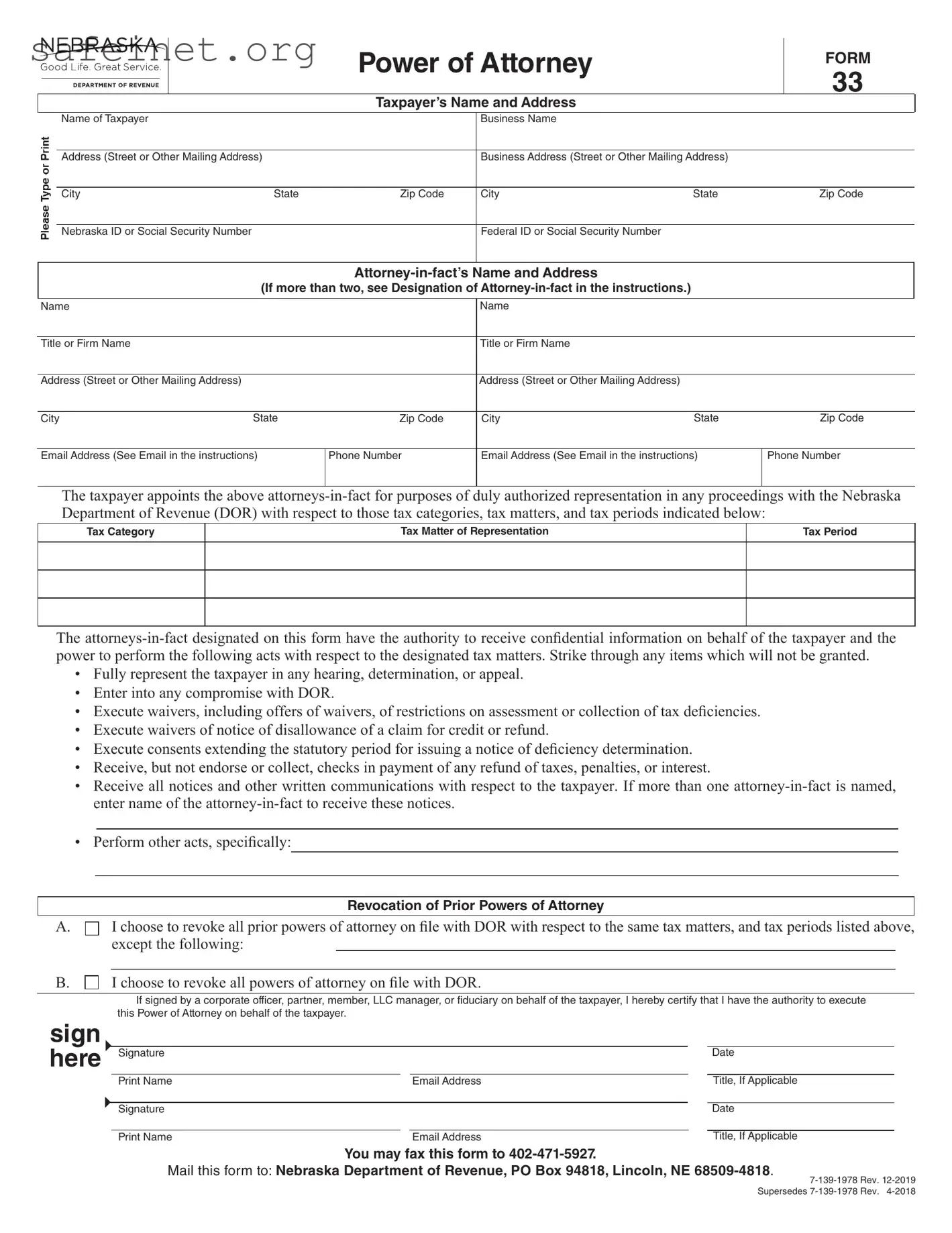

The Tax POA Form 33 is an essential tool for taxpayers who wish to authorize someone else to act on their behalf regarding tax matters. This form allows you to designate an individual—often a tax professional or attorney—to handle various interactions with the IRS or state tax authorities. By submitting Form 33, you grant your representative the authority to receive information, make inquiries, and secure access to your tax records, which can be particularly beneficial during audits or other proceedings. Moreover, the form simplifies communication between you and the tax agency, ensuring that your representative can advocate on your behalf while maintaining your privacy. Completing the Tax POA Form 33 carefully is critical, as it requires specific details such as the taxpayer's information, the representative’s details, and the scope of authority granted. Furthermore, understanding the implications of this form can help you navigate the complex world of taxation more effectively, enabling you to stay informed about your tax obligations while having a qualified individual handle the heavy lifting.

|

b)_EBRASl<A- |

|

|

Power of Attorney |

|

FORM |

||||||

|

Good Life. Great Service. |

|

|

|

||||||||

|

|

|

|

|

|

33 |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||

I |

|

|

|

|

Taxpayer’s Name and Address |

|

|

I |

||||

|

|

|

Name of Taxpayer |

|

|

Business Name |

|

|

|

|

||

|

|

C: |

|

|

|

|

|

|

|

|

|

|

~- |

|

|

|

|

|

|

|

|||||

Address (Street or Other Mailing Address) |

|

|

Business Address (Street or Other Mailing Address) |

|

|

|

||||||

0 |

|

|

|

|

|

|

|

|

|

|

||

|

|

Q) |

|

|

|

|

|

|

|

|

|

|

|

~a. |

|

|

|

|

|

|

|

||||

City |

State |

Zip Code |

City |

State |

Zip Code |

|

|

|||||

|

|

..Q) |

|

|

|

|

|

|

|

|

|

|

|

|

Q) |

|

|

|

|

|

|

|

|

|

|

1/1 |

|

|

|

|

|

|

|

|

|

|

||

|

ii: |

Nebraska ID or Social Security Number |

|

|

Federal ID or Social Security Number |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

I

(If more than two, see Designation of

I

Name |

|

|

Name |

|

|

|

|

|

|

|

|

Title or Firm Name |

|

|

Title or Firm Name |

|

|

|

|

|

|

|

|

Address (Street or Other Mailing Address) |

|

|

Address (Street or Other Mailing Address) |

|

|

|

|

|

|

|

|

City |

State |

Zip Code |

City |

State |

Zip Code |

|

|

|

|

||

Email Address (See Email in the instructions) |

Phone Number |

Email Address (See Email in the instructions) |

Phone Number |

||

|

|

I |

|

|

I |

The taxpayer appoints the above

Tax Category

Tax Matter of Representation

Tax Period

The

•Fully represent the taxpayer in any hearing, determination, or appeal.

•Enter into any compromise with DOR.

•Execute waivers, including offers of waivers, of restrictions on assessment or collection of tax deficiencies.

•Execute waivers of notice of disallowance of a claim for credit or refund.

•Execute consents extending the statutory period for issuing a notice of deficiency determination.

•Receive, but not endorse or collect, checks in payment of any refund of taxes, penalties, or interest.

•Receive all notices and other written communications with respect to the taxpayer. If more than one

•Perform other acts, specifically:

|

|

|

|

Revocation of Prior Powers of Attorney |

|

|

|

||||

A. □ |

|

I choose to revoke all prior powers of attorney on file with DOR with respect to the same tax matters, and tax periods listed above, |

|||||||||

|

|

except the following: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

B. □ |

|

I choose to revoke all powers of attorney on file with DOR. |

|

|

|

||||||

|

|

If signed by a corporate officer, partner, member, LLC manager, or fiduciary on behalf of the taxpayer, I hereby certify that I have the authority to execute |

|||||||||

sign |

|

this Power of Attorney on behalf of the taxpayer. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

here |

|

|

|

|

|

|

|

|

|||

|

Signature |

|

|

|

|

|

Date |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Name |

|

|

|

Email Address |

Title, If Applicable |

|

|||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|||

|

|

Signature |

|

|

|

|

|

Date |

|

||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Name |

|

|

|

Email Address |

Title, If Applicable |

||||

|

|

|

|

|

|

|

|||||

You may fax this form to

Mail this form to: Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

Supersedes

Instructions

Who Must File. Any taxpayer who wishes to secure representation by another party in matters before the Nebraska Department of Revenue (DOR) with regard to any tax imposed by the tax laws of the State of Nebraska, must fle a Power of Attorney (POA), Form 33, or other appropriate POA. A POA authorizes that party to receive confdential tax information regarding the taxpayer. The Form 33 is provided for the taxpayer’s convenience in designating a POA, but it is not the sole form which may be used. DOR will honor all other properly completed and signed POA authorizations.

When and Where to File. The completed Form 33 may be fled any time. This form, or another properly completed and signed POA, must be fled with DOR before any person designated can represent the taxpayer in matters involving disclosure of confdential tax information.

This form, or other appropriate POA, may be faxed or mailed to DOR:

•Fax to

•Mail to the Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

Taxpayer’s Name and Address. If the taxpayer is an individual, a Social Security number must be listed. If a married, fling jointly return was fled, enter both spouses’ Social Security numbers in the spaces provided.

If the taxpayer is a corporation, partnership, or association, enter the name, state and federal ID numbers (if applicable), and the business address. If the Form 33 will be used in a tax matter in the case of a partnership for which the names, addresses, and Social Security numbers or ID numbers have not already been furnished to DOR, these items should be listed on an attached sheet.

If the taxpayer is an estate or trust, enter the name, title, and address of the fduciary, as well as the name and ID number or Social Security number of the taxpayer. If this space is used to list other information, clearly label the change.

Designation of

Email. By entering an email address, the taxpayer acknowledges that DOR may contact the taxpayer by email. The taxpayer accepts any risk to confdentiality associated with this method of communication. DOR will send all confdential information by secure email or the State of Nebraska’s fle share system. If you do not wish to be contacted by email, write “Opt Out” on the line labeled “email address.”

Tax Category, Tax Matter, and Tax Period. Form 33 is designed to clearly express the scope of the authority granted by the taxpayer to any

“Tax Category” requires a list of the type of tax, such as “income” or “sales and use.” “Tax Matter of Representation” requires a brief summary of the subjects for which the attorney-

Authorized Acts. The Form 33 lists several acts which can be performed by the

If the taxpayer wishes to authorize an act which is not listed, a concise and specifc statement about the additional authorization must be made in the space provided, or a separate signed statement may be attached to the Form 33.

Revocation of Prior Powers of Attorney. To revoke any POAs previously fled with DOR, choose Box A or B.

Box A. Checking this box allows the taxpayer the option of revoking all POAs on fle with DOR with the exception of those listed on the lines provided (or on a list attached to the Form 33). Check box A and list the names, addresses, and zip codes of the

Box B. Checking this box revokes all POAs previously fled with DOR. Check Box B, and sign the form.

If no boxes are checked, all prior POAs will remain in force.

Signature. The taxpayer must sign and date the form. If spouses fle a married, fling jointly income tax return, which both have signed, then both spouses must sign the Form 33. If only one spouse in a married couple signs Form 33, then a separate Form 33 must be signed by the other spouse. If there is only one spousal signature or a second POA is not signed, then only the person designated by the POA would be authorized to perform the acts authorized by the POA. The nonsigning spouse who has fled a joint return with his or her spouse may still obtain information about, and may discuss issues regarding, the couple’s joint return. However, a person may not authorize another party, or themselves, to receive confdential tax information regarding separate returns fled by the person’s spouse.

Only certain people may represent a taxpayer in a contested case once a hearing offcer is appointed: (1) the taxpayer;

(2)a Nebraska attorney; or (3) a

If the taxpayer is a partnership, all partners must sign, unless one is duly authorized to act in the name of the partnership. Nebraska has adopted the Uniform Partnership Act of 1998 (Neb. Rev. Stat. §§

If the taxpayer is a corporation or an association, an offcer having authority to bind the entity must sign. The offcer must indicate his or her offcial title on the line provided.

If the taxpayer is a Nebraska limited liability company (LLC), then the Form 33 must be signed by a member of the LLC. The validity of the authorizations made by a foreign LLC will be determined governed by the laws of the state in which the LLC was organized.

| Fact Name | Description |

|---|---|

| Purpose | The Tax Power of Attorney (POA) form 33 allows a designated representative to manage your tax affairs with the state tax authority on your behalf. |

| Governing Laws | The form is governed by state tax laws, including but not limited to specific regulations set forth by the Department of Revenue in your state. |

| Who Can Use It | Any individual or business entity can use the POA form 33 to appoint a representative to handle their tax matters. |

| Submission | The completed form must be submitted to the appropriate state tax agency, where it becomes effective upon approval. |

Once you have gathered the necessary information, you are ready to complete the Tax POA Form 33. This form will allow a designated individual to act on your behalf regarding tax matters, enabling smooth communication with tax authorities.

What is the Tax POA Form 33?

The Tax Power of Attorney (POA) Form 33 is a document that allows a taxpayer to designate an authorized representative to act on their behalf concerning tax matters. This form enables your chosen representative to communicate with the IRS, handle your tax issues, and receive sensitive tax information. Completing and submitting this form is essential for ensuring that your taxes are managed according to your preferences, especially if you cannot handle them directly due to various reasons such as time constraints, health concerns, or simply the need for expert assistance.

Who can be designated as a representative on the Tax POA Form 33?

A representative must meet certain criteria to be authorized through the Tax POA Form 33. Generally, this person can be a certified public accountant (CPA), an attorney, or an enrolled agent. However, taxpayers can also designate a trusted friend, family member, or colleague, as long as they sign the form. It's crucial that the chosen individual understands tax matters and can navigate the complexities of the IRS processes effectively. Having an informed representative can greatly reduce potential issues with tax filings and correspondence.

How do I complete and submit the Tax POA Form 33?

To complete the Tax POA Form 33, start by filling in your personal information, including your name, address, and Social Security number or Employer Identification Number (EIN). Next, provide the details of the representative you wish to designate, ensuring their name and contact information are accurate. Additionally, indicate the specific tax matters for which the representative will have authority. After completing the form, it must be signed and dated by you, the taxpayer. Submission can typically be done via mail, and it’s wise to keep a copy for your records. Some taxpayers may also be able to submit the form electronically if their representative has authorization to e-file on their behalf.

What happens after submitting the Tax POA Form 33?

Once the Tax POA Form 33 is submitted and processed by the IRS, your designated representative will receive a confirmation of their authority to act on your behalf. They will then be able to contact the IRS for inquiries, review your tax account, and receive unredacted copies of your tax returns. However, it’s important to remain engaged in your own tax matters, as the final responsibility and liability still rest with you as the taxpayer. Periodically checking in with your representative about your tax situation can foster a beneficial relationship and keep you informed of any developments.

Not including sufficient personal identification information. Make sure to provide your full name, address, and Social Security number or taxpayer identification number.

Failing to sign the form. The form is not valid unless it is signed by the taxpayer.

Using outdated versions of the form. It's crucial to use the latest version available from the IRS website to ensure compliance.

Not specifying the tax matters. Clearly state what tax years or types of taxes are covered by the Power of Attorney.

Leaving out the representative information. Provide full details about the person you are authorizing, including their name and contact information.

Submitting the form without keeping a copy. Always retain a copy for your own records after submission.

Neglecting to use clear and legible handwriting. Ensure all information is easy to read to avoid processing delays.

Forgetting to update the form if circumstances change. If your representation or tax matters change, submit a new form.

Not checking for accuracy before submission. Double-check all information for errors or omissions to prevent any issues with the IRS.

When dealing with tax matters, the Tax Power of Attorney (POA) form 33 is often accompanied by several other important documents. These documents help facilitate communication with tax authorities and ensure that your rights and interests are protected. Below is a list of common forms and documents that may be used alongside the Tax POA form 33.

Collectively, these documents can help ensure that your tax-related matters are handled efficiently and effectively. Keeping them organized and readily accessible can make a significant difference during your interactions with tax authorities.

The Tax Power of Attorney (POA) form 33 is similar to the Durable Power of Attorney. Both documents allow someone to act on behalf of another person in financial matters. While the Tax POA specifically grants authority over tax-related decisions, the Durable Power of Attorney applies to a broader range of financial and legal transactions. This wider scope makes the Durable POA useful for various situations, including those where an individual becomes incapacitated.

Another similar document is the Limited Power of Attorney. Like the Tax POA, the Limited Power of Attorney grants specific authority to act on behalf of another person, but it usually covers a narrower set of tasks. The holder of the Limited POA can only make decisions in the areas specified. This makes it helpful for situations where someone wants to delegate authority for a particular purpose, such as signing documents for a specific real estate transaction.

The Healthcare Power of Attorney also shares similarities with the Tax POA form 33. This document permits someone to make healthcare decisions for another person when they can no longer do so themselves. While the Tax POA deals specifically with tax matters, both documents involve granting someone the power to act in critical situations where quick decisions are necessary.

Next, there's the General Power of Attorney. This document gives the agent broad authority to handle various financial matters, much like the Tax POA allows for tax-related issues. However, the General Power of Attorney is not limited to taxes and extends to other financial transactions. Users appreciate this document for its flexibility, allowing for a wide range of actions in the financial realm.

The Affidavit is another document that resembles the Tax POA form 33. It’s used to affirm that something is true in a legal context. While an Affidavit doesn’t authorize someone to act on your behalf, it can be related. For instance, if a tax issue requires a sworn statement, the Tax POA can empower someone to submit that affidavit on your behalf, facilitating the resolution of tax matters.

Then, there’s the Consent to Release Information form. This document permits a third party, often a tax professional, to access your private tax information. Though it doesn’t grant the authority to make decisions, it allows the third party to obtain necessary data for tax preparation or audits. This is crucial for situations where detailed information from tax documents is required for filing.

Power of Attorney for Finances is another related document. It allows someone to manage another’s financial affairs, which can sometimes include tax responsibilities. This type of document offers broad control over financial matters but may not be limited to taxes. It's useful for individuals looking for someone to manage all aspects of their financial life.

Finally, there’s the Letter of Authorization. Similar to the Tax POA, this letter permits someone to act on another's behalf in specific matters. While it may not carry the same legal weight as a formal Power of Attorney, it still allows for limited representation, particularly in simpler situations where formal documentation may not be necessary.

When completing the Tax Power of Attorney (POA) Form 33, it is essential to adhere to best practices to ensure accuracy and compliance with the law. Below are five important do's and don'ts to consider.

The Tax Power of Attorney (POA) Form 33 can often lead to confusion. Here are nine common misconceptions about this form, along with clarifications to help you better understand it.

This is not true. The form is used to appoint someone to represent you before the IRS, but it does not need to be submitted with every tax return. You should only file it when you want someone else to act on your behalf.

Actually, you can name multiple representatives on the form. Just make sure to provide the necessary details for each person you wish to authorize.

This is incorrect. You have the right to revoke the POA at any time. To do this, you simply need to submit a written notice to the IRS.

There is no requirement for notarization. The signature you provide on the form is sufficient. However, make sure it is signed appropriately.

The Tax POA Form 33 is specific for federal tax matters. It does not cover state or other types of taxation issues. Make sure you know which jurisdiction the issue falls under.

This is false. You can specify which actions your representative can take on your behalf. Be clear about the limits you want to establish.

It is not just for complicated issues. If you prefer assistance with any aspect of your tax matters, you can use this form to grant power to someone you trust.

The process is quite straightforward. Fill out the required information, sign it, and submit it to the IRS. Simple steps lead to effective representation.

Your representative can only access information relevant to the specific matters you outlined on the POA form. They cannot misuse the access for unrelated issues.

Understanding these misconceptions can help you make informed decisions about managing your tax affairs. If there are uncertainties, seeking guidance from a tax professional is always a good choice.

When it comes to filling out and using the Tax POA form 33, it's important to keep a few key points in mind. This form is essential for appointing someone to represent you before the IRS concerning tax matters. Here are some important takeaways:

By keeping these takeaways in mind, you can confidently complete and use the Tax POA form 33, ensuring a smoother experience for you and your representative.