The Tax Power of Attorney (POA) Form N-848 serves as a crucial tool for individuals seeking assistance in their tax matters, particularly concerning representation before the Internal Revenue Service (IRS). This form allows taxpayers to designate an individual or entity to act on their behalf, facilitating communication with the IRS and streamlining the handling of tax-related issues. By submitting the N-848, taxpayers can ensure that their representatives have the authority to discuss confidential tax information, such as income, deductions, and credits. Furthermore, the form enables the designated representative to receive IRS notices and respond to inquiries, providing a layer of convenience and expertise that can be vital during audits or disputes. The procedure for completing and submitting Form N-848 is straightforward, yet it includes specific requirements that need attention to ensure effectiveness and compliance with IRS regulations. Understanding the significance and functionality of this form can empower taxpayers to manage their tax affairs more efficiently while maintaining peace of mind during potentially stressful situations.

FORM

(REV. 2018)

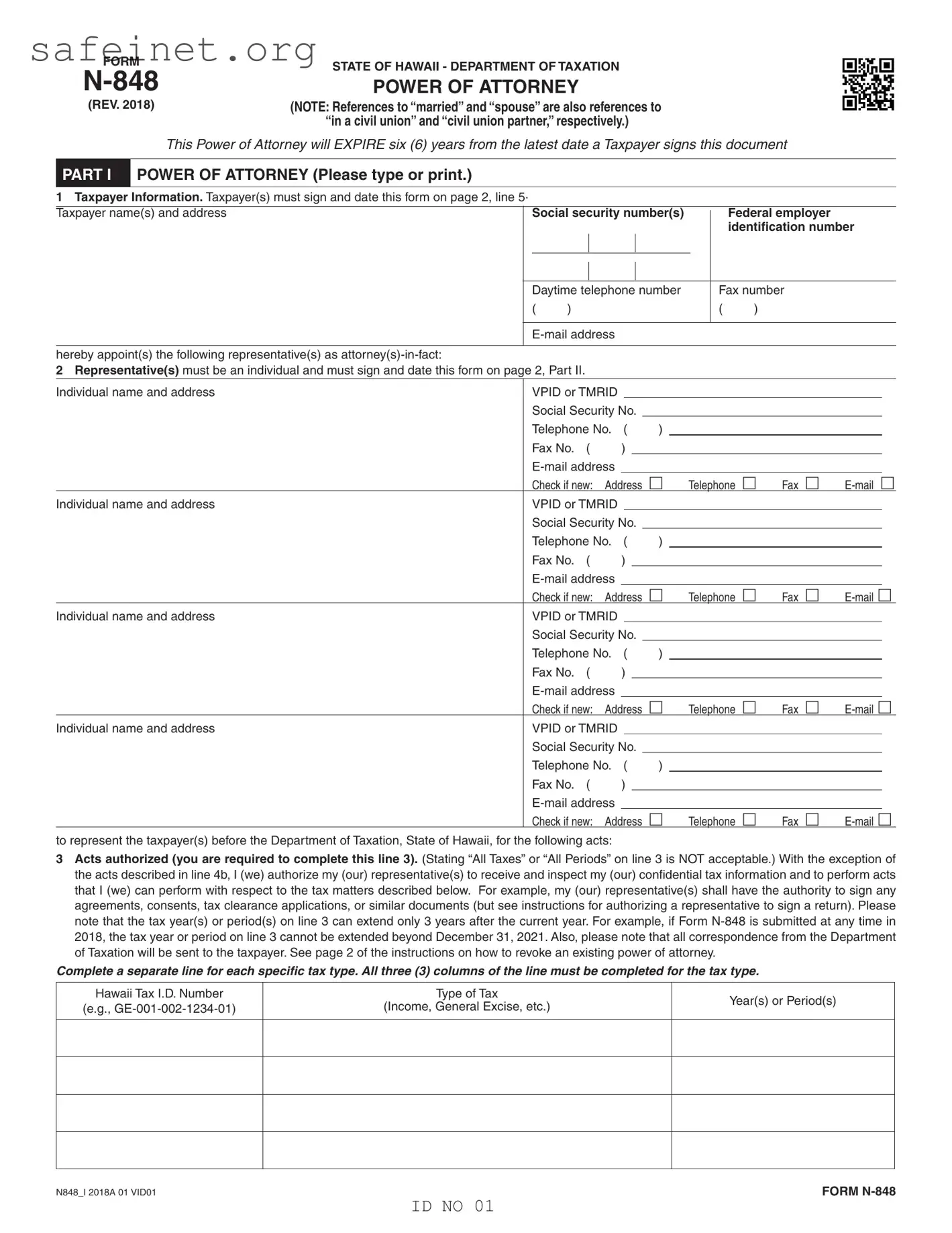

STATE OF HAWAII - DEPARTMENT OF TAXATION

POWER OF ATTORNEY

(NOTE: References to “married” and “spouse” are also references to “in a civil union” and “civil union partner,” respectively.)

This Power of Attorney will EXPIRE six (6) years from the latest date a Taxpayer signs this document

PART I POWER OF ATTORNEY (Please type or print.)

|

1 Taxpayer Information. Taxpayer(s) must sign and date this form on page 2, line 5. |

Social security number(s) |

Federal employer |

|||||

|

Taxpayer name(s) and address |

|||||||

|

|

|||||||

|

|

|

|

|

|

|

identification number |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daytime telephone number |

Fax number |

||||

|

|

|

( ) |

( ) |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

hereby appoint(s) the following representative(s) as |

|

|

|

|

|

|

|

2Representative(s) must be an individual and must sign and date this form on page 2, Part II.

Individual name and address |

VPID or TMRID |

|

|

|

|

|

|

|

|

|

|||

|

Social Security No. |

|

|

|

|

|

|

|

|

|

|||

|

Telephone No. ( ) |

|

|

|

|

|

|

|

|

||||

|

Fax No. ( ) |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

Check if new: Address |

|

Telephone |

|

Fax |

|

|||||||

Individual name and address |

VPID or TMRID |

|

|

|

|

|

|

|

|

|

|||

|

Social Security No. |

|

|

|

|

|

|

|

|

|

|||

|

Telephone No. ( ) |

|

|

|

|

|

|

|

|

||||

|

Fax No. ( ) |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

Check if new: Address |

|

Telephone |

|

Fax |

|

|||||||

Individual name and address |

VPID or TMRID |

|

|

|

|

|

|

|

|

|

|||

|

Social Security No. |

|

|

|

|

|

|

|

|

|

|||

|

Telephone No. ( ) |

|

|

|

|

|

|

|

|

||||

|

Fax No. ( ) |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

Check if new: Address |

|

Telephone |

|

Fax |

|

|||||||

Individual name and address |

VPID or TMRID |

|

|

|

|

|

|

|

|

|

|||

|

Social Security No. |

|

|

|

|

|

|

|

|

|

|||

|

Telephone No. ( ) |

|

|

|

|

|

|

|

|

||||

|

Fax No. ( ) |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

Check if new: Address |

|

Telephone |

|

Fax |

|

|||||||

to represent the taxpayer(s) before the Department of Taxation, State of Hawaii, for the following acts:

3Acts authorized (you are required to complete this line 3). (Stating “All Taxes” or “All Periods” on line 3 is NOT acceptable.) With the exception of the acts described in line 4b, I (we) authorize my (our) representative(s) to receive and inspect my (our) confidential tax information and to perform acts that I (we) can perform with respect to the tax matters described below. For example, my (our) representative(s) shall have the authority to sign any agreements, consents, tax clearance applications, or similar documents (but see instructions for authorizing a representative to sign a return). Please note that the tax year(s) or period(s) on line 3 can extend only 3 years after the current year. For example, if Form

Complete a separate line for each specific tax type. All three (3) columns of the line must be completed for the tax type.

Hawaii Tax I.D. Number

(e.g.,

Type of Tax

(Income, General Excise, etc.)

Year(s) or Period(s)

N848_I 2018A 01 VID01

ID NO 01

FORM

FORM |

|

(REV. 2018) |

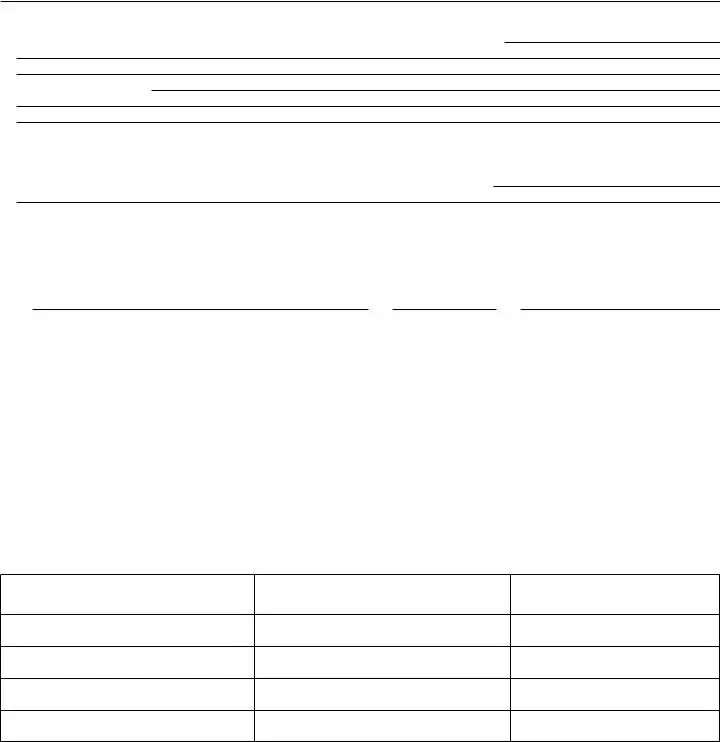

PAGE 2 |

4a Additional acts authorized. In addition to the acts listed on line 3 above, I (we) authorize my (our) representative(s) to perform the following acts (see instructions): Authorize disclosure to third parties; Substitute or add representatives; Sign a return;

Other acts authorized:

4b Specific acts not authorized. My (our) representative(s) is (are) not authorized to endorse or otherwise negotiate any check (including directing or accepting payment by any means, electronic or otherwise, into an account owned or controlled by the representative(s) or any firm or other entity with whom the representative(s) is (are) associated) issued by the government in respect of a Hawaii tax liability.

List any specific deletions to the acts otherwise authorized in this power of attorney (see instructions):

5Signature of Taxpayer(s). If a tax matter concerns a year in which a joint return was filed, both spouses must sign if joint representation is requested. If signed by a corporate officer, partner, guardian, tax matters partner/person, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

IF NOT SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED TO THE TAXPAYER.

|

|

|

|

Signature |

|

Date |

|

Title (if applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Name |

|

Print name of taxpayer from line 1 if other than individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature |

|

Date |

|

Title (if applicable) |

|

|

|

|

|||||||

|

|

|

|

Print Name |

|

|

|

|

|

|

PART II |

SIGNATURE OF REPRESENTATIVE(S) |

|

|

|

|

|

||

|

|

|

COMPLETED, SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED TO THE TAXPAYER. REPRESENTATIVES |

||||||

|

|

MUST SIGN IN THE ORDER LISTED IN PART I, LINE 2. |

|

|

|

|

|

||

Type or Print Name

Signature

Date

Filing the Power of Attorney

File the original, photocopy, or facsimile transmission (fax) with each letter, request, form, or other document for which the power of attorney is required. For example, if you wish to designate an individual to represent you in obtaining tax clearance certificates, a copy of Form

Hawaii Department of Taxation

P.O. Box 259

Honolulu, HI

or send it by FAX to (808)

QUESTIONS? Call

| Fact Name | Description |

|---|---|

| Purpose | The Tax Power of Attorney (POA) Form N848 is designed to authorize an individual to act on behalf of another person regarding tax matters. |

| Governing Law | This form is governed by the laws of the relevant state where the tax obligations are incurred, ensuring compliance with local regulations. |

| Who Can Be Authorized? | Individuals such as tax professionals, accountants, or trusted family members can be designated to represent the individual in tax-related matters. |

| Filing Process | To complete the process, the form must be filled out, signed, and submitted to the appropriate tax authority. |

| Duration of Authority | The authority granted through the N848 form remains in effect until revoked by the individual or until the tax matter in question is resolved. |

Filling out the Tax Power of Attorney (POA) Form N-848 is an important task that requires careful attention to detail. After you complete the form correctly, you will submit it to the relevant tax authority to authorize another individual to act on your behalf in tax matters. The following steps will guide you through the process of filling out the form accurately.

Once you have filled out the form, double-check to ensure all information is correct. Then, you can send it to the relevant tax office. Keep a copy of the completed form for your records, and consider following up with the agency to confirm receipt and processing of your Power of Attorney request.

What is the Tax POA Form N848?

The Tax POA Form N848 is a Power of Attorney form used by individuals to authorize someone else to handle their tax matters. This can include dealing with the IRS and state tax authorities on your behalf. This authorization allows another person, often a lawyer or accountant, to represent you in tax matters.

Who can be appointed as an agent using Form N848?

You can appoint anyone you trust as your agent using Form N848. This can be a family member, friend, or professional tax advisor. However, make sure the person is someone you trust to handle sensitive financial information.

What types of tax matters can an agent handle with Form N848?

An agent can represent you in a variety of tax matters. This includes filing your tax returns, responding to audits, negotiating payment plans, and communicating with tax authorities. An agent can also receive your tax documents and notices from the IRS.

Do I need to fill out any additional forms?

You may not need additional forms if your agent is only handling matters covered under the N848. However, if they will represent you before specific tax authorities or require more specific powers, other forms might be necessary. It is best to check the requirements for your particular situation.

How long is the Form N848 valid?

The Tax POA Form N848 does not have a specific expiration date. However, you may revoke it at any time if you decide that you no longer want your agent to have those powers. Inform both your agent and the tax authorities if you revoke the form.

Can I change my agent if I fill out Form N848?

Yes, you can change your agent. If you want to appoint a different person, you can fill out a new Form N848. Be sure to revoke the old form to avoid confusion and ensure that only your current agent has authority.

How do I submit the Tax POA Form N848?

You can submit the Tax POA Form N848 to the IRS or your state tax authority depending on whom you are authorizing to act on your behalf. Make sure to send it to the correct address. You might also want to keep a copy for your records.

Is there a fee to file Form N848?

No, there is typically no fee associated with filing Form N848. It's a straightforward form intended to give someone else the ability to represent you in tax matters without a charge directly tied to the form itself.

What should I do if my agent does not act in my best interest?

If you feel your agent is not acting in your best interest, you can revoke the authority granted by the N848. You should notify your agent and inform the tax authorities of your decision. This is important to protect your tax matters.

Not specifying the correct type of representation. It's important to indicate whether the authorized person is acting as an attorney-in-fact, CPA, or enrolled agent.

Forgetting to include the taxpayer’s Social Security Number (SSN) or Employer Identification Number (EIN). This information is crucial for the IRS to identify the taxpayer.

Neglecting to sign and date the form. An unsigned form may be deemed invalid, delaying the representation process.

Failing to clearly list the tax years or periods for which representation is granted. Without these details, the authority might not extend to all relevant issues.

Using outdated versions of the form. Always ensure you have the most current form by checking the IRS website.

Not providing adequate information about the authorized representative. The representative’s name, address, and phone number must be included.

Leaving any requested fields blank. All sections need to be completed, even if some do not seem applicable.

Confusing “taxpayer” with “representative.” Ensure that the information provided clearly distinguishes between the two parties.

Not notarizing the form when required. In some cases, notarization may be necessary to validate the document.

When dealing with tax matters, individuals often need to use various forms and documents in conjunction with the Tax Power of Attorney (POA) Form N-848. Each of these documents serves a specific purpose in representing the taxpayer's interests or facilitating communication with tax authorities. Below is a list of related forms and documents that might frequently accompany the N-848 form.

These forms and documents play crucial roles in ensuring compliance with tax regulations and facilitating communication with tax authorities. Having them at hand can streamline processes and potentially lead to more favorable outcomes in tax matters.

The IRS Form 2848 is known as the Power of Attorney and Declaration of Representative. Like the Tax POA form N848, this document allows taxpayers to authorize an individual to represent them before the IRS. It grants the designated representative the power to receive confidential tax information and provide assistance regarding tax matters. Both forms serve the same essential purpose, empowering an agent to act on behalf of the taxpayer in communications with tax authorities.

Form 8821, Tax Information Authorization, is another document that shares similarities with the Tax POA form N848. This form allows you to designate an individual to receive certain tax information from the IRS. While it does not grant representation rights like a POA, it enables the authorized individual to access the taxpayer's records. This provides insight into the taxpayer's affairs without full representation rights, thus serving a slightly different but related function.

The State Power of Attorney forms, which are often used in various states, are quite similar to the Tax POA form. These forms allow individuals to appoint someone to handle different matters, including tax issues, on their behalf at the state level. Each state may have specific requirements and variations, but the fundamental concept of granting authority remains consistent with the N848 form.

Financial Power of Attorney documents allow individuals to authorize a trusted person to manage their financial affairs. While these forms can encompass a wider range of financial matters, they can also address tax liabilities and filings. Similar to the Tax POA form N848, a Financial Power of Attorney ensures that someone can act in the taxpayer's best interest and handle their obligations efficiently.

Durable Power of Attorney forms are similar in that they allow an agent to act on behalf of the principal even if the principal becomes incapacitated. This arrangement can cover various aspects, including tax responsibilities. Thus, like the N848 form, these durable documents ensure that tax matters are addressed continuously, even in challenging times.

Health Care Power of Attorney documents, while primarily focused on medical decisions, can share procedural similarities with the Tax POA form N848. In both instances, individuals appoint someone to act on their behalf. Although the primary focus is different, both forms require explicit consent and can involve sensitive information, showcasing the necessity of trust in both situations.

Form 201, the Business Power of Attorney, serves as a means for business owners to appoint someone to handle business affairs, including tax matters. This form, like the Tax POA form N848, allows individuals to grant authority for someone to act in their name regarding business taxes. Understanding both forms helps clarify representation options whether for personal or business tax affairs.

Form 4506, Request for Copy of Tax Return, allows taxpayers to authorize someone else to obtain copies of their tax returns from the IRS. Though it's distinct from the Tax POA form N848, it also requires an individual to designate a representative. The two documents facilitate access to tax documents but differ in the scope of authority granted.

Form 8962, Premium Tax Credit, While primarily used to claim a tax credit related to health insurance premiums, it can require an authorization similar to that of the N848 form. Taxpayers may need to appoint individuals to assist with this process, thus showing how tax-related forms can intersect in support of a specific financial benefit.

Lastly, Form W-9, Request for Taxpayer Identification Number and Certification, allows individuals to authorize another party to access their tax identification information. Though focusing on information collection rather than representation, it shares the commonality of requiring explicit consent and trust in the appointed party, akin to the Tax POA form N848.

When filling out the Tax Power of Attorney (POA) Form N-848, adhering to best practices can facilitate a smoother process. Here are five important things to do and not do.

Misconception 1: The N-848 form can only be completed by tax professionals.

While tax professionals often assist clients, individuals can also fill out the form themselves if they meet the qualifications.

Misconception 2: The N-848 form is only used for federal tax matters.

This form is a Power of Attorney for tax purposes and can apply to various tax-related situations, including state taxes.

Misconception 3: Signing the N-848 form allows the agent to do anything with my taxes.

The form specifically limits the agent's authority to what is specified, such as receiving confidential information or representing the taxpayer before the IRS.

Misconception 4: The N-848 form is valid indefinitely.

The authority given by the form typically remains until it is revoked or the tax matter is resolved, making it crucial to monitor its status regularly.

Misconception 5: One form is enough for multiple tax issues.

In some cases, separate forms may be required for different tax matters or years, depending on the complexity of each situation.

Misconception 6: I cannot change my agent after submitting the N-848 form.

Taxpayers have the right to revoke the power of attorney and appoint a new agent at any time, as long as the appropriate steps are followed.

Misconception 7: Only one agent can be named on the N-848 form.

The form allows for the designation of multiple agents, enabling taxpayers to appoint more than one person to handle their tax issues.

Misconception 8: Filing the N-848 form is a complicated process.

Filling out the form is straightforward and can be done with clear instructions, aiding taxpayers in their representation needs.

Misconception 9: The N-848 form is only relevant during tax season.

This form can be utilized throughout the year for various tax-related situations, illustrating its ongoing relevance.