The Tax POA 151 form is an essential document for individuals and entities who wish to designate someone else to act on their behalf in tax matters with the Internal Revenue Service (IRS). This form allows taxpayers to grant a power of attorney, enabling the appointed representative to receive and disclose tax information, represent them at tax hearings, and perform other tax-related duties. It simplifies the process of tax representation by clearly identifying the taxpayer, the representative, and the scope of authority granted. By completing the Tax POA 151, a taxpayer ensures that their representative has the legal standing to address issues such as disputes or questions regarding tax liabilities. The form mandates the inclusion of relevant details, including the taxpayer's identifying information and the specific tax matters that the representative is permitted to handle. Clarity in these areas helps minimize confusion and streamline communication between the IRS and the designated agent. Additionally, the form provides a clear path for revoking powers of attorney, should the taxpayer choose to do so. Understanding the structure and requirements of the Tax POA 151 is crucial for effective tax representation and compliance.

Michigan Department of Treasury |

Issued under authority of Public Act 122 of 1941. |

151 (Rev. |

|

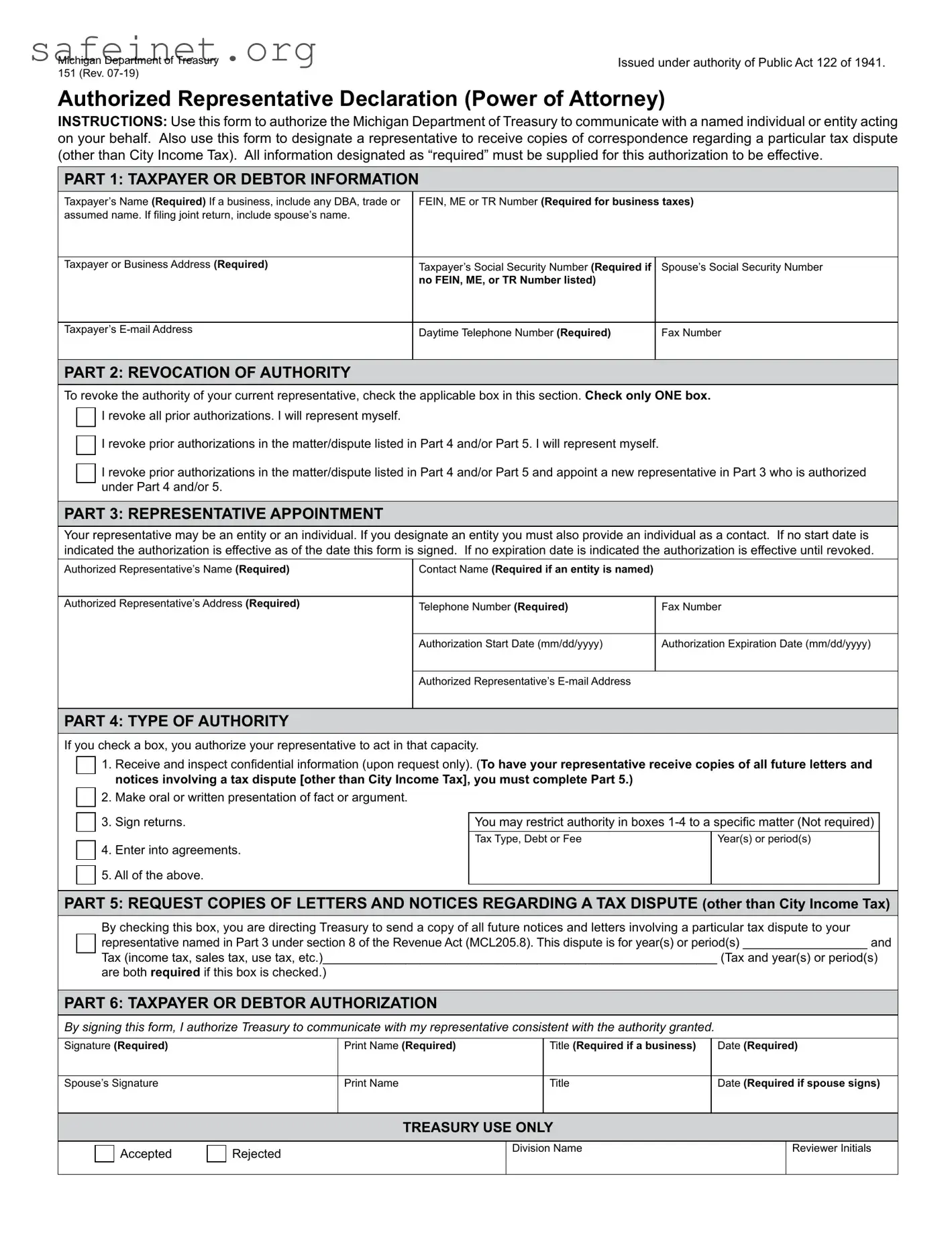

Authorized Representative Declaration (Power of Attorney)

INSTRUCTIONS: Use this form to authorize the Michigan Department of Treasury to communicate with a named individual or entity acting on your behalf. Also use this form to designate a representative to receive copies of correspondence regarding a particular tax dispute (other than City Income Tax). All information designated as “required” must be supplied for this authorization to be effective.

PART 1: TAXPAYER OR DEBTOR INFORMATION

Taxpayer’s Name (Required) If a business, include any DBA, trade or |

FEIN, ME or TR Number (Required for business taxes) |

|

assumed name. If filing joint return, include spouse’s name. |

|

|

|

|

|

Taxpayer or Business Address (Required) |

Taxpayer’s Social Security Number (Required if |

Spouse’s Social Security Number |

|

no FEIN, ME, or TR Number listed) |

|

|

|

|

Taxpayer’s |

Daytime Telephone Number (Required) |

Fax Number |

|

|

|

PART 2: REVOCATION OF AUTHORITY

To revoke the authority of your current representative, check the applicable box in this section. Check only ONE box. □

I revoke all prior authorizations. I will represent myself.

I revoke all prior authorizations. I will represent myself.

□

I revoke prior authorizations in the matter/dispute listed in Part 4 and/or Part 5. I will represent myself.

I revoke prior authorizations in the matter/dispute listed in Part 4 and/or Part 5. I will represent myself.

□ I revoke prior authorizations in the matter/dispute listed in Part 4 and/or Part 5 and appoint a new representative in Part 3 who is authorized under Part 4 and/or 5.

PART 3: REPRESENTATIVE APPOINTMENT

Your representative may be an entity or an individual. If you designate an entity you must also provide an individual as a contact. If no start date is indicated the authorization is effective as of the date this form is signed. If no expiration date is indicated the authorization is effective until revoked.

Authorized Representative’s Name (Required) |

Contact Name (Required if an entity is named) |

|

|

|

|

Authorized Representative’s Address (Required) |

Telephone Number (Required) |

Fax Number |

|

|

|

|

Authorization Start Date (mm/dd/yyyy) |

Authorization Expiration Date (mm/dd/yyyy) |

|

|

|

|

Authorized Representative’s |

|

|

|

|

PART 4: TYPE OF AUTHORITY

If you check a box, you authorize your representative to act in that capacity. |

|

|

|||||

|

|

|

1. |

Receive and inspect confidential information (upon request only). (To have your representative receive copies of all future letters and |

|

||

|

□ |

|

|

||||

|

|

|

notices involving a tax dispute [other than City Income Tax], you must complete Part 5.) |

|

|

||

|

□ |

|

2. |

Make oral or written presentation of fact or argument. |

|

|

|

|

|

|

|

|

|

|

|

|

□ |

|

3. |

Sign returns. |

You may restrict authority in boxes |

|

|

|

|

|

|

Tax Type, Debt or Fee |

Year(s) or period(s) |

|

|

|

□ |

|

4. |

Enter into agreements. |

|

|

|

|

|

5. All of the above. |

|

|

|

||

|

□ |

|

I |

I |

I |

||

|

|

|

|

|

|

|

|

PART 5: REQUEST COPIES OF LETTERS AND NOTICES REGARDING A TAX DISPUTE (other than City Income Tax)

By checking this box, you are directing Treasury to send a copy of all future notices and letters involving a particular tax dispute to your

□ representative named in Part 3 under section 8 of the Revenue Act (MCL205.8). This dispute is for year(s) or period(s) __________________ and

Tax (income tax, sales tax, use tax, etc.)_________________________________________________________ (Tax and year(s) or period(s)

are both required if this box is checked.)

PART 6: TAXPAYER OR DEBTOR AUTHORIZATION

By signing this form, I authorize Treasury to communicate with my representative consistent with the authority granted.

Signature (Required) |

Print Name (Required) |

Title (Required if a business) |

Date (Required) |

Spouse’s Signature |

Print Name |

Title |

Date (Required if spouse signs) |

TREASURY USE ONLY

□ Accepted |

□ Rejected |

Division Name |

Reviewer Initials |

I |

I |

Form 151, Page 2

Purpose

Use the Authorized Representative Declaration (Power of Attorney) (Form 151) to authorize the Michigan Department of Treasury (Treasury) to communicate with a named individual or entity acting on your behalf. This form may also be used to revoke your representative’s authority or to designate a representative to receive letters and notices regarding a particular tax dispute.

Required information. If a box includes the word “Required,” you must provide the information. If a box does not contain the required information, the form is invalid and you will be notified by letter.

Part 2: Revoking the authority of a representative. Complete Part 2 if you want to revoke your representative’s authority in whole or in part or all prior authorizations. After you revoke your representative’s authority, you may represent yourself, or you may appoint a new representative.

Part 3: Appointing an entity as your representative. If you appoint an entity as your representative, then any individual within that entity is authorized to act on your behalf. For example, if you appoint the XYZ Law Firm as your representative, any attorney or paralegal from that firm is authorized to act on your behalf. The “Contact Name” is only to ensure that information sent to the entity is directed to the individual overseeing your representation. The contact name is NOT your sole authorized representative. To appoint an entity, write in the Name and Address box (for example):

XYZ Law Firm 1234 Street

City, State, ZIP Code

Appointing an individual as your representative. If you appoint a specific individual as your representative, then only that individual is authorized to act on your behalf. Treasury will only discuss with or disclose information to that individual. For example, if a specific attorney at the XYZ Law Firm is named as your representative, Treasury will not discuss with or disclose information to any other attorney or paralegal at the same firm. To appoint an individual, write in the Name and Address box (for example):

Lynn Lee XYZ Law Firm 1234 Street

City, State, ZIP Code

Part 4: Type of authority: General or limited. You may grant your representative general or limited authority to act on your behalf. The actions that your representative may take will depend on the boxes that you check in Part 4. Confidential information (box 1) will only be provided upon request; Treasury will not automatically send confidential information to your representative. If you check box 5 in Part 4, you are granting your representative general authority to act on your behalf regarding any tax return and any debt. However, granting your representative general authority does not give the representative the right to receive future copies of letters and notices unless Part 5 is also completed.

Part 5: Requesting copies of letters and notices with respect to a tax dispute.

NOTE: This part does not apply to City Income Tax.

If you complete Part 5, you must identify on the line in Part 5 a single tax matter that is in dispute. The dispute may cover more than one tax period or year. If you have more than one dispute with Treasury and want your representative to receive copies of future notices and letters with respect to those additional disputes, you must fill out a separate form for each dispute. Part 5 does not give a representative authority to act on your behalf. You must give your representative authority to act on your behalf by checking one or more boxes in Part 4 if you want your representative to do more than just receive future notices and letters. Only one representative can be authorized to receive future letters and notices regarding a specific tax dispute under Part 5. Treasury will only send future letters and notices to the person identified on the most recent form. If you appoint an entity as your representative, future letters and notices will be sent to the attention of the first “Contact Name.”

Deceased taxpayer. Do not use this form for a deceased taxpayer. File a Claim for Refund Due a Deceased Taxpayer

MAILING OR FAXING INSTRUCTIONS

Individual taxpayers:

Michigan Department of Treasury

Customer Contact Center

Individual Correspondence Section

P.O. Box 30058

Lansing, Ml 48909

Fax:

When Treasury Collections asks for this form and any attachments:

Michigan Department of Treasury — Coll

P.O. Box 30149

Lansing, Ml 48909

Fax:

When a Treasury field office representative asks for this form, send it as directed by that office.

For all others:

Michigan Department of Treasury

Customer Contact Center

Registration Section

P.O. Box 30778

Lansing, Ml 48909

| Fact Name | Details |

|---|---|

| Purpose | The Tax POA 151 form is used to designate a representative to handle tax matters with the IRS on behalf of the taxpayer. |

| Eligibility | Taxpayers of all types, including individuals and businesses, can use this form to appoint a representative. |

| Form Requirement | The form must be completed and submitted to authorize a representative to act on behalf of the taxpayer. |

| Governing Laws | This form is governed by federal tax law, specifically under the Internal Revenue Code. |

| Submission Process | The completed form can be submitted to the IRS along with any related tax documents or claims. |

| Validity Period | The authorization remains effective until the taxpayer revokes it or when it otherwise expires, as indicated on the form. |

| Information Required | Taxpayer's name, address, taxpayer identification number (such as Social Security Number), and the representative's information are required. |

| Signature Requirement | The taxpayer must sign the form to validate the authorization of the representative. |

| IRS Processing Time | Typically, the IRS processes the form within a few weeks, depending on the volume of submissions. |

| Revocation | A taxpayer can revoke the authorization at any time, which usually requires submitting a separate form or written notice. |

When you decide to designate someone to represent you before the IRS, preparing the Tax POA 151 form is an important step. Follow these straightforward instructions to fill out the form accurately. After completing the form, you’ll submit it to authenticate your chosen representative's authority to act on your behalf regarding tax matters.

Making sure to complete each of these steps carefully will help streamline the process. Your representative can then begin acting on your behalf once the IRS processes the form.

What is the Tax POA 151 form?

The Tax POA 151 form is a Power of Attorney document that allows you to designate someone else to represent you in tax matters before the Internal Revenue Service (IRS). This individual can be an accountant, attorney, or another trusted person. By granting this authority, you enable them to handle communication with the IRS on your behalf, which can simplify the tax process for you.

Who can I appoint using the Tax POA 151 form?

You can appoint any individual who is eligible to represent you before the IRS. This includes licensed attorneys, certified public accountants (CPAs), and enrolled agents. If you choose a friend or family member, they should have a good understanding of your tax situation to effectively assist you.

What kind of authority does the Tax POA 151 form grant?

This form grants the designated representative the ability to deal with the IRS on a variety of tax matters. Your representative can receive confidential tax information, discuss your tax account, and sign documents related to your tax return, among other responsibilities. However, the specifics of the authority can vary depending on your preferences, which can be indicated on the form.

How do I complete the Tax POA 151 form?

To complete the Tax POA 151 form, you will need to provide your personal information, including your name, Social Security number, and address. Next, you will need to enter the details of the person you wish to appoint as your representative. Be sure to review the authority you are granting to ensure it aligns with your needs. It is always advisable to double-check the information for accuracy before submitting the form.

Do I need to submit this form every year?

Generally, the Tax POA 151 form does not need to be submitted annually. Once executed, it remains valid until you revoke it or the IRS processes a termination. However, if you want to change your representative or if there’s a significant change in your tax situation, you will need to complete a new form.

Where should I send the Tax POA 151 form?

The Tax POA 151 form should be sent to the appropriate IRS office that handles your tax returns. The specific address can depend on your location and the nature of your tax matters. It’s prudent to verify the correct mailing address based on your circumstances, and always keep a copy of the submitted form for your records.

Can I revoke the Tax POA 151 form?

Yes, you can revoke the Tax POA 151 form at any time. To do so, you must send a written notice to the IRS. This notice should clearly state your intent to revoke the power of attorney and include your identifying information, as well as the information about the person you previously appointed. Maintaining control over your tax matters is important, and revocation is straightforward.

Is there a filing fee for the Tax POA 151 form?

No, there is no fee for filing the Tax POA 151 form. It is a necessary document for compliance with tax regulations, and the IRS does not charge for its submission. Therefore, you can appoint someone to assist you without incurring any additional costs.

What happens if I do not file the Tax POA 151 form?

If you do not file the Tax POA 151 form and require representation for your tax matters, the IRS will not recognize anyone else as having the authority to communicate on your behalf. This can lead to complications and misunderstandings regarding your tax obligations. It’s advisable to complete this form if you foresee needing assistance with your tax situation.

Not properly identifying the representative: People often fail to provide clear and complete information about their chosen representative. This can lead to confusion and delays in processing the power of attorney.

Missing or incorrect signatures: Many individuals forget to sign the form themselves or neglect to ensure that their representative signs it as well. An unsigned form will not be considered valid, which can create significant issues.

Providing outdated or incorrect information: It's crucial to use current contact information for both the taxpayer and the representative. Mistakes in personal details, like phone numbers or addresses, may lead to difficulties in communication.

Failure to specify the scope of authority: Some individuals do not clearly define what powers they are granting their representative. Without this specificity, the representative may not be able to act effectively on the taxpayer’s behalf.

The Tax POA 151 form is an essential tool for individuals who wish to authorize someone to represent them before the IRS. When managing tax-related matters, there are several other forms and documents that may be needed to enhance the process. Below are a few commonly used forms that complement the Tax POA 151.

Understanding these related forms can help ensure a smoother experience when dealing with tax matters. Proper documentation supports better communication and management of tax responsibilities, ensuring that individuals receive the assistance they need.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is a key document allowing individuals to appoint a representative to act on their behalf regarding tax matters. It grants the authorized agent the ability to represent the taxpayer before the IRS, similar to the Tax POA 151. This form is comprehensive and can cover multiple tax years, permitting the representative to handle various issues, including audits and appeals. Both forms aim to ease the communication between a taxpayer and tax authorities, ensuring that the taxpayer's interests are well-represented.

An additional document is the IRS Form 8821, Tax Information Authorization. This form allows a person to receive confidential tax information from the IRS without granting power of attorney like the Tax POA 151 does. Although it does not allow the individual to act on behalf of the taxpayer, it does permit the authorized individual to access necessary information. This is beneficial if someone needs to verify tax information without being involved in decision-making processes.

The Durable Power of Attorney (DPOA) serves a broader purpose than tax-specific forms. While its primary function is to grant someone authority to make decisions on behalf of another in a variety of areas (such as health care and financial decisions), it can also include tax matters. Similar to the Tax POA 151, the DPOA remains valid even if the person who created it becomes incapacitated, ensuring continued representation when it's most needed.

The Limited Power of Attorney focuses on granting specific powers for a limited time or particular purpose. This could range from handling one financial transaction to managing a particular tax situation. Like the Tax POA 151, it empowers someone to act on behalf of another, but it is often narrower in scope, which can be beneficial for particular tasks without relinquishing broad authority.

The IRS Form 8822 is a Change of Address form that allows taxpayers to update their address with the IRS. Even though it doesn't deal with representation like the Tax POA 151, it does facilitate proper communication between the taxpayer and the IRS. Keeping address information updated is crucial for receiving tax-related correspondence and ensuring that a representative can effectively act on the taxpayer’s behalf.

Lastly, a Banking Power of Attorney allows someone to manage financial accounts. It enables authorized individuals to make banking decisions, pay bills, and manage financial responsibilities. While the focus of the Tax POA 151 is strictly on tax matters, both documents share the main objective of facilitating management of important responsibilities when an individual is unable to do so themselves. Each document serves a unique function depending on the specific needs of the person granting authority.

When it comes to filling out the Tax Power of Attorney (POA) Form 151, it’s vital to proceed with caution. Here are some important do's and don'ts to keep in mind.

By following these guidelines, you can ensure a smoother process for your Tax POA Form 151 submission. Proper attention to detail can save time and prevent potential issues down the road.

The Tax Power of Attorney (POA) Form 151 is a helpful tool for individuals who wish to authorize someone else to handle their tax-related matters. However, several misconceptions can lead to confusion regarding its purpose and use. Below is a list of nine common misconceptions, along with clarifications for each.

Understanding these misconceptions can help individuals and businesses make more informed decisions regarding their tax representation needs.

When filling out and using the Tax POA 151 form, several important points should be kept in mind to ensure a smooth process.

By keeping these takeaways in mind, individuals can navigate the use of the Tax POA 151 form with greater confidence and effectiveness.