The Tax Power of Attorney (POA) D-2848 form serves as a crucial document in managing your tax matters effectively. This form allows individuals to authorize another person, such as an attorney or tax advisor, to represent them before the Internal Revenue Service (IRS). By granting this authority, a taxpayer can ensure that their interests are adequately represented, facilitating communication with the IRS. The D-2848 provides comprehensive coverage regarding specific tax matters, including income tax, estate tax, and business tax obligations. Additionally, this form encompasses the ability to handle the issuance of requests for information, as well as negotiating tax debts. By understanding the major components of the form, including the appointment of the representative, the scope of authority granted, and the revocation process, individuals can navigate the complexities of tax representation with confidence and clarity. Proper completion and submission of the D-2848 are essential to prevent any misunderstandings or lapses in representation, making it a key element in tax compliance and management.

This is a

- |

Government of the |

OFFICIAL USE ONLY |

|

*** District of Columbia |

Declaration of Representation |

|

|

|

|

||

▲

▲

▲

▲

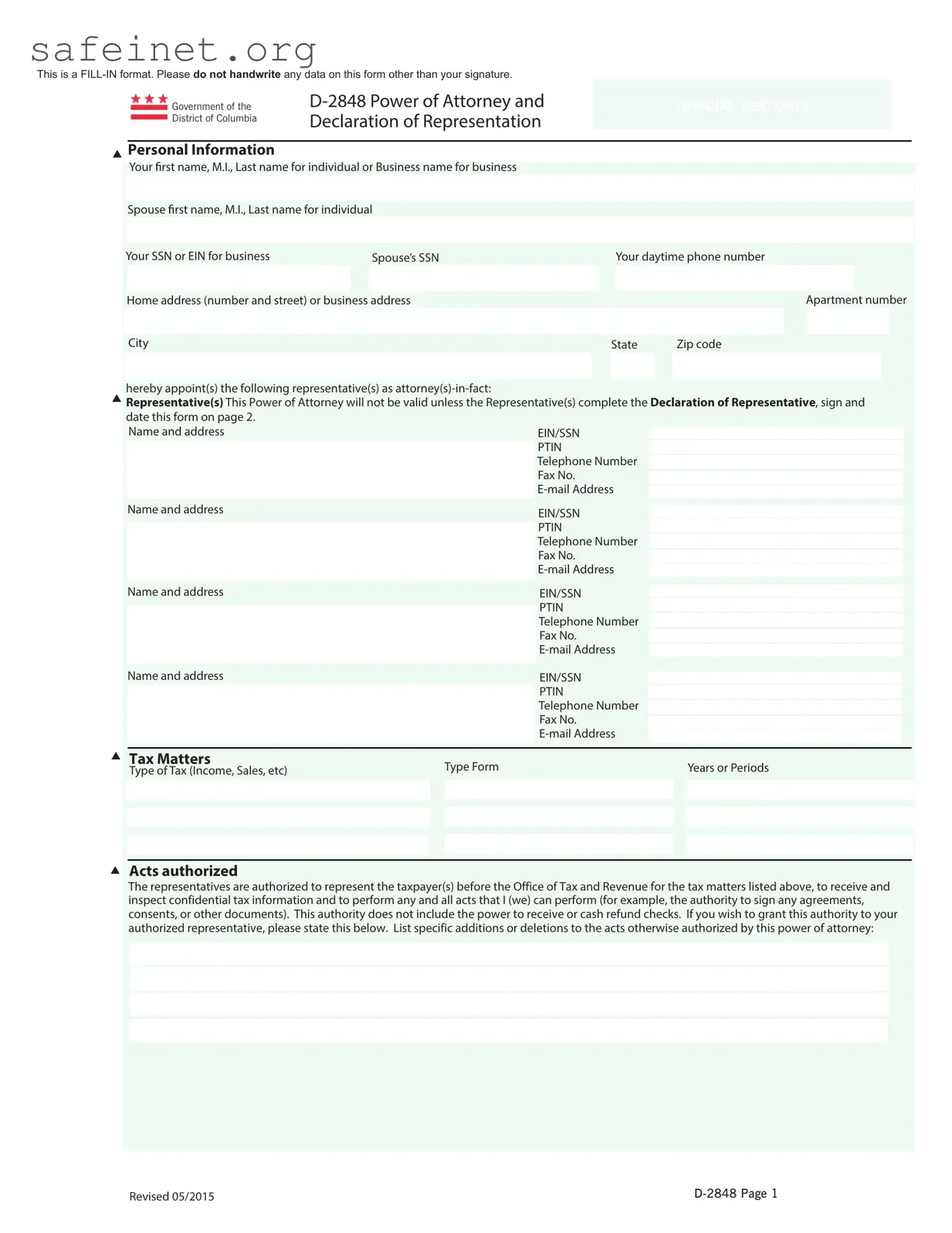

Personal Information

Your frst name, M.I., Last name for individual or Business name for business

Spouse frst name, M.I., Last name for individual

|

Your SSN or EIN for business |

|

Spouse’s SSN |

|

|

|

Your daytime phone number |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street) or business address |

|

|

|

|

|

|

Apartment number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

Zip code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

hereby appoint(s) the following representative(s) as

Representative(s) This Power of Attorney will not be valid unless the Representative(s) complete the Declaration of Representative, sign and date this form on page 2.

Name and addressEIN/SSN

PTIN Telephone Number

Fax No.

Name and address |

|

|

|

|

|

|

|

|

|||

|

|

EIN/SSN |

|

|

|

|

|

|

|||

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

Fax No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Name and address |

|

|

EIN/SSN |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

Fax No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

Name and address |

|

|

EIN/SSN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Fax No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax Matters |

Type Form |

|

|

|

|

|

Years or Periods |

|

|

|

|

Type of Tax (Income, Sales, etc) |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Acts authorized

The representatives are authorized to represent the taxpayer(s) before the Office of Tax and Revenue for the tax matters listed above, to receive and inspect confidential tax information and to perform any and all acts that I (we) can perform (for example, the authority to sign any agreements, consents, or other documents). This authority does not include the power to receive or cash refund checks. If you wish to grant this authority to your authorized representative, please state this below. List specific additions or deletions to the acts otherwise authorized by this power of attorney:

Revised 05/2015 |

▲

▲

▲

▲

▲

Taxpayer's SSN or FEIN |

|

Taxpayer's Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retention/revocation of prior power(s) of attorney By filing this power of attorney form, you automatically revoke all earlier power(s) of attorney on file with the Office of Tax Revenue for the same tax matters and years or periods covered by this document.

If you do not want to revoke a prior power of attorney, check here:

You must attach a copy of any Power of Attorney you want to remain in effect.

Signatures

Signature of taxpayer(s) If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer. If other than the taxpayer, print the name here and sign below.

Your Signature |

|

Date |

|

Title if other than individual |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse's signature if filing jointly |

|

Date |

|

|

|

|

|||

|

|

Telephone number if other than the taxpayer |

|||||||

|

|

|

|

|

|

|

|

|

|

If not signed and dated, this power of attorney will be returned

Declaration of Representative Representative(s) must complete this section and sign below.

Under penalties of perjury, I declare that:

As the authorized representative of the taxpayer(s) identified for the tax matter(s) specified herein; I am one of the following:

a.A member in good standing of the bar of the highest court of the jurisdiction shown below.

b.A Certified Public Accountant duly qualified to practice in the jurisdiction shown below.

c.An Enrolled Agent under the requirements of Treasury Department Circular # 230.

d.A bona fide officer of the taxpayer’s organization.

e.A

f.A member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

g.A general partner of a partnership.

h.Student Attorney or CPA- receives permission to represent taxpayers before the IRS by virtue of his/her status as a law, business, or accounting student working in an Low Income Taxpayer Clinic or Student Tax Clinic Program.

i.Other

Designation- |

|

Licensing jurisdiction (state) |

Bar, license, certification, |

|

|

|

|

|

||

|

Insert above |

|

or other licensing authority |

registration, or enrollment number |

|

Signature |

|

Date |

|

|

|

letter |

|

(if applicable) |

(if applicable) |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If you have any questions regarding the Power of Attorney, contact the Office of Tax and Revenue, Customer Service Administration, 1101 4th Street, SW, Washington, DC 20024; or call (202)

Mail the original Power of Attorney to:

Office of Tax and Revenue, Customer Service Administration, PO Box 470, Washington, DC

If this declaration is not signed and dated, this power of attorney will be returned

| Fact Name | Description |

|---|---|

| Purpose | The D-2848 form is used to grant someone the authority to represent you before the tax authorities. |

| Authorization Scope | It allows the representative to discuss and resolve tax-related matters on behalf of the taxpayer. |

| Who Can Use It | Any individual or business entity can use the D-2848 form to designate a representative. |

| Eligibility Requirements | The representative must be a qualified tax professional, such as a CPA or attorney. |

| Filing Deadline | It should be filed with the relevant tax authority before any tax-related matters are handled. |

| Duration of Authority | The authority granted by the D-2848 form remains in effect until revoked or until it expires based on the taxpayer's need. |

| Specific State Requirements | In some states, additional forms or documentation may be required based on local tax laws, such as representing in California or New York. |

| Signature Requirement | Both the taxpayer and the representative must sign the D-2848 form to validate the authority being granted. |

| Revocation Process | The taxpayer can revoke the representative's authority by submitting a written notice to the tax authority. |

Filling out the Tax POA D-2848 form is a crucial step in ensuring that you can designate someone to represent you before the IRS regarding your tax matters. It’s essential to complete the form accurately to avoid delays or complications in processing your request for power of attorney. Below are the steps needed to effectively fill out the form.

After submitting the form, you should allow some time for processing. It’s important to follow up if you do not receive confirmation from the IRS. Ensure your representative is prepared to take action on your behalf, keeping in mind they may need additional information from you to proceed with your tax matters.

What is the Tax POA D-2848 form?

The Tax POA D-2848 form, also known as the Power of Attorney for Tax Matters, is a document that allows an individual to authorize someone else to represent them in front of tax authorities. This representation can include managing tax disputes, filing tax returns, or making inquiries about the taxpayer’s account. It is commonly used in the context of federal and state tax issues.

Who can I designate as my representative using the D-2848 form?

You can designate individuals such as attorneys, accountants, or any person you trust to handle your tax matters. The representative must be someone who is eligible to practice before the tax authority in question. For example, they could be a certified public accountant (CPA), enrolled agent, or attorney.

How do I complete the Tax POA D-2848 form?

To complete the form, provide your personal information, including your name, address, and taxpayer identification number. Then clearly list the name and contact information of your representative. It's vital to indicate the specific tax matters and the tax years covered by the Power of Attorney. Always ensure that the form is signed and dated to validate it.

Do I need to submit the D-2848 form to my tax authority?

Yes, once the form is completed and signed, it must be submitted to the tax authority you are dealing with. Some agencies might allow it to be submitted electronically, while others may require a mailed copy. Check the specific requirements of the agency involved.

How long is the D-2848 form valid?

The Power of Attorney granted through the D-2848 form generally remains in effect until you revoke it in writing or until the tax matter is resolved. It is advisable to review the terms annually or when circumstances change, as you may need to update the appointment or the authority granted.

Can I revoke the D-2848 form once it is submitted?

Yes, you have the right to revoke the Power of Attorney at any time. To do this, you must provide written notice to the tax authority along with a copy of the revocation letter to your former representative. This action effectively terminates their authority to act on your behalf.

Are there any fees associated with the D-2848 form?

Generally, there are no fees for submitting the D-2848 form itself to the tax authority. However, if you choose to hire a representative such as a CPA or attorney to assist you, there may be fees associated with their services. It’s important to clarify any potential costs with your chosen representative beforehand.

What should I do if I need to change my representative after submitting the D-2848 form?

If you need to change your representative, you should file a new D-2848 form with the updated information for your new representative. You should also revoke the previous Power of Attorney unless the change is being made simultaneously. Clear communication about these changes with both the tax authority and your representatives is crucial to avoid confusion.

Where can I find the D-2848 form?

The D-2848 form is typically available on the website of the tax authority you are dealing with. You can find it as a downloadable PDF document. Ensure you are looking at the most current version of the form, as templates and requirements may change over time.

Incorrect Personal Information: One of the most common mistakes occurs when individuals fail to provide accurate personal details. This includes the name, address, and taxpayer identification number (TIN). Any discrepancies can cause delays or even the rejection of the form.

Missing Signatures: Many people forget to sign the form. A signature is essential as it verifies consent for the appointed representative to act on behalf of the taxpayer. Ensure that both the taxpayer and any joint filers sign the document where required.

Failure to Specify the Scope of Authority: It's crucial to clearly outline what authority the representative will have. This could range from general representation to limited actions concerning specific tax periods. Not clarifying this can lead to misunderstandings or limitations on the representative's power.

Incorrect Date Entries: Filling in the date inaccurately is often overlooked. Dates should accurately reflect when the taxpayer or representative signed the form. An error here could result in processing issues, so double-check all date entries.

When preparing to grant someone the authority to represent you in tax matters, various forms and documents may be necessary alongside the Tax Power of Attorney (POA) D-2848 form. These documents help ensure that your wishes are clearly understood and legally supported. Here’s a list of commonly used forms:

Each of these forms serves a specific purpose and can complement the Tax POA D-2848 form in ensuring your tax matters are handled effectively and respectfully. It is always wise to consult with a tax professional to determine which documents best meet your needs.

The IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, allows individuals to authorize someone to act on their behalf regarding tax matters. A similar document is the IRS Form 8821, which serves as a Tax Information Authorization. While Form 2848 gives someone the power to represent you in tax matters, Form 8821 only allows the individual to receive and review your tax information without the authority to act on your behalf. This means that if you need help with specific actions, like filing or negotiating, Form 2848 is the better choice.

Next, the Durable Power of Attorney (DPOA) is another document that closely resembles the IRS Form 2848 in its intent but extends beyond tax issues. A DPOA appoints someone to manage your legal and financial affairs, even if you become incapacitated. This document is broader in scope, allowing the appointed person to handle various aspects of your life, whereas Form 2848 is strictly for tax representation. However, both documents share the essential function of granting authority to another individual.

The Health Care Power of Attorney (HCPOA) is also similar, though it focuses on medical decisions rather than taxes or financial matters. While Form 2848 allows someone to represent you to the IRS, a HCPOA empowers someone to make healthcare decisions on your behalf if you're unable to do so. Both forms emphasize the importance of designating trusted individuals to act in your best interests, making the appointment of a representative key in various life situations.

Another related document is the Limited Power of Attorney. This allows you to grant specific powers to someone for a limited time or for particular tasks, such as handling a real estate transaction or signing a check. While Form 2848 is specifically about tax matters, both documents share the idea of authorizing a representative to act on your behalf, albeit in a more restricted context in the case of a Limited Power of Attorney.

Finally, the General Power of Attorney (GPOA) allows an individual to act on your behalf in a broad range of circumstances. Like the IRS Form 2848, a GPOA can enable someone to take significant actions, but it covers many areas beyond just taxes, including financial and legal matters. The main difference is the specific purpose of Form 2848, which is targeted solely at tax-related issues, while the GPOA serves a more encompassing role.

When filling out the Tax POA D-2848 form, it's important to keep certain dos and don'ts in mind. Here’s a helpful list to guide you through the process:

By following these tips, you can help ensure that your form is filled out correctly and processed smoothly.

The IRS Form 2848, also known as the Power of Attorney (POA) form, is essential for individuals or businesses allowing someone to act on their behalf regarding tax matters. However, several misconceptions surround this form. Here are seven common misunderstandings:

Understanding these misconceptions can help individuals and businesses make informed decisions when completing IRS Form 2848. Clarity regarding how the form works ensures that you utilize it effectively and responsibly.

Filling out the Tax POA D-2848 form is essential for anyone looking to authorize a representative to handle their tax matters. Here are some key takeaways to consider when using this form.

By being thorough and clear when filling out the D-2848 form, you can ensure that your tax representation needs are met effectively and efficiently.