The Tax POA DO-10 form is a critical document that facilitates communication between taxpayers and the Department of Revenue. It serves as a power of attorney, allowing individuals to designate a representative to handle their tax matters on their behalf. This level of delegation can be especially beneficial during complex tax situations, audits, or when interacting with tax authorities. The form requires basic information about the taxpayer and the appointed representative, ensuring that the representative is authorized to act in specific capacities, such as receiving confidential information or negotiating on tax liabilities. Taxpayers must be mindful of completing the form accurately, as any errors may delay or complicate their tax interactions. Furthermore, it is important to understand the revocation process of this authorization, which provides taxpayers with control over their representation. Each year, the use of this form helps many navigate the complexities of tax law, reaffirming its importance in the lives of American taxpayers.

KANSAS DEPARTMENT OF REVENUE |

800618 |

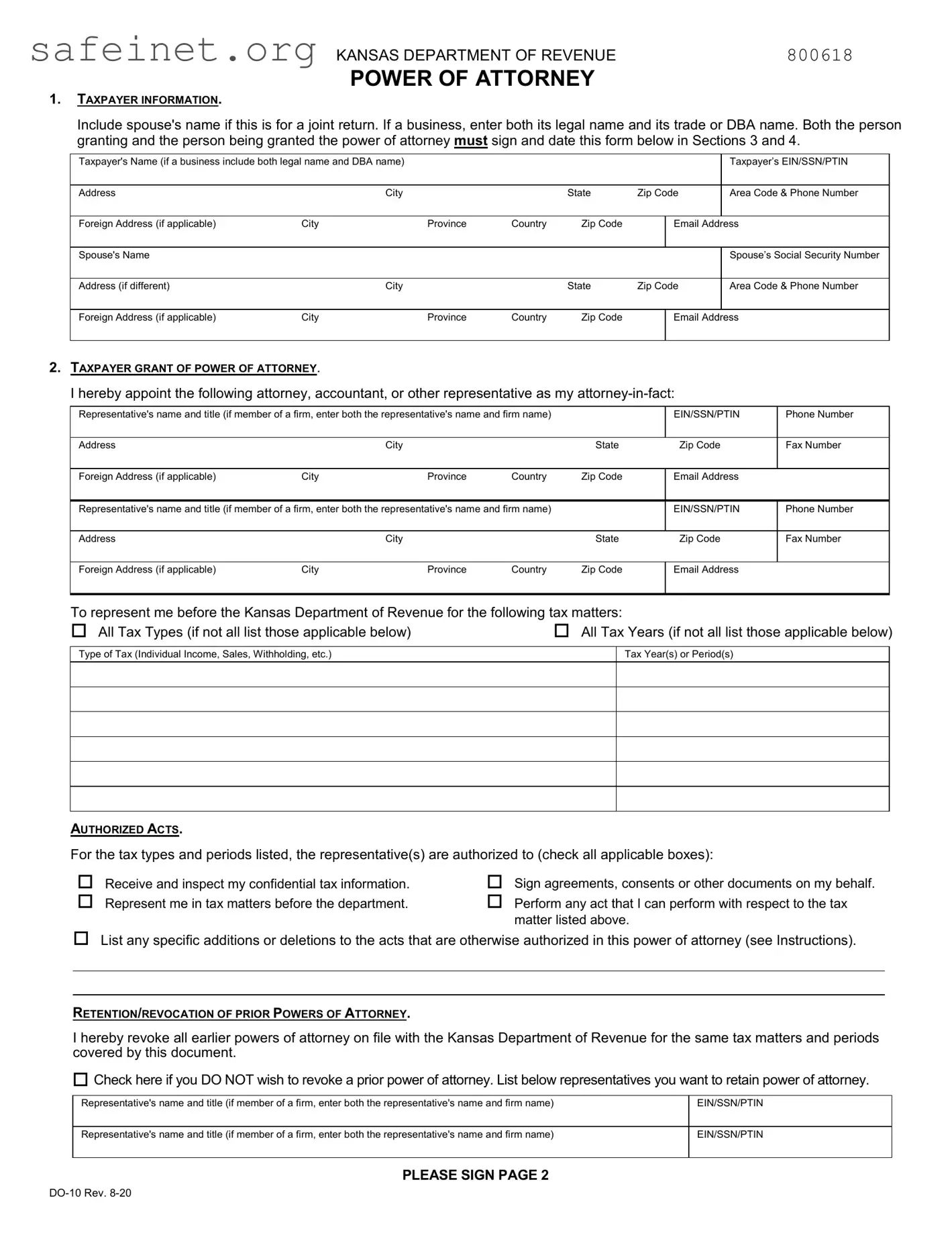

POWER OF ATTORNEY

1.TAXPAYER INFORMATION.

Include spouse's name if this is for a joint return. If a business, enter both its legal name and its trade or DBA name. Both the person granting and the person being granted the power of attorney must sign and date this form below in Sections 3 and 4.

Taxpayer's Name (if a business include both legal name and DBA name) |

|

|

|

|

|

Taxpayer’s EIN/SSN/PTIN |

|

|

|

|

|

|

|

|

|

Address |

City |

|

|

State |

Zip Code |

Area Code & Phone Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

|

IEmail Address |

|

Spouse's Name |

|

|

|

|

|

|

Spouse’s Social Security Number |

|

|

|

|

|

|

|

|

Address (if different) |

City |

|

|

State |

Zip Code |

Area Code & Phone Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

|

IEmail Address |

|

2.TAXPAYER GRANT OF POWER OF ATTORNEY.

I hereby appoint the following attorney, accountant, or other representative as my

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

|

EIN/SSN/PTIN |

Phone Number |

|

|||

|

|

|

|

|

|

|

|

Address |

|

City |

|

State |

Zip Code |

Fax Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

Email Address |

|

|

|

|

|

|

|

|||

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

|

EIN/SSN/PTIN |

Phone Number |

|

|||

|

|

|

|

|

|

|

|

Address |

|

City |

|

State |

Zip Code |

Fax Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

Email Address |

|

|

|

|

|

|

||||

To represent me before the Kansas Department of Revenue for the following tax matters: |

|

|

|

||||

All Tax Types (if not all list those applicable below) |

|

All Tax Years (if not all list those applicable below) |

|||||

Type of Tax (Individual Income, Sales, Withholding, etc.)

Tax Year(s) or Period(s)

AUTHORIZED ACTS.

For the tax types and periods listed, the representative(s) are authorized to (check all applicable boxes):

Receive and inspect my confidential tax information.

Represent me in tax matters before the department.

Sign agreements, consents or other documents on my behalf.

Perform any act that I can perform with respect to the tax matter listed above.

List any specific additions or deletions to the acts that are otherwise authorized in this power of attorney (see Instructions).

RETENTION/REVOCATION OF PRIOR POWERS OF ATTORNEY.

I hereby revoke all earlier powers of attorney on file with the Kansas Department of Revenue for the same tax matters and periods covered by this document.

Check here if you DO NOT wish to revoke a prior power of attorney. List below representatives you want to retain power of attorney.

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

EIN/SSN/PTIN |

|

|

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

EIN/SSN/PTIN |

|

|

PLEASE SIGN PAGE 2

3.SIGNATURE OF TAXPAYER(S). If a tax matter concerns a joint return, both husband and wife must sign when joint representation is requested. When a corporate officer, partner, guardian, executor, receiver, administrator, or trustee signs this section on behalf of a taxpayer, the signatory also certifies that the signatory is authorized to execute this form on behalf of the taxpayer.

(Signature) |

(Printed Name) |

(Date) |

(Signature) |

(Printed Name) |

(Date) |

4.SIGNATURE OF REPRESENTATIVE(S).

(Signature) |

(Printed Name) |

(Date) |

(Signature) |

(Printed Name) |

(Date) |

INSTRUCTIONS FOR POWER OF ATTORNEY AUTHORIZATION

A power of attorney is a legal document authorizing someone to act as your representative. You, the taxpayer, must complete, sign, and return this form if you wish to grant a power of attorney (POA) to an attorney, accountant, agent, tax return preparer, family member, or anyone else to act on your behalf with the Kansas Department of Revenue (KDOR). You may use this form for any matter affecting any tax administered by the department, including audit and collection matters. This POA will remain in effect until the expiration date, if included under Section 2, or until you revoke it, whichever is earlier. KDOR will accept copies of this form, including fax copies.

SECTION 1. TAXPAYER INFORMATION.

Individuals. In the block provided, enter your name, SSN, address, telephone number, and email address in the spaces provided. If this POA is for a joint return and your spouse is designating the same representative or representatives, enter your spouse’s name, address (if different from your own), Social Security number, and your spouse’s email address.

Businesses. Enter both the legal name and the DBA or trade name, if different. For example, if the business is an individual proprietorship, enter the proprietor's name and the name under which business is transacted. (e.g., Joe Smith dba Joe's Diner). Also enter the EIN (federal employer identification number), telephone number, business address, and email address.

Estates. Enter the name, title, address, and email address of the decedent’s executor/personal representative in the taxpayer section. Use the spouse’s section to enter the decedent’s name, date of death, and SSN.

SECTION 2. TAXPAYER GRANT OF POWER OF ATTORNEY.

Representative's name. Complete all the requested information for each representative. If the representative is a member of a firm, enter the firm’s name too. If you are designating more than two representatives, please complete another form and attach it to this form. Mark the second form “additional representatives.”

Type of tax. If you wish the power of attorney to apply to all periods and all tax types administered by KDOR, please check the box(es) for "All tax types" and "All tax periods". If for a specific tax type and/or tax year enter the type of tax and the tax years or reporting periods for each tax type. If the matter relates to estate, inheritance, or succession tax, please enter the date of the decedent’s death.

Authorized acts. Check all boxes that apply. Use the additional lines to limit, clarify, or otherwise define the acts authorized by this POA. For example, if you wish to limit the POA to a specific time period or to establish an expiration date, enter that information and the dates (month, day, and year) on these lines.

Retention/revocation of prior powers of attorney. Unless otherwise specified, this POA replaces and revokes all previous POAs on file with the department. If there is an existing POA that you do NOT want to revoke, check the box in this section and enter the representative’s name and EIN/SSN/PTIN in the space provided.

If you wish to revoke an existing POA without naming a new representative, attach a copy of the previously executed POA. On the copy of the previously executed POA, write “REVOKE” across the top of the form, and initial and date it again under your signature or signatures already in Section 3.

SECTION 3. SIGNATURE OF TAXPAYER(S).

You must sign and date the POA. If a joint return is being filed and both husband and wife intend to authorize the same person to represent them, both spouses must sign the POA unless one spouse has authorized the other in writing to sign for both. You must attach a copy of your spouse's written authorization to this POA.

SECTION 4. SIGNATURE OF REPRESENTATIVE(S).

Each representative that you name must sign and date this form.

TAXPAYER ASSISTANCE

If you have questions about this form, please visit or call our office.

Taxpayer Assistance Center

Scott State Office Building

120 SE 10th St.

PO Box 3506

Topeka, KS

Phone:

The Department of Revenue office hours are 8 a.m. to 4:45 p.m., Monday through Friday.

Additional copies of this form are available from our website at: ksrevenue.org

2

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA DO-10 form is used to grant power of attorney to an individual, allowing them to represent a taxpayer regarding tax matters. |

| State Specificity | This form is applicable in the state of New Jersey, following the provisions of the New Jersey Division of Taxation regulations. |

| Governing Law | The use of this form adheres to New Jersey laws, specifically N.J.S.A. 54:49-5 related to taxpayer representation. |

| Filing Requirement | Taxpayers must submit the Tax POA DO-10 form to the state Division of Taxation to formalize the representation. |

| Revocation | Taxpayers can revoke the power of attorney at any time by filing a formal revocation form with the Division of Taxation. |

Filling out the Tax POA DO-10 form is straightforward. Once it's complete, you'll be ready to submit it to the appropriate tax authority. The form will help designate someone to handle tax matters on your behalf.

After completing these steps, review the entire form for any mistakes. It's essential to ensure everything is accurate before submitting. You can then send the form to the relevant tax authority according to their submission guidelines.

What is the Tax POA DO-10 form?

The Tax POA DO-10 form is a Power of Attorney specifically designed for tax matters in the United States. This form allows an individual, known as the principal, to appoint another person, referred to as the agent or attorney-in-fact, to represent them before the tax authority. The appointed agent can handle various tax-related issues, including filing returns, making payments, and discussing any audits or disputes that may arise. By completing this form, taxpayers can ensure that their financial interests are managed by someone they trust while maintaining their rights as taxpayers.

Who can use the Tax POA DO-10 form?

Any individual who needs assistance with their tax affairs can use the Tax POA DO-10 form. This includes taxpayers who may be unable to navigate the complexities of tax filings or those who simply prefer to delegate their responsibilities to a trusted individual, such as a spouse, family member, or professional advisor. It is particularly beneficial for individuals who have busy schedules, are not confident in managing their own taxes, or have specific tax-related complications that require expertise.

How do I complete the Tax POA DO-10 form?

Completing the Tax POA DO-10 form involves filling out essential information about both the principal and the agent. This typically includes names, addresses, and taxpayer identification numbers for both parties. The form also allows you to specify the exact powers you are granting to your agent. Be mindful that the more detailed you are, the better your agent can act on your behalf. After filling out the form, it is important to sign and date it, as these are critical to its validity. Once completed, you may need to submit it to the relevant tax authority, depending on your specific circumstances.

What are the benefits of using the Tax POA DO-10 form?

Utilizing the Tax POA DO-10 form offers several advantages. First, it provides peace of mind by allowing you to choose someone who is knowledgeable to handle your tax matters efficiently. This can lead to more accurate filings and timely responses to any inquiries from tax authorities. Additionally, it saves you time and energy, freeing you to focus on other aspects of your life. Moreover, should disputes arise, having a designated agent can make the resolution process smoother, since your agent can engage directly with tax officials on your behalf.

Incorrect Information Entry: Many individuals provide inaccurate personal information on the form. This includes misspelled names, wrong addresses, or incorrect Social Security numbers. Ensure all details match official records.

Signature Issues: Failing to sign the form or using an outdated signature can lead to delays. The person granting power of attorney must sign the document for it to be valid.

Missing Authorization Sections: Some users neglect to fill out the sections that specify the powers being granted. Be clear about what authority the agent will have over your tax matters.

Failure to Submit on Time: Not submitting the form before important deadlines can result in inconvenience. Be proactive in submitting the Tax POA DO-10 to avoid complications with tax representation.

The Tax Power of Attorney (POA) DO-10 form is essential for individuals who wish to designate someone to act on their behalf regarding tax matters. Alongside this form, there are several other documents that can play a crucial role in the process. Below is a brief overview of these additional forms and documents commonly utilized in conjunction with the Tax POA DO-10 form.

Consideration of these documents can help streamline the process and ensure that all tax matters are handled efficiently and effectively. It is essential to understand each form's purpose and how it contributes to the overall management of one's tax responsibilities.

The IRS Form 2848, Power of Attorney and Declaration of Representative, serves a purpose similar to the Tax POA DO-10. Like the DO-10, the 2848 allows a taxpayer to designate someone, typically a tax professional, to represent them before the IRS. This form grants the representative authority to handle tax matters, communicate with the IRS, and access the taxpayer's tax information. With both documents, the taxpayer maintains control while benefiting from the expertise of their chosen representative.

The IRS Form 8821, Tax Information Authorization, also shares commonalities with the Tax POA DO-10. Whereas the 2848 designates a representative for advocacy, the 8821 authorizes someone to access a taxpayer’s tax information. This provides flexibility for taxpayers who may want to share their financial details with accountants or advisors without granting them full representation rights. Both forms streamline communication between the taxpayer and tax authority, ensuring that the appropriate people can receive pertinent information.

When filling out the Tax POA DO-10 form, you want to be careful and accurate. Here are some important dos and don'ts to keep in mind:

The Tax POA DO-10 form, also known as the Power of Attorney form for tax purposes, often leads to misunderstandings. Here are five common misconceptions about this form, along with clarifications to help demystify it.

Understanding these misconceptions can make the process smoother and help taxpayers navigate their tax responsibilities more confidently.

When filling out and using the Tax POA DO-10 form, consider the following key takeaways: