The Tax POA 285-I form is an important document for individuals who want to authorize someone else to represent them before the IRS. This form is necessary for ensuring that your designated representative can handle your tax matters effectively, including filing returns, receiving confidential information, and making decisions on your behalf. Typically, this form is utilized when different situations arise, such as the need for professional assistance with tax audits or when someone cannot attend to their tax responsibilities due to personal circumstances. The 285-I form not only outlines the powers granted to the representative but also specifies the limitations, which helps protect your interests. Completing the form correctly is crucial; any errors can delay the processing of your request or result in the rejection of the authorization. This overview will navigate through the key elements of the Tax POA 285-I form, detailing how to fill it out properly and what to consider before submitting it to the IRS.

ARIZONA FORM |

Individual Income Tax Disclosure/Representation |

|

|

Authorization Form |

|

|

|

ARIZONA DEPARTMENT OF REVENUE • 1600 WEST MONROE, PHOENIX, AZ 85007 |

|

|

|

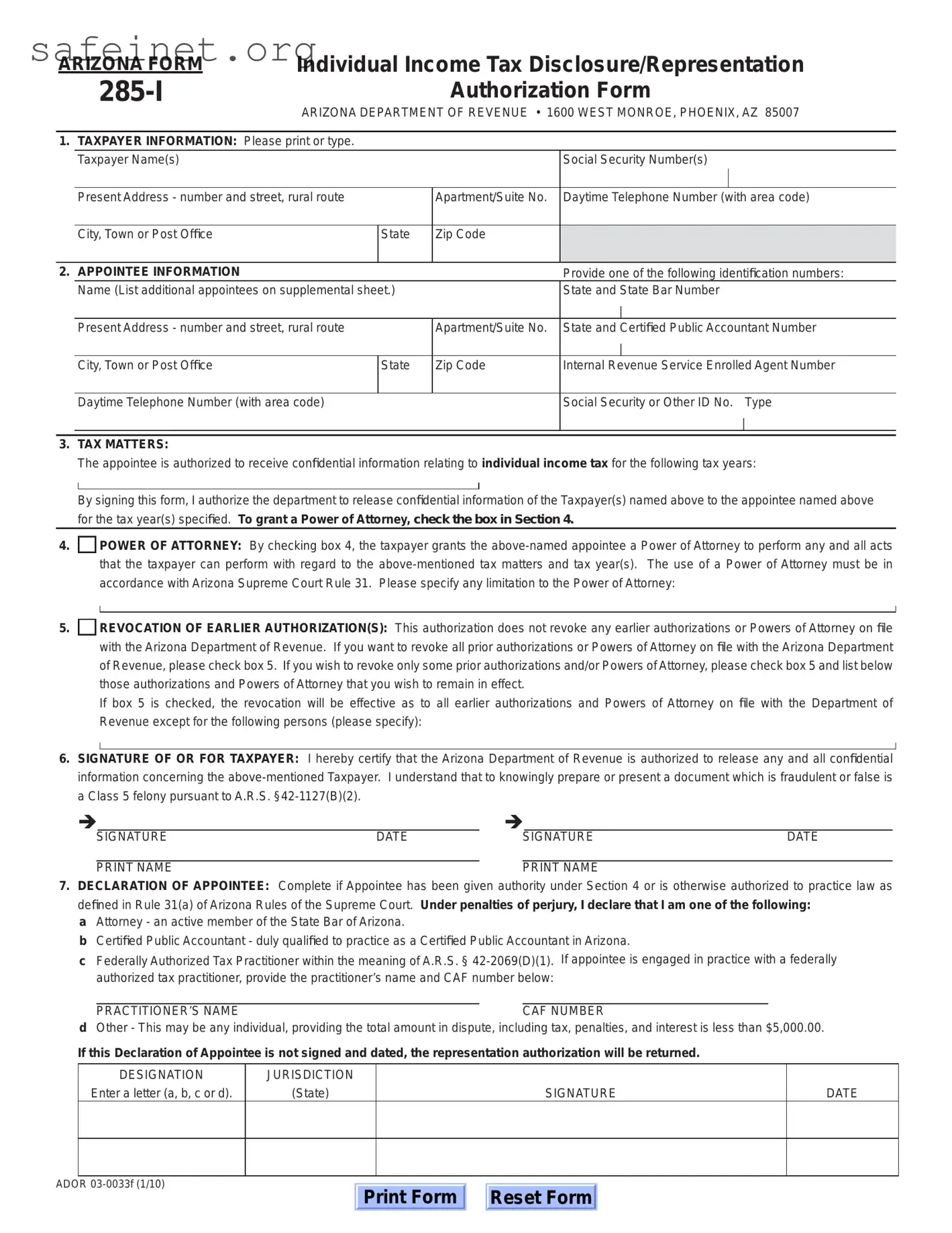

1. TAXPAYER INFORMATION: Please print or type. |

||

|

Taxpayer Name(s) |

Social Security Number(s) |

Present Address - number and street, rural route

Apartment/Suite No.

Daytime Telephone Number (with area code)

City, Town or Post Office

State

Zip Code

2. APPOINTEE INFORMATION |

|

|

Provide one of the following identification numbers: |

|

|

Name (List additional appointees on supplemental sheet.) |

|

State and State Bar Number |

|

|

|

|

|

| |

|

Present Address - number and street, rural route |

|

Apartment/Suite No. |

State and Certified Public Accountant Number |

|

|

|

|

| |

|

City, Town or Post Office |

State |

Zip Code |

Internal Revenue Service Enrolled Agent Number |

|

|

|

|

|

|

Daytime Telephone Number (with area code) |

|

|

Social Security or Other ID No. Type |

|

|

|

|

| |

|

|

|

|

|

3.TAX MATTERS:

The appointee is authorized to receive confidential information relating to individual income tax for the following tax years:

By signing this form, I authorize the department to release confidential information of the Taxpayer(s) named above to the appointee named above for the tax year(s) specified. To grant a Power of Attorney, check the box in Section 4.

4.

POWER OF ATTORNEY: By checking box 4, the taxpayer grants the

5.

REVOCATION OF EARLIER AUTHORIZATION(S): This authorization does not revoke any earlier authorizations or Powers of Attorney on file with the Arizona Department of Revenue. If you want to revoke all prior authorizations or Powers of Attorney on file with the Arizona Department of Revenue, please check box 5. If you wish to revoke only some prior authorizations and/or Powers of Attorney, please check box 5 and list below those authorizations and Powers of Attorney that you wish to remain in effect.

If box 5 is checked, the revocation will be effective as to all earlier authorizations and Powers of Attorney on file with the Department of Revenue except for the following persons (please specify):

6.SIGNATURE OF OR FOR TAXPAYER: I hereby certify that the Arizona Department of Revenue is authorized to release any and all confidential information concerning the

Î |

|

|

Î |

|

|

||

|

|

SIGNATURE |

DATE |

|

|

SIGNATURE |

DATE |

|

|

|

|

|

|

||

|

PRINT NAME |

|

PRINT NAME |

|

|||

7.DECLARATION OF APPOINTEE: Complete if Appointee has been given authority under Section 4 or is otherwise authorized to practice law as defined in Rule 31(a) of Arizona Rules of the Supreme Court. Under penalties of perjury, I declare that I am one of the following:

a Attorney - an active member of the State Bar of Arizona.

b Certified Public Accountant - duly qualified to practice as a Certified Public Accountant in Arizona.

c Federally Authorized Tax Practitioner within the meaning of A.R.S. §

PRACTITIONER’S NAME |

CAF NUMBER |

dOther - This may be any individual, providing the total amount in dispute, including tax, penalties, and interest is less than $5,000.00.

If this Declaration of Appointee is not signed and dated, the representation authorization will be returned.

DESIGNATION

Enter a letter (a, b, c or d).

JURISDICTION

(State)

SIGNATURE

DATE

ADOR

Print Form

Reset Form

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA 285-I form is used to authorize an individual or organization to act on your behalf regarding tax matters. |

| Who Can Use It | Taxpayers, including individuals and businesses, can use this form to delegate authority to their representatives. |

| Governing Law | This form is governed by the Internal Revenue Code and specific state tax laws depending on the state of filing. |

| Filing Requirements | The form must be completed and signed by the taxpayer, and it should be submitted to the appropriate tax authority. |

| Validity Period | Once submitted, the authority granted under the form is usually valid until revoked or until the taxpayer withdraws permission. |

| Limitations | Certain limitations may apply to the role of the representative, such as restrictions on accessing personal information or making decisions. |

Filling out the Tax POA 285-I form requires careful attention to detail. Once completed, it will allow an individual to authorize another person to represent them in tax matters. Ensure that all sections are filled in accurately to avoid any complications.

After submitting the form, allow time for processing. Confirm that your representative is recognized by the tax authority and capable of acting on your behalf. Communication with them will be essential for managing your tax matters effectively.

What is the Tax POA 285-I form?

The Tax POA 285-I form is a Power of Attorney form specifically for tax matters. It grants an individual or entity the authority to represent another person before tax authorities. This form is essential for allowing your representative to perform tasks on your behalf, such as managing tax returns, communicating with tax agencies, and resolving issues related to your tax obligations.

Who should use the Tax POA 285-I form?

Individuals who wish to grant someone else the authority to handle their tax affairs should use the Tax POA 285-I form. This may include taxpayers who are unable to manage their tax matters due to time constraints, physical limitations, or other reasons. Additionally, businesses may also use this form to designate representatives for handling tax-related issues.

How do I complete the Tax POA 285-I form?

Completing the Tax POA 285-I form involves several steps. First, fill out your name, address, and Social Security number or Employer Identification Number (EIN). Next, provide the same information for the person you are designating as your representative. Be sure to specify the tax matters and periods for which the authority is granted. Once filled out, the form must be signed and dated by you. Depending on the specific needs, you may also need to provide additional documentation.

Do I need to notify the IRS or state tax agency after submitting the Tax POA 285-I form?

Once you submit the Tax POA 285-I form, there is generally no need to notify the IRS or your state tax agency again. The submission itself serves as notification that you have authorized your representative to act on your behalf. However, it is wise to keep a copy of the submitted form for your records and ensure that your representative is aware of their responsibilities.

Can I revoke the authority granted through the Tax POA 285-I form?

Yes, you can revoke the authority granted by the Tax POA 285-I form at any time. To do this, you must submit a written notice of revocation to your representative and the tax agency. It is advisable to use the same format as the original form and clearly indicate that you are revoking the power of attorney. This action nullifies the representative's authority and ensures that your tax matters are handled according to your wishes going forward.

Is there a fee associated with filing the Tax POA 285-I form?

No fees are typically required when submitting the Tax POA 285-I form to the IRS or state tax agencies. However, you may incur costs for the services of the representative you choose to designate. It's essential to clarify any potential fees with your appointed representative before granting them authority through this form.

Incorrect information about the taxpayer: People often make mistakes inputting their name, Social Security number, or address. Double-checking this information is important to ensure accuracy.

Improper selection of representative: Selecting someone who isn’t authorized to act on your behalf can cause delays. Ensure the person you choose meets the criteria set by the IRS.

Missing signature: Leaving the signature field blank is a common mistake. Without a signature, the form is considered incomplete and will not be processed.

Not specifying the tax years or types: Failing to indicate the specific years or types of tax matters can lead to confusion. Clearly state what you need help with.

Failing to date the form: Forgetting to date the document is another oversight that can invalidate the request. Date it before submission.

Incorrect form version: Using an outdated version of the form can cause complications. Always check for the most current version on the IRS website.

Neglecting to read the instructions: Skipping over the instructions can lead to misunderstanding how to complete the form. Take the time to read them carefully.

Not providing a valid phone number: Your phone number is crucial for any follow-ups. Ensure you include a reliable contact number.

Submitting without keeping a copy: Failing to keep a copy for personal records can create problems if there is any dispute later on. Always retain a copy of everything you submit.

The Tax Power of Attorney (POA) 285-I form allows taxpayers to authorize an individual to represent them before the IRS. Various other forms and documents accompany this form to ensure complete compliance and facilitate the representation process. Below are several key documents often utilized alongside the Tax POA 285-I form.

Submitting the necessary forms alongside the Tax POA 285-I can streamline the process of tax representation. Each document plays a crucial role in ensuring that all parties have the authority and information needed to manage tax issues effectively.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is similar to the Tax POA 285-I form as both serve to grant a designated individual the authority to act on behalf of a taxpayer. Each form allows the appointed representative to receive and discuss taxpayer information, typically during audits or appeals. However, Form 2848 specifically addresses representation before the IRS, whereas Form 285-I is more focused on state-level tax issues, emphasizing the scope and jurisdiction of the authority granted.

The IRS Form 8821, Tax Information Authorization, also bears similarity to the Tax POA 285-I form. Both forms allow an individual to access a taxpayer’s information but differ in their granted powers. While the 285-I form allows representation, the 8821 form only authorizes the recipient to obtain and review tax information without the ability to make decisions on behalf of the taxpayer. This distinction is crucial for taxpayers who may wish to share information without ceding decision-making authority.

The Representative Authorization Form (often used at the state level) similarly aligns with the Tax POA 285-I. This document permits a designated agent to handle tax-related matters on behalf of the taxpayer, similar to the POA 285-I. Such forms are typically formatted to meet specific state requirements, which may center around local tax codes, illustrating how the application of authority might vary based on jurisdiction.

The Limited Power of Attorney, a more general form, shares key features with the Tax POA 285-I form. It allows a person to act on behalf of another but is often narrower in scope, specifying particular transactions or legal matters. In contrast, the 285-I form is tailored for tax-related authorities and issues, ensuring that the representative can fully engage with pertinent tax matters.

Finally, corporate resolutions designating an officer or agent to act on behalf of a company can also be compared to the Tax POA 285-I. These resolutions empower specific individuals to handle various tasks, including tax matters, representing the company’s interests. The legal authority conferred mirrors the powers granted through the Tax POA 285-I, yet corporate resolutions address a collective rather than an individual taxpayer, showcasing varied applications of authority in different contexts.

When filling out the Tax POA 285-I form, it's essential to follow certain guidelines to ensure accuracy and compliance. Here’s a list of ten do's and don'ts to keep in mind:

By following these tips, you can help ensure a smoother process when submitting your Tax POA 285-I form.

This is not accurate. The Tax POA 285-I form is designed for any taxpayer who wishes to appoint a representative to act on their behalf before the IRS. This includes situations where individuals seek guidance on tax matters, even if they have no outstanding tax liabilities.

While appointing a representative is an essential step in getting assistance, it does not assure that all issues will be resolved to the taxpayer’s satisfaction. The effectiveness of the representative largely depends on their experience and knowledge of tax matters, as well as the specifics of the taxpayer's situation.

This is incorrect. The authority granted via the Tax POA 285-I form can be revoked at any time by the taxpayer. Revocation should be communicated to both the representative and the IRS to prevent any confusion regarding representation status.

In reality, taxpayers can submit the Tax POA 285-I form via mail, fax, or online, depending on their circumstances. Moreover, representatives may be able to handle multiple aspects of a tax case remotely, thus simplifying the process significantly for the taxpayer.

When filling out the Tax POA 285-I form, there are several important points to keep in mind. This form designates someone to represent you before the IRS regarding tax matters. Here are some key takeaways to help you navigate the process effectively:

Taking these steps seriously ensures a smoother experience when dealing with tax matters through a representative.