The Tax POA Authorization to Disclose Tax Information form serves as a crucial tool that allows taxpayers to authorize another individual, often an accountant or tax professional, to access their sensitive tax information. This form is particularly important during tax season or when an individual needs assistance with their tax affairs. By completing this authorization, taxpayers can grant specified representatives the right to communicate directly with the IRS on their behalf. The form outlines vital details, including the taxpayer’s name, contact information, and the representative’s designation. Additionally, it details the extent of authority granted, which can range from basic inquiries about filing status to more complex matters involving specific tax years or forms. Completing the Tax POA form not only facilitates smoother communications between the taxpayer and the IRS but also ensures that the representatives can receive confidential information necessary for effective tax planning and resolution of disputes. Understanding how this form works is essential for anyone seeking to manage their taxes while relying on professional expertise.

CLEAR FORM

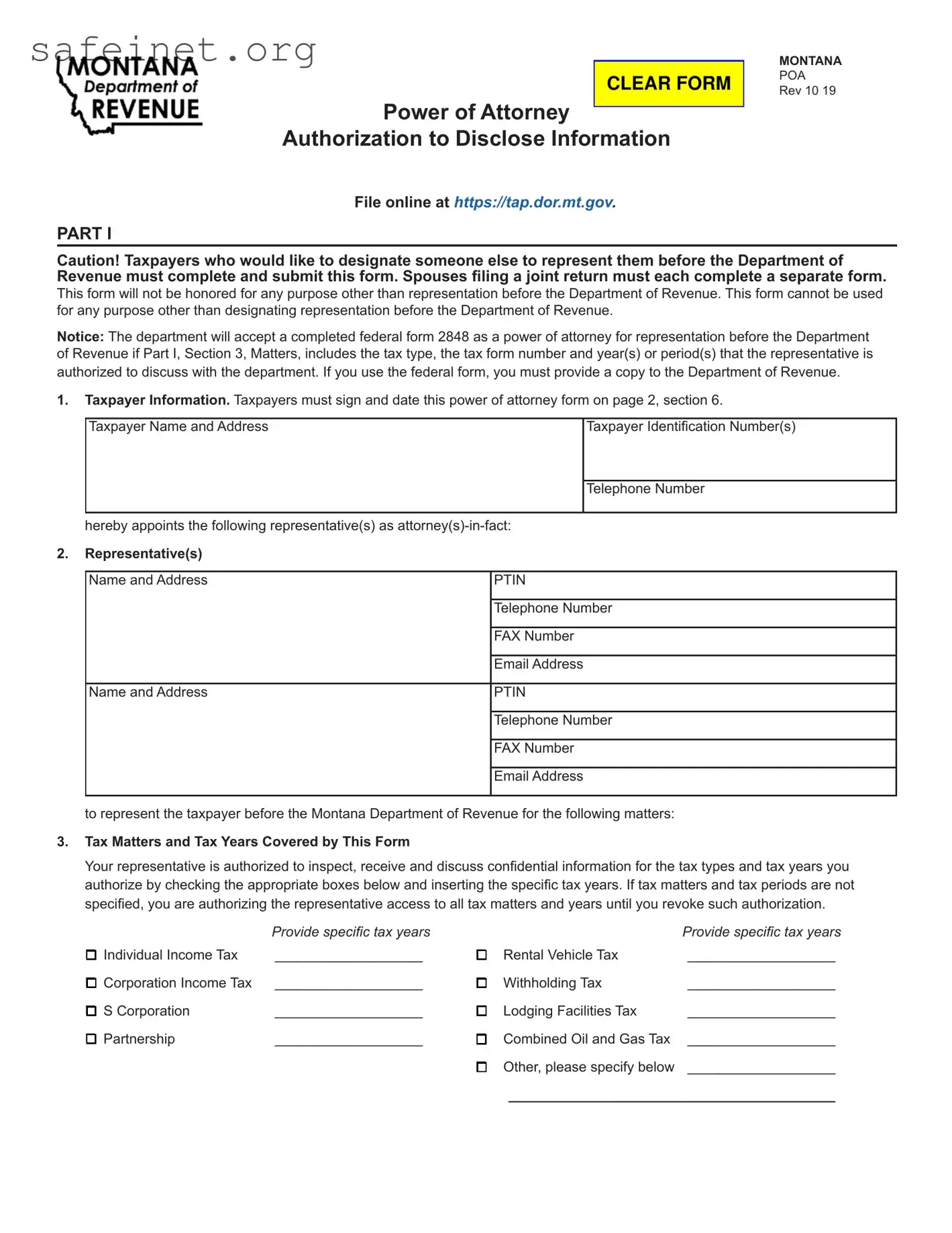

Power of Attorney

Authorization to Disclose Information

File online at https://tap.dor.mt.gov.

PART I

MONTANA POA Rev 10 19

Caution! Taxpayers who would like to designate someone else to represent them before the Department of Revenue must complete and submit this form. Spouses filing a joint return must each complete a separate form.

This form will not be honored for any purpose other than representation before the Department of Revenue. This form cannot be used for any purpose other than designating representation before the Department of Revenue.

Notice: The department will accept a completed federal form 2848 as a power of attorney for representation before the Department of Revenue if Part I, Section 3, Matters, includes the tax type, the tax form number and year(s) or period(s) that the representative is authorized to discuss with the department. If you use the federal form, you must provide a copy to the Department of Revenue.

1.Taxpayer Information. Taxpayers must sign and date this power of attorney form on page 2, section 6.

Taxpayer Name and Address

Taxpayer Identification Number(s)

Telephone Number

hereby appoints the following representative(s) as

2.Representative(s) Name and Address

Name and Address

PTIN

Telephone Number

FAX Number

Email Address

PTIN

Telephone Number

FAX Number

Email Address

to represent the taxpayer before the Montana Department of Revenue for the following matters:

3.Tax Matters and Tax Years Covered by This Form

Your representative is authorized to inspect, receive and discuss confidential information for the tax types and tax years you authorize by checking the appropriate boxes below and inserting the specific tax years. If tax matters and tax periods are not specified, you are authorizing the representative access to all tax matters and years until you revoke such authorization.

|

Provide specific tax years |

|

|

Provide specific tax years |

q Individual Income Tax |

___________________ |

q |

Rental Vehicle Tax |

___________________ |

q Corporation Income Tax |

___________________ |

q |

Withholding Tax |

___________________ |

q S Corporation |

___________________ |

q |

Lodging Facilities Tax |

___________________ |

q Partnership |

___________________ |

q Combined Oil and Gas Tax |

___________________ |

|

|

|

q Other, please specify below |

___________________ |

|

__________________________________________

4.Acts Authorized by This Form

Check the box that best describes what authorization you are delegating to your representative.

q Representation. Department employees can provide confidential information to the representative and discuss the information. q Information sharing. Department employees can provide confidential information to the representative, but cannot discuss

the information.

q

5.Revocation of Prior Power(s) of Attorney

q Check this box if you want all prior POAs revoked.

If you are a representative and want to withdraw an existing POA, write WITHDRAW across the top of the existing form. See instructions on page 3.

6.Signature of taxpayer. If a tax matter concerns a year in which a joint return was filed, the spouses each file a separate power of attorney even if the same representative(s) is(are) appointed. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, fiduciary or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form

on behalf of the taxpayer.

If not signed and dated, this power of attorney will not be in effect and the taxpayer will be notified.

_______________________________________ |

____________________ |

__________________________________ |

Signature |

Date |

Title (if applicable) |

_______________________________________ |

|

__________________________________ |

Print Name |

|

Print Taxpayer Name from Line 1 (if other |

|

|

than individual) |

PART II. Declaration of Representative

I declare that:

I am authorized to represent the taxpayer identified in Part I for the matter(s) specified there; and

I am one of the following:

a.Attorney - licensed to practice law in the jurisdiction shown below.

b.Certified Public Accountant - duly qualified to practice as a certified public accountant in the jurisdiction shown below.

c.Enrolled Agent or Licensed Public Accountant, etc.

d.Officer - a bona fide officer of the taxpayer’s organization.

e.Full time employee - a full time employee of the taxpayer.

f.Family member - a member of the taxpayer’s immediate family (for example, spouse, parent, child, grandparent,

g.Other

Representative Signature. See instructions on page 4.

Designation -

Insert Letter from

Above

Relationship to Taxpayer (see instructions for Part II)

Signature

Date

Filing this Form

►File Online on TransAction Portal at https://tap.dor.mt.gov.

►Fax to: (406)

Or, if you are already working with a department employee, fax your completed form to the number provided by that person.

►Mail the completed form to: Montana Department of Revenue 340 N. Last Chance Gulch

PO Box 5805

Helena, MT

2

Instructions for Power of Attorney

Authorization to Disclose Tax Information

Part I

Section 1. Taxpayer Information

Individual. Enter your name, personal address, social

security number (SSN), telephone number, individual taxpayer identification number (ITIN) and/or federal employee identification number (FEIN) if applicable. Do not use your representative’s address or post office box for your own. If you file a tax return that includes

a sole proprietorship business (federal Schedule C) and the matters for which you are authorizing the listed representative(s) to represent you include your individual and business tax matters, including employment tax liabilities, enter both your SSN (or ITIN) and your business

FEIN as your taxpayer identification numbers. If the tax

matter concerns a joint return, a separate power of attorney form is required for each spouse.

C Corporation, S corporations, partnership, limited

liability company or association. Enter the name, business address, federal employer identification number

(FEIN), and telephone number. If this form is being prepared for C corporations filing a combined tax return, a list of subsidiaries is not required. This power of attorney

applies to all members of the combined tax return.

Trust. Enter the name, title, address of the trustee, the name and FEIN of the trust and telephone number.

Estate. Enter the name of the decedent as well as the name, title and address of the decedent’s personal

representative. Enter the estate’s FEIN for the taxpayer identification number or, if the estate does not have an

FEIN, the decedent’s SSN (or ITIN).

Section 2. Authorization of Representative

Enter your representative’s full legal name. Use the identical full name on all submissions and correspondence.

Enter the representative’s telephone number, address or post office box and

If a trust, estate, guardianship or conservatorship wants an

individual other than the personal representative, trustee or other fiduciary to handle tax matters before the Department

of Revenue, the personal representative, trustee or other

fiduciary must complete this form and designate the

other individual with the power of attorney. Otherwise, the personal representative, trustee or other fiduciary has the requisite authority to handle tax matters before the

Department of Revenue and need not complete this form.

Section 3. Tax Matters and Tax Years Covered by the Form

Indicate, by checking the appropriate boxes, what tax types you are authorizing your representative to inspect, receive and discuss with the Department of Revenue.

You may list any tax years or periods that have already ended as of the date you sign the form.

If the matter relates to estate tax, enter the date of the

decedent’s death instead of a tax year.

If the tax matter and tax periods aren’t specified, you are authorizing the representative access to all tax matters and years until you revoke their authorization.

Section 4. Acts Authorized by This Form

If you are providing authorization to another individual, check one of the three boxes depending on what authorization you are providing to your representative. A disclosure authorized by this form may take place by telephone, letter, facsimile, email or a personal visit.

Note: If you check the “yes” box on the individual tax return next to the question “Do you want to allow another person

(third party designee) to discuss this return with us?” you

authorize Department of Revenue employees to discuss the tax return with the third party designee. They cannot

discuss any other issues, such as outstanding tax liabilities, without a completed power of attorney form.

Section 5. Revocation of Prior Power(s) of Attorney

Taxpayer Revocation. Check the box if you want all prior POAs revoked.

Revocation Withdraw by Representative. If you are a representative and want to revoke an existing POA, write REVOKE across the top of the form and submit the form as indicated on page 4.

Section 6. Signature

Individual. You must sign and date the form. If you file a joint return, your spouse must execute his or her own Montana power of attorney to designate a representative.

Corporation or association. An officer having authority to bind the corporation must sign.

Partnership. All partners must sign unless one partner is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if, under Montana law, the partner has authority to bind the partnership. If there is any doubt whether a partner has the authority to bind the partnership, it is best that all partners sign the form.

Limited Liability Company (LLC). If the LLC is member- managed, all members must sign, unless one member is authorized to act in the name of the LLC. If the LLC is

Estate, trust or other fiduciary. As discussed in Section 2, if a trust, estate, guardianship or conservatorship wants an

individual other than the personal representative, trustee or other fiduciary to handle tax matters before the Department

of Revenue, the personal representative, trustee or other

fiduciary must complete this form and designate the other individual with the power of attorney. Thus, the personal representative of an estate must sign. The trustee of a trust must sign. If a guardian or conservator has been appointed

3

for a taxpayer, the guardian or conservator must sign. In all cases, the fiduciary must include the representative capacity in which the fiduciary is signing, such as “John Doe, guardian of Jane Roe.”

Part II. Declaration of Representative

The representative(s) you name may sign and date the Declaration of Representative. Enter the applicable designation (items

a.Attorney – Enter the

b.Certified Public Accountant – Enter the

c.Enrolled Agent, Licensed Public Accountant, etc.

d.Officer – Enter the title of the officer (for example,

President, Vice President, Secretary, etc.).

e.

f.Family Member – Enter the relationship to the taxpayer (for example, spouse, parent, child, brother, sister, etc.).

g.Other – Identify the type of representative and enter a brief description of the representative’s relationship to the taxpayer.

Filing this Form

File Online on TransAction Portal at https://tap.dor.mt.gov.

Fax the completed form to (406)

Mail the completed form to:

Montana Department of Revenue

340 N. Last Chance Gulch

PO Box 5805

Helena, MT

Questions? Please call us at (406)

File online at https://tap.dor.mt.gov.

4

| Fact Name | Details |

|---|---|

| Purpose | The Tax Power of Attorney (POA) Authorization to Disclose Tax Information form allows individuals to designate a representative to access their tax information and communicate with the tax authorities on their behalf. |

| Eligibility | Any individual or entity, such as a business owner or an estate executor, may complete this form to authorize someone to act on their behalf regarding tax matters. |

| Governing Laws | This form is governed by federal tax laws, particularly the Internal Revenue Code, and any relevant state laws that apply, which may vary by jurisdiction. |

| Submission Process | Once completed, the form should be submitted to the appropriate tax authority, such as the IRS for federal matters, or the state department of revenue for state-specific issues. |

| Validity Duration | The authorization is typically valid until it is revoked by the taxpayer or until the tax matter for which it was granted is resolved. |

| Revocation | Taxpayers can revoke the authorization at any time. To do this, they should submit a notice to the tax authority indicating their intent to cancel the form. |

| Confidentiality | By completing this form, taxpayers grant their representatives access to their tax information. Therefore, it is essential to choose a trusted individual who can safeguard personal information. |

Filling out the Tax POA Authorization to Disclose Tax Information form is an important step for anyone needing to designate someone else to discuss or manage their tax matters. Following the steps provided will help ensure that your form is accurate and complete, which can facilitate a smooth process with the IRS.

After submitting the form, it's important to keep a copy for your records. Following up with the IRS to confirm that your authorization has been processed can also provide peace of mind. Remember, maintaining open communication with your designated representative is key to ensuring that your tax matters are handled efficiently.

What is the Tax POA Authorization to Disclose Tax Information form?

The Tax POA Authorization to Disclose Tax Information form is a legal document that allows an individual, referred to as the taxpayer, to authorize another person, known as the representative, to access their tax information. This form is often necessary for those who need assistance managing their tax affairs or who require representation before the Internal Revenue Service (IRS). It facilitates communication between the taxpayer and the IRS, ensuring that the designated representative can obtain relevant tax details on behalf of the taxpayer.

Who can be designated as a representative on this form?

Typically, any qualified individual can be designated as a representative on the Tax POA form. This includes tax professionals like certified public accountants (CPAs), attorneys, or enrolled agents. It is essential that the chosen representative is capable of handling tax-related matters and has the taxpayer's best interests in mind. The taxpayer should choose someone they trust to manage their tax information effectively.

How does one complete the Tax POA Authorization to Disclose Tax Information form?

Completing the form requires the taxpayer to provide certain personal information, such as their name, address, and Social Security number. Next, the representative's details must be included. The form typically requires a signature from the taxpayer, confirming their consent. After filling it out, the taxpayer should review all sections for accuracy and clarity before submitting it to the IRS. It is advisable to keep a copy for personal records.

Can the authorization be revoked once submitted?

Yes, the authorization can be revoked at any time by submitting a written statement to the IRS. This statement should clearly indicate the taxpayer’s intention to revoke prior authorization and must include identifying information about both the taxpayer and the previously authorized representative. Revocation is effective as soon as the IRS processes the request, ensuring that future tax information cannot be shared with the revoked representative.

Is there a limit to how much tax information a representative can access?

Generally, the Tax POA form allows the representative to access all tax information related to the taxpayer's federal tax accounts. However, the taxpayer can specify limitations on the type of information or the scope of the authorization within the document. Defining these boundaries is crucial for those who wish to maintain control over specific details of their tax situation.

How long is the Tax POA Authorization to Disclose Tax Information form valid?

The form remains valid until the taxpayer cancels the authorization, the IRS processes a written revocation, or upon the death of the taxpayer. It is also advisable to regularly review the necessity and relevance of the authorization, especially if there are significant changes in the taxpayer's circumstances or relationship with the representative. Keeping the authorization current helps ensure that tax matters are handled efficiently and legally.

Incorrect Information Entry: Many individuals fail to provide accurate personal information. This includes errors in name, Social Security number, or address. It's crucial that every detail matches the IRS records to avoid delays.

Missing Signatures: A common oversight is forgetting to sign the form. The IRS requires the taxpayer's signature for validation. Without it, the form will be considered incomplete.

Choosing the Wrong Representative: Sometimes, taxpayers authorize someone who is not eligible to represent them. Ensure the appointed individual is a recognized tax professional or meets other IRS requirements.

Not Specifying the Scope: Individuals often neglect to define the specific rights granted to the representative. Clearly stating what information can be disclosed prevents misunderstandings later.

Failure to Update Authorization: Life changes, and so do circumstances. Taxpayers frequently forget to update their POA form, leaving outdated representatives with access to their tax information.

When dealing with tax matters, it's common to encounter various forms and documents that work alongside the Tax POA Authorization to Disclose Tax Information form. Understanding these additional documents can streamline the process and ensure that all requirements are met effectively. Below are a few key forms that may be used in conjunction with the Tax POA.

Utilizing these documents appropriately can facilitate smoother communication with tax authorities and ensure that tax affairs are handled comprehensively. Each form serves a specific purpose, making it essential to choose the right one based on individual needs.

The IRS Form 2848, often referred to as the Power of Attorney (POA) form, is closely related to the Tax POA Authorization to Disclose Tax Information form. Both documents allow individuals to designate a representative who can act on their behalf in tax matters. This form grants permission to the representative to communicate with the IRS, receive information about the taxpayer's accounts, and represent the taxpayer in discussions about tax issues. Ultimately, both forms aim to facilitate better communication between the IRS and a taxpayer's appointed representative.

Another relevant document is IRS Form 8821, which is known as the Tax Information Authorization form. Similar to the Tax POA form, Form 8821 permits taxpayers to authorize another individual or organization to receive and review their tax information. However, the significant difference lies in the lack of representation authority; Form 8821 does not allow the designated individual to represent the taxpayer before the IRS, making it suitable for situations where taxpayers simply want to disclose tax information without granting broader powers.

The Durable Power of Attorney form serves a different but related purpose. This legal document allows individuals to grant someone the authority to make decisions on their behalf, which can include financial and tax-related decisions. While a Tax POA focuses specifically on tax matters, a Durable Power of Attorney can cover a wider scope, including healthcare and estate decisions, allowing for broader representation beyond just tax issues.

The Advance Health Care Directive, while primarily used for healthcare decisions, shares similarities with the Tax POA in the context of granting authority. Both documents allow individuals to appoint someone to make decisions on their behalf when they are unable to do so. The key difference lies in the subject matter, as the Health Care Directive pertains strictly to medical situations, whereas the Tax POA deals with financial and tax-related affairs.

An Authorization for Release of Information form is often used in various contexts but has parallels with the Tax POA. This form allows individuals to approve the release of personal or sensitive information to a designated third party, which can include information related to taxes. However, unlike the Tax POA form, this document does not simplify any communication or negotiation issues with a financial institution or tax authority.

Form 1065, the Partnership Return of Income, relates to tax disclosures within partnerships. While it serves a different function, it requires the disclosure of sensitive tax information to the IRS. Tax POAs can be used by the partners of a partnership to appoint someone to manage tax matters, reflecting a collaborative effort in handling taxation but focusing on individual rather than organizational tax authority.

The Medicaid Application also ties into the topic of tax authorization documents through its need to disclose financial information. Individuals often need to grant someone permission to access their financial records as part of the Medicaid application process. While the focus here shifts to healthcare eligibility, the underlying idea of authorizing access to financial information remains a connection between these documents.

Finally, the Form 4506-T is used to request tax returns or tax information from the IRS. Similar to the Tax POA, this form allows a designated individual to request important tax records on behalf of someone else. The fundamental difference lies in the nature of authority; the Tax POA authorizes representation while Form 4506-T focuses simply on obtaining information necessary for financial or legal purposes.

When filling out the Tax POA Authorization to Disclose Tax Information form, it’s important to be mindful of certain practices that can either help or hinder your process. Below are some essential dos and don’ts.

Things You Should Do:

Things You Shouldn't Do:

Understanding the Tax POA Authorization to Disclose Tax Information form can be challenging. Here are 9 common misconceptions about this important document.

Knowing the facts about the Tax POA Authorization to Disclose Tax Information form helps ensure proper handling and authorization of tax matters.

When filling out the Tax POA Authorization to Disclose Tax Information form, consider the following key takeaways:

By following these takeaways, you can effectively manage the process of authorizing someone to discuss your tax information.