The Tax Power of Attorney (POA) form ACd-31102 serves as an important tool for individuals or businesses seeking to grant authorized representatives the ability to act on their behalf in tax-related matters. This form facilitates communication between taxpayers and tax authorities, allowing designated agents to receive confidential information, represent taxpayers during audits, and resolve tax disputes. By completing and submitting the ACd-31102, taxpayers confirm their intention to delegate specific powers to an agent, thus permitting that agent to make decisions or perform actions related to the taxpayer's tax obligations. The form requires essential identifying information for both the taxpayer and the representative, ensuring clear identification throughout the tax process. Furthermore, it provides a mechanism for the revocation of previous powers of attorney by outlining how to officially terminate an existing authorization. Understanding the nuances of this form is crucial for effective tax management and compliance.

ACD - 31102 |

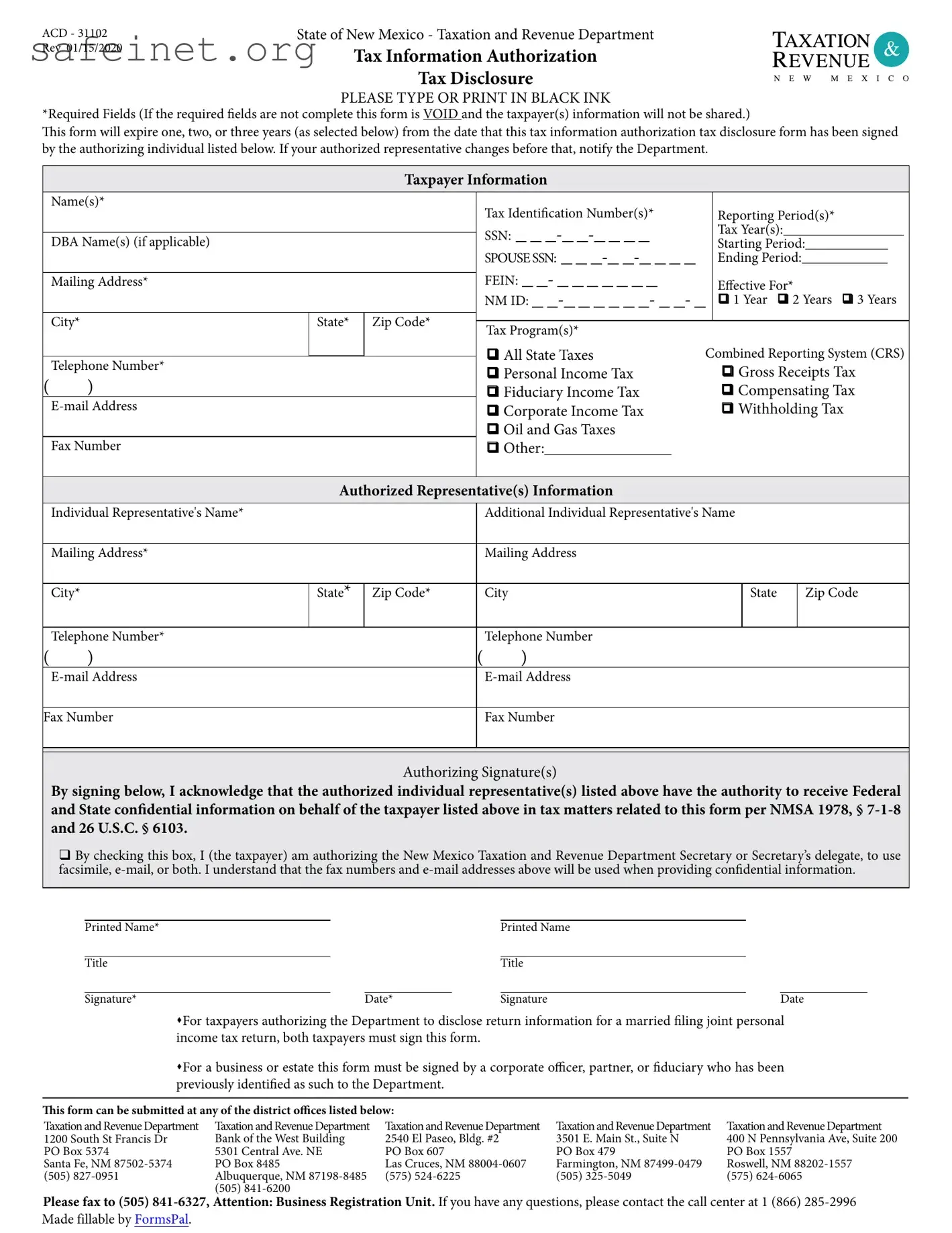

State of New Mexico - Taxation and Revenue Department |

TAXATION . |

Rev 01/15/2020 |

Tax Information Authorization |

|

|

REVENUE ~ |

|

|

Tax Disclosure |

NE W MEXICO |

PLEASE TYPE OR PRINT IN BLACK INK

*Required Fields (If the required felds are not complete this form is VOID and the taxpayer(s) information will not be shared.)

Tis form will expire one, two, or three years (as selected below) from the date that this tax information authorization tax disclosure form has been signed by the authorizing individual listed below. If your authorized representative changes before that, notify the Department.

Taxpayer Information

|

|

Name(s)* |

|

|

|

Tax Identifcation Number(s)* |

|

Reporting Period(s)* |

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

SSN: - - |

|

Tax Year(s): |

||||||||

|

|

DBA Name(s) (if applicable) |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

Starting Period: |

|||||||||||

|

|

|

|

|

|

|

SPOUSE SSN: - - |

|

Ending Period: |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

FEIN: - |

|

|

|

|

|

|

|

|||

|

|

Mailing Address* |

|

|

|

|

Efective For* |

||||||||||

|

|

|

|

|

|

|

NM ID: - |

|

q 1 Year |

q 2 Years q 3 Years |

|||||||

|

|

City* |

|

State* |

Zip Code* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax Program(s)* |

|

|

|

|

|

|

|

|

|||||

|

|

|

I |

|

I |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

q All State Taxes |

Combined Reporting System (CRS) |

|||||||||||

|

|

Telephone Number* |

|

|

|

||||||||||||

|

|

|

|

|

q Personal Income Tax |

|

q Gross Receipts Tax |

||||||||||

( |

) |

|

|

|

|

|

|||||||||||

|

|

|

|

q Fiduciary Income Tax |

|

q Compensating Tax |

|||||||||||

|

|

|

|

|

q Corporate Income Tax |

|

q Withholding Tax |

||||||||||

|

|

|

|

|

|

|

q Oil and Gas Taxes |

|

|

|

|

|

|

|

|

||

|

|

Fax Number |

|

|

|

q Other: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

Authorized Representative(s) Information |

|

|

|

|

|

|

|

|

|||||

|

|

Individual Representative's Name* |

|

|

|

Additional Individual Representative's Name |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

Mailing Address* |

|

|

|

Mailing Address |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

City* |

|

State* |

Zip Code* |

|

City |

|

State |

|

|

|

Zip Code |

||||

|

|

|

I |

|

I |

|

|

|

|

|

I |

|

I |

||||

|

|

Telephone Number* |

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|||

( |

) |

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Fax Number |

|

|

|

Fax Number |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Authorizing Signature(s)

By signing below, I acknowledge that the authorized individual representative(s) listed above have the authority to receive Federal and State confdential information on behalf of the taxpayer listed above in tax matters related to this form per NMSA 1978, §

qBy checking this box, I (the taxpayer) am authorizing the New Mexico Taxation and Revenue Department Secretary or Secretary’s delegate, to use facsimile,

Printed Name* |

|

Printed Name |

|

Title |

|

Title |

|

Signature* |

Date* |

Signature |

Date |

sFor taxpayers authorizing the Department to disclose return information for a married fling joint personal income tax return, both taxpayers must sign this form.

sFor a business or estate this form must be signed by a corporate ofcer, partner, or fduciary who has been previously identifed as such to the Department.

Tis form can be submitted at any of the district ofces listed below:

Taxation and Revenue Department |

Taxation and Revenue Department |

Taxation and Revenue Department |

Taxation and Revenue Department |

Taxation and Revenue Department |

1200 South St Francis Dr |

Bank of the West Building |

2540 El Paseo, Bldg. #2 |

3501 E. Main St., Suite N |

400 N Pennsylvania Ave, Suite 200 |

PO Box 5374 |

5301 Central Ave. NE |

PO Box 607 |

PO Box 479 |

PO Box 1557 |

Santa Fe, NM |

PO Box 8485 |

Las Cruces, NM |

Farmington, NM |

Roswell, NM |

(505) |

Albuquerque, NM |

(575) |

(505) |

(575) |

|

(505) |

|

|

|

Please fax to (505)

Made fillable by FormsPal.

| Fact Name | Details |

|---|---|

| Purpose | The Tax POA Form ACD-31102 is used to authorize an individual or entity to represent a taxpayer in dealings with the state tax authority. |

| Governing Law | This form complies with state tax regulations as outlined in [relevant state tax code or statute]. |

| Eligibility | Any individual or business entity with tax obligations can utilize this form to designate a representative. |

| Submission Process | Complete the form and submit it to the appropriate state tax authority, following any specific instructions provided for submission. |

When preparing to fill out the Tax POA form ACD-31102, it's important to ensure that all necessary information is accurately provided. This form enables someone to represent you in matters related to your taxes. Take your time to review each section carefully to prevent any mistakes.

After completing the form, ensure that it is sent to the relevant tax authority. It is advisable to check their specific submission guidelines, as methods may vary, including mail or electronic submission options.

What is the Tax POA Form ACD-31102?

The Tax POA Form ACD-31102 is a Power of Attorney form specifically designed for tax purposes. This form allows you to appoint an individual or professional entity to represent you before the IRS or state tax authorities. By completing this form, you grant your representative the authority to handle your tax matters, such as discussing issues with the tax agency, accessing your tax records, and making decisions on your behalf.

Who should use the Tax POA Form ACD-31102?

The form is beneficial for anyone who needs assistance in managing their tax-related issues. This includes individuals who may not have the time or expertise to navigate complex tax matters. Additionally, business owners may find it helpful to appoint a tax professional to manage their corporate tax filings and obligations.

How do I fill out the Tax POA Form ACD-31102?

Filling out the form requires careful attention. First, you will need to provide your personal information, including your name, address, and taxpayer identification number. Next, you will enter the details of your appointed representative, including their name and contact information. Finally, you will sign and date the form to validate your authorization. Make sure all information is accurate to avoid delays in processing.

When should I submit the Tax POA Form ACD-31102?

You should submit the form whenever you require someone to represent you on tax matters. It is advisable to complete the form before any upcoming discussions or audits with the IRS or state tax agency. If there are changes in representation, you must submit a new form to update the information.

What happens after I submit the Tax POA Form ACD-31102?

Once submitted, the tax authorities will review your form. Upon approval, your appointed representative will receive the authority to act on your behalf in the specified tax matters. You will also receive confirmation from the tax agency, ensuring that your representative can communicate about your account. Follow up if you have not received acknowledgment within a reasonable timeframe.

Can I revoke the Power of Attorney granted through the Tax POA Form ACD-31102?

Yes, you can revoke the Power of Attorney at any time if you decide to change your representative or manage your tax affairs independently. To do so, you will need to submit a written statement to the tax agency indicating the revocation of authority granted by the ACD-31102 form. It's essential to keep a record of this communication for your records.

Is there a fee associated with submitting the Tax POA Form ACD-31102?

Generally, there is no fee for submitting the Tax POA Form ACD-31102 itself. However, if you are hiring a tax professional or attorney to assist you, they may charge fees for their services. Be sure to discuss any costs associated with your representative prior to engaging their help.

Missing Signatures: Many individuals forget to sign the Tax POA form acd-31102, which renders it invalid. Ensure all required parties sign the form before submission.

Incorrect Tax Identification Number: Entering an incorrect social security number or employer identification number can cause delays. Double-check the accuracy of this information.

Overlooking Expiration Dates: The Power of Attorney does not last indefinitely. Failing to specify an expiration date may lead to confusion if the form is intended for a limited time.

Not Specifying the Scope of Authority: A common mistake is not clearly stating what powers are granted to the representative. Be explicit about the kinds of decisions and actions allowed.

Insufficient Identification of the Representative: Providing incomplete or unclear information about the representative, such as their address or organization name, can lead to processing issues.

Failing to Review the Form: Some people rush through completing the form without reviewing it for errors or omissions. A careful check can prevent mistakes that delay processing.

Ignoring State-Specific Requirements: Laws vary by state, and some may have additional requirements. Be aware of any state-specific rules that might apply to the Tax POA form.

When completing the Tax POA form ACD-31102, there are several other forms and documents that may be needed to support your tax-related matters. Below is a list of these documents along with a brief description of each.

Having these documents handy can streamline your tax processes and ensure that your tax representation is effective and comprehensive. Make sure to review each form to understand its specific purpose and how it interacts with your Tax POA form ACD-31102.

The Tax POA (Power of Attorney) form ACD-31102 allows individuals to grant authority to another person to act on their behalf regarding tax matters. One document that is similar in function is the General Power of Attorney. This document permits an individual, referred to as the principal, to appoint someone else, the agent, to manage a range of affairs, including financial matters. Both documents involve the transfer of decision-making authority, but the General Power of Attorney tends to cover a broader scope beyond tax issues.

Another important document is the Limited Power of Attorney. This form restricts the authority granted to the agent to specific tasks or situations. For example, a taxpayer might use a Limited Power of Attorney for a particular transaction or a defined period. Like the Tax POA, it grants authority, but it is tailored to address only certain activities rather than an all-encompassing power.

A Medical Power of Attorney serves a similar purpose in that it allows someone to make healthcare decisions on behalf of another. While the Tax POA deals specifically with tax-related issues, the Medical Power of Attorney centers on personal health decisions. Both documents highlight the importance of entrusting someone with significant responsibility to act in the best interests of another individual.

The Durable Power of Attorney is also comparable to the Tax POA. It maintains its effectiveness even if the principal becomes incapacitated. This ensures ongoing representation in financial matters, underlying a commitment to maintaining support during difficult times. In this way, both documents aim to ensure that decisions continue to be made by a trusted individual.

A Special Power of Attorney is another relevant document, as it can be customized for a specific purpose, similar to the Limited Power of Attorney. Individuals may select this option when they wish to grant authority for a narrow range of tasks while retaining control over other aspects of their lives. Both types emphasize the importance of clear boundaries in granting authority.

The Authorization to Release Information form is noteworthy since it enables one individual to authorize another to obtain private information, often from the government or financial institutions. While this document does not grant decision-making authority, it serves to facilitate communication and access to vital information, akin to the directive nature of the Tax POA.

Lastly, the Consent to Disclose Information form aligns with the Tax POA in that it allows individuals to provide consent for specific records or personal details to be shared with designated people or entities. Here, the emphasis is on the transfer of information rather than the authority to act, but both highlight the importance of consent in managing personal affairs.

When filling out the Tax POA form ACD-31102, there are several important guidelines to keep in mind. Following these tips can help ensure that the process goes smoothly and that your form is accepted without delay. Here’s what you should and shouldn’t do:

Misconceptions about tax forms can lead to confusion and misinterpretation of tax obligations. The Tax Power of Attorney (POA) form ACD-31102 is no exception. Below are six common misconceptions regarding this form, accompanied by explanations.

This form is not limited to individuals. It can also be utilized by businesses or organizations that need to designate a representative to act on their behalf in tax matters.

The authority provided via the Tax POA is specific and can be limited to certain tax matters or periods. The principal can define the extent of the powers granted.

Individuals can revoke the Tax POA at any time by submitting a revocation notice. It is essential to formally communicate this revocation to the designated representative and the tax authority.

While signing is an essential step, the representative must receive approval from the relevant taxing authority before they can actually perform any actions on behalf of the taxpayer.

In most cases, notarization is not necessary for the Tax POA form. A simple signature is typically sufficient, though it's advisable to check specific state requirements.

This form must be filed with the tax authority to designate a representative effectively. Without this filing, the representative may not have the authority to act on behalf of the taxpayer.

When dealing with taxes, having the right authorization can make a significant difference. Here are some important points to remember when filling out and using the Tax Power of Attorney (POA) form ACD-31102:

Using the Tax POA form ACD-31102 can streamline your tax processes and give peace of mind. With the right information and thoughtful choices, you can effectively manage your tax responsibilities through your chosen representative.