The Tax POA Form 20A100 serves as an essential tool for individuals seeking to grant power of attorney to another party in matters concerning tax issues. This form is primarily utilized to authorize an individual, often called an “attorney-in-fact,” to act on behalf of the taxpayer when dealing with the Internal Revenue Service (IRS) or state tax authorities. By completing this form, the taxpayer permits the designated agent to access tax information, communicate with tax officials, and make decisions regarding tax filings. Key aspects of the 20A100 include the specification of the powers granted, necessary identification details, and the signature of the taxpayer that validates the authority being conferred. Furthermore, the form accommodates various tax situations, ensuring it meets the diverse needs of taxpayers who may require assistance in navigating complex regulations. Understanding how to properly fill out this form and the implications of granting such authority can streamline the tax process, provide peace of mind, and prevent potential complications in the future.

20A100

DECLARATION OF REPRESENTATIVE

Commonwealth of Kentucky

Department of Revenue

1 TAXPAYER INFORMATION: Please type or print. |

|

Enter only those that apply. |

||||

|

|

|

|

|

|

|

Taxpayer Name |

|

|

|

Federal Taxpayer Identifcation Number |

||

|

|

|

|

|

||

Mailing Address - Number and Street |

|

Apartment/Suite No. |

||||

|

|

|

|

|

|

|

City |

State |

Zip Code |

IDaytime Phone |

|

|

|

2 |

REPRESENTATIVE(S) INFORMATION |

|

|

Enter applicable identifcation number. |

||

|

|

|

|

|

|

|

Name |

|

|

|

State and State Bar Number |

||

|

|

|

|

|

|

I |

Mailing Address - Number and Street |

|

Apartment/Suite No. |

State and CPA License Number |

|||

|

|

|

|

|

|

I |

City |

State |

Zip Code |

I |

Daytime Phone |

I |

|

|

IRS Enrolled Agent Number |

|||||

|

|

|

|

|

|

|

Name |

|

|

|

State and State Bar Number |

||

|

|

|

|

|

|

I |

Mailing Address - Number and Street |

|

Apartment/Suite No. |

State and CPA License Number |

|||

|

|

|

|

|

|

I |

City |

State |

Zip Code |

I |

Daytime Phone |

I |

|

|

IRS Enrolled Agent Number |

|||||

|

|

|

|

|

|

|

Name |

|

|

|

State and State Bar Number |

||

|

|

|

|

|

|

I |

Mailing Address - Number and Street |

|

Apartment/Suite No. |

State and CPA License Number |

|||

|

|

|

|

|

|

I |

City |

State |

Zip Code |

I |

Daytime Phone |

I |

|

|

IRS Enrolled Agent Number |

|||||

|

|

|

|

|

|

|

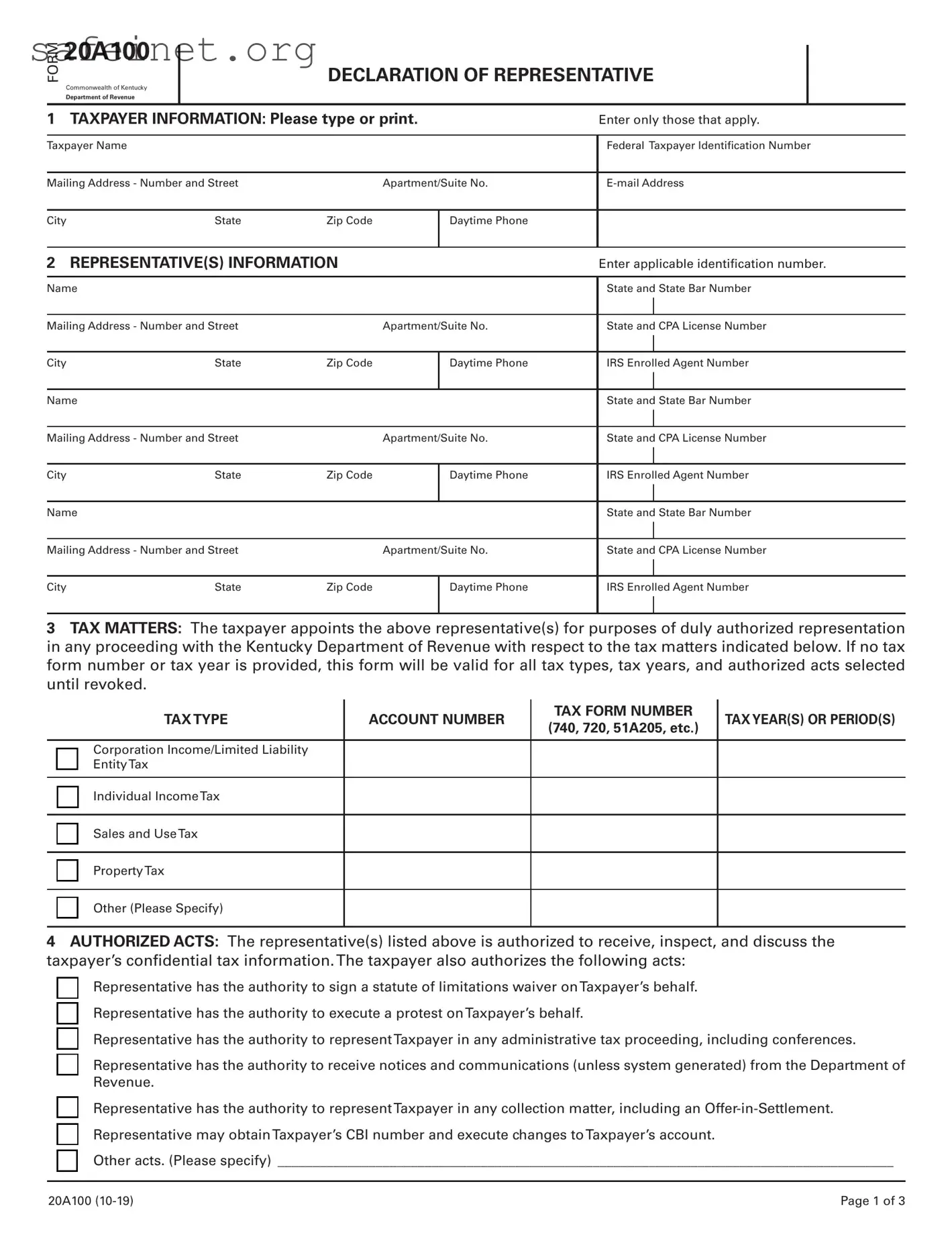

3TAX MATTERS: The taxpayer appoints the above representative(s) for purposes of duly authorized representation in any proceeding with the Kentucky Department of Revenue with respect to the tax matters indicated below. If no tax form number or tax year is provided, this form will be valid for all tax types, tax years, and authorized acts selected until revoked.

TAX TYPE |

ACCOUNT NUMBER |

TAX FORM NUMBER |

TAX YEAR(S) OR PERIOD(S) |

|

(740, 720, 51A205, etc.) |

||||

|

|

|

Corporation Income/Limited Liability

¨EntityTax

¨Individual IncomeTax

¨Sales and UseTax

¨PropertyTax

¨Other (Please Specify)

4AUTHORIZED ACTS: The representative(s) listed above is authorized to receive, inspect, and discuss the taxpayer’s confdential tax information.The taxpayer also authorizes the following acts:

¨Representative has the authority to sign a statute of limitations waiver onTaxpayer’s behalf.

¨Representative has the authority to execute a protest onTaxpayer’s behalf.

¨Representative has the authority to representTaxpayer in any administrative tax proceeding, including conferences.

¨Representative has the authority to receive notices and communications (unless system generated) from the Department of Revenue.

¨Representative has the authority to representTaxpayer in any collection matter, including an

¨Representative may obtainTaxpayer’s CBI number and execute changes toTaxpayer’s account.

¨Other acts. (Please specify) ________________________________________________________________________________________

20A100 |

Page 1 of 3 |

FORM 20A100

DECLARATION OF REPRESENTATIVE

Page 2 of 3

5CONSOLIDATED OR UNITARY COMBINED RETURN FILERS: If the taxpayer fles a consolidated or unitary combined tax return per KRS 141.200(11) and/or KRS 141.201(3)(a), the authorized acts will be extended to the subsidiaries included in the return. If any subsidiaries are to be excluded from the authorized acts, list below.

NAME

FEDERAL IDENTIFICATION

NUMBER

TAX YEARS

6 RETENTION/REVOCATION OF PRIOR POWER(S) OF ATTORNEY OR REPRESENTATIVE AUTHORIZATION(S)

The fling of this authorization form automatically revokes any prior power(s) of attorney or representative authorization(s) on fle with the Department of Revenue for the same matter(s) and year(s) or period(s) covered by this document. If you do not want to revoke any prior power(s) of attorney or representative authorization(s), you must attach a copy of any power(s) of attorney or

representative authorization(s) you wish to remain in effect for the same matter(s) and year(s) or period(s) covered.

7SIGNATURE OFTAXPAYER. If a tax matter concerns a year in which a joint return was fled, each spouse must fle a separate representative authorization even if they are appointing the same representative(s). If signed by a corporate offcer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the legal authority to execute this form on behalf of the taxpayer.

NOT VALID UNLESS COMPLETED, SIGNED, AND DATED BY THE TAXPAYER.

Signature |

Date Signed |

|

|

|

|

Print Name |

Title (if applicable) |

|

8 SIGNATURE OF REPRESENTATIVE(S)

Under penalties of perjury, by my signature below I declare that:

•I am not currently suspended or disbarred from practice, or ineligible for practice;

•I am subject to regulations contained in Circular 230 (31 CFR, Subtitle A, Part 10) as amended, governing practice before the Internal Revenue Service;

•I am authorized to represent the taxpayer for the matter(s) specifed; and

NOT VALID UNLESS COMPLETED, SIGNED, AND DATED BY THE REPRESENTATIVE(S).

Signature |

Date Signed |

|

|

|

|

Printed Name |

PTIN (if applicable) |

|

|

|

|

Signature |

Date Signed |

|

|

|

|

Printed Name |

PTIN (if applicable) |

|

|

|

|

Signature |

Date Signed |

|

Printed Name |

PTIN (if applicable) |

FORM 20A100

Instructions for Form 20A100

Page 3 of 3

Purpose of Form 20A100

Use the Declaration of Representative (Form 20A100) to authorize the individual(s) to represent you before the Kentucky Department of Revenue. You may grant the individual(s) authorization to act on your behalf with regard to any tax administered by the Kentucky Department of Revenue. Form 20A100 is provided for the taxpayer’s convenience. One form may be submitted to designate all tax types the Department is authorized to communicate with the authorized representative(s). You may revoke this form at any time.

1Taxpayer

Name and

Daytime

Federal Taxpayer Identifcation

2Representative Information

Enter up to three individuals authorized to represent you and act on your behalf before the Department about the tax matters and authorized acts specifed on this form. Provide the name, address, and telephone number of the authorized representative(s). If the authorized representative is an attorney, certifed public accountant (CPA), or enrolled agent, provide the appropriate identifcation number.

3Tax Matters

Select the tax types the authorized representative(s) may act on your behalf with the Department. Provide the account number for all tax types selected. If authorization is being granted for specifc forms and tax periods, list the tax forms and tax periods. If tax forms and tax periods are left blank, this form will be valid for all tax types, tax periods, and authorized acts selected until revoked.

4Authorized Acts

This form allows the authorized representative(s) to communicate and receive confdential tax information. You may also select other acts the authorized representative(s) may perform on your behalf. If an act is not listed, select “Other” and specify.

Note: This form does not allow the authorized representative to sign tax returns or settlement agreements on your behalf.

5Consolidated or Unitary Combined Return Filers

If a consolidated or unitary combined tax return has been fled, list any subsidiary(ies) to be excluded from this authorization. The Department will not discuss or provide confdential tax information to the authorized representative(s) for any subsidiary listed. If no subsidiaries are listed, this form will extend to all corporations in a consolidated or unitary combined tax return.

6Retention/Revocation

Filing this form will automatically revoke any prior power of attorney or authorization letter submitted to the Department for the tax matters included on this form. If you do not want to revoke a prior power of attorney or authorization letter, a copy MUST be attached to this form to remain in effect.

7Signature of Taxpayer

This form must be signed and dated by the taxpayer to be valid. If the taxpayer is a business entity, it must be signed by an individual with the authority to delegate a representative on behalf of the taxpayer. If not signed and dated, the Department will not communicate with or provide confdential tax information to the authorized representative(s) included on this form.

8Signature of the Authorized Representative(s)

This form must be signed and dated by the authorized representative(s) to be valid. If not signed and dated, the Department will not communicate with or provide confdential tax information to the authorized representative(s) included on this form.

Mail this form to the following address:

Kentucky Department of Revenue

P. O. Box 181, Station 56

Frankfort, Kentucky

| Fact Name | Description |

|---|---|

| What is Tax POA? | The Tax POA form 20a100 is used to appoint a representative for tax matters before the state’s tax authority. |

| Governing Law | This form is governed by state tax laws, including the Uniform Administrative Procedures Act. |

| Who Can Use It? | Any individual or entity needing representation in tax matters can use this form to designate a power of attorney. |

| Eligible Representatives | Representatives can be attorneys, accountants, or other qualified individuals authorized to handle tax affairs. |

| Important Deadline | Filing the Tax POA form 20a100 should be done as soon as possible; failing to do so can delay your representation. |

| Signature Requirement | A signature from the taxpayer is required on the form and may need to be notarized depending on state regulations. |

| Revocation of POA | The taxpayer can revoke the power of attorney at any time by filling out a specific revocation form. |

| Common Mistakes | Incomplete forms or missing signatures are common errors that can lead to processing delays. |

| Where to Submit | The completed Tax POA form must be submitted to the appropriate state tax agency, often via mail or online portal. |

Completing the Tax POA form 20a100 requires careful attention to detail. After you have filled out the form correctly, you will submit it to the appropriate tax authority to grant someone the authority to act on your behalf regarding tax matters.

Once the form is submitted, allow some time for processing. You'll want to ensure that the appointed representative can handle your tax matters effectively while you monitor their actions as needed.

What is the Tax POA form 20a100?

The Tax POA form 20a100, also known as the Power of Attorney (POA) for Tax Matters, is a document that allows individuals to appoint an official representative to handle their tax affairs. This form is particularly useful for taxpayers who may need assistance with tax issues, such as filing returns, receiving tax information, or communicating with tax agencies on their behalf. By filling out this form, taxpayers provide their designated representative the authority to act in their stead regarding specific tax matters.

Who can I appoint as my representative using the 20a100 form?

You have the flexibility to appoint various individuals as your representative using the Tax POA form 20a100. This can include a family member, a friend, or a qualified tax professional, such as an accountant or tax attorney. It's crucial to choose someone who you trust and who understands your tax situation, as they will have access to sensitive information and the authority to act on your behalf.

What are the specific powers granted to my representative?

The representative you appoint using the 20a100 form can perform several important tasks related to your tax matters. These tasks may include preparing and filing returns, receiving information from tax authorities, and discussing your tax situation with tax officials. However, it's important to note that the exact powers granted can vary based on the options you select on the form. Therefore, it's vital to understand which powers you wish to confer to your representative before submitting the form.

Do I need to file the 20a100 form annually?

No, the Tax POA form 20a100 does not need to be filed annually. Once you appoint a representative using this form, the power remains in effect until you revoke it or until the circumstances change. It’s important, however, to keep your representative and tax authorities updated if any changes occur in your situation or if you wish to designate a different representative.

What happens if I change my mind about my representative?

If you decide to revoke or change your representative, you can do so by submitting a new 20a100 form with the updated information. Make sure to inform your former representative of the change, as they may still have access to your tax information if the prior form isn’t formally revoked. Clarity and communication are key to ensuring that your tax matters are handled as you prefer.

Where can I obtain the Tax POA form 20a100?

The Tax POA form 20a100 can usually be obtained from the official website of your state’s Department of Revenue or equivalent tax authority. Most tax agencies provide downloadable and printable versions of the form. If you prefer not to access it online, you can often request a hard copy by contacting your local tax office directly.

Incomplete Personal Information: Many individuals neglect to fill in all required personal details, such as their full name, address, and Social Security number (SSN).

Not Identifying the Authorized Representative: Sometimes, people fail to correctly identify the individual or organization they are granting power of attorney to, which can result in delays.

Forgetting to Sign: A common oversight is not signing the form. Without a signature, the form is invalid and cannot be processed.

Missing Dates: Failing to include the date when signing the form can lead to confusion regarding when the authorization takes effect.

Inadequate Scope of Authority: Some filers do not specify the exact powers they want to grant, which could cause limitations in what the representative can do on their behalf.

Providing Incorrect Information: Any inaccuracies, such as misspellings of names or incorrect addresses, may create complications in processing the form.

Not Following Submission Instructions: Ignoring details on how to submit the form can lead to delays. It’s important to pay attention to whether it should be mailed, faxed, or submitted online.

Neglecting State Requirements: Some individuals overlook the fact that different states may have varying requirements for filing a Tax POA form.

Using Outdated Forms: It's vital to ensure that you're using the most current version of the form to avoid unnecessary issues.

Not Keeping a Copy: Failing to retain a copy of the submitted form can be problematic if there are questions or issues later on.

The Tax Power of Attorney (POA) form 20A100 is an important document that allows an individual to designate someone else to act on their behalf regarding tax matters. When filing this form, you may also need to provide additional documents to support your requests or clarify your intentions. Below are some other forms and documents you might encounter in conjunction with the Tax POA form.

Having these documents on hand can facilitate the tax filing process and ensure that all necessary authorizations and declarations are properly submitted. Each form serves a specific purpose and can help streamline communications between you, your appointed representative, and the tax authorities.

The Tax POA form 20A100 is often compared to the IRS Form 2848, known as the Power of Attorney and Declaration of Representative. This document allows a designated individual to represent a taxpayer before the IRS. The two forms serve similar purposes in giving authority to third parties. Both documents require the taxpayer's signature and the specific scope of the authority granted, such as the ability to discuss tax matters or negotiate settlements. When a taxpayer submits Form 2848, it authorizes the representative to act in various capacities, much like the Tax POA form does at the state level.

Another document similar to the Tax POA form is the IRS Form 8821, which is used to authorize an individual or entity to receive and inspect confidential tax information. While Form 2848 allows for representation and negotiation, Form 8821 strictly permits access to tax information without granting the authority to act on behalf of the taxpayer. The key distinction lies in the extent of power granted, with the 20A100 and 2848 providing broader powers than Form 8821. Both require the taxpayer's information and identification, ensuring proper identification of the parties involved.

The state-level Power of Attorney forms often resemble the Tax POA form 20A100 in their intent and structure. Many states have their own specific POA documents that allow individuals to name representatives for a wide range of matters, including financial, health, and legal decisions. These POA forms share fundamental similarities with the Tax POA form by specifying the powers granted to the designated representative. They require identifying information for both the principal and the agent, creating a clear framework for the relationship between the parties.

Business-related Power of Attorney documents share traits with the Tax POA form as well. For example, a corporate Power of Attorney allows a designated representative to handle business transactions and affairs on behalf of a company. Just like the Tax POA form, these documents clarify the extent of the authority granted and any limitations that may apply. Both forms aim to streamline processes, allowing authorized representatives to act without needing to contact the principal directly for each action.

Lastly, the Durable Power of Attorney is another document that exhibits similarities with the Tax POA form. Designed to remain effective even if the principal becomes incapacitated, a Durable Power of Attorney allows appointed individuals to manage a person’s financial or medical decisions. Both types of documents require clear definitions of the powers granted and necessitate the principal's signature. While the contexts in which they operate differ, the underlying principle of empowering someone to act on behalf of another is a common thread that binds them together.

When filling out the Tax POA form 20a100, there are important guidelines to follow. Below is a list of things you should and shouldn't do to ensure your submission is accurate and effective.

Following these guidelines will help ensure that your Tax POA form is completed correctly and processed without unnecessary delays.

The Tax POA form 20a100 is a crucial document for taxpayers allowing them to appoint a representative for matters relating to their tax affairs. However, several misconceptions exist regarding its use and requirements. Below is a list of six common misconceptions.

This is inaccurate. Taxpayers can appoint a variety of representatives, including accountants or other individuals, as long as they are authorized to represent the taxpayer in tax matters.

This is not true. Once the form is filed, it remains in effect until the taxpayer revokes it or if the representative is changed.

The POA form 20a100 gives limited authority regarding specific tax matters, rather than broad legal powers.

Filing the form does not influence the outcome of any tax situation. It simply allows the appointed representative to advocate on behalf of the taxpayer.

This misconception is incorrect. The form can be submitted both electronically and via mail, depending on the taxpayer's preference.

This is false. The representative can communicate with tax authorities on the taxpayer’s behalf without the taxpayer being present.

When filling out and using the Tax POA form 20a100, keep these key points in mind: