The Tax POA 500 form plays a crucial role in the process of appointing an authorized representative to act on behalf of a taxpayer during interactions with the Illinois Department of Revenue. Designed to streamline communications between taxpayers and the state, this form simplifies the authorization process for individuals seeking assistance with tax matters. It allows designated representatives, such as attorneys or tax professionals, to receive confidential information and discuss tax-related issues directly with tax authorities. By completing and submitting the form, taxpayers ensure legal representation and facilitate a more efficient resolution of tax concerns. Additionally, the form requires essential details, including the taxpayer's information and the chosen representative’s credentials, which helps establish clear lines of communication. Understanding the nuances of the Tax POA 500 form can significantly benefit those navigating the complexities of tax compliance and representation.

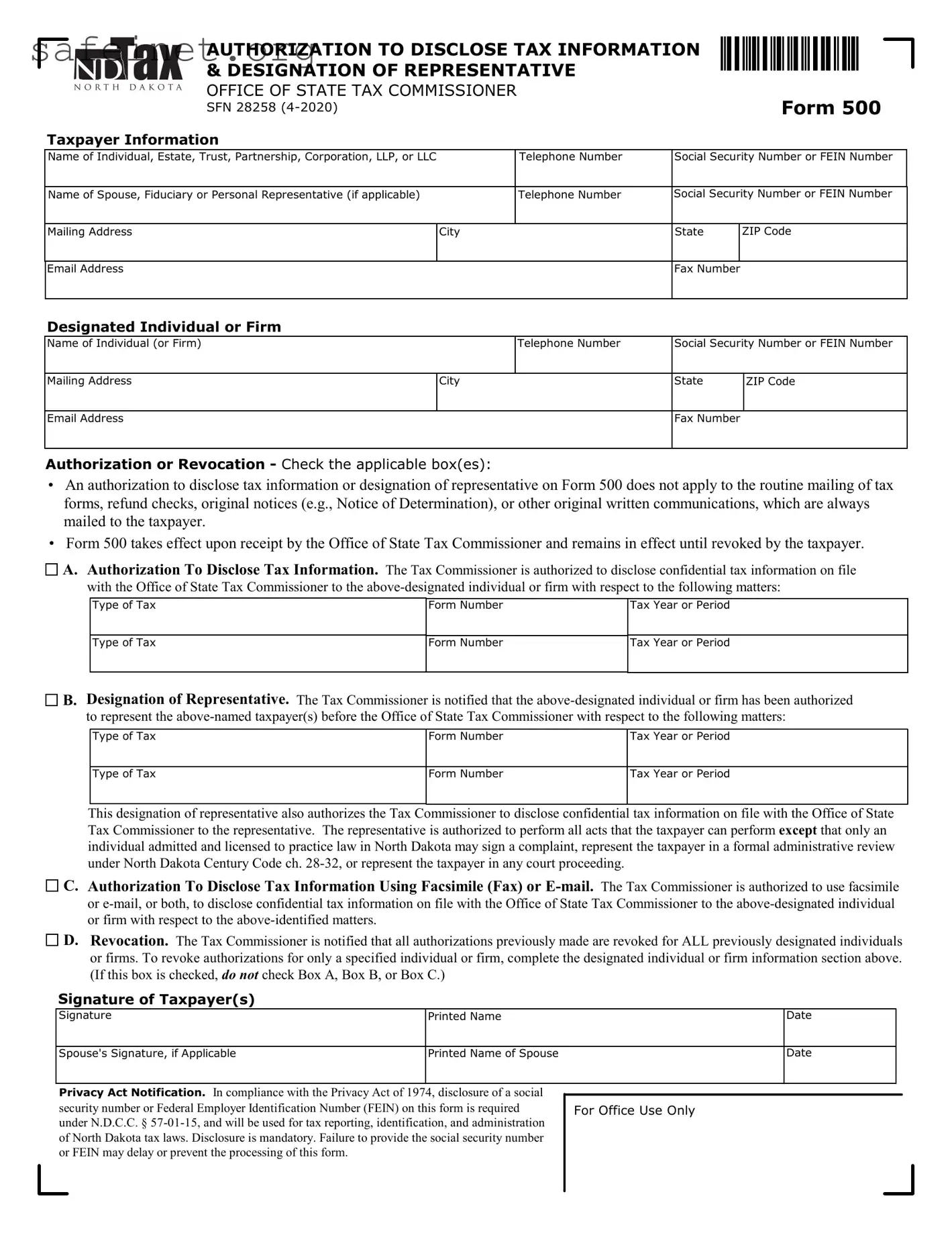

1,~.,ax AUTHORIZATION TO DISCLOSE TAX INFORMATION

&DESIGNATION OF REPRESENTATIVE

NORTH DAKOTA OFFICE OF STATE TAX COMMISSIONER

SFN 28258

Taxpayer Information

Ill

I

I

IIIII

IIIII

I

I

llll

llll

111111111111111

111111111111111

7

7

Form 500

Name of Individual, Estate, Trust, Partnership, Corporation, LLP, or LLC |

Telephone Number |

Social Security Number or FEIN Number |

|||

|

|

|

|

|

|

Name of Spouse, Fiduciary or Personal Representative (if applicable) |

|

Telephone Number |

Social Security Number or FEIN Number |

||

|

|

|

|

|

|

Mailing Address |

City |

|

State |

|

ZIP Code |

|

I |

|

|

I |

|

Email Address |

|

|

Fax Number |

|

|

|

|

|

|

|

|

Designated Individual or Firm |

|

|

|

|

|

Name of Individual (or Firm) |

|

Telephone Number |

Social Security Number or FEIN Number |

||

|

|

I |

|

|

|

Mailing Address |

City |

|

State |

ZIP Code |

|

|

I |

|

|

|

I |

Email Address |

|

|

Fax Number |

|

|

|

|

|

|

|

|

Authorization or Revocation - Check the applicable box(es):

•An authorization to disclose tax information or designation of representative on Form 500 does not apply to the routine mailing of tax forms, refund checks, original notices (e.g., Notice of Determination), or other original written communications, which are always mailed to the taxpayer.

•Form 500 takes effect upon receipt by the Office of State Tax Commissioner and remains in effect until revoked by the taxpayer.

□

A. Authorization To Disclose Tax Information. The Tax Commissioner is authorized to disclose confidential tax information on file with the Office of State Tax Commissioner to the

A. Authorization To Disclose Tax Information. The Tax Commissioner is authorized to disclose confidential tax information on file with the Office of State Tax Commissioner to the

Type of Tax

Form Number

Tax Year or Period

Type of Tax

Form Number

Tax Year or Period

□

B. Designation of Representative. The Tax Commissioner is notified that the

B. Designation of Representative. The Tax Commissioner is notified that the

Type of Tax |

Form Number |

Tax Year or Period |

Type of Tax |

Form Number |

Tax Year or Period |

This designation of representative also authorizes the Tax Commissioner to disclose confidential tax information on file with the Office of State Tax Commissioner to the representative. The representative is authorized to perform all acts that the taxpayer can perform except that only an individual admitted and licensed to practice law in North Dakota may sign a complaint, represent the taxpayer in a formal administrative review under North Dakota Century Code ch.

□

C. Authorization To Disclose Tax Information Using Facsimile (Fax) or

C. Authorization To Disclose Tax Information Using Facsimile (Fax) or

□

D. Revocation. The Tax Commissioner is notified that all authorizations previously made are revoked for ALL previously designated individuals or firms. To revoke authorizations for only a specified individual or firm, complete the designated individual or firm information section above. (If this box is checked, do not check Box A, Box B, or Box C.)

D. Revocation. The Tax Commissioner is notified that all authorizations previously made are revoked for ALL previously designated individuals or firms. To revoke authorizations for only a specified individual or firm, complete the designated individual or firm information section above. (If this box is checked, do not check Box A, Box B, or Box C.)

Signature of Taxpayer(s)

Signature |

Printed Name |

Date |

|

|

|

|

|

Spouse's Signature, if Applicable |

Printed Name of Spouse |

Date |

|

|

|

|

Privacy Act Notification. In compliance with the Privacy Act of 1974, disclosure of a social security number or Federal Employer Identification Number (FEIN) on this form is required under N.D.C.C. §

L

For Office Use Only

_J

Form 500 Instructions

SFN 28258

General Instructions

Form 500 may be used by a taxpayer to do one of the following:

Authorize the North Dakota Office of State Tax Commissioner to disclose the taxpayer’s confidential tax information to another individual or firm not otherwise entitled to the information.

Designate another individual or firm to represent or act on behalf of the taxpayer before the Office of State Tax Commissioner, and to authorize the North Dakota Office of State Tax Commissioner to disclose the taxpayer’s confidential tax information to the designated representative or firm.

Form 500 does not apply to the routine mailing of tax forms, refund checks, original notices (e.g., a Notice of Determination), or other original written communications, which are always mailed to the taxpayer.

Unless Box C on Form 500 is checked to authorize the sending of confidential tax information by facsimile (fax) transmission or email, the Office of State Tax Commissioner will send confidential tax information authorized by Form 500 to the designated individual or firm only by letter or telephone.

Changing a previously filed Form 500. To change a Form 500 previously filed with respect to a particular designated individual or firm, complete and file

a new Form 500 for that designated individual or firm. The new Form 500 automatically revokes and replaces the previously filed Form(s) 500.

Revoking a previously filed Form 500. To revoke a previously filed Form 500, see instructions to Box D under “Authorization or Revocation.”

When Form 500 takes effect. Form 500 takes effect upon receipt by the Office of State Tax Commissioner and remains in effect until revoked by the taxpayer.

Specific Instructions

Taxpayer Information

Enter the taxpayer’s name, social security number or federal employer identification number (FEIN), mailing address, and contact information.

For a trust, enter the trust’s name and FEIN, and the name, mailing address, and contact information of the fiduciary.

For an estate, enter the decedent’s name and social security number, and the name, mailing address, and contact information of the decedent’s personal representative or fiduciary.

Designated Individual or Firm

Enter the name, social security number or federal employer identification number (FEIN), mailing address, and contact information for the designated individual or firm. If designating more than one individual or firm, attach a statement listing each one.

Note: Do not complete this section of the form if filing this form to revoke previously filed Forms 500 and the revocation is intended to apply to all previously designated individuals and firms.

Authorization or Revocation

For Box A and Box B, the authorization to disclose or the designation of representative can be limited to a certain tax type (e.g., individual income tax or sales tax), form number, or taxable year or period by entering that information in the spaces provided.

If attaching a statement to identify additional designated individuals or firms, indicate the authority being given to each one by entering “Box A” or “Box B” (and “Box C” if desired) next to each one listed on the statement.

Box A - Check this box to authorize the Office of State Tax Commissioner to disclose confidential tax information to the designated individual or firm.

Box B - Check this box to designate an individual or firm to represent or act on behalf of the taxpayer before the Office of

State Tax Commissioner, and to authorize the Office of State Tax Commissioner to disclose confidential tax information to the designated individual or firm.

Box C - Check this box to authorize the Office of State Tax Commissioner to send confidential tax information to the designated individual or firm by facsimile (fax) transmission or email.

Box D - Check this box to revoke all previously filed Forms 500. To limit the revocation to a specific designated individual or firm, identify that individual or firm by completing the “Designated Individual or Firm” section of the form. Otherwise, leave that section of the form blank to apply the revocation to all previously designated individuals and firms. If checking this box, do not check any of the other boxes (A, B, or C) on the form.

Signature of Taxpayer(s)

Partnership (all types). One of the general partners must sign.

Corporation. An officer having authority to bind the corporation must sign.

Limited liability company. A governor or manager must sign.

Estate, trust, or any other situation where there is a fiduciary relationship. The personal representative, trustee, guardian, conservator, or other fiduciary must sign.

Where to Send Form 500

Form 500 may be submitted to the North Dakota Office of State Tax Commissioner by fax, email, or regular mail.

Fax or email

Income & Withholding Taxes—

Fax701.328.1942

Email [email protected]

Business Registration—

Fax701.328.0332

Email [email protected]

General (other tax or purpose)—

Fax701.328.3700

Email[email protected]

Regular mail

Office of State Tax Commissioner

600 E. Boulevard Ave., Dept. 127

Bismarck, ND

| Fact Name | Description |

|---|---|

| Form Purpose | The Tax POA 500 form is used to authorize a representative to act on behalf of a taxpayer concerning tax matters. |

| Governing Law | This form is governed under the Internal Revenue Code, along with applicable state tax laws. |

| Eligibility | Any individual or entity can use this form, provided they have a legitimate interest or need for representation. |

| Filing Process | The form must be completed and submitted to the appropriate tax authority before representation becomes effective. |

| Revocation | Taxpayers can revoke the form at any time, but must notify the representative and the tax authority in writing. |

| Duration | The authorization remains in effect until revoked, or until the issue for which it was granted has been resolved. |

| Required Information | Form requires taxpayer details, representative information, and specific tax matters for which representation is authorized. |

| Submission Methods | The form can typically be submitted through mail, online portals, or sometimes in-person at tax offices. |

| State Variations | States may have variations of this form; ensure to check local tax authority requirements for specifics. |

| Confidentiality | Submitting the form grants the representative access to sensitive tax information, highlighting the importance of trust. |

Completing the Tax POA 500 form is an important step to manage tax matters efficiently. After filling out the form, you will need to submit it to the appropriate tax authority. This process enables you to designate a representative who can act on your behalf regarding tax issues.

What is the Tax POA 500 form used for?

The Tax POA 500 form is a Power of Attorney document utilized by taxpayers in the United States. It allows an individual or an entity to designate another person, usually a tax professional, to represent them before the Internal Revenue Service (IRS) or state tax authorities. This representation includes the ability to discuss tax matters, receive confidential information, and make decisions on behalf of the taxpayer regarding tax-related issues.

Who can I appoint using the Tax POA 500 form?

Taxpayers can appoint any individual qualified to represent them before the IRS. This may include certified public accountants (CPAs), enrolled agents, and tax attorneys. It is essential to choose someone who understands tax laws and regulations, as they will act on your behalf in all communications with tax authorities.

How do I complete the Tax POA 500 form?

Completing the Tax POA 500 form involves filling out key details such as the taxpayer's name, address, and Social Security number or EIN. The appointee's information, including their name and contact details, also must be provided. Finally, both the taxpayer and the designated representative must sign the form to validate it. Ensuring all information is accurate and complete is crucial to avoid delays in processing.

How long is the Tax POA 500 form valid?

The Tax POA 500 form remains valid until the taxpayer revokes it, the IRS processes a new Power of Attorney, or the appointed representative withdraws from their representation. If a taxpayer has ongoing tax matters, it is advisable to regularly review and confirm the continued validity of the Power of Attorney.

Do I need to file the Tax POA 500 form with the IRS?

The Tax POA 500 form does not need to be filed with the IRS for it to be effective. However, it is crucial to submit the form to the IRS if you want the appointed individual to receive confidential tax information. Providing a copy of the form to the appointee is also recommended to ensure they can serve effectively in their role.

Can I revoke the Tax POA 500 form once it has been submitted?

Yes, a taxpayer can revoke the Tax POA 500 form at any time. To do so, the taxpayer should submit a written revocation notice to the IRS. It is important to notify the appointed representative as well, to ensure they are aware of the change in authority. Promptly revoking the Power of Attorney protects a taxpayer's interests and ensures that no further actions are taken by the appointee on their behalf.

Filling out the Tax POA 500 form can be daunting, and it's easy to make mistakes. Here are five common errors people often make, which can lead to delays or issues with their tax representation.

Many individuals accidentally enter incorrect personal information, such as their Social Security number or taxpayer identification number. Double-checking these numbers is crucial, as a simple typo can lead to confusion and hinder the process.

Neglecting to sign the form is a frequent oversight. Without a signature, the form is not valid, and it can’t be processed. Always ensure that both the taxpayer and the representative sign where required.

Some people forget to clearly define the scope of authority they are granting to their representative. It's important to specify what powers the representative will have, whether to handle all matters or just specific ones.

Another common mistake involves failing to provide adequate contact information for both the taxpayer and the representative. Missing phone numbers or emails can result in significant delays in communication regarding tax matters.

People may inadvertently use an older version of the Tax POA 500 form. Tax forms frequently get updated. Always verify that you are using the most recent version available from the tax authority to ensure compliance.

By paying attention to these common pitfalls, individuals can enhance their chances of successfully completing the Tax POA 500 form and establishing effective tax representation.

When engaging in tax matters, several forms and documents may accompany the Tax POA 500 form. These documents serve various purposes and can help streamline the process of tax representation. Below is a list of commonly used forms along with brief descriptions of each.

Understanding these related forms can significantly enhance the tax representation process. Each document serves a specific purpose, ensuring that taxpayer rights are protected and that communication with tax authorities is clear and effective.

The IRS Form 2848, Power of Attorney and Declaration of Representative, serves a similar purpose as Tax POA 500. Both forms enable individuals to authorize a representative to act on their behalf in tax matters. Form 2848 is specific to federal tax issues, allowing the appointed representative to handle most IRS business, whereas Tax POA 500 may be geared more toward state-specific tax concerns. Each form requires the taxpayer's consent and detailed information about the representative's authority.

The IRS Form 8821, Tax Information Authorization, is often compared to the Tax POA 500. While Tax POA 500 allows a representative to make decisions, Form 8821 only grants authorization to receive tax information. This distinction is crucial when individuals simply want their representatives to be informed without granting them decision-making power. Both forms require accurate sections to identify the taxpayer and the type of tax involved.

Power of Attorney forms used by various states, such as California’s Form FTB 3520, share similarities with Tax POA 500. These state-specific forms empower representatives to manage tax affairs at the state level, ensuring compliance with local regulations. Similar to Tax POA 500, they require the taxpayer's signature to validate the authorization. Each state may have unique requirements, but the intent remains the same: to allow a designated person to act in tax matters.

Form 4506, Request for Copy of Tax Return, aligns with Tax POA 500 in that both forms require explicit taxpayer consent to disclose sensitive tax information. However, while Tax POA 500 grants powers beyond information access, Form 4506 strictly serves to obtain copies of past tax returns. Thus, Tax POA 500 encompasses broader powers pertaining to tax representation.

Another pertinent document is the Durable Power of Attorney form. This form, while primarily a legal vehicle for a range of decisions beyond taxes, can include provisions for tax representation. The resemblance to Tax POA 500 lies in the capacity granted to a representative to act on behalf of the individual. However, the Durable Power of Attorney remains in effect even if the individual becomes incapacitated, which is not necessarily the case with Tax POA 500.

The Uniform Power of Attorney Act simplifies the comparison with Tax POA 500 by standardizing the power of attorney process across states. This act provides a framework for authority delegation that, while broader in scope, shares core principles with Tax POA 500. Both documents ultimately hinge upon granting specific powers to a designated representative, whether for taxation or other decisions.

Form 8822, Change of Address, also holds some similarities. While its primary function is to notify the IRS about an address change, the form can include an option to authorize a third party to manage communication regarding that change. This fosters a relationship between taxpayer and representative, akin to the relationships detailed in Tax POA 500. However, its scope is far narrower.

Tax consent forms, such as those used for third-party direct communications with tax authorities (like consent to disclose certain taxpayer information), highlight the sharing of information aspect present in Tax POA 500. These forms enable representatives to speak on behalf of taxpayers but do not generally extend powers beyond information sharing. Therefore, the essence of trust is established in both scenarios, with the representative acting within agreed limits.

Lastly, a health care power of attorney can be likened to Tax POA 500 in terms of granting another person authority to act on behalf of an individual. While health care powers are specific to medical decisions, the fundamental principle of empowering a designated representative remains consistent. Such documents typically require clear language about the scope and limit of authority, similar to provisions laid out in Tax POA 500.

When filling out the Tax POA 500 form, careful attention to detail is essential. Here is a list of things to consider:

The Tax POA 500 form, a key document for designating a representative, often faces misunderstandings. Here are nine common misconceptions:

Only tax professionals can be designated on the Tax POA 500 form. This is incorrect. Individuals can appoint anyone, including friends or family members, as their representative.

Filing the form is only necessary during tax audits. Many believe it's needed solely for audits, but it can be useful in various situations, including during regular tax filing or inquiries.

The form is the same for all states. Each state has its own version of a power of attorney form. Make sure to use the correct form for your specific state.

Once filed, it cannot be revoked. This is a myth. You can revoke a Power of Attorney by submitting a written revocation notice at any time.

Signing the POA allows unlimited access to your tax information. While the form grants access, you can specify which tax years and types of information your representative can view.

There is a filing fee associated with the Tax POA 500 form. In general, there are no fees for filing this form with the IRS or state tax agencies.

The form must be submitted in person. This is not true. The Tax POA 500 can typically be submitted via mail, fax, or e-file, depending on regulations.

Once designated, a representative has control over your tax return. A representative can assist and communicate with the tax authority but cannot make final decisions without your consent.

The form is only valid for one year. The validity of the form depends on the specifics mentioned in it. You should check for any expiration clauses in your designation.

Understanding these misconceptions can help individuals effectively use the Tax POA 500 form, ensuring they empower trusted representatives without misunderstanding the implications.

When dealing with tax matters, understanding how to fill out and use the Tax Power of Attorney (POA) 500 form can significantly simplify the process. Here are some key takeaways to keep in mind:

Understanding these points can help you navigate tax representation effectively, making the process less daunting.