When navigating the complexities of tax matters, the importance of proper representation cannot be overstated. The Tax Power of Attorney (POA) form, known as the DP-2848, serves as a crucial tool that empowers individuals to appoint an authorized representative to act on their behalf with the Internal Revenue Service (IRS). This form not only grants the designated individual the authority to resolve tax-related issues, but it also delineates the specific permissions granted which can range from accessing tax information to making decisions regarding returns and payments. Completing the DP-2848 can ensure that taxpayers do not have to face the IRS alone, allowing them to delegate responsibilities to those who possess the necessary expertise. Additionally, the form sets clear boundaries around the scope of authority, thereby enhancing the protection of personal and financial information. For both individuals and businesses, understanding how to effectively utilize the DP-2848 can streamline communication with the IRS and alleviate the stress of tax proceedings. Recognizing the nuances of this form can ultimately empower taxpayers to pursue resolutions to tax issues with greater confidence.

DO NOT STAPLE

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

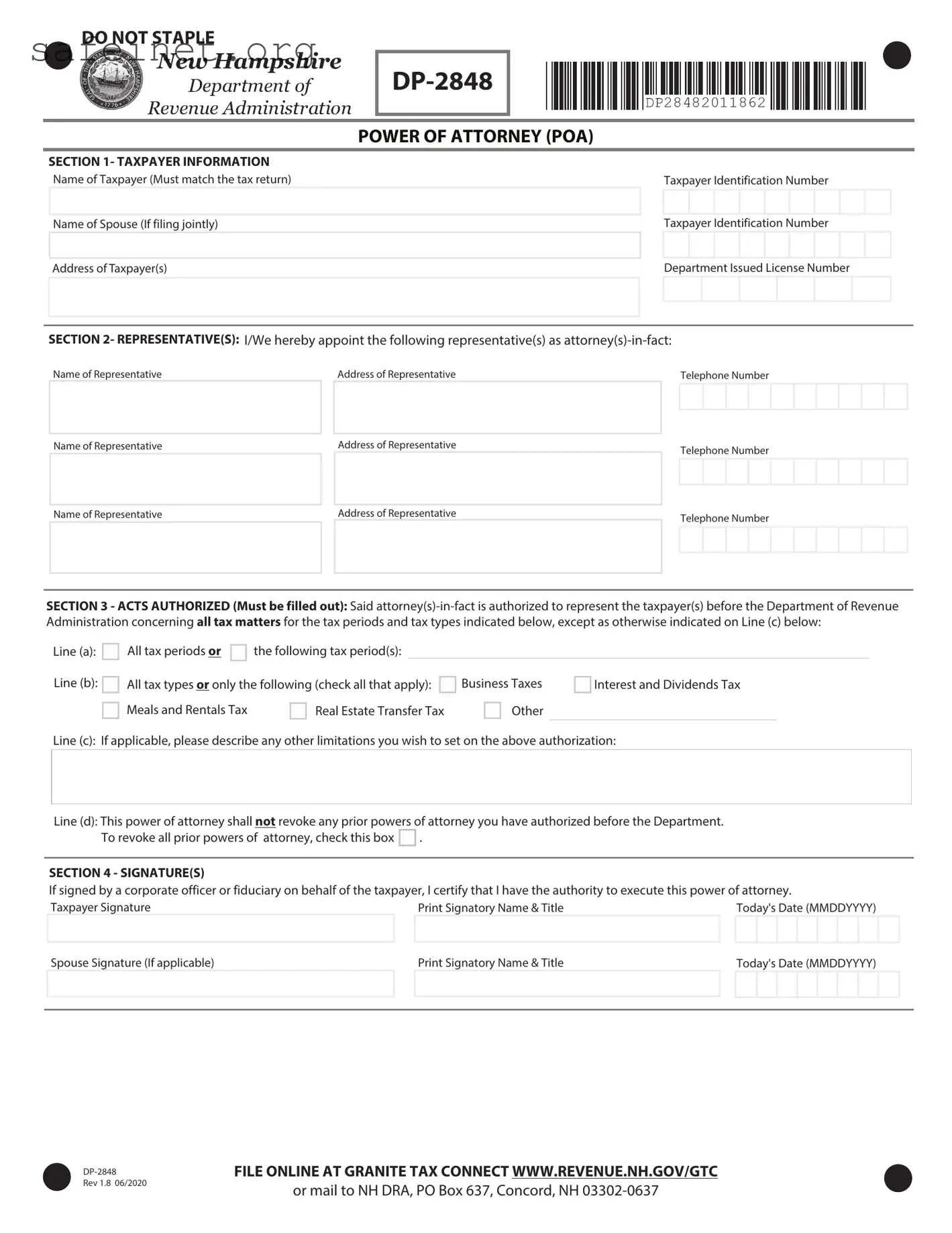

POWER OF ATTORNEY (POA) |

|

|

|

||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

SECTION 1- TAXPAYER INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Name of Taxpayer (Mustmatchthe |

tax |

return) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer Identification Number |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Name of Spouse (If filing jointly) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer Identification Number |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Taxpayer(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Department Issued License Number |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECTION 2- REPRESENTATIVE(S): I/We hereby appoint the following representative(s) as

|

Name of Representative |

|

Address of Representative |

Telephone Number |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Representative |

|

Address of Representative |

Telephone Number |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Representative |

|

Address of Representative |

Telephone Number |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECTION 3 - ACTS AUTHORIZED (Must be filled out): Said

Line (a):

Line (b):

All tax periods or |

|

the following tax period(s): |

All tax types or only the following (check all that apply):

Meals and Rentals Tax |

|

Real Estate Transfer Tax |

Business Taxes

Other

Interest and Dividends Tax

Line (c): If applicable, please describe any other limitations you wish to set on the above authorization:

Line (d): This power of attorney shall not revoke any prior powers of attorney you have authorized before the Department.

To revoke all prior powers of attorney, check this box |

. |

SECTION 4 - SIGNATURE(S)

If signed by a corporate officer or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney.

Taxpayer Signature |

Print Signatory Name & Title |

Today's Date (MMDDYYYY) |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse Signature (If applicable) |

Print Signatory Name & Title |

Today's Date (MMDDYYYY) |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rev 1.8 06/2020

FILE ONLINE AT GRANITE TAX CONNECT WWW.REVENUE.NH.GOV/GTC

or mail to NH DRA, PO Box 637, Concord, NH

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

POWER OF ATTORNEY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

INSTRUCTIONS |

(POA) |

||||||||||||||

|

|

|

|

|

|

|||||||||||

WHEN TO FILE

A Power Of Attorney (POA) is required prior to the Department of Revenue Administration communicating with anyone other than the taxpayer regarding any issue relating to the taxpayer.

WHERE TO FILE

File online at Granite Tax Connect www.revenue.nh.gov/gtc or mail to NH DRA, Taxpayer Services Division, PO Box 637, Concord NH

PLEASE NOTE

All applicable items must be filled in to properly complete Form

SECTION 1 - TAXPAYER INFORMATION

Enter the taxpayer's name (must match the tax return), current mailing address including zip code, and taxpayer identification number (and Department issued license number if applicable). If joint returns are involved and you and your spouse are designating the same representative(s), also enter your spouse's name and taxpayer identification number (and Department issued license number if applicable). If you need to list additional taxpayers, an additional page may be attached with each taxpayer's name and taxpayer identification number.

SECTION 2 - REPRESENTATIVE(S)

Enter the name of the representative(s). This can be an individual(s) or the name of a firm. What you enter in the Name of Representative box determines who the Department will have authority to correspond with as your authorized representative. If you list only an individual(s) name from a firm, then only the individual(s) will have authority to represent you. If you put the firm name in the Name of Representative box then ANYONE with the firm will have the authority to represent you.

Enter the current mailing address including zip code of the representative in the Address of Representative box beside the Name of Representative box. Only the person(s) or firm named in the Name of Representative box has authorization to represent you with the Department. A firm name that is part of an individual's address does not mean that the employees of the firm can represent the taxpayer.

Provide the representative's phone number in the space provided. If more than one name is listed, provide the phone number of the first person listed.

This section allows for three representatives. If you have more than three, please attach an additional sheet and note "see attached" in one of the Name of Representative boxes.

SECTION 3 - ACTS AUTHORIZED (MUST BE FILLED OUT)

On Line (a), either check the "all" box to indicate that the representative applies to all tax periods, or limit the representation to a particular tax period(s) and provide the date range or period(s). If you enter only a year(s) (e.g. 2018) the representation will include any period (including any Meals and Rooms or Tobacco Tax periods, if authorized on Line (b)) that fall within that year. If you limit the representation to a date range, please be aware that your representative will not be permitted to discuss any other date range with the Department. Note: If you check both the "all" box and provide a date range, the representation will not be limited to the date range, but will apply to all dates and tax periods.

On Line (b), check the boxes for the tax types that apply to your representation. If the representation applies to all taxes, check the "all" box. To limit the representation to one or more taxes, check all the appropriate boxes and for any taxes not shown, check the "other" box and identify the taxes on the line (for example MET or UPT). Note: If you check both the "all" box and the boxes for specific taxes, the representation will not be limited to a specific tax, but will apply to all tax types.

On Line (c), describe any other limitations you wish to place on your representation. For example, if you wish to only authorize your representative to receive information, note this limitation on Line (c). Otherwise, your representative will not only be authorized to receive your confidential information but also full power to perform all acts necessary related to the subject matter of the indicated tax types and periods.

If the box on Line (d) is not checked, the filing of this form will not revoke or otherwise invalidate any prior powers on file with the Department. If you check the box provided on Line (d), you will revoke all prior powers of attorney, unless the representatives are identified again in Section 2 of this form.

If you are a representative that wishes to withdraw representation of a taxpayer, please forward a signed and dated letter with a copy of the POA you are withdrawing to the Department.

Rev 1.8 06/2020

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

POWER OF ATTORNEY

(POA)

INSTRUCTIONS Continued

SECTION 4 - SIGNATURE(S)

The taxpayer is required to sign and date the POA. The completed and signed form

NEED HELP?

Questions not covered here may be answered in our "Frequently Asked Questions" available on our website at www.revenue.nh.gov or by calling Taxpayer Services at (603)

Rev 1.8 06/2020

| Fact Name | Details |

|---|---|

| Purpose of Form | The IRS Form 2848, also known as Power of Attorney and Declaration of Representative, allows individuals to authorize someone to represent them before the IRS. |

| Types of Representation | The form can be used for various tax matters, including income tax, estate tax, and employment tax issues. |

| Signature Requirement | Both the taxpayer and the representative must sign the form for it to be valid. |

| Expiration of Authority | The power of attorney remains in effect until the taxpayer revokes it or the IRS receives a written notice of revocation. |

| Governing Law | Form 2848 operates under the authority of the Internal Revenue Code (26 U.S.C.) and IRS regulations. |

Completing the Tax POA Form DP-2848 requires careful attention to personal information and the specific details of the authority being granted. After filling out the form, you will submit it to the appropriate tax authority to designate someone to represent you regarding your tax matters.

What is the Tax POA form DP-2848?

The Tax POA form DP-2848, also known as Power of Attorney for Tax Matters, allows an individual to authorize another person to represent them before the tax authorities. This can be particularly useful for handling tax-related issues, filing returns, or engaging in discussions about tax matters on behalf of the individual.

Who can I appoint as my representative on the DP-2848 form?

You can appoint almost anyone as your representative for tax matters, including accountants, attorneys, or other trusted individuals. The person you choose must be willing and able to act on your behalf, and they should fully understand the responsibilities involved in representing you before tax authorities.

What are the key steps to fill out the DP-2848 form?

Filling out the DP-2848 form generally requires you to provide your personal information, including your name, address, and Social Security number or taxpayer identification number. Next, you will need to provide details about your appointed representative, such as their name and contact information. Finally, you must sign and date the form to validate it. Ensure that all information is accurate to avoid processing delays.

How long is the DP-2848 form valid for?

The validity of the DP-2848 form typically lasts until you revoke it or the authority of the representative is terminated. It is advisable to keep track of any changes in your situation that may require updates to the form or the appointment of a new representative.

Do I need to submit the DP-2848 form to the tax authorities directly?

Can I revoke my Power of Attorney once it is in effect?

Yes, you have the right to revoke your Power of Attorney at any time. To do so, you typically need to create a written statement indicating your intent to revoke, and you may also need to notify the person you appointed and the relevant tax authority. It is important to follow proper procedures to ensure that the revocation is recognized.

Where can I obtain a DP-2848 form?

The DP-2848 form can usually be accessed on the official website of the tax authority, such as the IRS or your state's department of revenue. You may also find print copies at local tax offices or request one through official channels if necessary.

Incomplete Information: Many individuals fail to provide all necessary details. This may include missing names, addresses, or identification numbers. Incomplete submissions can delay processing or lead to rejection.

Incorrect Signatures: Some people neglect to sign the form or sign it in the wrong place. The IRS requires appropriate signatures from both the taxpayer and the representative. Without valid signatures, the form cannot be accepted.

Wrong Representative Information: It is common for taxpayers to incorrectly list their representative's details. Providing an outdated or incorrect address or identification number can cause communication issues and hinder the representation process.

Failure to Specify Options: The form allows for specific options regarding the scope of representation. Some taxpayers do not specify these options clearly. This can lead to misunderstandings about what the representative is authorized to do.

When individuals need to appoint someone to represent them in tax matters, the Tax Power of Attorney (POA) Form, often referred to as Form DP-2848, is a crucial document. However, this form is often accompanied by several other important documents that facilitate various aspects of tax representation and compliance. Below is a detailed list of related forms and documents that may be necessary.

Understanding these related forms can greatly enhance the efficiency of tax representation. Each document plays a specific role in ensuring compliance and smooth communication with tax authorities. Equipped with this knowledge, taxpayers and their representatives can navigate the complexities of tax law more effectively.

The IRS Form 2848, known as the Power of Attorney and Declaration of Representative, is a document that gives someone the authority to represent a taxpayer before the IRS. It shares similarities with several other legal documents that grant powers to individuals or entities to act on behalf of others in various contexts. Understanding these documents can help clarify their function and scope in legal and financial matters.

One comparable document is the Durable Power of Attorney. This document allows an individual to designate another person to manage their financial and legal affairs, even if the individual becomes incapacitated. Like the 2848, the Durable Power of Attorney must be signed and typically requires a notary. However, it covers a broader range of issues beyond tax matters, making it more versatile for financial decision-making.

The Medical Power of Attorney is another similar document. This form designates someone to make healthcare decisions on behalf of another individual, should they become unable to communicate their wishes. Both forms require clear identification of the granting individual and the representative. While the 2848 is specific to tax issues, the Medical Power of Attorney deals solely with health-related decisions, showcasing the varied applications of appointed authority.

A Limited Power of Attorney restricts the powers granted to a representative, often specifying that they can only act in certain situations or for a set period. This is similar to the IRS Form 2848, which can limit the scope of the tax representative's authority by designating specific tax matters. However, the Limited Power of Attorney can apply to various aspects of life, not just tax situations, showcasing both its flexibility and specificity.

The General Power of Attorney is broader in scope than the Durable Power of Attorney. It allows the agent to act on behalf of the principal in a wide array of matters, including financial, legal, and personal affairs. Like the 2848, it requires proper execution and often notarization. However, the General Power of Attorney may be used for non-tax-related issues, drawing a distinction in their respective applications.

A Representation Agreement is another document that shares similarities with the IRS Form 2848. This agreement is often used in legal contexts, particularly allowing a lawyer or other representative to act on behalf of the client. It specifies the powers granted and can have limitations based on the nature of the legal issue, similar to how the 2848 delineates tax-related representation.

The Healthcare Proxy serves as a counterpart to the Medical Power of Attorney. This document allows individuals to appoint someone to make medical decisions on their behalf, paralleling how a tax representative is authorized to act before the IRS. Both forms ensure that individuals can have their preferences respected, either in healthcare or tax matters, and require consent from the party granting the authority.

A Trust Agreement is another legal document that often emerges in estate planning discussions. It allows a trustee to manage assets for the benefit of beneficiaries. Similar to the 2848, it requires formal creation and outlines specific powers granted to the trustee. However, its main focus is on financial management and property distribution rather than representation in legal matters exclusively.

The Advance Directive is a document that combines aspects of the Medical Power of Attorney and a Living Will. An Advance Directive allows a person to specify their healthcare preferences and designate an individual to make decisions on their behalf. Although primarily focused on health care, its structure bears resemblance to the 2848, as both require clear authority and a designated representative.

Lastly, the Employment Authorization Document (EAD) provides the holder permission to work in the United States. While the purpose differs from the IRS Form 2848, both documents involve granting specific rights to act—one for tax representation and the other for employment matters. Both require the appropriate identification of the individual granting the rights and can impose limitations based on specified criteria.

When completing the Tax Power of Attorney (POA) Form DP-2848, attention to detail is crucial. To ensure that the form is filled out correctly and efficiently, here are six recommendations, categorized into what you should and shouldn't do.

By adhering to these guidelines, you can navigate the process of filling out the Tax POA form effectively and minimize potential issues.

There are several misconceptions about the Tax Power of Attorney (POA) form, specifically the form DP-2848. These misunderstandings can lead to confusion for individuals seeking assistance with their taxes. Here are some common myths:

Understanding these points can help individuals make informed decisions about using the Tax POA form DP-2848.

When filling out and using the Tax POA (Power of Attorney) form, known as Form DP-2848, there are several important considerations to keep in mind. Proper understanding can help streamline the process and ensure your tax matters are handled effectively.

Understanding these key aspects of the Tax POA form DP-2848 will empower you to manage your tax dealings confidently. A well-handled POA can allow for smoother communication with tax authorities and alleviate stress during the tax process.