When dealing with tax matters, having the right authorizations in place can simplify the process significantly. The Tax Power of Attorney form 49357, also known as the POA-1 form, serves as a vital tool for taxpayers who wish to designate someone to handle their tax-related affairs. This form allows individuals or business entities to appoint a representative to act on their behalf before the IRS. By using the POA-1 form, taxpayers can ensure that their chosen representative has the authority to receive information, make inquiries, and even represent them during audits or discussions regarding tax liabilities. It covers various important components, such as the scope of the authority granted, and the specific tax years or periods that the authorization applies to. The form also details who can serve as a representative, ensuring that individuals understand their options and the implications of their choices. Understanding the functions and features of the POA-1 form is key to navigating the complexities of tax issues with greater ease and confidence.

|

|

|

|

POA - 1 |

|

|

|

|

Indiana Department of Revenue |

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

State Form 49357 |

|

|

|

|

POWER OF ATTORNEY |

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

(R7 / |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

1. Taxpayer Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Taxpayer(s) Name(s) |

|

|

|

|

|

|

|

|

DBA Name(s) (if applicable) |

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

☐ New Address? |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

City |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

Zip Code |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

I |

|

|||

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

2. Identification Numbers |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Indiana Taxpayer Identification Number (10 digits) |

or |

Employer Identification Number |

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

I |

I |

I |

|

|

I |

I |

I |

I |

I |

|

I |

I |

I |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Social Security Number |

|

|

|

|

|

Spouse’s Social Security Number |

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

~l |

|

□ |

~I~ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

Hereby appoint(s) the following: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

3. Representative Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Individual Representative Name |

|

|

|

|

|

|

|

|

Additional Individual Representative Name |

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

City |

|

|

|

|

|

|

|

|

|

|

State |

|

Zip Code |

City |

|

State |

Zip Code |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

Telephone Number |

|

|

|

Telephone Number |

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

Additional Individual Representative Name |

|

|

Additional Individual Representative Name |

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

City |

|

|

|

|

|

|

|

|

|

|

State |

|

Zip Code |

City |

|

State |

Zip Code |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

Telephone Number |

|

|

|

Telephone Number |

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

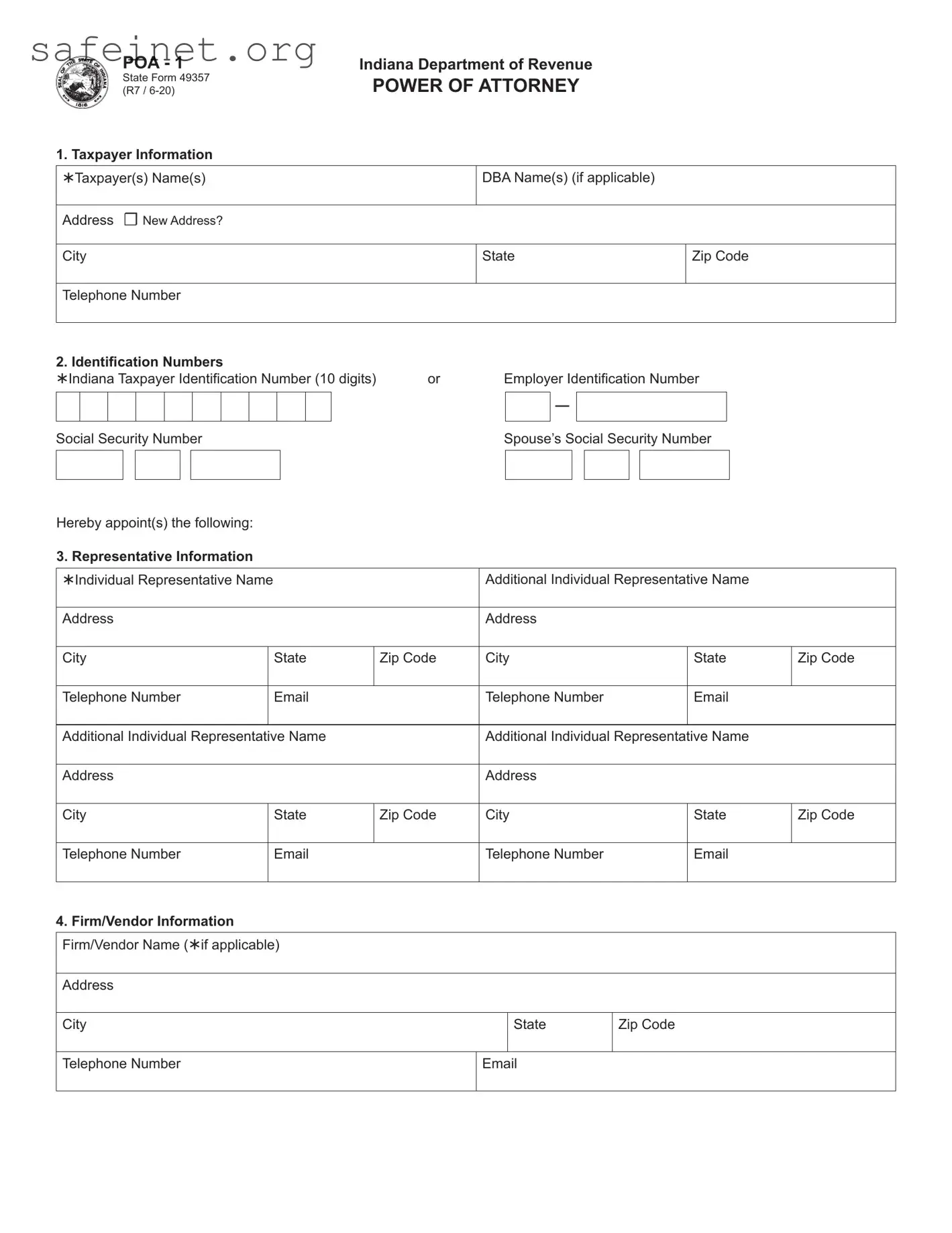

4.Firm/Vendor Information Firm/Vendor Name (if applicable)

Address

City |

|

State |

Zip Code |

|

|

I |

I |

Telephone Number |

|

||

|

I |

|

|

If firm or vendor, list representative(s) name, telephone number and email.

Representative(s) Name

Telephone Number

5. General Authorization

☐I authorize the listed representative(s), in addition to anything otherwise authorized on this form, to represent me regarding any matters with the Indiana Department of Revenue regardless of tax years or income periods. I understand that this authority will expire 5 years from the date this POA is signed or a written and signed notice is filed revoking this authorization.

6.Tax Type(s) (Not applicable if box is checked in question 5 above)

Type of Tax |

Year(s)/Period(s) |

(Income, Withholding, Sales, etc.) |

☐ Current Year ☐ Specify |

_______________________________________ |

___________________________________ |

_______________________________________ |

___________________________________ |

_______________________________________ |

___________________________________ |

I acknowledge that the designated representative has the authority to receive confidential information and full power to perform on behalf of the taxpayer in tax matters related to this Power of Attorney. This authority does not include the power to receive refund checks.

I acknowledge that actions taken by the designated representative are binding, even if the representative is not an attorney. Proceedings cannot later be declared legally defective because the representative was not an attorney.

If I am a corporate officer, partner, or fiduciary acting on behalf of the taxpayer, I certify that I have authority to execute this Power of Attorney on behalf of the taxpayer.

7. Authorizing Signature |

|

Signature _______________________________________________ |

Date _______________________________ |

Printed Name ____________________________________________ |

Title _______________________________ |

Telephone Number ________________________________________ |

Email ______________________________ |

Required fields - if not complete, this form will be returned to sender.

Instructions for Indiana Form

Casual conversations with a taxpayer’s representative who does not have a Power of Attorney on file are permitted. However, the Indi- ana Department of Revenue will not disclose tax return information or

Pursuant to 45 IAC

1.The taxpayer’s name, DBA name (if applicable), address (Please check the box if this is a new address), and telephone number.

2.The Indiana taxpayer’s identification

3.The name, address, and telephone number of your individual representative(s). Only individuals can be named as representatives. If you want to add one individual representative, enter one in the spaces provided. If you want to add more representatives, enter them in the spaces provided.

4.If your representative works for a consulting firm or vendor, enter the company’s name, address, telephone number, and email address. Enter the individual representative name(s) employed by the firm or vendor you have designated. If you want to add more than four individual representatives for a firm or vendor, you can provide the names of those representatives in a separate list, to be attached to this Power of Attorney form.

If you wish for your firm to be represented generally by a company such as a payroll processor, enter the company’s name,

address, telephone number, and email address. If the company is not listed, you must provide the names of one or more individual |

|

representatives. |

|

|

|

5.Check this box if you want to authorize your representative to represent you regarding all tax matters, regardless of the tax year or income period involved.

6.The Power of Attorney form can contain the specific type of tax, or the option ALL. By choosing the option ALL, you will be allowed access to ALL tax types appropriate to the taxpayer. The tax years must be specific.

7.The taxpayer’s signature or the signature of an individual authorized to execute the Power of Attorney on the taxpayer’s behalf.

NOTE: Include as an enclosure any restrictions or limitations the taxpayer has placed on the representative while acting as the tax- payer’s representative.

After the taxpayer executes a Power of Attorney, the department will communicate primarily with the taxpayer’s representative.

The department accepts faxed copies of original Power of Attorney forms. If a copy is provided, the person forwarding the copy certifies, under penalties for perjury, that the copy is a true, accurate, and complete copy of the original document.

Do not send

The department will not accept a Power of Attorney form that has been altered unless it has the initials of the taxpayer (or an individual authorized to execute the Power of Attorney on the taxpayer’s behalf) beside the alteration(s).

This Power of Attorney is effective for 5 years from the date the form is signed. After the expiration of 5 years, a new Power of Attorney form must be completed if the taxpayer wishes to permit the department to communicate with the taxpayer’s representative.

This Power of Attorney can be revoked prior to expiration only by written and signed notice. A subsequent Power of Attorney alone will NOT revoke a prior Power of Attorney.

Required fields – if not complete, this form will be returned to sender.

Submit the form using these methods:

•Fax: (317)

•Mail: Indiana Department of Revenue PO Box 7230

Indianapolis, IN

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 49357 (POA-1) allows individuals to authorize a third party to represent them before the IRS. |

| Filing Requirement | This form must be submitted whenever a taxpayer wants to designate someone, like a tax professional, to act on their behalf. |

| Scope of Authority | The form specifies the extent of the authority granted to the representative, which can include accessing tax records and discussing tax matters. |

| State Specificity | While the POA-1 is federal, some states have their own versions, such as California's Form 3520, governed by California Revenue and Taxation Code. |

| Signature Requirement | The taxpayer must sign the form to validate the authorization. Without this signature, the form is not recognized by the IRS. |

| Expiration | The authorization remains in effect until the taxpayer revokes it or the representative withdraws. |

| Multiple Representatives | Taxpayers can appoint multiple representatives by listing each on the form. Each representative must also provide their contact information. |

| Submission Methods | The completed form can be submitted via mail, fax, or electronically, depending on the IRS guidelines. |

| Access to IRS Information | Once processed, the authorized representative can access information regarding the taxpayer’s accounts and tax returns. |

Once you've obtained Form 49357 (POA-1), you’re ready to complete it. This form is essential for designating a representative to handle tax matters on your behalf, ensuring that your interests are properly represented. Keeping your information accurate and complete is crucial, as any errors could delay the process. Follow these steps carefully to fill out the form correctly.

After filling out the form, keep a copy for your records. If sent by mail, consider using a service that provides tracking for peace of mind. Your chosen representative will then be able to engage with the tax authority on your behalf, ensuring that your needs are met efficiently.

What is the Tax POA form 49357 (POA-1)?

The Tax POA form 49357, also known as POA-1, allows individuals to authorize someone else to represent them before the IRS regarding tax matters. This form grants the designated representative the authority to act on your behalf in discussions, negotiations, and any actions necessary regarding your tax responsibilities.

Who can I designate as my representative using this form?

You can designate anyone you trust as your representative, including a family member, friend, or professional such as an attorney or accountant. The important aspect is that the representative must agree to take on this responsibility and meet any requirements set by the IRS.

Do I need to provide any specific information on the form?

Yes, the form requires basic information about both you and your chosen representative. This includes names, addresses, Social Security numbers (or Employer Identification Numbers), and any relevant tax identification numbers. Ensure that this information is accurate to avoid processing delays.

How do I submit the POA-1 form to the IRS?

You can submit the completed form to the IRS by mailing it to the address specified in the instructions for the form. Alternatively, you may submit it electronically if you’re using certain tax software that supports e-filing of POA forms. Always keep a copy for your records after submission.

How long does the POA authorization last?

The authorization lasts until you revoke it or until the specific tax matters for which the POA was granted are resolved. You can revoke the power of attorney at any time by submitting a written notice to the IRS along with a copy of your POA form.

Can I limit the authority granted to my representative?

Absolutely. The form allows you to specify the extent of the authority you grant. You can restrict the representative to certain tax periods, types of tax, or specific issues. Clearly detailing these limitations on the form will help ensure your wishes are respected.

What happens if I don't submit the form?

If you do not submit the POA-1 form, you will need to handle any IRS communications and issues yourself. It may become challenging to manage complex tax matters alone, especially if you need expert advice or assistance in negotiations with the IRS.

Can I revoke the POA if I change my mind?

Yes, you can revoke the power of attorney at any time. Simply submit a written revocation notice to the IRS and provide a copy of your original POA form. This will officially terminate the authorization and prevent your representative from acting on your behalf.

Where can I find help with filling out the POA-1 form?

Assistance is available through various channels. You may find detailed instructions on the IRS website. Additionally, seeking help from a tax professional can ensure the form is completed correctly and meets all necessary requirements. Don't hesitate to ask questions if you need further clarification.

Incomplete Information: Failing to provide all required details can lead to processing delays. Always double-check that your name, Social Security number, and address are filled out accurately.

Wrong Representative Information: It's essential to ensure that the representative’s details, including their name and credentials, are correct. Errors here could cause the IRS to reject the form.

Not Signing the Form: Remember that your signature is necessary. Submitting a POA form without a signature invalidates it.

Incorrect Scope of Authority: Be clear about what powers you want to grant your representative. Ambiguities can lead to misunderstandings and limit their effectiveness.

Ignoring State-Specific Requirements: Some states might have additional requirements or forms. It’s wise to research if your state has specific needs related to tax POA.

Failing to Update or Revoke: If your circumstances change, don’t forget to update or revoke your POA. Keeping outdated forms can lead to complications.

Using Old Versions of the Form: Always use the latest version of the POA form. The IRS updates forms periodically, and using an old version may result in rejection.

Not Specifying the Tax Matters: Clearly outline the tax issues for which the POA is applicable. This helps streamline the process for your representative.

Missing Backup Documentation: Depending on your situation, you may need to include additional documents. Check to ensure you have all necessary paperwork attached.

Filing in the Wrong Place: Finally, always verify where to send your completed form. Sending it to the wrong address can slow down processing.

By being mindful of these common pitfalls, you can ensure a smooth experience when submitting the Tax POA form 49357 (POA-1). Taking a few extra moments to review can save you time and frustration down the line.

The Tax Power of Attorney form 49357 (POA-1) is a key document that authorizes an individual or entity to act on behalf of a taxpayer in matters concerning tax obligations. Along with this form, there are other important documents that may be utilized to streamline the process of tax representation. Below are some commonly used forms related to this purpose.

Understanding these documents can help ensure that tax-related matters are handled effectively and in a timely manner. Each form serves a specific purpose and, when used in conjunction with the Tax POA form, can facilitate communication and representation with tax authorities.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is commonly used by individuals or businesses to give consent to another person to represent them before the IRS. Like the Tax POA form 49357, this document allows for the designation of one or more representatives who have the authority to act on behalf of the taxpayer. It specifically allows the representative access to the taxpayer’s records and the ability to receive confidential information related to the taxpayer's financial standing and tax matters.

The IRS Form 8821, Tax Information Authorization, is another similar document. This form enables individuals to authorize a third party to receive and inspect their tax information. Unlike the POW-1, Form 8821 does not allow the designated party to represent the taxpayer before the IRS but does grant access to the taxpayer’s information for various purposes, such as financial and legal advice.

The IRS Form 4506, Request for Copy of Tax Return, serves a different function but often works in conjunction with a power of attorney document. This form is used to request copies of previously filed tax returns. A representative authorized by the taxpayer may use this document along with a POA to obtain necessary tax records for audit or review purposes.

The Form 1065, U.S. Return of Partnership Income, allows partnerships to file taxes and designate a partner to sign on behalf of the entity. This form has elements that can be viewed similarly to the Tax POA form because it authorizes one partner who acts on behalf of all other partners for tax matters, facilitating communication with the IRS.

Form 8879, IRS e-file Signature Authorization, is utilized in e-filing scenarios. By signing this form, taxpayers authorize the e-filing of their tax return through a tax professional. In a way similar to the POA, it grants authority for a professional to submit tax returns electronically, although it does not grant broader representation powers.

Each state has its own power of attorney forms, like California's Form POA-1, which allows individuals to designate someone to act on their behalf in matters including tax. Similar to the federal Tax POA form, state POA forms enable representatives to handle issues related to state taxes and any other financial matters within their jurisdiction.

The Uniform Power of Attorney Act (UPOAA) provides a general framework for powers of attorney that can include tax matters. Many states have adopted this model act, which allows individuals to designate others to handle a variety of affairs. This general template functions similarly to Tax POA form 49357 in terms of granting authority to act on another’s behalf but covers a broader scope, including legal, medical, and financial matters.

The IRS Form 56, Notice Concerning Fiduciary Relationship, allows a taxpayer to appoint a fiduciary who can act on their behalf concerning tax matters. While not strictly a power of attorney form, it shares a fundamental purpose of representation in tax issues, enabling a fiduciary to manage tax responsibilities for an individual unable to do so themselves.

The IRS Form 8822, Change of Address, may not directly revolve around representation. However, it is often used in conjunction with power of attorney forms when a taxpayer needs to update their address for correspondence. Proper handling of all tax-related documents is critical, and ensuring accurate address records can help representatives carry out their duties effectively.

The IRS Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return, requires representation when filing on behalf of an estate. Executors or administrators of an estate may use a power of attorney to manage tax filings and obligations of the deceased. This form of representation emphasizes the need for trusted individuals to manage tax-related affairs effectively.

When filling out the Tax POA form 49357 (POA-1), it is important to consider the following dos and don'ts:

There are several misconceptions surrounding the Tax Power of Attorney form 49357 (POA-1). Understanding these can help individuals navigate the complexities of tax representation effectively.

This is not true. The POA-1 form can designate multiple representatives. Taxpayers can authorize more than one person, allowing them to seek assistance from various professionals as needed.

This notion is incorrect. While the POA-1 does allow a representative to act on the taxpayer's behalf, the taxpayer always retains the right to revoke the power of attorney or withdraw consent at any time. Control remains with the taxpayer.

This belief is misleading. Individuals can also use the POA-1 form. It serves as a valuable tool for anyone needing representation for tax issues, whether they are individuals or businesses.

This assumption lacks clarity. While a properly completed POA-1 form allows a representative to communicate with tax authorities on behalf of the taxpayer, it does not guarantee the resolution of all matters. The outcome will depend on the specifics of the case.

When filling out the Tax POA form 49357 (POA-1), consider the following key takeaways: