Understanding how to navigate tax matters can be overwhelming, especially when it comes to granting authority to another person to act on your behalf. The Tax Power of Attorney (POA) form 21-002-13 provides an essential framework for individuals who wish to designate an authorized representative for tax-related purposes. This form allows taxpayers to appoint a trusted individual, such as a family member, accountant, or tax professional, to handle their tax affairs, ensuring that timely and correct filings are made. It is vital to ensure that all necessary details are correctly filled out, including the taxpayer's information and the scope of authority granted. Additionally, the form specifies any limitations on the representative’s powers, providing clarity on what actions they can take. Properly completing this form can help alleviate the burden of tax compliance, giving taxpayers the reassurance that their interests are being actively managed while they focus on other priorities. Understanding the nuances of the Tax POA form will empower taxpayers to make informed decisions about their representation in tax matters.

- DEPARTMENT OF - |

POWER OF ATTORNEY |

|

REV EN UE |

AND |

STATE OF M I SS I SSIPPI |

DECLARATION OF REPRESENTATION |

Form

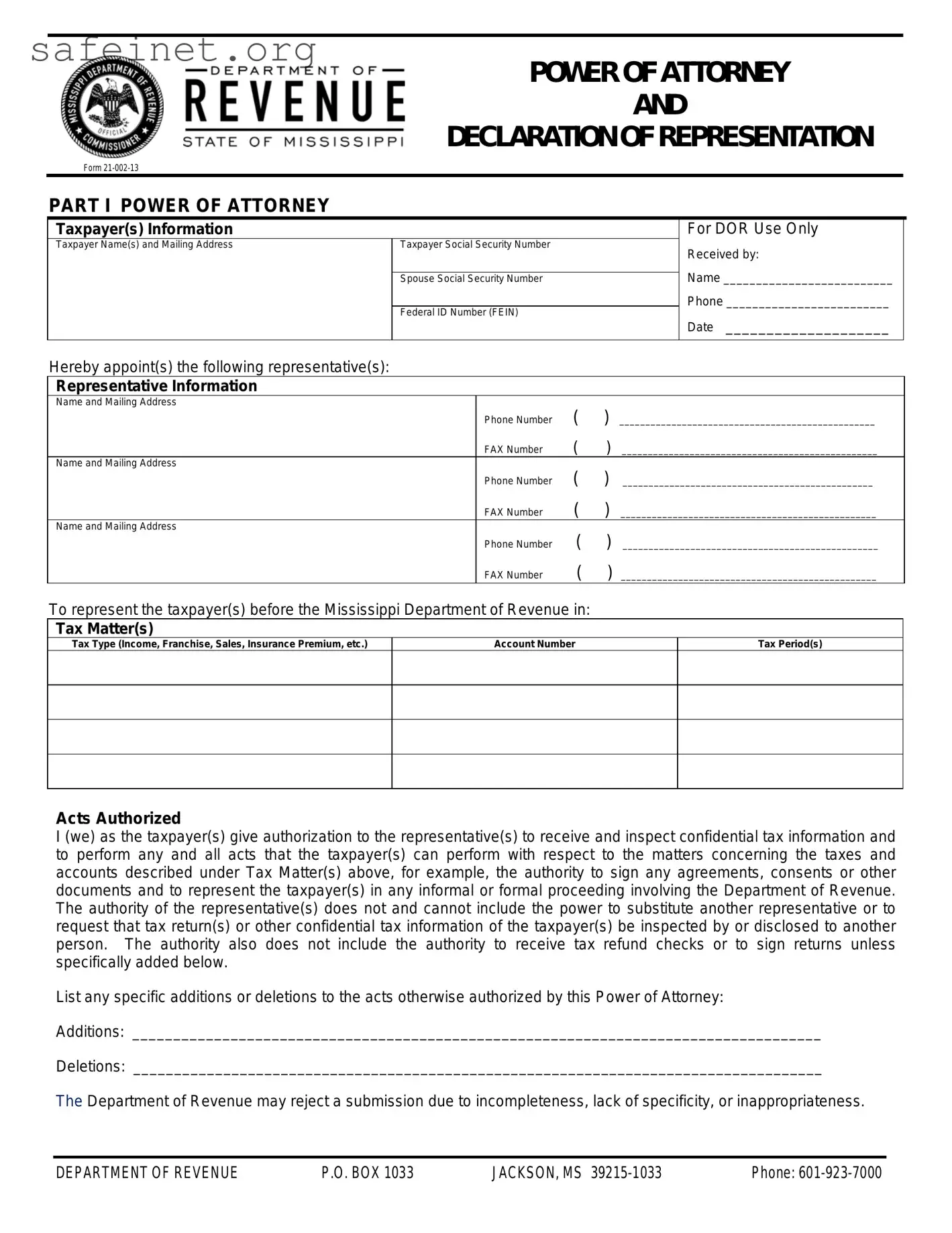

PART I POWER OF ATTORNEY

Taxpayer(s) Information

Taxpayer Name(s) and Mailing Address |

Taxpayer Social Security Number |

|

Spouse Social Security Number |

|

Federal ID Number (FEIN) |

For DOR Use Only

Received by:

Name __________________________

Phone _________________________

Date ____________________

Hereby appoint(s) the following representative(s):

Representative Information

Name and Mailing Address

Phone Number |

( |

) |

_________________________________________________ |

FAX Number |

( |

) |

_________________________________________________ |

Name and Mailing Address |

( |

) |

|

Phone Number |

________________________________________________ |

||

FAX Number |

( |

) |

_________________________________________________ |

Name and Mailing Address |

( |

) |

|

Phone Number |

_________________________________________________ |

||

FAX Number |

( |

) |

_________________________________________________ |

To represent the taxpayer(s) before the Mississippi Department of Revenue in:

Tax Matter(s)

Tax Type (Income, Franchise, Sales, Insurance Premium, etc.)

Account Number

Tax Period(s)

Acts Authorized

I (we) as the taxpayer(s) give authorization to the representative(s) to receive and inspect confidential tax information and to perform any and all acts that the taxpayer(s) can perform with respect to the matters concerning the taxes and accounts described under Tax Matter(s) above, for example, the authority to sign any agreements, consents or other documents and to represent the taxpayer(s) in any informal or formal proceeding involving the Department of Revenue. The authority of the representative(s) does not and cannot include the power to substitute another representative or to request that tax return(s) or other confidential tax information of the taxpayer(s) be inspected by or disclosed to another person. The authority also does not include the authority to receive tax refund checks or to sign returns unless specifically added below.

List any specific additions or deletions to the acts otherwise authorized by this Power of Attorney:

Additions: ____________________________________________________________________________________

Deletions: ____________________________________________________________________________________

The Department of Revenue may reject a submission due to incompleteness, lack of specificity, or inappropriateness.

DEPARTMENT OF REVENUE |

P.O. BOX 1033 |

JACKSON, MS |

Phone: |

DOR Power of Attorney, Form

Retention/Revocation of Prior Power(s) of Attorney

The filing of this Power of Attorney automatically revokes all earlier Power(s) of Attorney on file with the Department of Revenue for the same tax matter(s) covered by this document. If you do not want to revoke a prior Power or Attorney,

check here D

and ATTACH A COPY OF THE POWER(S) OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

and ATTACH A COPY OF THE POWER(S) OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

Who Must Sign and What Documentation of Authority Must Be Attached

If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested. A corporation or subsidiary MUST contain the signatures of a principal officer and the secretary or other officer. A guardian, executor, receiver, administrator, conservator or trustee MUST attach the appropriate documentation granting the authority from the court or taxpayer.

Signing is Certification Under Oath Subject to Penalty of Perjury

The person(s) signing this Power of Attorney and Declaration of Representations certifies under oath that all the information contained in this document is true and correct and that he, she or they have the authority to sign this document as the taxpayer(s) or on behalf of the taxpayer(s) and acknowledge that this Power of Attorney and Declaration of Representation is being signed under the penalty of perjury pursuant to Miss. Code Ann. §

IF NOT SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED.

Signature |

Date |

Title (if applicable) |

Print Name |

Phone Number |

FAX Number |

Signature |

Date |

Title (if applicable) |

Print Name |

Phone Number |

FAX Number |

PART II DECLARATION OF REPRESENTATIVE

Under penalties of perjury and Miss. Code Ann.

1)I am authorized to represent the taxpayer(s) identified in Part I for the tax matter(s) specified there: and

2)I am one of the following:

a.Attorney – a member in good standing of the bar of the highest court of the jurisdiction shown below.

b.Certified Public Accountant – duly authorized to practice as a certified public accountant in the jurisdiction shown.

c.Officer – a bona fide officer of the taxpayer’s organization.

d.

e.Family Member – a member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

f.Enrolled Agent – enrolled as an agent under the requirements of the IRS.

g.Other – Provide explanation ________________________________________________________________

IF NOT SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED.

Designation – Insert |

State Issuing |

State License |

Above letter |

License |

Number |

|

|

|

Signature

Date

DEPARTMENT OF REVENUE |

P.O. BOX 1033 |

JACKSON, MS |

Phone: |

| Fact Name | Details |

|---|---|

| Form Title | Tax Power of Attorney (POA) Form 21-002-13 |

| Purpose | This form allows an individual to authorize another person to act on their behalf regarding tax matters. |

| Who Can Use It | Any taxpayer needing assistance with tax-related issues can use this form to appoint a representative. |

| Governing Law | This form is governed by federal tax laws and regulations in the United States. |

| Signature Requirement | The taxpayer’s signature is required to validate the form. |

| Filing Location | The completed form should be submitted to the relevant tax authority or agency. |

| Effective Date | The authority granted is effective as soon as the form is filed with the tax agency. |

| Duration of Authority | The authority granted remains in effect until revoked or until the taxpayer’s death. |

| Supported Tax Matters | It covers a wide range of tax matters, including filing returns and resolving issues. |

| Revocation Process | To revoke the POA, a separate revocation form may be submitted to the tax authority. |

After obtaining the Tax POA form 21-002-13, you will need to fill it out completely and accurately. Ensure that you have all necessary information at hand before you begin. This will streamline the process and help avoid errors that could delay your submission.

What is the Tax POA form 21-002-13?

The Tax POA form 21-002-13, or Power of Attorney, is a document used to grant someone the authority to act on your behalf concerning tax matters. This form is particularly relevant for those who may want to delegate their responsibilities regarding tax filings or communications with the Internal Revenue Service (IRS) to another individual, such as a tax professional or family member.

Who can be appointed using the Tax POA form 21-002-13?

Any individual can be appointed as your representative using this form, provided they are capable of acting in that role. Common appointments include certified public accountants, enrolled agents, or trusted family members. It’s important to choose someone you trust, as they will have the authority to discuss and resolve your tax issues with the IRS.

What powers does the Tax POA form 21-002-13 grant?

This form allows your appointed representative to access your tax information, communicate with the IRS, and make decisions regarding your tax matters. However, the specific powers can vary based on how you fill out the form. You can limit these powers or grant full authority, depending on your preference.

How do I complete the Tax POA form 21-002-13?

Completing the form involves providing your personal information, detailing the authority you wish to grant, and signing the document. Make sure to include your representative's name and contact information. After filling it out, both you and your representative must sign the form to make it legally binding.

Do I need to submit this form to the IRS?

Yes, once completed and signed, the Tax POA form 21-002-13 must be submitted to the IRS to activate the powers granted to your representative. You can send it directly to the IRS or instruct your representative to do so on your behalf. The IRS requires it to process any inquiries or filings made by your appointed individual.

Can I revoke the Tax POA form 21-002-13 at any time?

You maintain the right to revoke the Tax POA form 21-002-13 whenever you choose. To do this, you must provide written notice to both the IRS and your representative. This ensures that your former representative no longer has the authority to act on your behalf. It is a straightforward process, ensuring you retain control over your tax matters.

Filling out the Tax POA (Power of Attorney) form 21-002-13 can seem straightforward, but there are common mistakes that can lead to delays or issues. Here’s a list of four frequent errors:

Incorrect Personal Information: People often make mistakes in entering their names, addresses, or Social Security numbers. This information must match what the IRS has on file, as any discrepancies can cause problems.

Not Specifying the Scope: Leaving the scope of authority blank is another common oversight. Make sure to clearly outline what powers you are granting to your representative. Use specific terms to avoid ambiguity.

Failing to Sign and Date: It may seem basic, but forgetting to sign or date the form is a frequent mistake. Your signature is essential for the document to be valid, and missing it can invalidate the entire form.

Not Keeping Copies: Some individuals forget to keep a copy of the completed form for their records. It’s important to have a copy with your signature for future reference and to confirm what authority was granted.

Avoiding these common errors can help ensure that your Tax POA form is processed smoothly. Taking the time to double-check your information can save you from potential headaches down the line.

When completing the Tax Power of Attorney (POA) form 21-002-13, several additional documents may be useful to ensure thorough processing. Below is a brief overview of four commonly used forms that often accompany the Tax POA form.

These forms, alongside the Tax POA form 21-002-13, provide a comprehensive way to manage your tax representation needs. Ensuring that you have the correct documents prepared will help facilitate the process and reduce any potential delays.

The Tax Power of Attorney (POA) Form 21-002-13 is quite similar to the IRS Form 2848, which is also a Power of Attorney form used by taxpayers. Both forms grant someone the authority to represent a taxpayer before the respective tax authority—in this case, the IRS. The IRS Form 2848 designates a person to handle tax matters, including the ability to receive confidential information and make decisions on behalf of the taxpayer. This similarity ensures that the appointed representative has the legal ability to communicate with tax officials effectively on behalf of the taxpayer.

Another document closely related to the Tax POA form is the State Tax Power of Attorney, which is used at the state level. Just as with the IRS form, a state tax POA permits a designated individual to represent the taxpayer regarding state income taxes and other state tax-related issues. Each state may have its own specific form and requirements, but the underlying principle is the same: to grant authority to someone trusted to manage tax responsibilities and advocate for the taxpayer’s interests.

A third document that shares similarities with the Tax POA is the Medical Power of Attorney. While focused on health care decisions rather than tax issues, both documents provide a means for individuals to appoint someone to act on their behalf. The Medical Power of Attorney allows the designated person to make medical decisions in the event that the individual cannot do so. Both documents highlight the importance of having a trusted representative in critical areas of personal and financial life.

Finally, the Durable Power of Attorney is another document comparable to the Tax POA form. This legal document allows a person to empower someone else to handle a wide range of legal and financial matters, which may extend beyond just taxes. The durable aspect means that the appointed individual can act even if the principal becomes incapacitated. Similar to the Tax POA form, the Durable Power of Attorney ensures that someone the individual trusts can manage important issues when they are unable to do so themselves.

When filling out the Tax POA form 21-002-13, attention to detail is crucial. Here are some guidelines to help you navigate the process successfully.

By adhering to these dos and don’ts, you can simplify the process and minimize any potential problems that may arise with your Tax POA form.

When it comes to the Tax Power of Attorney (POA) form 21-002-13, several misconceptions may arise. Understanding the realities surrounding this form can help taxpayers make informed decisions.

This form can be used for various tax matters, including property taxes and estate taxes, not just income tax.

Taxpayers have the right to revoke the POA at any time by submitting a written notice to the tax authority.

While legal assistance can be helpful, individuals can fill out the form on their own without requiring a lawyer.

A representative can also discuss matters with the IRS, receive tax information, and negotiate settlements on behalf of the taxpayer.

Even for minor tax matters, having a POA can simplify communication and representation with the tax authority.

In reality, the form is straightforward and can typically be processed quickly by tax authorities.

The POA remains valid for any and all tax years unless specified otherwise in the form itself.

A designated representative can sign if they have the proper authority and consent from the taxpayer.

When filling out and using the Tax Power of Attorney (POA) form 21-002-13, there are several important considerations to keep in mind. Here are four key takeaways that can help ensure the process goes smoothly.

Taking these steps can make the process of granting a tax Power of Attorney easier and more effective. Always keep a copy of your submitted forms for your records.