The Tax POA E1285V4 form plays a crucial role for taxpayers seeking representation in tax matters before the IRS. This form designates an authorized individual to act on your behalf, ensuring that your interests are effectively communicated and protected in any dealings with federal and state tax authorities. It simplifies the process of granting power of attorney, allowing your representative to receive your confidential tax information, make inquiries, and handle disputes. Key details on the form include your personal information, the representative’s details, and the specific limitations of their authority. By using the E1285V4, you maintain control over your tax matters while enabling qualified professionals to assist you in navigating the complexities of the tax system. Proper completion and submission of this form is essential to avoid delays and ensure that your representative can act without hindrance.

SD EForm - 1285 V4

~

Department of

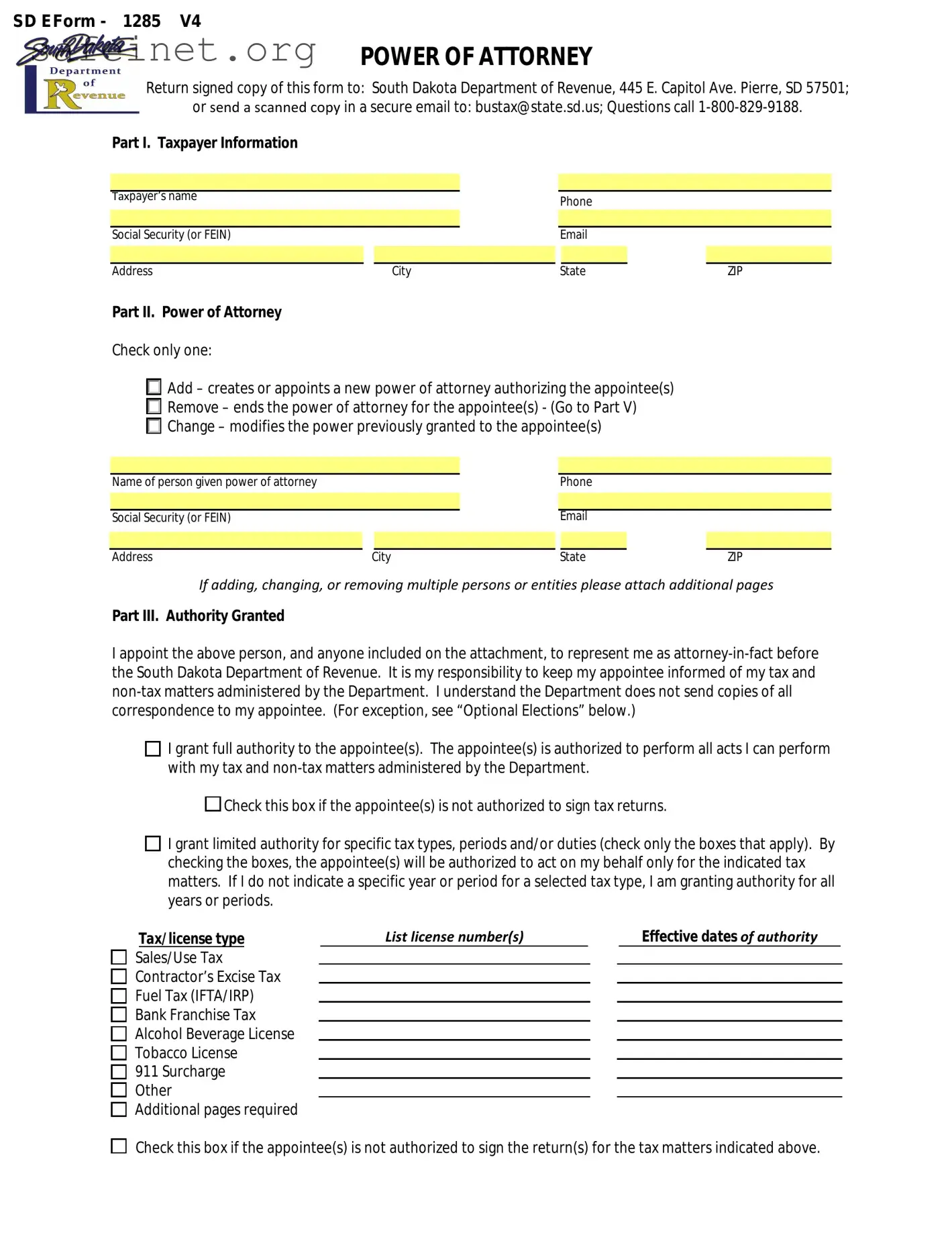

POWER OF ATTORNEY

Return signed copy of this form to: South Dakota Department of Revenue, 445 E. Capitol Ave. Pierre, SD 57501;

or send a scanned copy in a secure email to: [email protected]; Questions call

Part I. Taxpayer Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer’s name |

|

|

|

|

Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Social Security (or FEIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

City |

|

|

State |

|

ZIP |

Part II. Power of Attorney |

|

|

|

|

|

|

|

Check only one:

Add – creates or appoints a new power of attorney authorizing the appointee(s)

Remove – ends the power of attorney for the appointee(s) - (Go to Part V)

Change – modifies the power previously granted to the appointee(s)

|

|

|

|

|

|

|

|

Name of person given power of attorney |

|

|

|

|

Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Social Security (or FEIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

City |

|

|

State |

|

ZIP |

If adding, changing, or removing multiple persons or entities please attach additional pages

Part III. Authority Granted

I appoint the above person, and anyone included on the attachment, to represent me as

I grant full authority to the appointee(s). The appointee(s) is authorized to perform all acts I can perform with my tax and

Check this box if the appointee(s) is not authorized to sign tax returns.

I grant limited authority for specific tax types, periods and/or duties (check only the boxes that apply). By checking the boxes, the appointee(s) will be authorized to act on my behalf only for the indicated tax matters. If I do not indicate a specific year or period for a selected tax type, I am granting authority for all years or periods.

Tax/license type |

List license number(s) |

|

|

|

Effective dates of authority |

|

||

Sales/Use Tax |

|

|

|

|

|

|

||

Contractor’s Excise Tax |

|

|

|

|

|

|

|

|

Fuel Tax (IFTA/IRP) |

|

|

|

|

|

|

|

|

Bank Franchise Tax |

|

|

|

|

|

|

|

|

Alcohol Beverage License |

|

|

|

|

|

|

|

|

Tobacco License |

|

|

|

|

|

|

|

|

911Surcharge Other

Additional pages required

Check this box if the appointee(s) is not authorized to sign the return(s) for the tax matters indicated above.

Part IV. Optional Elections.

1. Authorize primary appointee to receive all correspondence, including refunds, from the Department.

I elect to the have South Dakota Department of Revenue send the primary appointee all refunds, legal notices, and correspondence about the tax and nontax debt matters specified in this document. By making this election, I understand that I will no longer receive anything – including refunds and legal notices – from the Department and my primary appointee will receive it on my behalf.

2. Authorize appointee to communicate by email.

I authorize the South Dakota Department of Revenue to communicate by email with my appointee(s). I understand private tax data about me will be sent over the Internet. I accept the risk my data may be accessed by someone other than the intended recipient. I agree the South Dakota Department of Revenue is not liable for any damages I may have as a result of interception.

Part V. Expiration Date and Signature

Expiration Date: ____________________________________________________________

(If no date is provided, this power of attorney and optional elections are valid until removed)

This power of attorney and elections are not valid until this document is signed by the taxpayer before a Notary and received by the Department.

_____________________________________ |

_________________________ |

___________________ |

|

Taxpayer’s signature (corporate officer, partner or fiduciary) |

Print name (and title, if applicable) |

Date |

|

Part VI. Notarization |

|

|

|

State of: |

_______________________ |

|

|

County of: |

_______________________ |

|

|

On this the _____ day of ________________, 20______, before the undersigned, a Notary Public for the State of

_______________________________ personally appeared _______________________________, known to me or

satisfactorily proven to be the person who executed the foregoing instrument, and acknowledged that he executed the same, in capacity as shown, of his own free act and deed.

In witness whereof I hereunto set my hand and official seal this ___ day of ___________, 20____.

__________________________

Notary Public

__________________________

My commission expires on:

| Fact Name | Description |

|---|---|

| Form Purpose | The Tax POA E1285V4 form is used to authorize an individual to represent a taxpayer before the tax authorities, allowing them to receive confidential information and take action on behalf of the taxpayer. |

| Who Can Use It? | This form can be utilized by individuals, businesses, or organizations that need someone to handle their tax matters, ensuring proper management of their tax responsibilities. |

| Governing Laws | The form is governed by federal tax regulations and may be subject to specific state laws depending on the taxpayer's state of residence or business. Always check local laws for additional requirements. |

| Filing Instructions | Once completed, the taxpayer must submit the E1285V4 form to the appropriate tax authority, ensuring that it is filled out correctly to avoid delays in processing. |

Filling out the Tax POA E1285V4 form is an essential step when designating someone to handle your tax matters. This form facilitates communication between the IRS and your chosen representative. Understanding each step is crucial to ensure accuracy and compliance.

After submitting the form, your designated representative will receive communication from the IRS regarding the matters you've authorized them to handle. Keep a copy of the completed form for your records, as it may be necessary for future reference or inquiries.

What is the Tax POA E1285V4 form?

The Tax POA E1285V4 form is a Power of Attorney document that allows an individual or a business to designate someone else to act on their behalf when dealing with tax matters. This could be a tax professional, a family member, or another trusted individual. It gives the appointed representative the authority to communicate with the IRS and handle tax-related issues, such as filing returns and receiving confidential information regarding taxes.

Who should use the Tax POA E1285V4 form?

This form is suitable for anyone who needs assistance with tax issues and wants to authorize another person to represent them. This includes individuals who may not have the time or expertise to handle their tax matters effectively. Business owners may also find it helpful to appoint a tax advisor, especially during complex transactions or audits.

How do I fill out the Tax POA E1285V4 form?

To complete the Tax POA E1285V4 form, start by providing your personal information, such as your name, address, and Social Security number or Employer Identification Number. Then, clearly state the name of the person you are authorizing. Be sure to specify the type of tax matters they can handle on your behalf. Review the form for accuracy before signing and dating it. It’s important that all fields are filled out correctly to avoid any issues.

Do I need to submit the Tax POA E1285V4 form to the IRS?

Yes, once you have filled out and signed the Tax POA E1285V4 form, you need to submit it to the IRS. The completed form can typically be sent via mail or, in some cases, submitted electronically. After the form is submitted, the IRS will recognize your appointed representative and allow them to act on your behalf in tax matters. Keep a copy of the submitted form for your records.

Ignoring Instructions: Many people fail to thoroughly read the instructions that accompany the form. Each section of the form has specific requirements that must be followed.

Incorrect Taxpayer Identification Number: Entering the wrong Taxpayer Identification Number (TIN) can lead to processing delays or rejection of the form.

Poor Signature Practices: Some forget to sign the form or use a signature that doesn’t match their legal name, causing further issues.

Missing Dates: It’s critical to date the form correctly. Omitting the date can lead to ambiguity about when the authority was granted.

Incorrectly Identifying the Representative: Not providing accurate details about the person representing you can create significant complications, including the denial of representation.

Inadequate Specification of Tax Matters: Failing to specify the exact tax matters can result in the representative not having the authority to act on certain issues.

Neglecting to Provide Additional Documentation: Some individuals do not supply necessary documents, such as proof of identity for their representative.

Overlooking State Requirements: Tax laws vary by state and some people do not check if their state has additional requirements for the form.

Using an Outdated Version of the Form: Using an old version instead of the most current one can cause issues with acceptance.

Failing to Keep Copies: Not keeping a copy of the submitted form for personal records can lead to problems if any disputes arise in the future.

The Tax Power of Attorney (POA) E1285V4 form is a crucial document that enables an individual to authorize someone else to handle tax matters on their behalf. When using this form, several other documents may be beneficial or required to ensure all aspects of tax representation are covered. Below is a list of related forms and documents commonly used alongside the Tax POA E1285V4.

In summary, the Tax POA E1285V4 form often pairs with various other documents to streamline tax-related processes and ensure comprehensive representation. Collecting and understanding these forms is essential in navigating tax matters effectively.

The IRS Form 2848 is often compared to the Tax POA E1285V4 form, as both documents grant someone authority to represent a taxpayer before the IRS. By submitting Form 2848, a taxpayer designates an individual, such as an accountant or attorney, to handle their tax matters. It specifies the types of tax matters the representative can discuss or negotiate, ensuring that the taxpayer maintains control over their tax affairs while receiving assistance when needed.

Another similar document is Form 8821, which is known as the Tax Information Authorization. Unlike the Tax POA E1285V4, the 8821 form allows an appointee to obtain tax information on behalf of the taxpayer but does not grant them the authority to represent the taxpayer in dealings with the IRS. This makes it a good option for taxpayers who need someone to gather information without the complexity of full representation.

The California Form 540-POA is relevant for individuals filing state taxes in California. This document serves a similar purpose by allowing a person to act on behalf of the taxpayer for state tax matters as the Tax POA E1285V4 does for federal matters. It helps bridge the gap for individuals who need support with state-level compliance and issues.

In New York, the Form POA-1 serves a parallel function to the Tax POA E1285V4, granting authority to a representative to act on behalf of a taxpayer for New York State income tax purposes. The similarities lie in how both forms formalize the relationship between a taxpayer and their chosen representative, streamlining the process for handling tax affairs.

Form 56, also known as Notice Concerning Fiduciary Relationship, has similarities with the Tax POA E1285V4, especially for individuals who appoint a fiduciary. This form establishes a formal fiduciary relationship recognized by the IRS, allowing the fiduciary to manage tax matters on behalf of the taxpayer, similar to a power of attorney.

For businesses, the IRS Form 8821-B is designed to authorize third parties to receive tax information on behalf of business entities. While it parallels the Tax POA E1285V4 in terms of authorization, it is distinct in its focus on business-related tax matters. This allows companies to grant access to their tax records without giving full representation rights.

Furthermore, many states have their own version of a Power of Attorney specifically targeting tax issues, like Florida’s Form DR-835. This document allows taxpayers in Florida to appoint a representative to manage local tax matters. Its aim is consistent with the Tax POA E1285V4, as both facilitate communication and negotiation between taxpayers and tax authorities.

In Texas, the Form 01-117 serves a similar purpose. This statewide document allows individuals to designate a representative for handling state tax issues. It shares the general intent of the Tax POA E1285V4, ensuring that representatives can act on behalf of a taxpayer effectively, whether on the state or federal level.

Lastly, the Delegation of Authority form often used in corporate settings is akin to the Tax POA E1285V4. It allows executives to transfer their decision-making power to others for specific matters, including tax. Both documents empower others to act on behalf of the principal or taxpayer, whether for individual tax issues or broader organizational decisions.

When filling out the Tax POA E1285V4 form, it’s crucial to follow best practices to ensure accuracy and compliance. Here’s a list of do's and don’ts to guide you through the process.

Here are ten misconceptions about the Tax POA E1285V4 form, along with brief explanations:

This is not true. Individuals can file the form on their own behalf.

The Tax POA E1285V4 form can be used for various federal tax matters, not limited to specific taxes.

The power of attorney needs to be renewed or can be revoked at any time. It is not automatically ongoing.

Filing the form does not guarantee acceptance of requests made by the appointed representative.

There is no fee associated with filing the Tax POA E1285V4 form with the IRS.

The IRS allows different methods for submission, including fax in certain cases.

You can submit a new form to change your representative whenever necessary.

Notarization is not a requirement for the Tax POA E1285V4 form.

You can easily revoke the power of attorney by submitting a revocation form.

The Tax POA E1285V4 form serves as a Power of Attorney for tax purposes. Below are key takeaways for effectively completing and utilizing this form.

Understanding these key points can help ensure that the form is completed accurately and that your representative can effectively manage your tax matters.