The Tax POA 774 form plays a crucial role in streamlining the communication between taxpayers and the IRS. This form, designed for individuals seeking to appoint a representative to act on their behalf, simplifies complex matters often associated with tax issues. By filling out this form, taxpayers authorize designated individuals, such as attorneys or accountants, to receive sensitive tax information and manage their tax affairs. This capability is particularly important when dealing with audits, disputes, or other sensitive interactions that necessitate expert guidance. Additionally, the POA 774 form ensures confidentiality and compliance, providing peace of mind for those navigating the tax system. Understanding this form not only helps in securing reliable representation but also empowers individuals to make informed decisions about their tax obligations and rights.

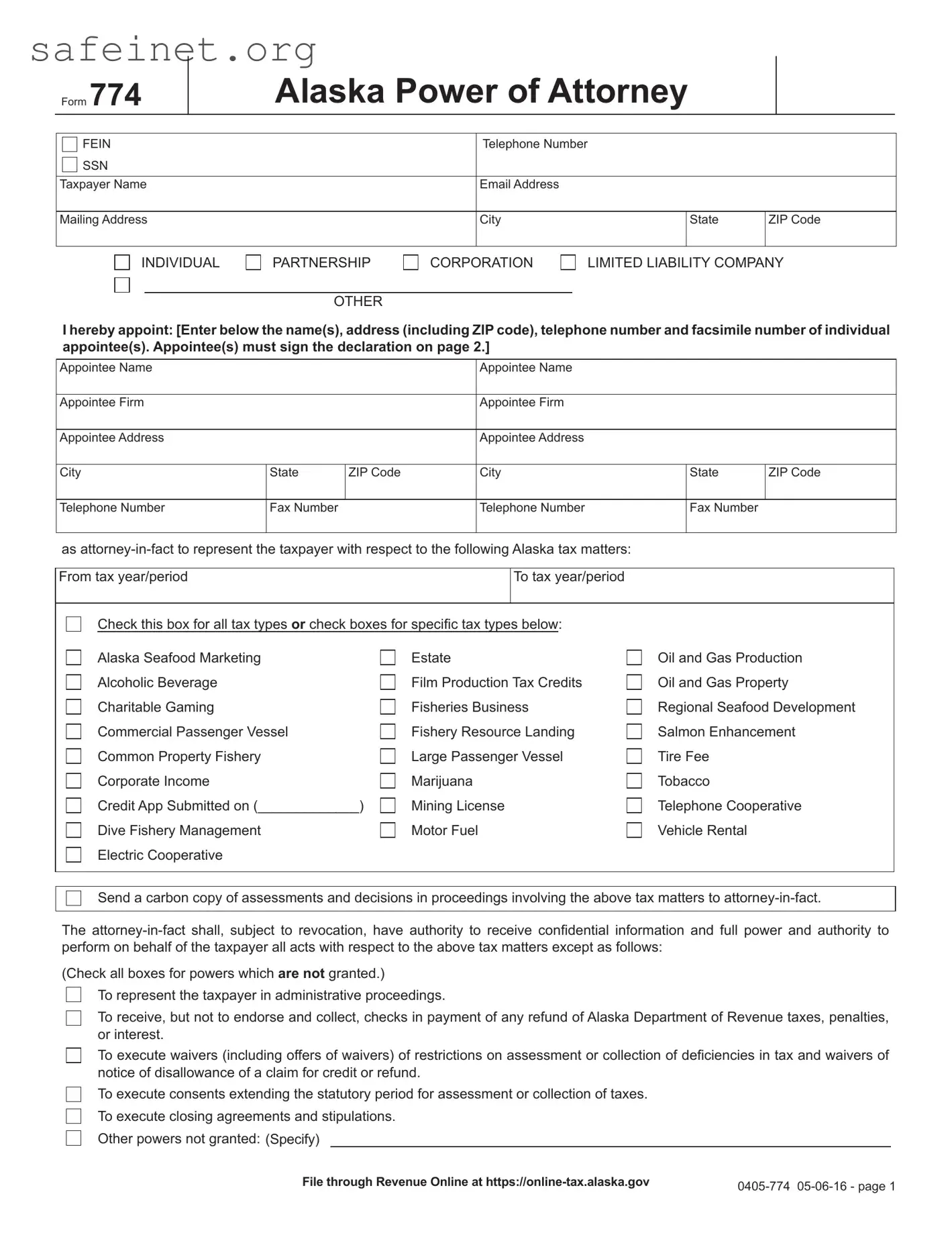

Form 774

Alaska Power of Attorney

FEIN |

Telephone Number |

|

|

SSN |

|

|

|

|

|

|

|

Taxpayer Name |

Email Address |

|

|

|

|

|

|

Mailing Address |

City |

State |

ZIP Code |

|

|

|

|

INDIVIDUAL

PARTNERSHIP

OTHER

CORPORATION

LIMITED LIABILITY COMPANY

I hereby appoint: [Enter below the name(s), address (including ZIP code), telephone number and facsimile number of individual appointee(s). Appointee(s) must sign the declaration on page 2.]

Appointee Name |

|

|

Appointee Name |

|

|

Appointee Firm |

|

|

Appointee Firm |

|

|

Appointee Address |

|

|

Appointee Address |

|

|

City |

State |

ZIP Code |

City |

State |

ZIP Code |

Telephone Number |

Fax Number |

|

Telephone Number |

Fax Number |

|

as

From tax year/period |

|

To tax year/period |

|

|

|

|

|

Check this box for all tax types or check boxes for specific tax types below: |

|

||

Alaska Seafood Marketing |

Estate |

Oil and Gas Production |

|

Alcoholic Beverage |

Film Production Tax Credits |

Oil and Gas Property |

|

Charitable Gaming |

Fisheries Business |

Regional Seafood Development |

|

Commercial Passenger Vessel |

Fishery Resource Landing |

Salmon Enhancement |

|

Common Property Fishery |

Large Passenger Vessel |

Tire Fee |

|

Corporate Income |

Marijuana |

Tobacco |

|

Credit App Submitted on (_____________) |

Mining License |

Telephone Cooperative |

|

Dive Fishery Management |

Motor Fuel |

Vehicle Rental |

|

Electric Cooperative |

|

|

|

|

|

|

|

Send a carbon copy of assessments and decisions in proceedings involving the above tax matters to

The

(Check all boxes for powers which are not granted.)

To represent the taxpayer in administrative proceedings.

To receive, but not to endorse and collect, checks in payment of any refund of Alaska Department of Revenue taxes, penalties, or interest.

To execute waivers (including offers of waivers) of restrictions on assessment or collection of deficiencies in tax and waivers of notice of disallowance of a claim for credit or refund.

To execute consents extending the statutory period for assessment or collection of taxes.

To execute closing agreements and stipulations.

Other powers not granted: (Specify)

File through Revenue Online at |

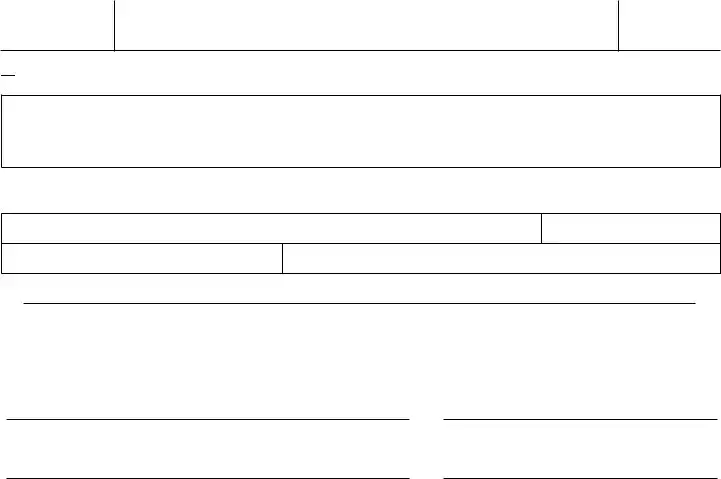

Form 774

Alaska Power of Attorney

This power of attorney revokes all prior powers of attorney filed with respect to the same matters and years or periods covered by this instrument, except the following: (Specify and attach copies of the powers of attorney)

This power of attorney revokes all prior powers of attorney filed with respect to the same matters and years or periods covered by this instrument, except the following: (Specify and attach copies of the powers of attorney)

Signature of Taxpayer – If signed by a corporate officer, partner, or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney on behalf of the taxpayer.

Signature |

Date |

Printed Name |

Printed Title |

DECLARATION OF REPRESENTATIVE

The undersigned representative hereby declares under the penalty of unsworn falsification that he/she is an individual authorized to represent a taxpayer before the Department of Revenue and that he/she is authorized to represent the named taxpayer in this matter.

Signature |

Date |

Signature |

Date |

POWER OF ATTORNEY INFORMATION

USE THIS FORM TO GRANT AUTHORITY TO AN INDIVIDUAL TO REPRESENT YOU BEFORE THE DEPARTMENT AND TO RECEIVE TAX INFORMATION.

An individual who is not the taxpayer must be a recognized representative before the individual may represent a taxpayer before the Department of Revenue. A recognized representative is an individual who is appointed as an

A power of attorney is a document signed by the taxpayer by which another individual is given the authority to appear before the department and act for the taxpayer. An

Generally, the power of attorney encompasses all matters relating to a taxpayer’s rights, privileges, or liabilities under laws and regulations administered by the department. This includes, for example, such things as the preparation and filing of necessary documents, receipt of otherwise confidential tax particulars, correspondence and communication with department personnel, and representation of a taxpayer at audits, conferences, hearing, and other meetings.

Forms filed through Revenue Online are considered original forms and do not need to be mailed in. The original of this form, if not filed through Revenue Online, must be mailed to the department.

| Fact Name | Details |

|---|---|

| Form Purpose | The Tax POA 774 form is used to authorize a representative to act on behalf of a taxpayer regarding tax matters. |

| Governing Law | This form is governed by the Internal Revenue Code and is aligned with the regulations set by the Internal Revenue Service (IRS). |

| Who Can Use It? | Taxpayers, including individuals and businesses, can use the form to appoint an authorized representative. |

| Required Information | The form requires the taxpayer's name, address, Social Security number or Employer Identification Number, and the representative's details. |

| Submission Process | Taxpayers must complete the form and submit it to the IRS or state tax agency, depending on their location. |

| Validity Period | Once submitted, the authorization remains valid until revoked by the taxpayer or a specific expiration date is indicated. |

| Benefits of Using It | Using the Tax POA 774 form allows the appointed representative to receive confidential tax information and represent the taxpayer before the IRS. |

After obtaining the Tax POA 774 form, you will need to complete it carefully to ensure it meets all necessary requirements. This form will allow you to designate someone to act on your behalf regarding certain tax matters. Follow the steps below to fill it out correctly.

What is the Tax POA 774 form?

The Tax POA 774 form, also known as the Power of Attorney for Tax Matters, allows you to authorize someone else to represent you before the IRS or state tax authorities. It is crucial for delegating tax responsibilities while ensuring that your interests are handled professionally.

Who should use the Tax POA 774 form?

This form is beneficial for individuals or business owners who need to appoint a trusted representative, such as an accountant or tax attorney, to manage tax-related issues. If you find the tax process overwhelming or simply want expert assistance, using this form is a good choice.

How do I fill out the Tax POA 774 form?

Filling out the Tax POA 774 form involves providing your personal information, the details of your representative, and any specific tax matters that your representative will handle. It's essential to ensure all the information is accurate. Clear and complete details will help avoid delays in processing.

Can I revoke the Tax POA 774 form once it's filed?

Yes, you have the right to revoke the Tax POA 774 form at any time. If you decide to revoke it, you need to submit a written statement to inform the IRS or state tax authorities. This statement should include your name, the name of your representative, and a clear statement of revocation.

Do I need to submit the Tax POA 774 form to the IRS?

Yes, you must submit the form to the IRS if you want your representative to act on your behalf regarding federal tax matters. For state tax authorities, you should check their specific requirements, as they might have different submission guidelines.

How long does it take for the Tax POA 774 form to be processed?

Processing times can vary depending on the IRS or state agency workload. Generally, it can take up to four to six weeks to process. If you need fast action, consider following up with the agency after submitting the form.

Is there a fee to file the Tax POA 774 form?

There is no fee associated with filing the Tax POA 774 form itself. However, if you are hiring a professional to assist you, they might charge a fee for their services. Always clarify any potential costs upfront.

What if my representative needs to sign documents on my behalf?

Your authorized representative can sign documents related to the tax matters specified in the Tax POA 774 form. Make sure that the form includes the specific tax years and types of tax issues you are allowing them to address. This ensures they can act without needing additional approval for each transaction.

Can I use the Tax POA 774 form for state taxes?

Yes, the Tax POA 774 form can be used for both federal and state tax matters, but you should verify if the state tax authority requires a specific format or additional documentation. Each state may have different rules regarding power of attorney forms.

When individuals fill out the Tax Power of Attorney (POA) 774 form, mistakes can lead to delays or even rejections. Here are four common errors to watch out for:

Incorrect or Incomplete Information: It’s crucial to provide accurate details on the form. Mistakes in names, Social Security numbers, or addresses can cause significant issues. Ensure every box is filled out completely.

Failure to Sign the Form: Many people overlook the importance of their signature on the POA form. Without it, the IRS will not process the request, and your tax representative will not have the authority to act on your behalf.

Not Specifying the Scope of Authority: When filling out the POA form, it's essential to clearly define what powers you are granting to your representative. Leaving this section vague can lead to misunderstandings down the road.

Ignoring State-Specific Requirements: While the form is a federal document, some states have additional requirements for POA forms. Be sure to check whether your state has any specific stipulations that might apply to your situation.

By being aware of these common pitfalls, you can ensure that your Tax POA 774 form is filled out correctly and efficiently, smoothing the path for your tax representative to assist you.

The Tax Power of Attorney (POA) Form 774 is an essential document that allows a designated individual to act on behalf of someone else in tax-related matters. In addition to this form, a few other documents are commonly used in conjunction to ensure a smooth handling of tax issues. The following list outlines some of these frequently associated forms and documents.

Each of these documents serves a specific purpose and contributes to managing tax matters effectively. Understanding the roles of these forms can simplify the process of dealing with tax issues and ensure that individuals receive the proper assistance and representation as needed.

The IRS Form 2848, officially known as the Power of Attorney and Declaration of Representative, is similar to the Tax POA 774 form. Both documents grant an individual the authority to represent a taxpayer before the IRS. However, Form 2848 is more broadly applicable, allowing representatives to act on behalf of a taxpayer for various tax matters. It requires specific information about the taxpayer and the representative, including their Tax Identification Numbers, to ensure proper identification and authorization.

Another related document is the IRS Form 8821, which serves as a Tax Information Authorization. Unlike the Tax POA 774 form, Form 8821 only gives the authorized person access to the taxpayer's information. This means the representative can review the taxpayer's records but lacks the authority to act on the taxpayer's behalf. This document is often used when taxpayers want to allow someone to access their tax information without granting full power of attorney.

The Department of Justice’s Form A and Form B are also relevant. These forms are used for federal tax issues where individual taxpayers grant legal authority to specific attorneys. Both forms serve a similar function as the Tax POA 774 by enabling the authorized attorney to handle tax matters. However, Form A and Form B are specific to legal representation in federal tax disputes, while the Tax POA 774 may pertain to various tax-related matters within a local jurisdiction.

The Medicaid Authorization Form is another parallel document. This form allows individuals to appoint a representative to conduct business related to their Medicaid application. Like the Tax POA 774, it provides a formal way for taxpayers to authorize someone to act on their behalf. However, Medicaid forms concern healthcare and state assistance programs, while the Tax POA 774 is specifically about tax matters.

The Durable Power of Attorney is further comparable. This document can grant authority for handling various financial matters, including tax issues, even if the principal becomes incapacitated. While both documents enable representation, the Durable Power of Attorney has broader applications beyond tax concerns, covering areas such as real estate and financial investments.

The Medical Power of Attorney, though focused on healthcare decisions, mirrors the Tax POA 774's essential function of granting decision-making authority to another individual. This type of document allows someone to make medical decisions for another person and is activated when that person is unable to do so. While one is concerned with health matters, the underlying principle of representation is consistent.

The Corporate Resolution to Act is pertinent for businesses and can function similarly to the Tax POA 774 for corporate tax situations. This document allows corporate officers to designate individuals who can represent the company in dealings with tax authorities. The Tax POA 774 offers a similar capacity for individuals, facilitating their representation in tax matters.

Lastly, the IRS Form 706 is relevant for estate tax matters. This form, while primarily used to report and calculate estate taxes, often requires the involvement of a representative with authority to act in the estate's interests. Like the Tax POA 774, it concerns tax obligations, though it is specific to estate matters rather than individual taxation.

When filling out the Tax POA 774 form, it is essential to proceed with care to ensure accuracy and compliance. Here are some helpful guidelines on what to do and what to avoid:

Misconception 1: The Tax POA 774 form is only for business entities.

This form can be used by both individuals and businesses. It’s designed to grant authority to a representative for tax matters, regardless of the entity type.

Misconception 2: The form needs to be filed with every tax return.

Only file the Tax POA 774 form when you want to appoint someone to represent you. You don’t need to submit it with each tax return.

Misconception 3: A Power of Attorney is permanent and cannot be revoked.

The authority granted via this form can be revoked at any time. It simply requires notifying the IRS of the revocation.

Misconception 4: You must provide personal financial information on the form.

No personal or financial details are required on the Tax POA 774 form itself. The focus is on the appointment of your representative.

Misconception 5: You cannot change your representative after filing.

You can modify your choice of representative easily by submitting a new POA form. Changes can be made as often as needed.

Misconception 6: The IRS requires notarization of the form.

Notarization is not necessary for the Tax POA 774 form. Simply signing it will suffice to grant authority to your representative.

Misconception 7: A lawyer must complete the form on your behalf.

While many people choose to seek legal advice, you can complete the form yourself. It’s intended to be user-friendly for anyone to fill out.

Misconception 8: The form limits the representative's authority only to tax issues.

The authority outlined in the Tax POA 774 form applies specifically to tax matters, but it can encompass a range of related issues. Clarity on your intentions will help define the limits of the authority granted.

The Tax POA 774 form, which is used to authorize someone to act on your behalf for tax matters, is important for simplifying interactions with the IRS. Here are key takeaways to keep in mind when filling it out and using it:

Understanding these points can make the process smoother and ensure you effectively delegate your tax matters.