The IRS Power of Attorney (POA) Form 2848-ME is a crucial document for individuals seeking to designate someone to represent them in tax matters. By filling out this form, you grant your chosen representative the authority to handle various tax-related issues on your behalf. This includes communicating with the IRS, accessing your tax information, and making decisions regarding your tax filings. The form is particularly important for those who may be unable to manage their tax obligations themselves, whether due to time constraints, complexity of the tax code, or personal circumstances. Completing Form 2848-ME correctly ensures that your representative can act effectively and in your best interests. Additionally, it delineates the specific powers you confer to them, allowing for tailored representation that meets your unique needs. In any tax situation, ensuring proper representation can alleviate stress and facilitate smoother communication and resolution with the IRS.

FORM

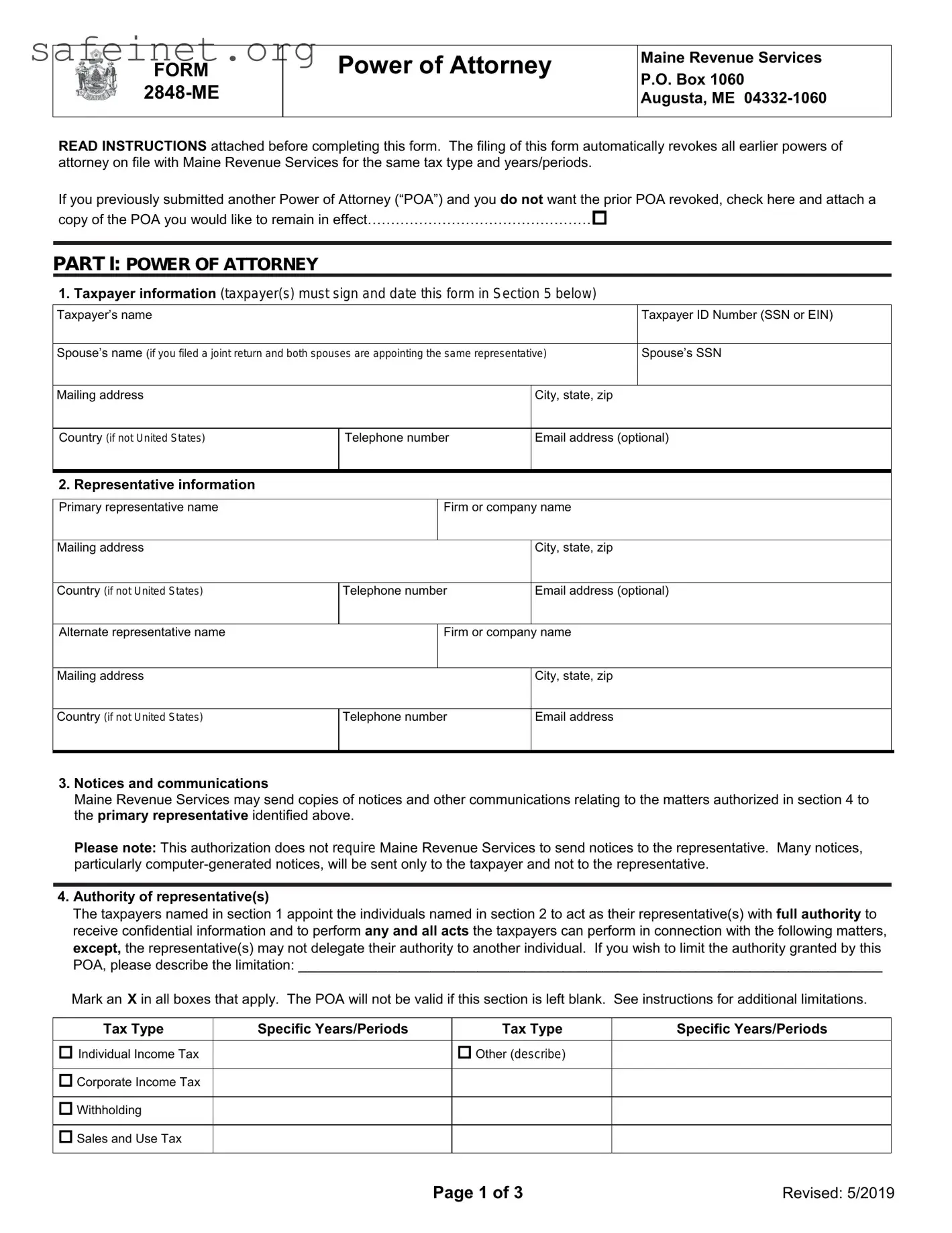

Power of Attorney

Maine Revenue Services

P.O. Box 1060

Augusta, ME

READ INSTRUCTIONS attached before completing this form. The filing of this form automatically revokes all earlier powers of attorney on file with Maine Revenue Services for the same tax type and years/periods.

If you previously submitted another Power of Attorney (“POA”) and you do not want the prior POA revoked, check here and attach a copy of the POA you would like to remain in effect…………………………………………

PART I: POWER OF ATTORNEY

1.Taxpayer information (taxpayer(s) must sign and date this form in Section 5 below)

Taxpayer’s name |

Taxpayer ID Number (SSN or EIN) |

|

|

Spouse’s name (if you filed a joint return and both spouses are appointing the same representative) |

Spouse’s SSN |

|

|

Mailing address

Country (if not United States) |

Telephone number |

I

2. Representative information

City, state, zip

Email address (optional)

Primary representative name |

Firm or company name |

|

I |

|

City, state, zip |

Mailing address |

|

|

|

|

|

|

Email address (optional) |

Country (if not United States) |

Telephone number |

||

|

I |

|

name |

Alternate representative name |

Firm or company |

|

|

|

I |

|

City, state, zip |

Mailing address |

|

|

|

|

|

|

Email address |

Country (if not United States) |

Telephone number |

||

|

I |

|

|

3.Notices and communications

Maine Revenue Services may send copies of notices and other communications relating to the matters authorized in section 4 to the primary representative identified above.

Please note: This authorization does not require Maine Revenue Services to send notices to the representative. Many notices, particularly

4.Authority of representative(s)

The taxpayers named in section 1 appoint the individuals named in section 2 to act as their representative(s) with full authority to receive confidential information and to perform any and all acts the taxpayers can perform in connection with the following matters, except, the representative(s) may not delegate their authority to another individual. If you wish to limit the authority granted by this POA, please describe the limitation: ___________________________________________________________________________

Mark an X in all boxes that apply. The POA will not be valid if this section is left blank. See instructions for additional limitations.

Tax Type |

Specific Years/Periods |

Tax Type |

Individual Income Tax |

|

Other (describe) |

Corporate Income Tax

Withholding

Sales and Use Tax

Specific Years/Periods

Page 1 of 3 |

Revised: 5/2019 |

5.Taxpayer signature

I certify, under penalty of perjury, that I am the taxpayer identified in section 1 above, or if signing as a corporate officer, that I am a partner, member, manager, or fiduciary acting on behalf of the taxpayer, that I have the authority to execute this POA.

Signature

Print name (and title, if applicable)

Date

Spouse’s signature (required if listed above)

Print name

Date

PART II: DECLARATION OF REPRESENTATIVE

I certify, under penalty of perjury, that I am:

Primary Alternate

A member in good standing of the bar of the highest court of the following jurisdiction: ______________________

Duly qualified to practice as a certified public accountant in the following jurisdiction: _______________________

|

An enrolled agent under U.S. Department of Treasury Circular 230 |

A bona fide officer of the taxpayer’s organization

A

|

A member of the taxpayer’s immediate family |

A fiduciary of the taxpayer

Other (explain): ______________________________________________________________________________

Signature – Primary Representative

Print name (and title, if applicable)

Date

Signature – Alternate Representative

Print name (and title, if applicable)

Date

FORMS NOT SIGNED, DATED, OR OTHERWISE INCOMPLETE WILL NOT BE ACCEPTED.

Page 2 of 3 |

Revised: 5/2019 |

Instructions

General Information

Use Form

Unless you limit the authority (see section 4), your representative will be authorized to perform any and all acts you can perform, including, but not limited to: receiving your confidential information; agreeing to tax adjustments; signing settlement agreements; and making otherwise binding decisions on your behalf with regard to the tax matters covered by the POA.

Limited Power of Attorney Form

If you want your representative to communicate with and receive confidential information from MRS, but you do not want that person to act on your behalf, please fill out Form

Revocation

Filing Form

Example 1:

On 5/1/2017, you authorize Jane Doe to represent you for individual income tax for 2015. On 10/1/2017, you authorize Jim Jones to represent you for individual income tax for 2016. Both POA’s are valid.

Example 2:

On 5/1/2017, you authorize Jane Doe to represent you for individual income tax for 2015. On 10/1/2017, you authorize Jim Jones to represent you for sales and use tax for 2015. Both POA’s will be valid.

Example 3:

On 5/1/2017, you authorize Jane Doe to represent you for individual income tax for 2015. On 10/1/2017, you authorize Jim Jones to represent you for individual income tax for years

If you do not want a prior POA automatically revoked, you must check the box at the top of the form and attach a copy of the prior POA you would like to remain in effect.

Other requests to revoke a POA must be in writing and must be signed by the taxpayer.

Section 2 – Representative information

Form

Section 3 – Notices and communications

MRS may send copies of notices and other communications relating to the tax matters authorized in section 4 only to the primary representative. Many notices, particularly

Section 4 – Authority of representatives

This section allows you to specify which tax matters are covered by the POA and what authority you are granting your representative. By default, your representative will have full authority to receive your confidential information and to perform any and all acts you can perform in connection with the matters described in section 4. However, your authorized representative may not delegate their authority to another individual. If you wish to limit your representative’s authority, please specifically describe the limitation.

For this form to be valid, you must select both the tax type and years/periods covered by the POA. If no tax type is selected, the POA will not be accepted.

You may list current, prior, or future years/periods. You must use specific periods. General references such as “All Years” will not be accepted.

Note: MRS will not accept a POA for future years/period which begin more than three years from the date the POA is received by MRS.

Section 5 – Taxpayer signature

You must sign, print your name, and date the POA for it to be valid. If you filed a joint return and both spouses are appointing the same representative, both spouses must sign. POA forms must be hand- signed.

If you are signing on behalf of the taxpayer, please include your

PART I – Power of Attorney

Section 1 – Taxpayer information

The Taxpayer’s identification number may be a social security number (“SSN”) or employer identification number (“EIN”) depending on the type of taxpayer. Please fill out the taxpayer information section accurately and completely. Note: By providing an email address, you authorize MRS to communicate your confidential information via email to the address provided.

PART II – Declaration of Representatives

Your representative must indicate their relationship to you and sign and date the form. The POA must be signed by the representative to be valid.

Submitting Completed POA Form

Completed POA forms should be mailed to MRS at the address at the top of the form. Completed POA forms may also be faxed or emailed to the MRS division responsible for the tax type covered by the POA. For fax/email contact info for the specific divisions, visit our website at: www.maine.gov/revenue/about/contact.

Page 3 of 3 |

Revised: 5/2019 |

| Fact Name | Description |

|---|---|

| Purpose of Form | The Tax POA Form 2848-ME is used by individuals to authorize someone to represent them before the Maine Revenue Services for tax matters. |

| Governing Law | This form is governed by the laws of the State of Maine, specifically the Maine Taxation statute. |

| Who Can Be Authorized | Individuals can authorize a certified public accountant, attorney, or enrolled agent to act on their behalf for specific tax issues. |

| Submission Requirements | Form 2848-ME must be signed by the taxpayer and submitted to the Maine Revenue Services for acceptance and processing. |

When preparing to fill out Form 2848, ensure you have all necessary information and understand which sections apply to your situation. Completing this form accurately is essential for designating a representative to handle your tax matters with the IRS. Follow the steps outlined below carefully.

After submission, the IRS will process your form, granting your representative the necessary authority to act on your behalf. Keep a copy of the completed form for your records. If you need to revoke authorization later, additional steps will be required.

What is the Tax POA form 2848-ME?

The Tax Power of Attorney (POA) form 2848-ME allows individuals to authorize another person, such as an attorney or accountant, to represent them before the tax authorities on specific matters. This form is crucial when seeking assistance with tax issues, audits, or filings.

Who needs to fill out the form 2848-ME?

Any taxpayer who wishes to grant authority to someone else to handle their tax matters should complete this form. This includes individuals who may be busy or unable to manage their taxes directly and need assistance from a trusted professional.

What information is required to complete the form?

The form will require personal identification details such as your name, address, taxpayer identification number, and the specific tax matters you are authorizing your representative to handle. Accurate information is essential to avoid any delays or issues in processing.

How do I submit the 2848-ME form?

You can submit the completed form to the appropriate tax authority by mail or electronically, depending on the requirements of your specific jurisdiction. Ensure that you check the guidelines for submission to ensure proper processing.

Does the form have an expiration date?

The authorization granted under the form 2848-ME remains in effect until you revoke it, the representative withdraws, or the matter is resolved. However, it is good practice to review and renew the authorization periodically.

Can I revoke the power of attorney once it is granted?

Yes, you can revoke the power of attorney anytime by submitting a written statement to the tax authority that originally received the 2848-ME form. Ensure that you also notify your representative of the revocation, so they cease acting on your behalf.

What if I need to appoint multiple representatives?

You can indeed appoint more than one representative using the 2848-ME form. Just provide their details in the respective sections of the form, ensuring that each representative’s qualifications are clearly stated.

How can I ensure my form is processed quickly?

To expedite processing, double-check that all required fields are completed accurately and that you provide any necessary supporting documentation. Submitting your form electronically, if permitted, may also help speed up the process.

Is there a fee associated with filing form 2848-ME?

No, there is no fee for submitting the form 2848-ME. However, fees may apply if you hire a professional to assist with your taxes, which is a separate consideration.

Where can I find more information or assistance regarding the 2848-ME form?

You can find additional information about the Tax POA form 2848-ME on the official tax authority website. For specific questions or concerns, contacting a tax professional is advisable to ensure all aspects of the form and its implications are understood thoroughly.

Filling out the Tax Power of Attorney (POA) Form 2848-ME can be a straightforward process, but mistakes are common. Avoid these seven pitfalls to ensure your form is completed correctly:

It’s crucial to provide accurate information about the representative. Ensure their name is spelled correctly and verify their designation.

Many people forget to sign or date the form, which can render it invalid. Always check for both before submission.

Be specific when listing the tax matters the representative is authorized to handle. Generalizations may lead to confusion about their authority.

Individuals often overlook indicating whether the representative is an attorney, CPA, enrolled agent, or another type of representative. This is essential information.

Make sure to include complete contact details for the representative. Missing phone numbers or addresses can delay processing.

If there are any additional documents required, such as proof of representation or identification, ensure these accompany the form.

Each form comes with specific instructions. Not following them can lead to unnecessary issues or rejection of the form.

Taking your time and carefully reviewing each section can help avoid these common errors. A properly completed form ensures your tax needs are addressed efficiently.

The Power of Attorney (POA) form 2848 serves as a crucial document for taxpayers who wish to authorize an individual to act on their behalf in matters related to federal tax. When dealing with tax-related issues, several other forms and documents often accompany the 2848 form. Understanding these additional documents can help taxpayers navigate their responsibilities and ensure compliance with tax regulations.

Each of these forms and documents plays a vital role in supporting tax management and compliance. Being aware of them ensures taxpayers can adequately prepare and respond to their tax obligations, facilitating a smoother process when engaging with the IRS.

The IRS Form 8821, Tax Information Authorization, serves a similar purpose to Form 2848, but with a key difference. While Form 2848 allows a designated individual to represent a taxpayer before the IRS, Form 8821 grants permission for a third party to receive tax information without the authority to act on behalf of the taxpayer. This form is helpful for those who want someone to assist them by providing guidance or information regarding their taxes, without the legal powers associated with full representation.

An additional document that resembles Form 2848 is the Durable Power of Attorney (DPOA). Unlike the tax-specific forms, a durable power of attorney can extend beyond financial matters and remains effective even if the principal becomes incapacitated. When a person appoints someone as their agent through a DPOA, they grant that agent the authority to make a variety of decisions, similar to what is permitted with Form 2848 in the context of tax-related issues. However, DPOAs do not limit their authority to taxation and can address broader legal and financial matters.

The Limited Power of Attorney (LPOA) also shares similarities with Form 2848. This document restricts the powers of the appointed individual, typically to very specific tasks. For example, a taxpayer can specify that an agent only has authority to represent them during a specific audit or tax period. This targeted approach allows for more control over what actions the designated individual can take, focusing on immediate needs or concerns, just as Form 2848 does within the bounds of tax representation.

Lastly, the Corporate Power of Attorney (CPA) includes elements similar to those found in Form 2848, but is tailored specifically for corporate entities. Companies use a corporate power of attorney to authorize individuals to receive tax information or take actions on behalf of the corporation. Just as Form 2848 allows individuals to represent taxpayers, a corporate power of attorney enables businesses to ensure that their interests are represented in tax matters effectively.

When completing the Tax Power of Attorney (POA) Form 2848, there are important steps to follow. Here is a list of what you should and shouldn't do during this process.

Understanding the Tax Power of Attorney (POA) form 2848-ME is crucial for anyone who needs tax assistance. However, several misconceptions can lead to confusion. Here are seven common misunderstandings about the form:

Clear understanding of these misconceptions can help ensure proper use of the Tax POA form 2848-ME and effective communication with tax representatives.

Understanding the Tax Power of Attorney (POA) form 2848-me is essential for anyone looking to appoint someone to handle their tax matters. Here are some key takeaways to help clarify its purpose and usage: