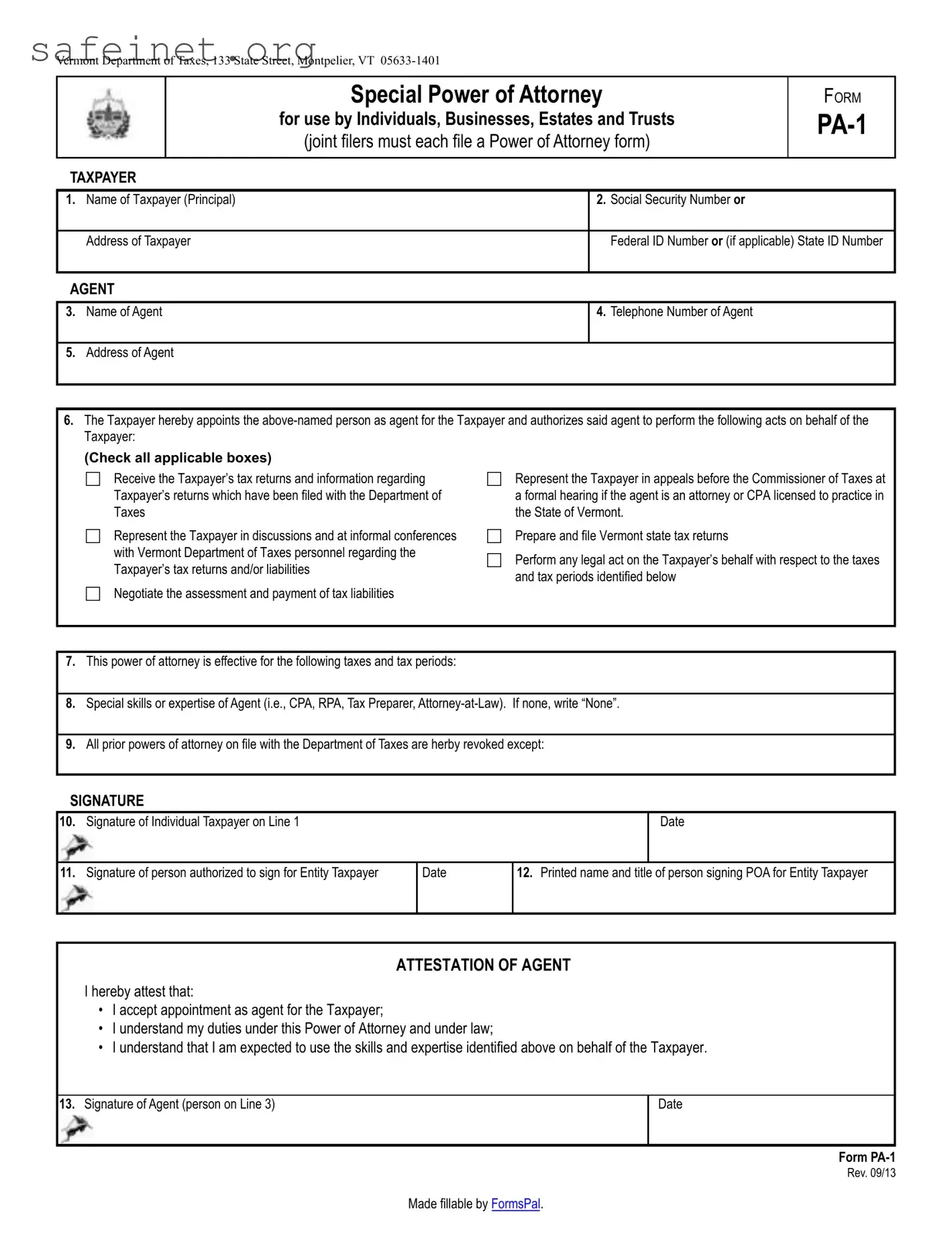

The Tax POA Form PA-1 is an essential document for anyone looking to designate a representative to act on their behalf regarding tax matters in Pennsylvania. This form provides legal authority, allowing an appointed individual to receive confidential information, communicate with the Department of Revenue, and manage tax-related issues on behalf of the taxpayer. Whether it's a tax advisor, family member, or another trusted individual, the form facilitates streamlined interaction between the taxpayer and the state. It covers various topics such as the specific powers granted to the representative, the need for taxpayer consent, and the importance of using the correct identification details. By completing and submitting the PA-1 form, taxpayers can ensure that their interests are effectively managed while maintaining compliance with state requirements. Proper use of this form not only simplifies tax processes but also safeguards the taxpayer’s rights and information.

Vermont Department of Taxes, 133 State Street, Montpelier, VT

|

|

|

Special Power of Attorney |

|

FORM |

|

|

|

|

for use by Individuals, Businesses, Estates and Trusts |

|||

|

|

|

(joint filers must each file a Power of Attorney form) |

|

||

TAXPAYER |

|

|

|

|

||

1. |

Name of Taxpayer (Principal) |

|

2. |

Social Security Number or |

|

|

|

|

|

|

|

||

|

Address of Taxpayer |

|

|

Federal ID Number or (if applicable) State ID Number |

||

|

|

|

|

|

||

AGENT |

|

|

|

|

||

|

|

|

|

|

|

|

3. |

Name of Agent |

|

4. |

Telephone Number of Agent |

|

|

|

|

|

|

|

|

|

5. |

Address of Agent |

|

|

|

|

|

|

|

|

|

|

|

|

6. The Taxpayer hereby appoints the

|

Taxpayer: |

|

|

(Check all applicable boxes) |

|

|

Receive the Taxpayer’s tax returns and information regarding |

Represent the Taxpayer in appeals before the Commissioner of Taxes at |

|

Taxpayer’s returns which have been filed with the Department of |

a formal hearing if the agent is an attorney or CPA licensed to practice in |

|

Taxes |

the State of Vermont. |

|

Represent the Taxpayer in discussions and at informal conferences |

Prepare and file Vermont state tax returns |

|

with Vermont Department of Taxes personnel regarding the |

Perform any legal act on the Taxpayer’s behalf with respect to the taxes |

|

Taxpayer’s tax returns and/or liabilities |

|

|

and tax periods identified below |

|

|

Negotiate the assessment and payment of tax liabilities |

|

|

|

|

|

|

|

|

|

|

7. |

This power of attorney is effective for the following taxes and tax periods: |

|

|

|

|

8. |

Special skills or expertise of Agent (i.e., CPA, RPA, Tax Preparer, |

|

|

|

|

9. |

All prior powers of attorney on file with the Department of Taxes are herby revoked except: |

|

|

|

|

SIGNATURE |

|

|

10. |

Signature of Individual Taxpayer on Line 1 |

Date |

? |

|

|

|

|

|

11. |

Signature of person authorized to sign for Entity Taxpayer |

|

Date |

12. Printed name and title of person signing POA for Entity Taxpayer |

|

?- |

|

|

|

|

|

|

|

|

|

||

|

|

ATTESTATION OF AGENT |

|||

|

I hereby attest that: |

|

|

|

|

|

• I accept appointment as agent for the Taxpayer; |

|

|

|

|

|

• I understand my duties under this Power of Attorney and under law; |

|

|

||

|

• I understand that I am expected to use the skills and expertise identified above on behalf of the Taxpayer. |

||||

|

|

|

|

|

|

13. |

Signature of Agent (person on Line 3) |

|

|

|

Date |

|

|

|

|

|

|

Form

Rev. 09/13

Made fillable by FormsPal.

INSTRUCTIONS FOR COMPLETING VERMONT DEPARTMENT OF TAXES

SPECIAL POWER OF ATTORNEY (POA).

•This form may be used by individuals, businesses, estates and trusts. Joint income tax filers must each complete and file a power of attorney form.

•All POA forms submitted to the Department of Taxes must comply with the requirements of chapter 123 of Title 14, except that signatures of a witness and notary are not required.

•POA forms must be signed by the agent. THE DEPARTMENT OF TAXES WILL NOT ACCEPT A POA UNLESS

SIGNED BY THE AGENT.

•By signing, an agent attests that he/she accepts appointment as agent and understands the duties of agent, both under the POA and under the law. In addition, if special skills or expertise of the agent are identifed, the agent must attest that he/ she understands that he/she is expected to use those skills and expertise on behalf of the Taxpayer.

1.Print the name and address of the Taxpayer.

2.Enter the Social Security Number of an individual Taxpayer or Federal ID Number or (if applicable) State ID Number of an entity Taxpayer.

3.Print the name of the Agent.

4.Print the telephone number of the Agent.

5.Print the address of the Agent.

6.Check applicable boxes if you are authorized to prepare and file Vermont state tax returns, the returns must still be signed by the taxpayer.

7.List specific tax types (i.e., “income tax”) and tax periods (i.e., “2002”) for which Agent is authorized to

act on your behalf. If all taxes and tax periods, write “ALL”.

8.Identify any special skills or expertise of Agent which will be exercised by agent on behalf of Taxpayer, such as CPA, RPA, tax preparer,

9.List any prior Powers of Attorney on file with the Department of Taxes which are NOT revoked.

10.Signature of person on Line 1 if an individual Taxpayer.

11.Signature of person signing for an entity Taxpayer.

12.Print the name and title of person signing for an entity taxpayer.

13.Signature of Agent and date agent signed.

| Fact Name | Details |

|---|---|

| Purpose | The Tax POA Form PA-1 authorizes a representative to act on behalf of a taxpayer concerning tax matters in Pennsylvania. |

| Governing Law | This form is governed by the Pennsylvania Department of Revenue regulations and state tax laws. |

| Eligibility | Any taxpayer may use the PA-1 form to grant power of attorney to individuals or organizations for specific tax-related issues. |

| Submission Requirements | The completed form must be submitted to the Pennsylvania Department of Revenue. No additional document is required for its validity. |

| Revocation | The taxpayer can revoke the power of attorney at any time by submitting a written notice to the Department of Revenue. |

To proceed with filling out the Tax POA form PA-1, gather all necessary information before starting. This will ensure a smooth process. Follow these steps carefully to complete the form and prepare it for submission.

What is the Tax POA Form PA-1?

The Tax POA Form PA-1 is a Power of Attorney form specifically designed for taxpayers in Pennsylvania. This form allows you to designate another individual, such as a family member or a tax professional, to act on your behalf in tax matters concerning the Pennsylvania Department of Revenue. By granting this authority, you enable your representative to communicate with the tax authorities and make decisions regarding your tax situation.

Who can be appointed as my representative?

You can choose any individual as your representative as long as they are not disqualified by the Pennsylvania Department of Revenue. Typically, people select tax preparers, accountants, lawyers, or trusted family members. Just ensure that the person you appoint is willing to accept this responsibility and is knowledgeable about your tax issues.

How do I fill out the PA-1 form?

To complete the PA-1 form, you'll need to provide basic information such as your name, address, Social Security number or EIN, and details about the person you are appointing. You will also specify the scope of the authority you are granting and sign the form to confirm your decision. Pay attention to the instructions included with the form for guidance on each section.

Is there a fee to file the PA-1 form?

There is no fee associated with filing the PA-1 form. This form is designed to facilitate efficient communication between you and the Pennsylvania Department of Revenue. Therefore, you can submit it without incurring any costs.

Where should I send the completed PA-1 form?

Once you have completed and signed the PA-1 form, you can submit it to the Pennsylvania Department of Revenue. Generally, you can send the form by mail or, in certain cases, submit it electronically through the department's online services. Check the Pennsylvania Department of Revenue’s official website for the most current submission options and addresses.

How long does it take for the PA-1 form to be processed?

Processing times can vary based on the current workload of the Pennsylvania Department of Revenue. Typically, it may take anywhere from a few days to several weeks for the department to process your submitted PA-1 form. Once processed, you and your representative will receive confirmation of the authorization.

Can I revoke the POA once it is granted?

Yes, you have the right to revoke the Power of Attorney at any time. To do this, you must submit a written notice of revocation to the Pennsylvania Department of Revenue. It’s best to inform your representative as well, so they are aware that their authority has been terminated.

What should I do if my representative and I disagree about tax matters?

If a disagreement arises between you and your appointed representative, it's important to communicate openly. You can also choose to revoke their authority using the process outlined earlier. If necessary, you might consider consulting a different professional or contacting the Pennsylvania Department of Revenue for guidance on your specific situation.

Do I need to attach any additional documents with the PA-1 form?

In most cases, you do not need to attach any documents when submitting the PA-1 form. However, if your tax situation is particularly complex or involves additional forms, it might be helpful to include any relevant documentation. Refer to the form's instructions for any specifics regarding additional attachments.

Filling out the Tax Power of Attorney (POA) Form PA-1 can be a straightforward process, but many individuals encounter common pitfalls. Understanding these mistakes can help ensure that the form is completed accurately. Here’s a list of eight mistakes to avoid:

Incorrect Personal Information: Providing the wrong name, address, or tax identification number can lead to significant delays in processing.

Missing Signatures: All required signatures must be present. Omitting a signature will render the form invalid and could prevent the designated representative from acting on your behalf.

Choosing the Wrong Type of Authority: It’s essential to select the correct powers you wish to grant. Misunderstanding these options can result in your representative having either too much or too little authority.

Not Specifying an Expiration Date: Failing to include an expiration date can lead to confusion or unintended consequences, as the authorization might remain in effect longer than intended.

Submitting Copies Instead of Originals: Always submit original forms rather than photocopies, as tax authorities typically require original documents for processing.

Neglecting to Check for Changes in the Law: Tax laws can change frequently. Staying updated will help in completing the form correctly according to the latest regulations.

Failing to Notify the Appointee: Make sure to inform the person you are appointing. They need to be aware that they are acting as your representative.

Inadequate Review Before Submission: Double-checking the entire form for errors or omissions before sending it off is crucial. Errors that go unnoticed can cause delays or complications.

By avoiding these common mistakes, you can improve the likelihood that your Tax POA form PA-1 is processed without issues, ultimately making tax matters easier to manage.

When dealing with tax matters, various forms and documents come into play alongside the Tax Power of Attorney (POA) form PA-1. Understanding these documents helps individuals navigate their tax responsibilities more effectively. Below is a list of key forms often used in conjunction with the PA-1.

By gathering these documents along with the Tax POA form PA-1, taxpayers can streamline their interactions with the IRS and ensure that all necessary information is readily available. Knowledge of these forms empowers individuals to handle their tax situations with confidence.

The Tax Power of Attorney (POA) Form PA-1 is notably similar to the IRS Form 2848, which serves a similar purpose at the federal level. Just like the PA-1, the IRS Form 2848 allows taxpayers to appoint someone to represent them before the IRS. This could be a tax professional, family member, or anyone authorized to handle tax matters in an official capacity. Both forms require the taxpayer’s signatures and the representative's details, ensuring that the designated person can access information regarding tax filings and make decisions on behalf of the taxpayer.

Another document that shares similarities with the PA-1 is the IRS Form 8821, which is a Tax Information Authorization. While both the PA-1 and Form 8821 involve sharing tax-related responsibilities, the key difference lies in the extent of authority granted. The PA-1 gives broad powers to the representative, allowing them to act on the taxpayer's behalf in various tax matters. In contrast, Form 8821 focuses solely on the permission to receive information from the IRS but does not authorize the representative to act on the taxpayer's behalf.

The durable power of attorney (DPOA) is yet another document that resembles the PA-1. This legal document allows someone to make decisions on behalf of another person. Just like the Tax POA, a DPOA can be specific or general in nature. While a DPOA can cover a wide range of responsibilities—including financial and medical decisions—the PA-1 is specifically tailored for tax issues, giving the representative authority directly related to taxes without overreaching into other personal affairs.

Similar to the PA-1, the state-specific tax power of attorney forms serve taxpayers who want to appoint a representative for state taxation matters. These forms are often variations of the PA-1 designed to cover state tax issues. Depending on the state, these forms might require different information or follow different rules, but the underlying function remains the same: to authorize someone to act on the taxpayer's behalf regarding state tax responsibilities.

The power of attorney for medical decisions also aligns conceptually with the PA-1, albeit in a healthcare context. This document allows a trusted individual to make medical decisions on behalf of someone who may be incapacitated or unable to express their wishes. Like the PA-1, this document emphasizes trust and provides clear lines of authority, showing that, while they serve different purposes, both involve designating someone to act on behalf of another.

The financial power of attorney (FPOA) shares a resemblance with the PA-1 too. This document grants someone authority to manage financial matters, including bank transactions, investments, and real estate decisions. Similar to the PA-1, the FPOA enables a designated individual to act for someone else, with a clear focus on financial implications rather than tax-specific concerns.

Another document is the General Durable Power of Attorney, which creates a broad authority for the appointed agent. This is akin to the PA-1, where the authority to act is extended directly to tax issues. While the general power can cover any legal, financial, or personal matters, the PA-1 remains specific to tax liabilities, filings, and communications with relevant authorities.

The Form 56, Notice Concerning Fiduciary Relationship, is another relevant document. While it doesn't function as a power of attorney per se, it is somewhat similar to the PA-1 in that it acknowledges a representative's responsibility in handling a taxpayer's affairs. Form 56 is used to inform the IRS of a fiduciary relationship, allowing a representative to manage tax obligations. However, it doesn't confer the same level of direct power that the PA-1 does.

Lastly, session-based agreements or letters of authorization often bear similarities to the PA-1 form. These documents allow brief, limited authorization for someone to act on a taxpayer’s behalf, particularly in specific situations like resolving a single tax year’s issue. While they may not offer permanent power like the PA-1, they do share the goal of facilitating communication and representation between taxpayers and the authorities involved.

When completing the Tax Power of Attorney (POA) Form PA-1, it’s essential to be careful and thorough. Here are five things to consider doing and avoiding.

Understanding the Tax Power of Attorney (POA) form PA-1 is crucial for taxpayers. However, several misconceptions can create confusion. Below is a list of ten common misconceptions about the Tax POA form PA-1.

Correcting these misconceptions is essential for ensuring that taxpayers understand their rights and responsibilities when dealing with tax matters.

Filling out and using the Tax POA Form PA-1 is essential for managing tax matters effectively. Here are ten key takeaways to consider: