalf,

2.Authorize an employee or officer of your business to discuss routine issues regarding return filings and payments submitted by your business, or

3.Authorize a fiduciary (trustee, receiver, or guardian) to act as Authorized Agent, because a fiduciary already stands in the position of the taxpayer.

Virginia Tax will discuss routine issues regarding return filings and payments and related assessments and adjustments with your designated tax professionals and the

employees and officers of a business, provided we are able to verify the person and the person’s relationship to you or your business.

Exceptions - The power of attorney you grant to your representative using Form PAR 101 does not include the power to receive refund checks, the power to substitute another representative, the authority to execute a request for a tax return, the power to sign certain returns for you, or the power to consent to a disclosure of tax information.

Section 1 - Taxpayer Information

Individual - If the tax matter involves a joint return and you and your spouse are designating the same representative, provide your spouse’s name and social security number.

Sole Proprietor - For business tax matters, enter your name and the federal employer identification number for your business.

Corporations, Partnerships, or Associations - Enter the legal name of the organization and the organization’s federal employer identification number. If the tax matter involves a consolidated or a combined tax return filed for a corporation, do not attach a list of subsidiaries or affiliated corporations to this form. Only the parent corporation‘s information is required in Section 1. A subsidiary or affiliate must file its own PAR 101 for returns that it files separately.

Fiduciary/Trust - Enter the name and federal employer identification number of the trust, and the telephone number and email address of the trustee. The trustee must sign the form.

Estate or Inheritance Tax - Applicable only for decedents whose date of death was prior to July 1, 2007. Enter the name and the social security number of the deceased taxpayer and provide the address, telephone number, and email address of the decedent’s personal representative. The taxpayer’s personal representative must sign and date the form.

Section 2 - Revoking or Maintaining Prior Authorization

Check the box that applies. If you are naming a representative, any prior power of attorney on file with Virginia Tax for the same tax matters covered by the Form PAR 101 you are submitting will be automatically revoked unless you attach a copy of any power of attorney you want to remain in effect.

Either the taxpayer or their representative may revoke the power of attorney. This must be done in writing by submitting a copy of Form PAR 101 with “REVOKE” written on the top of the form or by sending a written request. If you wish to revoke the power of attorney for only one spouse on a joint power of attorney, this should be done by a submitting a letter to indicate which spouse is no longer represented.

Section 3 - Tax Matters

Be specific. You should only grant a person your power of attorney for taxable periods for which you have a tax matter.

You may specify taxable periods no more than 3 years into the future. Future periods are determined starting after Dec. 31 of the year in which we receive Form PAR 101. You may list the current taxable year or period and any taxable years or periods that have already ended as of the date you sign Form PAR 101.

Annual Income Taxes - If the tax matter involves individual, corporate,

Business, Excise, Commodity, and Other Taxes - You must enter the tax type and the beginning and ending periods covered by this form. For each tax type, you must also provide your assigned

Exceptions - For the following tax types, leave the Virginia Tax Account Number field blank: Apple Excise Tax, Bank Franchise Tax, and Rolling Stock Tax on Railroads and Freight Car Companies.

Section 4 - Authorized Agent/Representative Information

You must provide complete information for each representative listed on the form. You cannot name a business as your representative. Your representative must be a person. In addition, each representative must sign and date the form. The signature must be an actual signature and cannot be an electronic signature or rubber stamp.

Virginia Tax will automatically mail copies of all outgoing correspondence sent to you regarding the tax matters listed in Section 3 to your Authorized Agent provided that:

•Your Authorized Agent is registered with Virginia Tax, and

•You provide the Authorized Agent’s number, a unique

Virginia Tax will not automatically mail correspondence to your Authorized Agent in the following situations:

•You do not provide your Authorized Agent’s number, or

•You check the box indicating that you do not want correspondence automatically mailed to your Authorized Agent.

We will automatically mail copies of secure email to your Authorized Agent if you have opted to have copies of email communications sent to your agent.

Taxpayers may use secure email to discuss specific questions related to their account. The authorized representative(s) will receive copies of this secure email communication through the U.S mail. To use secure email on Virginia Tax’s website at www.tax.virginia.gov, log in to iFile (business or individual) or iReg, select Secure Message to send and receive secure email.

To register as an Authorized Agent, your representative must submit Virginia Form

www.tax.virginia.gov.

Sections 5 and 6 - Signature of Taxpayer(s),

Acknowledgment of Authorized Acts, and

Representative Signature

Individuals - You must sign and date the form. If the tax matter involves a joint return and you and your spouse are designating the same Authorized Agent(s), your spouse must also sign and date the form.

Corporations or Associations - An officer having authority to bind the taxpayer must sign and date the form.

Partnerships - All partners should sign unless only one partner is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if, under state law, the partner has authority to bind

the partnership. A copy of such authorization should be attached. For dissolved partnerships, see 26 CFR 601.503(c)(6).

All others - If the taxpayer is a dissolved corporation, decedent, insolvent, or a person for whom or by whom a fiduciary (a trustee, guarantor, receiver, executor, or administrator) has been appointed, see 26 CFR 601.503(d).

The representative(s) must sign and date the form.

Note - Generally, the taxpayer signs first, granting the authority and then the Authorized Agent signs, accepting the authority granted. The date for both the taxpayer and the representative must be within 45 days for domestic authorizations and within 60 days for authorization from taxpayers residing abroad. If the taxpayer signs last, then there is no timeframe requirement.

All signatures on the form must be actual and cannot be electronic or rubber stamps.

* * * * *

Mail or fax the completed form and enclosures to:

Virginia Tax

P.O. Box 1115

Richmond, Virginia

Business fax: (804)

Individual fax: (804)

For individual assistance call: (804)

For business assistance call: (804)

| Fact Name | Description |

|---|---|

| What is Tax POA? | The Tax Power of Attorney (Tax POA) form allows an individual to authorize someone else to represent them before tax authorities. |

| Common Uses | This form is often used for handling tax issues, disputes, and communications with revenue agencies. |

| Who Can be Authorized? | Any individual, such as a tax consultant or family member, can be appointed as an agent. |

| Signature Requirement | The individual granting the power must sign the form, ensuring consent. |

| State Variations | Some states may have their own versions of the Tax POA form that comply with local laws. |

| Revocation of Authority | The grantor can revoke the power at any time by notifying the authorized agent and the tax authority. |

| Confidentiality | Agents must respect privacy and handle all tax-related information confidentially. |

| Governing Laws | Each state governs the Tax POA process through their own tax statutes; ensure compliance with local regulations. |

| Validity Period | The Tax POA remains valid until revoked or upon the death of the individual who appointed the agent. |

| Submission Process | The completed form must be submitted directly to the relevant tax authority to be effective. |

When completing the Tax Power of Attorney (POA) Form PAR 101, ensure that you have all necessary information readily available. The process will involve providing details about your identity and the representative you are designating. Each step is essential for ensuring that the form is filled out accurately, which helps facilitate smooth communications regarding your tax matters.

Once the Tax POA Form PAR 101 is filled out, review it to ensure accuracy. After verification, submit the form according to the instructions provided—this may include mailing it to the appropriate tax office or emailing it, depending on your location and tax situation.

What is the Tax POA Form PAR 101?

The Tax Power of Attorney Form PAR 101 allows you to authorize an individual, typically a tax professional, to act on your behalf regarding tax matters. By completing this form, you grant authority to the designated representative to handle specific issues with tax authorities, such as filing returns, addressing tax notices, and discussing your tax situation. This streamlines communication between you and the tax agency, ensuring that your representative can effectively manage your tax responsibilities.

Who should complete the Tax POA Form PAR 101?

Anyone who needs assistance with their tax matters may consider filing the Tax POA Form PAR 101. This includes individuals who are unable to handle their tax affairs due to time constraints, lack of tax knowledge, or other valid reasons. Additionally, if you want a tax professional to represent you during an audit or other dealings with tax authorities, completing this form is essential. You can appoint anyone you trust, whether that's a certified tax preparer, attorney, or another trusted individual.

What information is required to complete the form?

Completing the Tax POA Form PAR 101 involves providing specific information about both you and your designated representative. You will need to include your name, address, and Social Security number or taxpayer identification number. Additionally, you'll need to enter the representative's details, including their name, address, and contact information. The form may also require you to specify the scope of the authority you are granting and any limitations you wish to set on their representation.

How long is the Tax POA Form PAR 101 valid?

The Tax POA Form PAR 101 remains valid until you revoke it or until the tax matter for which it was filed is resolved. If you decide to cancel the Power of Attorney, you must submit a revocation form to the same tax authority or communicate this change in writing. It’s important to monitor your taxation matters regularly and ensure that your representation aligns with your current needs. Regular updates to the form can help maintain clear and effective communication.

Incorrect Identification Information: Filling out the form with incorrect names or Social Security Numbers can cause delays or rejection.

Missing Signatures: Forgetting to sign the form or missing the signature of the representative can invalidate the request.

Not Specifying the Type of Authorization: Failing to indicate whether this is a general or specific power of attorney can lead to confusion.

Improper Date Entries: Dates must accurately reflect when the power of attorney is granted. Incorrect dates can affect the validity.

Failure to Provide Contact Information: Omitting phone numbers or addresses may hinder communication with the IRS.

Inaccurate Representative Information: If the appointed representative's details are wrong, the IRS may not recognize them as authorized.

Neglecting to Keep Copies: Not keeping a copy of the submitted form can pose problems if issues arise later.

Filing in the Wrong Manner: Submitting the form through the wrong channel can lead to unnecessary delays.

Inadequate Understanding of Limitations: Misunderstanding the limits of what the power of attorney covers can lead to overreach or confusion.

When filing taxes or engaging with the Internal Revenue Service (IRS), individuals and businesses may often use various forms and documents alongside the Tax Power of Attorney (Tax POA) form, also known as Form 2848. Below is a list of commonly associated documents that can aid in the tax process.

Utilizing these documents appropriately can facilitate effective communication with the IRS and support the overall filing process. Each form serves a specific purpose and may be necessary depending on the individual circumstances of the taxpayer.

The IRS Form 2848, Power of Attorney and Declaration of Representative, allows individuals to authorize someone to represent them before the IRS. Much like the Tax POA form par 101, this document grants the designated representative the authority to act on behalf of the taxpayer in dealing with tax matters. It provides flexibility in appointing individuals, which can include attorneys, CPAs, or other qualified representatives. Both forms enable supporters to handle tax issues, but Form 2848 is specifically tailored for interactions with the IRS.

An equivalent form is the IRS Form 8821, Tax Information Authorization, which also pertains to tax matters. While the Tax POA form par 101 allows a representative to act on a taxpayer's behalf, Form 8821 solely gives permission to receive tax information without the authority to act in the taxpayer's stead. This form is useful for those who need their financial details shared with a third party without granting them full power of attorney.

Another related document is the Limited Power of Attorney, often used in various legal contexts. Similar to the Tax POA form par 101, a Limited Power of Attorney grants authority to a person for specific tasks, such as managing financial matters or signing tax returns. However, unlike the broad authority provided by the Tax POA, the Limited Power of Attorney confines the appointed individual to predetermined responsibilities, making it a more restrictive option.

The Durable Power of Attorney is a document that remains effective even if the person who created it becomes incapacitated. Like the Tax POA form par 101, it enables continuous representation in legal and financial affairs. However, the major distinction lies in its scope. The Durable Power of Attorney can cover a wide array of financial matters beyond just taxes, ensuring that the designated individual can act even when the principal cannot.

The Medical Power of Attorney is another variant that allows a person to make medical decisions on behalf of another. While it does not pertain to tax issues, it shares the concept of designating authority to another party. Like the Tax POA form par 101, it must be legally executed and is based on trust that the appointed representative will make decisions in the best interest of the individual.

State-specific Power of Attorney forms often function similarly to the Tax POA form par 101. Each state may have its unique version of a Power of Attorney, which can cover various domains, including financial, medical, or tax-related matters. These forms are tailored to meet local laws but fulfill the same foundational purpose of allowing someone to act on another's behalf.

The Corporate Power of Attorney is commonly used in the business context. This document authorizes an agent to act on behalf of a corporation, usually for specific business or financial decisions. While the Tax POA form par 101 is tailored for individual tax matters, both documents address the delegation of authority, ensuring that business or personal affairs can be effectively managed through trusted representatives.

Finally, the General Power of Attorney provides a broad authority to an agent to act on someone else's behalf. Similar to the Tax POA form par 101, it allows a designated person to manage various affairs, including financial and tax-related issues. However, the General Power of Attorney does not have the same focus on tax matters, covering a more extensive range of responsibilities. This makes it a versatile option that may not be as tailored as the Tax POA form par 101.

When filling out the Tax Power of Attorney (POA) Form 101, attention to detail is essential. To help you navigate this process, here are ten dos and don’ts that will make completing the form smoother and more successful.

By following these guidelines, you can minimize errors and ensure a smoother experience when filing your Tax POA Form 101.

Understanding the Tax Power of Attorney (POA) Form 101 can be complicated. Here are some common misconceptions surrounding it:

Only certain individuals are authorized to represent you before the IRS. This typically includes licensed attorneys, certified public accountants (CPAs), and enrolled agents.

The powers granted depend on what you specify in the POA form. You can limit the authority based on the tax matters and time frame you choose.

The POA is not forever. It remains in effect until you revoke it, or the IRS processes a new form that replaces it.

The Tax POA Form 101 is specific to tax matters. A general POA allows broader powers and responsibilities beyond tax issues.

In many cases, the person representing you must also sign the form to validate their authority.

Even when filing jointly, each spouse needs to authorize representation through a separate POA if both are involved in discussions or dealings with the IRS.

While there is no fee for filing the form with the IRS, you may incur costs associated with hiring a representative to assist you.

You can submit the Tax POA electronically, provided you follow the IRS guidelines and the representative meets e-filing requirements.

Simply submitting the POA does not mean the IRS knows of your specific request. Ensure you communicate any necessary details related to your tax situation.

Understanding these misconceptions can help you navigate the process of granting someone power of attorney for your tax matters more effectively.

The Tax POA (Power of Attorney) form is essential for tax-related matters. Using this form allows you to authorize someone else to act on your behalf regarding tax issues. Here are key takeaways to keep in mind: