The Tax POA 2848a form plays a crucial role in the management of tax affairs for individuals and businesses alike. This form is designed to authorize an individual, typically a tax professional, to act on behalf of the taxpayer when dealing with the Internal Revenue Service (IRS). It streamlines communication and establishes a formal relationship between the taxpayer and their representative. Notably, the form requires specific information, including the taxpayer's details, the representative’s credentials, and the scope of authority being granted. Furthermore, this form is not only vital for ensuring proper representation but also crucial for maintaining compliance with tax obligations. By using the POA 2848a, taxpayers can effectively delegate responsibilities, ensuring that their tax matters are handled efficiently and professionally. Understanding this form's significance can help taxpayers navigate their financial responsibilities with greater ease and confidence.

|

FORM |

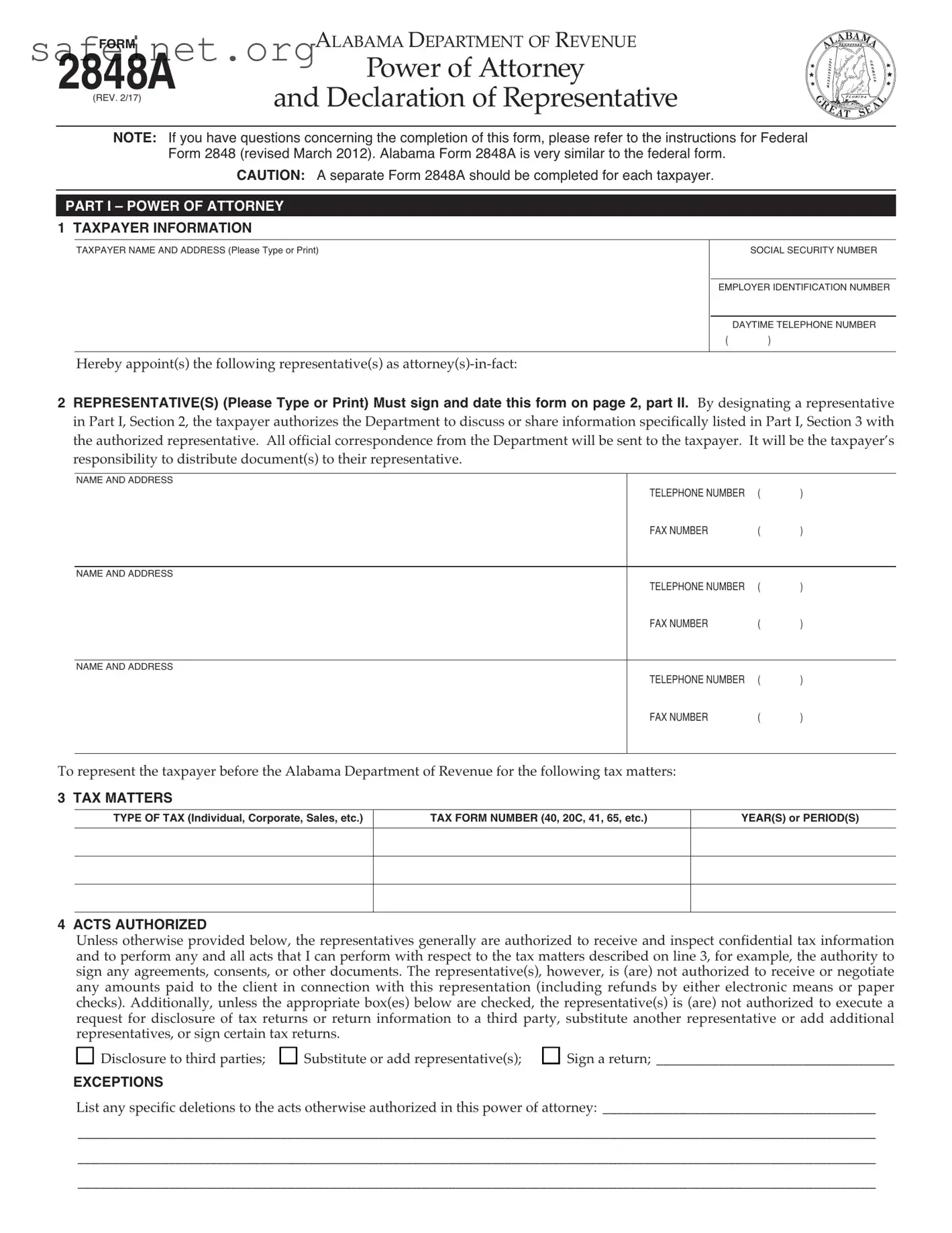

ALABAMA DEPARTMENT OF REVENUE |

|

|

|

2848A |

Power of Attorney |

|

|

||

and Declaration of Representative |

|

|

|||

|

(REV. 2/17) |

|

|

|

|

|

NOTE: If you have questions concerning the completion of this form, please refer to the instructions for Federal |

||||

|

Form 2848 (revised March 2012). Alabama Form 2848A is very similar to the federal form. |

|

|||

|

|

CAUTION: A separate Form 2848A should be completed for each taxpayer. |

|

|

|

1 TAXPAYER INFORMATION |

|

|

|||

|

TAXPAYER NAME AND ADDRESS (Please Type or Print) |

|

|

SOCIAL SECURITY NUMBER |

|

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER |

|

|

Hereby appoint(s) the following representative(s) as |

|

|

DAYTIME TELEPHONE NUMBER |

|

|

|

( |

) |

||

|

|

|

|

||

|

|

|

|

|

|

2 REPRESENTATIVE(S) (Please Type or Print) Must sign and date this form on page 2, part II. By designating a representative |

||

in Part I, Section 2, the taxpayer authorizes the Department to discuss or share information specifically listed in Part I, Section 3 with |

||

the authorized representative. All official correspondence from the Department will be sent to the taxpayer. It will be the taxpayer’s |

||

responsibility to distribute document(s) to their representative. |

|

|

NAME AND ADDRESS |

|

|

TELEPHONE NUMBER |

( |

) |

FAX NUMBER |

( |

) |

NAME AND ADDRESS |

|

|

TELEPHONE NUMBER |

( |

) |

FAX NUMBER |

( |

) |

NAME AND ADDRESS |

|

|

TELEPHONE NUMBER |

( |

) |

FAX NUMBER |

( |

) |

To represent the taxpayer before the Alabama Department of Revenue for the following tax matters: |

|

|

3 TAX MATTERS |

TAX FORM NUMBER (40, 20C, 41, 65, etc.) |

YEAR(S) or PERIOD(S) |

TYPE OF TAX (Individual, Corporate, Sales, etc.) |

||

4 ACTS AUTHORIZED |

|

Unless otherwise provided below, the representatives generally are authorized to receive and inspect confidential tax information |

|

and to perform any and all acts that I can perform with respect to the tax matters described on line 3, for example, the authority to |

|

sign any agreements, consents, or other documents. The representative(s), however, is (are) not authorized to receive or negotiate |

|

any amounts paid to the client in connection with this representation (including refunds by either electronic means or paper |

|

checks). Additionally, unless the appropriate box(es) below are checked, the representative(s) is (are) not authorized to execute a |

|

request for disclosure of tax returns or return information to a third party, substitute another representative or add additional |

|

representatives, or sign certain tax returns. |

|

Disclosure to third parties; |

Substitute or add representative(s); Sign a return; __________________________________ |

EXCEPTIONS |

|

List any specific deletions to the acts otherwise authorized in this power of attorney: _______________________________________

__________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________

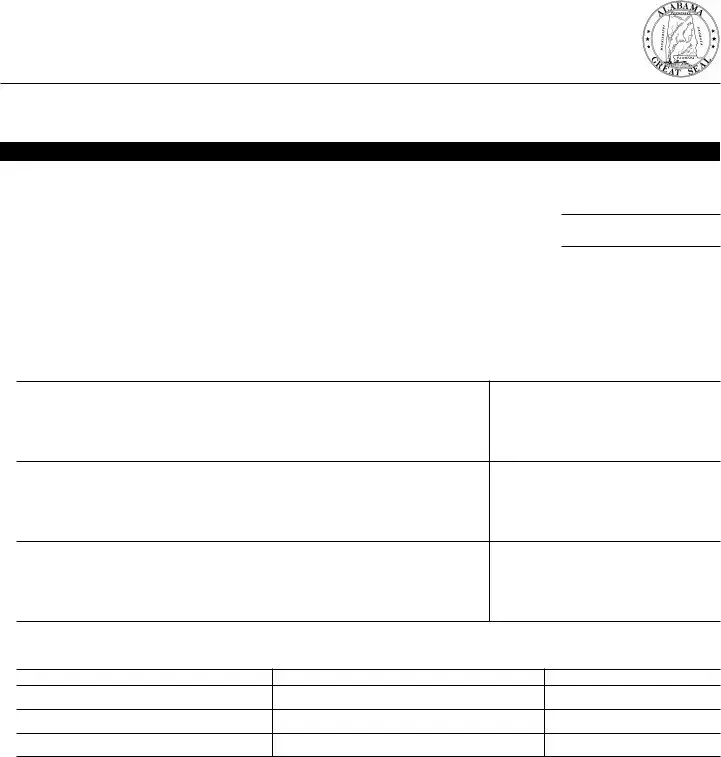

FORM 2848A (REV. 2/17) |

PAGE 2 |

5 RETENTION / REVOCATION OF PRIOR POWER(S) OF ATTORNEY |

|

The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Alabama |

|

Department of Revenue for the same tax matters and years or periods covered by this document. If you do not want |

|

to revoke a prior power of attorney, check here |

6 SIGNATURE OF TAXPAYEou MuStR AttAch A copY oF ANY power oF AttorNeY You wANt to reMAIN IN eFFect.

If a tax matter concerns a year in which a joint return was filed, the husband and wife must each file a separate power of attorney even if the same representative(s) is (are) being appointed. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

If this power of attorney is not signed and dated, it will be returned to the taxpayer.

SIGNATURE |

DATE |

TITLE (If Applicable) |

|

|

|

PRINT NAME |

|

|

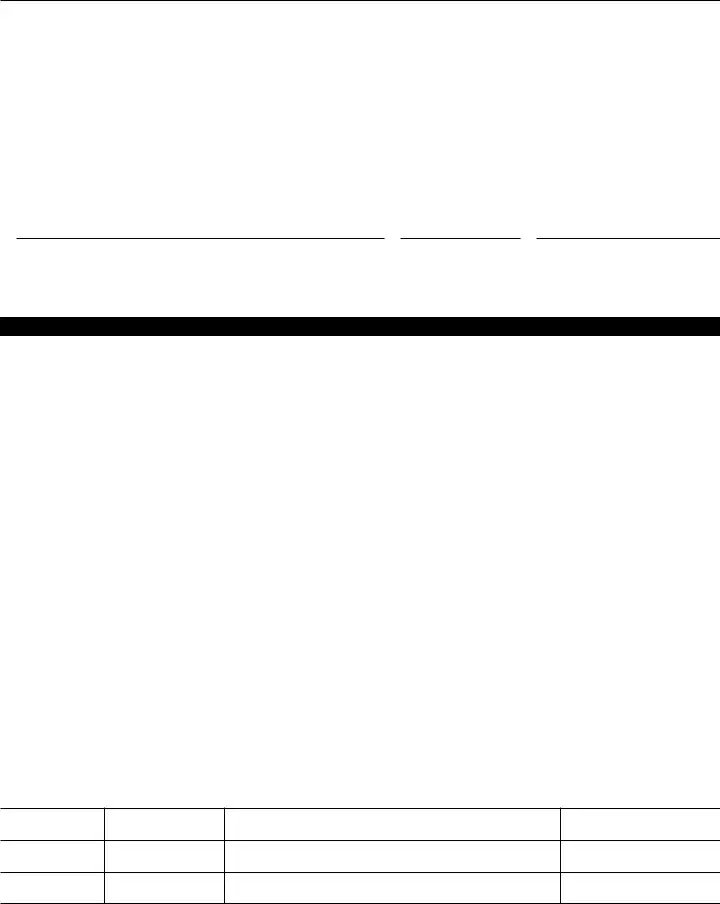

Under penalties of perjury, I declare that:

• I am not currently under suspension or disbarment from practice before the Internal Revenue Service;

• I am aware of regulations contained in Treasury Department Circular No. 230 (31 CFR, Part 10), as amended, concerning the practice of attorneys, certified public accountants, enrolled agents, enrolled actuaries, and others;

• I am authorized to represent the taxpayer identified in Part I for the tax matter(s) specified there; and

• I am one of the following:

Attorney – a member in good standing of the bar of the highest court of the jurisdiction shown below.

a. Certified Public Accountant – duly qualified to practice as a certified public accountant in the jurisdiction shown below. b. Enrolled Agent – enrolled as an agent under the requirements of Treasury Department Circular No. 230.

c. Officer – a bona fide officer of the taxpayer’s organization. d.

e. Family Member – a member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

f. Enrolled Actuary – enrolled as an actuary by the Joint Board for the Enrollment of Actuaries under 29 U.S.C. 1242 (the g. authority to practice before the Service is limited by section 10.3(d)(1) of Treasury Department Circular No. 230).

Unenrolled Return Preparer – an unenrolled return preparer under section 10.7(c)(1)(viii) of Treasury Department Circular h. No. 230.

Registered Tax Return Preparer – registered as a tax return preparer under the requirements of section 10.4 of Circular 230.

i. Your authority to practice before the Internal Revenue Service is limited. You must have been eligible to sign the return under examination and have signed the return. See Notice

StudentunenrolledAttorneyand returnor CPApreparers– receivesin permissionthe in tructitopracticens. before the IRS by virtue of his/her status as a law, business, or j. accounting student working in LITC or STCP under section 10.7(d) of Circular 230. See instructions for Part II for additional

information and requirements.

Enrolled Retirement Plan Agent – enrolled as a retirement plan agent under the requirements of Circular 230 (the authority to k. practice before the Internal Revenue Service is limited by section 10.3(e)).

If this declaration of representative is not signed and dated, the power of attorney will be returned.

Note: For designations

DESIGNATION – INSERT

ABOVE LETTER

JURISDICTION (State) or

ENROLLMENT CARD NO.

SIGNATURE

DATE

Made fillable by FormsPal.

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA 2848a form allows an individual to appoint someone to represent them before the IRS in tax matters. This is crucial for ensuring that taxpayers have the support they need in handling their tax issues. |

| Eligibility | Any individual or entity can complete the form to designate a representative. This includes tax professionals, family members, or friends who can assist with tax-related matters. |

| Filing Requirements | The completed form must be sent to the IRS office handling the taxpayer's account. This ensures that the representative is recognized and authorized to act on behalf of the taxpayer. |

| State-Specific Forms | Some states may have their own power of attorney forms governing tax matters. For example, California uses Form 3520 to appoint a tax representative, with relevant guidelines outlined in the California Revenue and Taxation Code. |

To successfully complete the Tax POA 2848a form, follow these steps carefully. Each section must be accurately filled out to ensure that your tax matters are handled correctly. After submitting this form, you’ll be able to designate a representative who can conduct business on your behalf with the IRS.

What is the purpose of the Tax POA 2848a form?

The Tax POA 2848a form allows individuals to designate a representative to act on their behalf regarding federal tax matters. This can include negotiating settlements, discussing payment options, or handling any correspondence with the IRS. It is essential for taxpayers who need assistance managing their tax responsibilities or who cannot handle their tax affairs personally.

Who can I designate as my representative on the Tax POA 2848a form?

You can appoint an attorney, certified public accountant, enrolled agent, or any individual you trust to represent you. The appointed person must be willing to take on the responsibility and must sign the form, confirming their agreement to represent you before the IRS.

How do I fill out the Tax POA 2848a form?

Filling out the form requires providing specific information, including your name, Social Security Number (or Employer Identification Number), and details about the representative being appointed. Both parties must sign and date the form to make it valid. Ensure that all information is accurate to prevent processing delays.

Can I restrict the scope of the authority granted to my representative?

Yes, the form allows for limitations on the authority granted to the representative. You can specify particular tax matters or periods for which the appointment is valid, ensuring that the representative only acts within the defined scope. This aspect is particularly useful for taxpayers who may not want to grant full representation rights.

How long is the Tax POA 2848a form effective?

The POA remains in effect until you revoke it, or until the designated representative notifies the IRS that they no longer wish to act on your behalf. Taxpayers should periodically review their designations to ensure they are still relevant to their needs.

What happens if I accidentally submit an incomplete Tax POA 2848a form?

If the form is submitted incomplete, the IRS may reject it, leading to delays in processing your request for representation. It is crucial to double-check all sections for accuracy and completion before submission to avoid any issues.

Is there a fee associated with submitting the Tax POA 2848a form?

Generally, there is no fee charged by the IRS for submitting the Tax POA 2848a form. However, if you seek assistance from a professional (like an attorney or CPA), they may charge a fee for their services.

Can I revoke the Tax POA 2848a form once it is submitted?

Yes, you can revoke the power of attorney at any time by submitting a written notice to the IRS. It is advisable to send the revocation request directly to the same office where the original form was filed to ensure that it is processed correctly.

What should I do if my representative cannot continue to act on my behalf?

If your appointed representative can no longer represent you, you need to either revoke the existing POA and appoint a new representative or allow your current representative to formally withdraw from the case. Ensure that all relevant parties are notified to avoid confusion or miscommunication regarding your tax matters.

Where can I send the Tax POA 2848a form once it is completed?

The completed Tax POA 2848a form can be sent to the appropriate address listed on the form itself, depending on your specific circumstances. Different addresses may apply based on whether you are a domestic or foreign taxpayer. Always reference the latest instructions to confirm the correct submission address.

Incomplete Information: One common mistake occurs when individuals fail to provide all requested details on the form. Missing information, such as addresses, Social Security numbers, or dates, can lead to processing delays or outright rejection of the authorization.

Incorrect Agent Designation: Another frequent error involves misidentifying the authorized representative. If individuals select the wrong person or entity to act on their behalf, it can result in unauthorized actions or miscommunications with the IRS.

Failing to Sign the Form: Signing the Tax POA 2848a form is crucial. Many forget or overlook this step, thinking that the form is complete without their signature. Without it, the IRS will not recognize the authorization.

Not Specifying the Scope of Authority: It's essential to indicate the specific tax matters and years for which the authorization applies. If individuals leave this section blank or too vague, their representatives may not have the appropriate authority to act on their behalf, causing unnecessary complications.

When filing your Tax Power of Attorney using Form 2848, you might encounter several other forms and documents that can assist you with your tax needs. Each document serves a specific purpose and can help streamline your tax process.

Utilizing these forms alongside the Tax POA 2848 can help ensure that your tax matters are handled efficiently. Always ensure you have the appropriate documentation required for your specific tax situation.

The IRS Form 2848, otherwise known as the Power of Attorney (POA), allows an individual to designate someone to act on their behalf for tax matters. Similar to this form, the IRS Form 8821 is also used for delegating authority, but it differs in scope. While the 2848 authorizes an agent to represent you, the 8821 simply allows someone to receive information from the IRS. It’s a great option for those who want someone to handle inquiries without granting them full power to act on their behalf.

The Form 8850, used for Pre-Screening for the Work Opportunity Credit, shares some similarities with the POA form in its purpose of representation, but it is more narrowly focused. The 8850 works as a tool for employers to pre-qualify applicants for special tax credits, rather than appointing someone for ongoing tax representation. It seeks to ensure that specific criteria are met to qualify for tax benefits, showing a different angle on tax-related authority.

An additional document to consider is the IRS Form 8862, which is for the Reestablishment of Earned Income Credit Eligibility. While it doesn't directly relate to POA, it involves the representation of individuals regarding their eligibility for certain credits. Applicants utilize this form to assert their claims and ensure they receive all the credits they're entitled to, thus becoming a vital part of the tax process.

The IRS Form 4506-T, Request for Transcript of Tax Return, also parallels the 2848 in that it grants authorized parties access to tax return information. This form is particularly important for those who seek to verify income or tax payments, especially in scenarios like loan applications. Its function emphasizes the accessibility of tax records while still requiring a level of authorization.

The Form 1040X, used for Amended Tax Returns, somewhat aligns with the POA since it allows you to rectify previously filed tax information. In its essence, it acts as a formal request to change the IRS's understanding of your tax situation, much like how the 2848 enables someone to manage that understanding on your behalf. Both require clear communication and proper documentation to ensure compliance with IRS guidelines.

Moving on to state-level forms, the California Power of Attorney for Tax Matters mirrors the IRS Form 2848 in functionality at the state level. It allows taxpayers to designate a representative to handle their California state tax issues. This ensures that individuals maintain their rights under state law while receiving assistance in managing their state tax responsibilities.

The Uniform Power of Attorney Act (UPOAA) is a broader template for powers of attorney that can include tax matters. While 2848 is specific to tax cases, UPOAA allows for a more generalized power, which can include any legal matters such as finance, healthcare, or property management. Individuals may choose this approach for a more comprehensive delegation of authority in various aspects of their lives.

The Form 8822, Change of Address, provides another unique link to the 2848. While it focuses solely on updating the IRS with your new address, having an accurate address is crucial for effective representation. Should you designate someone with Form 2848, they need to ensure they are working with the correct information, making the 8822 an essential supporting document.

Lastly, the Form 9465 for Installment Agreements relates to tax representation as well. Once someone is appointed through the Form 2848, they can facilitate negotiations with the IRS for payment plans on tax debts using this form. Therefore, while not a power of attorney itself, it can be a critical document used in conjunction with one, assisting representatives to handle tax responsibilities effectively.

When filling out the Tax POA 2848a form, it is important to follow certain guidelines to ensure accuracy and efficiency. Below are ten things to consider doing and avoiding.

By adhering to these guidelines, you can help ensure the successful processing of the Tax POA 2848a form.

The IRS Power of Attorney form, known as the Form 2848, can often lead to misunderstandings. Here are five common misconceptions about this form:

Many people believe that only tax professionals can use the Form 2848. While it's true that tax advisors often use this form to represent clients, individuals can complete it to allow anyone they trust to handle their tax matters, including family members or friends.

Some think that signing this form allows the representative to do anything with their taxes. In reality, the authority granted on the form is specific to the actions listed. You can customize it to fit your needs, whether it’s for specific tax years or particular issues.

Many assume that submitting Form 2848 once is sufficient for all future tax matters. However, if there are changes in representation, tax issues, or if you need to appoint multiple representatives, a new form will be necessary to update or change existing designations.

People often think that different states require separate versions of Form 2848. This is not accurate. The IRS Form 2848 is a federal form, and it is used uniformly across all states for granting power of attorney regarding tax matters.

It is a common belief that the Power of Attorney form must be included with a tax return submission. In fact, you may submit Form 2848 at any time, and it does not have to accompany a tax return. Just make sure it is sent to the IRS if needed for specific representation purposes.

Understanding the Power of Attorney (POA) form 2848a is essential. This form allows you to authorize someone else to handle your tax matters with the IRS on your behalf. It’s a critical tool for ensuring that your affairs are managed by a trusted individual.

When filling out the form, you must provide accurate personal information. This includes your name, address, and taxpayer identification number. Errors in this section can lead to delays or complications in the processing of your request.

Clearly specify the scope of authority you are granting. The form allows you to define the specific tax matters and tax years you’re giving access to. This clarity helps avoid misunderstandings later.

After completing the form, remember that you need to submit it to the IRS for it to be valid. Keep a copy for your records and confirm that the IRS has processed your request to avoid any issues down the line.