The IRS Form 548, often referred to as the Tax Power of Attorney (POA) form, plays a crucial role in the relationship between taxpayers and the tax authorities. This form enables individuals or entities to designate another individual as their representative in dealings with the Internal Revenue Service. By completing this form, taxpayers grant their representatives the authority to act on their behalf concerning tax matters, which may include the ability to receive confidential information and make legal decisions related to a tax situation. It is important to note that the appointed representative does not need to be a tax professional; family members or friends can also be designated. When completing the Form 548, taxpayers must provide important information, including the representative’s name, address, and the specific powers being granted. Additionally, this form must be signed by the taxpayer, conducting an authorization that holds legal weight. Understanding the nuances of the Tax POA Form 548 can aid taxpayers in navigating their obligations and rights under tax law, ensuring that competent representation is available when needed. Properly executed, this form can simplify the often daunting communication with the IRS, ultimately facilitating a more efficient resolution of tax matters.

■ |

|

MARYLAND |

POWER OF ATTORNEY |

|

|

|

|

|

|

|||||

|

FORM |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

548 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

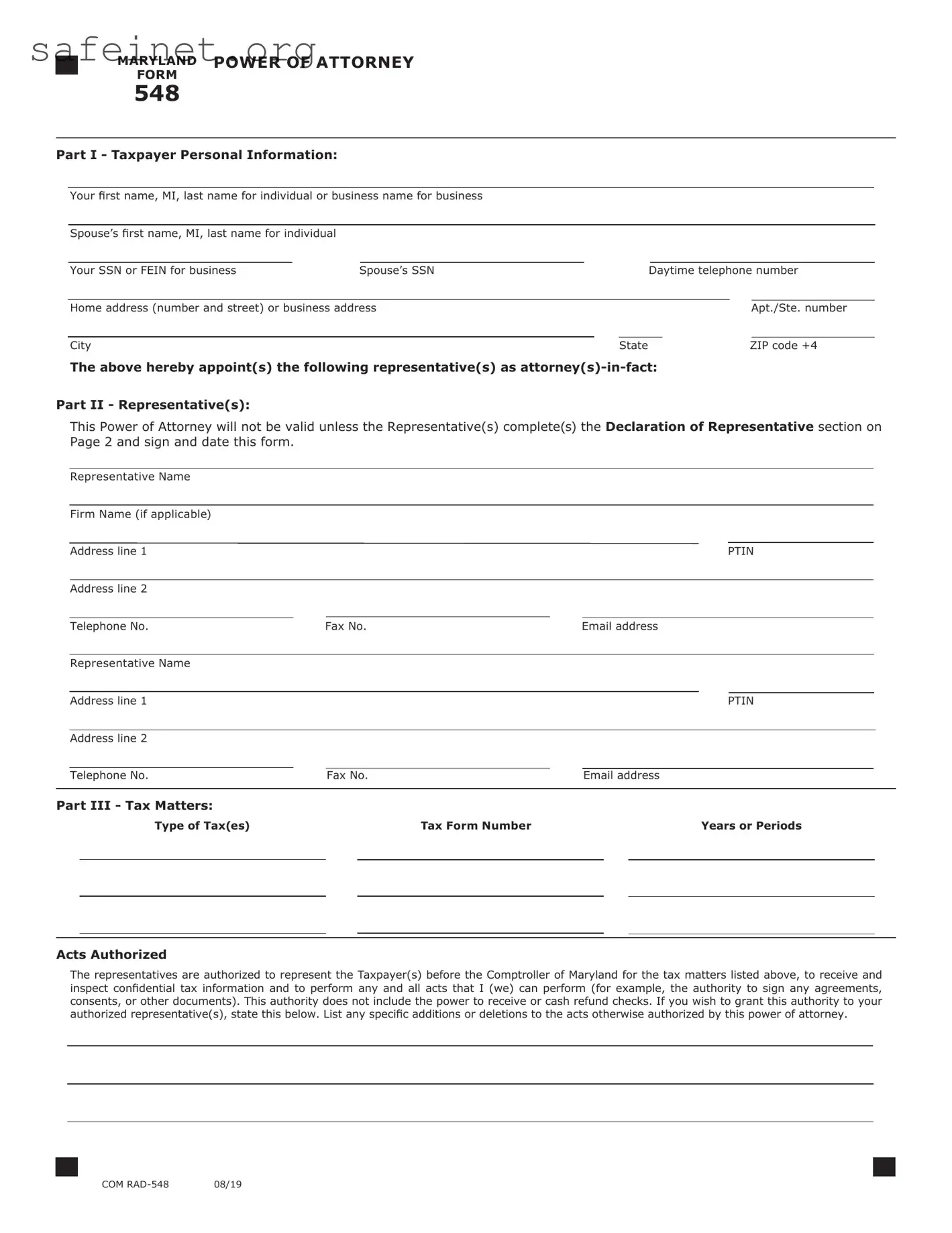

Part I - Taxpayer Personal Information: |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|||||||

|

Your first name, MI, last name for individual or business name for business |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Spouse’s first name, MI, last name for individual |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|||||||

|

Your SSN or FEIN for business |

Spouse’s SSN |

|

Daytime telephone number |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Home address (number and street) or business address |

|

|

|

|

Apt./Ste. number |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

State |

|

|

ZIP code +4 |

|

||

The above hereby appoint(s) the following representative(s) as

Part II - Representative(s):

This Power of Attorney will not be valid unless the Representative(s) complete(s) the Declaration of Representative section on Page 2 and sign and date this form.

Representative Name

|

Firm Name (if applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address line 1 |

|

|

|

|

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address line 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Telephone No. |

Fax No. |

Email address |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Representative Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address line 1 |

|

|

|

|

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address line 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Telephone No. |

|

Fax No. |

|

Email address |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

Part III - Tax Matters: |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Type of Tax(es) |

|

|

Tax Form Number |

|

|

|

|

Years or Periods |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Acts Authorized

The representatives are authorized to represent the Taxpayer(s) before the Comptroller of Maryland for the tax matters listed above, to receive and inspect confidential tax information and to perform any and all acts that I (we) can perform (for example, the authority to sign any agreements, consents, or other documents). This authority does not include the power to receive or cash refund checks. If you wish to grant this authority to your authorized representative(s), state this below. List any specific additions or deletions to the acts otherwise authorized by this power of attorney.

■ |

COM |

■ |

■ |

MARYLAND |

POWER OF ATTORNEY |

Page 2 |

FORM |

|

|

|

|

548 |

|

|

Taxpayer’s SSN or FEIN |

|

Taxpayer’s Name |

Retention/Revocation of Prior Power(s) of Attorney

By filing this power of attorney form, you automatically revoke all earlier power(s) of attorney on file with the Comptroller of Maryland for the same tax matters and years or periods covered by this document.

If you do not want to revoke a prior power of attorney, check here □

You must attach a copy of any Power of Attorney you want to remain in effect.

Signature of Taxpayer(s)

If a tax matter concerns a joint return, both spouses must sign if joint representation is requested. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the Taxpayer, I certify that I have the authority to execute this form on behalf of the Taxpayer. If other than the Taxpayer, print the name here and sign below.

Your signature |

Date |

|

|

Spouse’s signature if filing jointly |

Date |

Title, if business taxpayer or if other than individual taxpayer

Telephone number if other than the Taxpayer

If not signed and dated, this power of attorney will not be processed.

Declaration of Representative Representative(s) must complete this section and sign below.

Under penalties of perjury, I declare that

•I am not currently under suspension or disbarment from practice within the State of Maryland or in any jurisdiction;

•I have verified the identity of the taxpayer described under Taxpayer Personal Information and that the person signing as the authorized taxpayer is the same person described under Taxpayer Personal Information;

•I am aware of regulations governing the practice of attorneys, certified public accountants, public accountants, enrolled agents and others; and the penalties for false or fraudulent statements provided;

•I am authorized to represent in Maryland, the Taxpayer(s) identified for the tax matter(s) specified herein; and I am one of the following:

1.A member in good standing of the bar of the highest court of the jurisdiction shown below.

2.A Certified Public Accountant duly qualified to practice in the jurisdiction shown below.

3.An Enrolled Agent.

Attach

4.A Maryland Registered Individual Tax Preparer.

5.A bona fide officer of the Taxpayer.

6.A

7.A member of the Taxpayer’s immediate family (spouse, parent, child, grandparent, grandchild,

8.A general partner of the Taxpayer (partnership).

9.A fiduciary for the Taxpayer (Estate or trust).

10.Other (attach statement).

Jurisdiction (state)

Signature

Identification Number

(Bar, CPA, EA, Certification or Federal Employer Identification Number)

Date

An incomplete Form 548 will not be processed.

■ |

COM |

■ |

| Fact Name | Description |

|---|---|

| Purpose of Form | The Tax Power of Attorney (POA) Form 548 allows an individual to authorize another person to act on their behalf in tax matters. |

| Governing Law | This form is governed by the Internal Revenue Code Section 6013(d)(3) and varies by state regulations. |

| Eligibility | Any individual taxpayer can complete and submit Form 548 to designate a representative. |

| Who Can Be an Agent | Both individuals and organizations can serve as agents, including accountants and tax advisors. |

| State-Specific Forms | Many states have their own POA forms for tax purposes which must be used in conjunction with federal forms. |

| Validity Period | The powers granted remain in effect until revoked, but specific limitations can alter this duration. |

| Filing Requirements | The form must be submitted to the appropriate tax authority to ensure the agent has the authority to act. |

| Revocation | Form 548 can be revoked at any time by submitting a written notice to the designated agent and the tax authority. |

| Signature Requirement | The taxpayer’s signature is necessary, affirming their intent to appoint the agent. |

| Confidentiality | While the agent can access tax information, taxpayer confidentiality remains protected under federal law. |

Filling out Tax POA form 548 is an important step for those who wish to authorize someone to act on their behalf regarding tax matters. This process allows you to designate a representative who can handle specific tasks with the IRS. Follow these straightforward steps to successfully complete the form.

Once the form is submitted, the IRS will process your request. Keep in mind that you should follow up if you do not receive confirmation regarding the authorization. Staying organized will help both you and your designated representative effectively manage your tax matters.

What is the Tax POA Form 548?

The Tax Power of Attorney (POA) Form 548 allows an individual to authorize someone else to handle their tax matters with the IRS. This could be a family member, a tax professional, or an attorney. By completing this form, the taxpayer grants the designated person the authority to act on their behalf in dealings with tax authorities.

Who can be appointed as a representative on Form 548?

Any individual can be appointed as a representative through Form 548, provided they are qualified to represent taxpayers before the IRS. This might include tax preparers, attorneys, or accountants. However, the representative must consent to the arrangement and cannot be a party that would create a conflict of interest.

How long does the power of attorney last?

The power of attorney granted through Form 548 remains in effect until the taxpayer revokes it or passes away. Additionally, the IRS will automatically terminate the authority if the designated representative becomes incapacitated or dies. It is essential for taxpayers to keep their records updated for any changes in representation.

What specific powers does Form 548 grant?

Form 548 permits the appointed representative to perform various tasks on behalf of the taxpayer. This includes discussing tax matters with the IRS, receiving and reviewing tax information, and signing tax documents. However, certain decisions, such as filing a legal course of action, may require separate consent or documentation.

Is there a need for the taxpayer to notify the IRS after submitting Form 548?

No additional notification is necessary once Form 548 is submitted. The IRS processes the form and acknowledges the authority granted to the representative. However, it is wise for the taxpayer to retain copies of the form and any related correspondence for their records.

Can multiple representatives be authorized on the same Form 548?

Yes, multiple representatives can be authorized using Form 548. The taxpayer must provide the names and other required details of each representative. Clear communication among all parties is essential to avoid confusion regarding the scope of authority granted to each representative.

What steps should be taken to revoke the power of attorney?

To revoke the power of attorney, the taxpayer must submit a written notice to the IRS, along with a copy of Form 548 that indicates the revocation. It is also best practice to inform the appointed representative that the authority has been rescinded. Keeping accurate records of this process is crucial.

Where can taxpayers find Form 548?

Form 548 can be obtained directly from the IRS website. It is available for download in PDF format, which can be completed and submitted as instructed. Additionally, taxpayers may seek assistance from a tax professional if they require help in completing the form or have any inquiries about the process.

Not Specifying the Correct Tax Matters: One common error is failing to specify the exact tax matters for which the power of attorney (POA) is granted. Ensure you clearly indicate the year or period and types of tax returns involved.

Forget to Sign and Date: It’s critical to sign and date the form. Without a signature and date, the IRS may reject the POA. Remember, both the taxpayer and the representative must provide their signatures.

Incorrect Representative Information: Double-check the information of the person you are authorizing. A common mistake is inaccurate names, addresses, or identification numbers. Ensure all details are entered correctly.

Not Providing Full Authority: Sometimes people don’t realize that they should provide full authority. Make sure you check the boxes that grant the representative the authority to act on your behalf in all tax matters.

Failing to Keep Copies: After submission, some forget to keep a copy of the completed form. It’s important to retain one for your records in case there are questions or issues later.

The Tax Power of Attorney (POA) Form 548 is a crucial document for allowing someone else to handle tax matters on your behalf. However, individuals often need additional forms or documents to ensure tax-related issues are managed effectively. Below is a list of commonly used forms and documents that correspond with a Tax POA.

Understanding these additional forms can facilitate a smoother experience when dealing with tax responsibilities. Working with a representative who has proper authority can save time and reduce stress during tax season.

The IRS Form 2848, known as the Power of Attorney and Declaration of Representative, is similar to Form 548 because both documents authorize an individual to represent a taxpayer in dealings with the Internal Revenue Service. This form must be signed by the taxpayer, granting permission for another person, usually a tax professional, to discuss tax matters on their behalf. Such authorization is crucial for ensuring effective communication and assistance during audits or disputes with the IRS. Both forms require clear identification of the taxpayer, the representative, and the tax matters involved.

Form 8821, Tax Information Authorization, functions similarly to Form 548 by allowing an individual to designate someone to receive the taxpayer's confidential information from the IRS. Unlike Form 2848, however, Form 8821 does not grant the representative the authority to act for the taxpayer in any way or represent them in front of the IRS. It is often used when taxpayers need someone to review their tax information without giving them complete power of attorney, illustrating the nuanced ways in which individuals can manage their tax affairs.

Form 4506, Request for Copy of Tax Return, can be compared to Form 548 in that it involves the rights of the taxpayer and the authority of a designated representative. When a taxpayer needs a copy of their past tax returns, they can authorize someone to request documents on their behalf. While Form 4506 focuses specifically on obtaining copies of returns, it complements the authorization granted in Form 548 by facilitating access to necessary documentation for representatives who may require historical tax information to effectively assist their clients.

Form 8886, Reportable Transaction Disclosure Statement, serves a distinct purpose but shares similarities in terms of authorization. This form is used when taxpayers engage in reportable transactions, and it is crucial to disclose such activities to the IRS. Although it does not serve as a power of attorney, the form requires both the taxpayer's information and the representation of a tax advisor who understands the complexities associated with reportable transactions. Clear disclosure and proper representation are vital in both forms, underscoring the relationship between taxpayers and their advisors in navigating tax obligations.

Lastly, Form 9465, Installment Agreement Request, parallels Form 548 in that both involve situations where a taxpayer needs support. When a taxpayer cannot pay their tax bill in full, this form allows them to request an installment agreement to make payments over time. Although it does not designate a representative in the same way that Form 548 does, it represents a key interaction with the IRS where having the right support – such as an advisor who understands tax debt management – can make a significant difference in the taxpayer’s overall experience and resolution of their tax issues.

When you are filling out the Tax Power of Attorney (POA) form 548, there are several important considerations to keep in mind. These tips will help you navigate the process more efficiently and avoid common pitfalls.

By following these dos and don’ts, you can help ensure that your Power of Attorney form is submitted correctly. Proper preparation and attention to detail are key in this process.

The IRS Form 548, also known as the Power of Attorney (POA) form, is often misunderstood. Here are six common misconceptions about this form, along with clarifications.

This is untrue. Individuals, sole proprietorships, and small businesses can also use Form 548 to designate a representative for tax matters.

Actually, the authority granted is specifically limited to tax matters. Your representative does not gain access to other personal or financial information unless explicitly stated.

In reality, Form 548 must be submitted every time you want to appoint a new representative or if changes are needed regarding the scope of authority.

This is incorrect. You can specify different levels of authority for different representatives, enabling you to customize who can do what.

In truth, you can revoke your Power of Attorney at any time by submitting a new form that clearly states your intent to revoke.

This is misleading. The IRS accepts electronically filed POA forms, making the process more convenient and efficient for taxpayers.

Understanding these misconceptions can help individuals feel more secure when using Form 548 for their tax needs.

When it comes to filling out and using the Tax Power of Attorney (POA) Form 548, there are several important aspects to consider. Understanding these elements can streamline the process and ensure compliance with tax obligations.

By grasping these key takeaways, individuals can effectively navigate the complexities of the Tax POA Form 548, leading to smoother interactions with the IRS and more effective management of tax responsibilities.