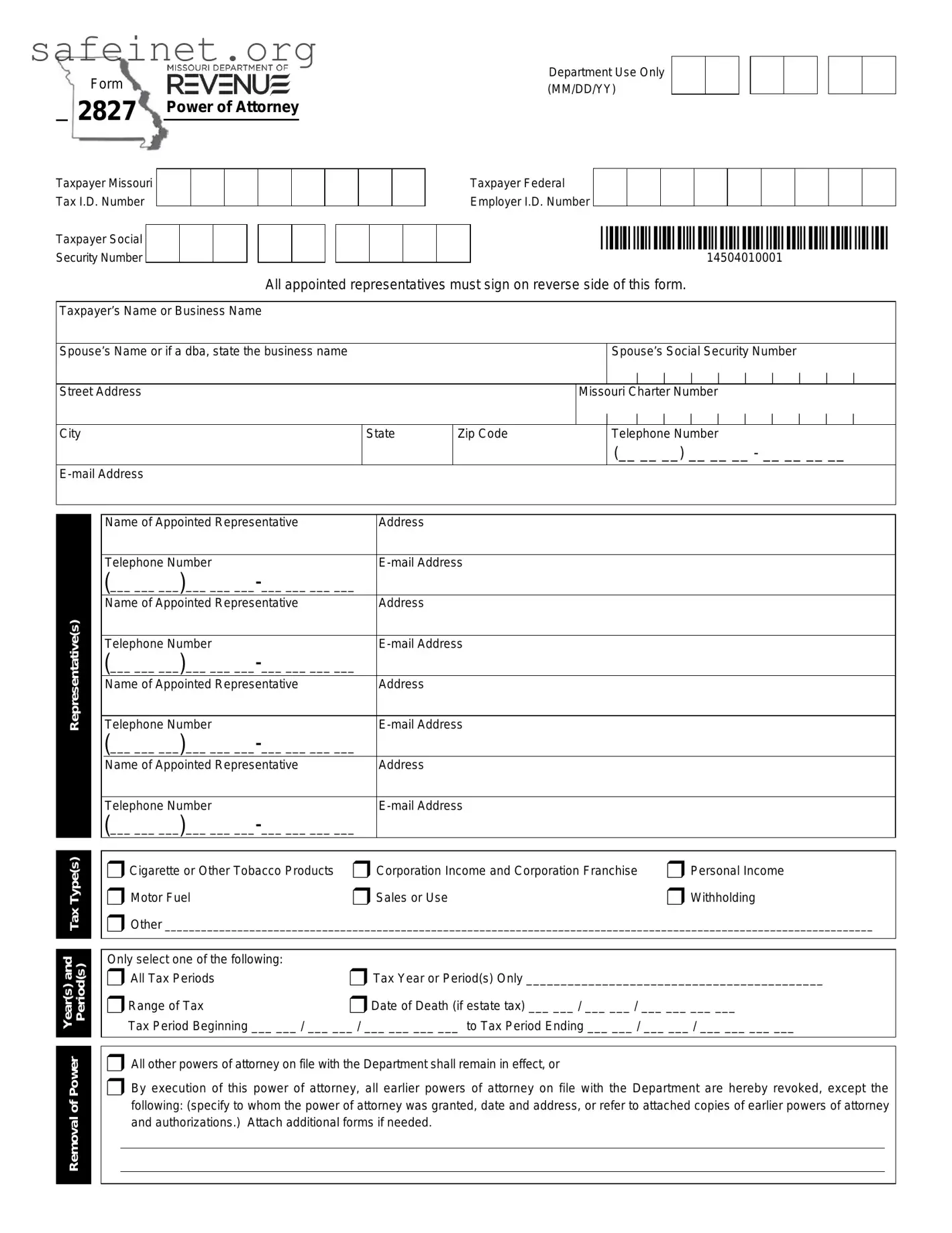

The Tax Power of Attorney (POA) Form 2827 is an important document that allows taxpayers to designate a representative to act on their behalf in tax matters. This form serves as a formal agreement between the taxpayer and their chosen representative, often providing the agent with the authority to review confidential information and communicate directly with the Internal Revenue Service (IRS). When properly executed, the form enables the designated individual to receive information about the taxpayer’s account and make necessary decisions during an audit or other tax investigations. The scope of authority granted can include filing returns, paying taxes, and negotiating tax matters. It is essential for individuals to understand the implications and requirements of Form 2827, as its completion involves specific details, including the taxpayer's identification information, the representative's credentials, and the limited period of representation, if applicable. Ensuring accurate and timely submission of this form can significantly impact how tax-related issues are handled and resolved.

Form |

|

R:V:NUS |

|

|

|

|

(MM/DD/YY) |

[IJ[IJ[IJ |

||

|

|

|

DEPARTMENT OF |

|

|

|

|

Department Use Only |

|

|

2827 |

|

|

|

|

|

|

|

|

||

|

Power of Attorney |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||

Taxpayer Missouri |

I |

I |

I |

I I I |

I |

I |

I |

Taxpayer Federal |

I I I I I I I |

|

Tax I.D. Number |

Employer I.D. Number I I I |

|||||||||

Taxpayer Social |

|

I |

I |

IITJ I |

I |

I |

I |

I |

*14504010001* |

|

Security Number I |

|

|

14504010001 |

|||||||

All appointed representatives must sign on reverse side of this form.

Taxpayer’s Name or Business Name

Spouse’s Name or if a dba, state the business name |

|

|

|

Spouse’s Social Security Number |

|

|

|

|

|

|

I |

| | | | | | |

| |

| |

| |

Street Address |

|

|

Missouri Charter Number |

|

|

|

|

|

|

|

I | |

| | | | | | |

| |

| |

| |

City |

State |

Zip Code |

|

Telephone Number |

|

|

|

|

I |

I |

I(__ __ __) __ __ __ - __ __ __ __ |

|

|||

|

|

|

|

|

|

|

|

Representative(s)

Year(s) and Removal of Power Period(s) Tax Type(s)

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

rCigarette or Other Tobacco Products r Corporation Income and Corporation Franchise r Personal Income

r Motor Fuel |

r Sales or Use |

r Withholding |

rOther _____________________________________________________________________________________________________________________

Only select one of the following: |

|

r All Tax Periods |

r Tax Year or Period(s) Only ___________________________________________ |

r Range of Tax |

r Date of Death (if estate tax) ___ ___ / ___ ___ / ___ ___ ___ ___ |

Tax Period Beginning ___ ___ / ___ ___ / ___ ___ ___ ___ to Tax Period Ending ___ ___ / ___ ___ / ___ ___ ___ ___

rAll other powers of attorney on file with the Department shall remain in effect, or

rBy execution of this power of attorney, all earlier powers of attorney on file with the Department are hereby revoked, except the following: (specify to whom the power of attorney was granted, date and address, or refer to attached copies of earlier powers of attorney and authorizations.) Attach additional forms if needed.

Signature

Under penalties of perjury, I (we) hereby certify that I (we) am (are) the taxpayer(s) named herein or that I have the authority to execute this power of attorney on behalf of the taxpayer(s).

Name

Signature |

Date (MM/DD/YYYY) |

Taxpayer Telephone Number |

|

__ __ / __ __ / __ __ __ __ |

I(___ ___ ___)___ ___ |

Name |

Title (if applicable) |

|

|

|

|

Signature |

Date (MM/DD/YYYY) |

Taxpayer Telephone Number |

|

__ __ / __ __ / __ __ __ __ |

I(___ ___ ___)___ ___ |

Declaration of Representative(s)

Please consult Missouri Regulation 12 CSR

I declare that I am aware of Regulation 12 CSR

1. |

a member in good standing of the bar; |

5. |

a fiduciary for the taxpayer; |

2. |

a certified public accountant duly qualified to practice; |

6. |

an enrolled agent; |

3. |

an officer of the taxpayer organization; |

7. |

tax preparer, or |

4. |

a |

8. |

other authorized representative or agent |

Note: All appointed representatives must sign below. No digital signatures allowed.

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|||||

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|||||

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

|

|

|

|

|

||||

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|||||

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

|

|

|

|

|

||||

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|

|

|

|

|

Mail to: |

|

|

Form 2827 (Revised |

|

|

|

|

(Business Tax) |

(Personal Tax) |

(Motor Fuel Tax) |

(Cigarette or Other Tobacco Products Tax) |

Taxation Division |

Taxation Division |

Taxation Division |

Taxation Division |

P.O. Box 357 |

P.O. Box 2200 |

P.O. Box 300 |

P.O. Box 811 |

Jefferson City, MO |

Jefferson City, MO |

Jefferson City, MO |

Jefferson City, MO |

Phone: (573) |

Phone: (573) |

Phone: (573) |

Phone: (573) |

Fax: (573) |

Fax: (573) |

Fax: (573) |

Fax: (573) |

If this is being submitted in response to an audit, please fax to (573)

Visit http://dor.mo.gov/ for additional information.

*14504020001*

14504020001

| Fact Name | Description |

|---|---|

| Purpose | The Tax Power of Attorney (POA) Form 2827 allows individuals to appoint an agent to represent them before the IRS. |

| Authority Granted | It grants the appointed agent the authority to perform various tasks, including signing tax returns and handling communications with the IRS. |

| Revocation | The form can be revoked at any time by the taxpayer by notifying the IRS in writing. |

| Who Can Be an Agent | Individuals, corporations, or other legal entities can be chosen as agents on the form. |

| Signature Requirement | The taxpayer must sign the form for it to be valid. This includes providing the date of the signature. |

| Submission Process | The completed form can be submitted to the IRS by mail or fax depending on the specific circumstances. |

| Validity Duration | This form remains in effect until it is revoked or until the taxpayer dies. |

| State-Specific Laws | Some states may have their own POA forms governed by state law, which can affect how taxes are handled. |

Once you have the Tax POA form 2827 in hand, it’s vital to ensure it is filled out correctly to allow your designated representative to act on your behalf concerning tax matters. Follow the steps below to complete the form accurately.

What is the Tax Power of Attorney (POA) Form 2827?

The Tax Power of Attorney Form 2827 is a document that allows individuals to appoint an authorized representative to act on their behalf concerning tax matters. This form is particularly useful when a taxpayer needs assistance from a tax professional or wants someone else to handle their tax-related issues. By completing this form, taxpayers can enable their chosen representative to receive confidential tax information, correspond with the IRS, and represent them during audits or other proceedings.

Who can use Form 2827?

Any individual or business entity that needs assistance with their tax matters may use Form 2827. This includes sole proprietors, partnerships, corporations, and even estates. Taxpayers must ensure that the appointed representative is a qualified person, such as a certified public accountant (CPA), enrolled agent, or tax attorney, who is knowledgeable about tax laws and procedures.

How do I fill out Form 2827?

Filling out Form 2827 requires basic information about both the taxpayer and the representative. The taxpayer should provide their name, address, Social Security number or Employer Identification Number (EIN), and the representative's details, including their name, firm name (if applicable), and address. Additionally, taxpayers need to specify the tax matters they are granting authority over, which may include income tax, payroll tax, or sales tax. Once the form is completed, the taxpayer must sign and date it to validate their consent.

How long is the authority granted by Form 2827 valid?

The authority granted through Form 2827 does not have a specific expiration date, but it remains in effect until the taxpayer revokes it or the representative is no longer eligible to act on behalf of the taxpayer. Taxpayers have the right to revoke the POA at any time by submitting a written notice to the IRS. In such cases, it is advisable to also notify the appointed representative of the termination.

Where should I submit Form 2827?

Form 2827 should be submitted to the IRS office that handles the taxpayer's specific case or tax matters. It's important to check the IRS website or contacting the IRS directly for the appropriate mailing address, as it can vary based on the type of tax involved, the taxpayer's location, and whether they are submitting additional forms or payments. A copy of the submitted form should be kept for personal records.

Incorrect Selection of Taxpayer: Individuals often select the wrong taxpayer when completing the form. It is crucial to ensure that the taxpayer's name, Social Security number, and other identifying information are entered accurately to avoid delays in processing.

Failure to Sign the Form: Many overlook the necessity of signing the form. Without a signature, the form is incomplete, and the designated representative will not be authorized to act on behalf of the taxpayer.

Not Specifying the Authority Being Granted: The form requires the taxpayer to clearly indicate the scope of authority being granted to the representative. Failing to define the limits can lead to misunderstandings about what actions the representative is permitted to take.

Ignoring Filing Deadlines: Timeliness is crucial when submitting the Tax POA form 2827. Delays could hinder a representative’s ability to act during essential periods, particularly around tax deadlines.

Providing Incomplete Contact Information: Incomplete or inaccurate contact details for both the taxpayer and the representative can result in communication difficulties. It is important to provide clear and current information to facilitate any necessary discussions.

The Tax Power of Attorney (POA) Form 2848 is a crucial document that allows individuals to appoint someone to act on their behalf before the Internal Revenue Service (IRS). When filing this form, several other forms and documents are often needed to ensure comprehensive representation and compliance with tax laws. Below are some of these commonly used forms and documents, each serving a specific purpose in the tax representation process.

Understanding the various forms and documents that accompany the Tax POA Form 2848 is essential for taxpayers seeking effective representation. Each document serves its own function and together, they facilitate smoother communication and compliance with tax obligations, ultimately benefiting the taxpayer and their appointed representative.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is quite similar to Form 2827. Both forms allow individuals to appoint someone to represent them before the IRS. They enable the designated representative to receive and respond to IRS communications on behalf of the taxpayer. The key difference is that Form 2848 can be used not only for tax matters but also for other IRS-related issues, making it broader in scope compared to Form 2827.

Form 4506, Request for Copy of Tax Return, shares similarities with the Tax POA Form 2827 in that both involve the taxpayer's consent and provide authorization for access to specific tax information. However, while Form 2827 gives authority to a representative to act on behalf of a taxpayer, Form 4506 specifically allows individuals to obtain copies of previously filed tax returns, thus serving a different purpose in the tax process.

Form 8821, Tax Information Authorization, is another document that is closely associated with Form 2827. Like Form 2827, it allows a third party to access a taxpayer's confidential tax information. The main distinction lies in the fact that Form 8821 does not grant the representative the right to represent the taxpayer in dealings with the IRS; rather, it only authorizes them to receive information, limiting their authority compared to Form 2827.

The Durable Power of Attorney is often compared to the Tax POA Form 2827. While both documents allow a designated individual to act on behalf of another, the Durable Power of Attorney covers a broader range of legal and financial matters, extending beyond just tax issues. Additionally, a Durable Power of Attorney remains effective even if the principal (the person granting authority) becomes incapacitated, unlike the specific focus and temporary nature of Form 2827.

The Medical Power of Attorney bears some resemblance to Form 2827 in that both allow individuals to appoint someone to make decisions on their behalf. However, the Medical Power of Attorney pertains specifically to health care decisions, while Form 2827 is limited to tax-related matters. This document is crucial during situations where individuals are unable to express their medical wishes, showcasing a significant difference in context and application.

Form W-7, Application for IRS Individual Taxpayer Identification Number, is related to Form 2827 in that both must be used to facilitate interactions with the IRS. While not a power of attorney in itself, Form W-7 allows non-resident aliens and others who do not qualify for a Social Security number to obtain an ITIN for tax purposes. The purpose of both forms is to ensure appropriate representation and compliance with IRS regulations.

The Limited Power of Attorney is another document that can be likened to the Tax POA Form 2827. Just as the Tax POA form allows for representation in specific tax matters, a Limited Power of Attorney grants a designated individual authority to act in certain, defined situations. The scope of the authority can vary, but like Form 2827, it confines the representative's powers to specified actions rather than granting broader authority.

Finally, the General Power of Attorney is broadly similar to Form 2827, as both permit someone to act on behalf of another. However, the General Power of Attorney is extensive and covers a wide range of financial and legal matters, not just taxes. This type of document usually comes into play for more comprehensive, everyday decisions, contrasting with the focused intent of Form 2827 in dealing specifically with tax matters.

When filling out the Tax POA Form 2827, it's essential to approach it with care. Here are some important dos and don'ts to keep in mind:

Understanding the Tax Power of Attorney (POA) Form 2827 is crucial for effectively managing tax matters. Below are some common misconceptions about this form:

When filling out and utilizing the Tax Power of Attorney (POA) Form 2827, there are several important considerations to keep in mind. Below are key takeaways to ensure a smooth process.

Taking careful steps when completing the Tax POA Form 2827 will facilitate effective communication and representation with the IRS. Your diligence can help prevent misunderstandings and ensure that your tax needs are met efficiently.