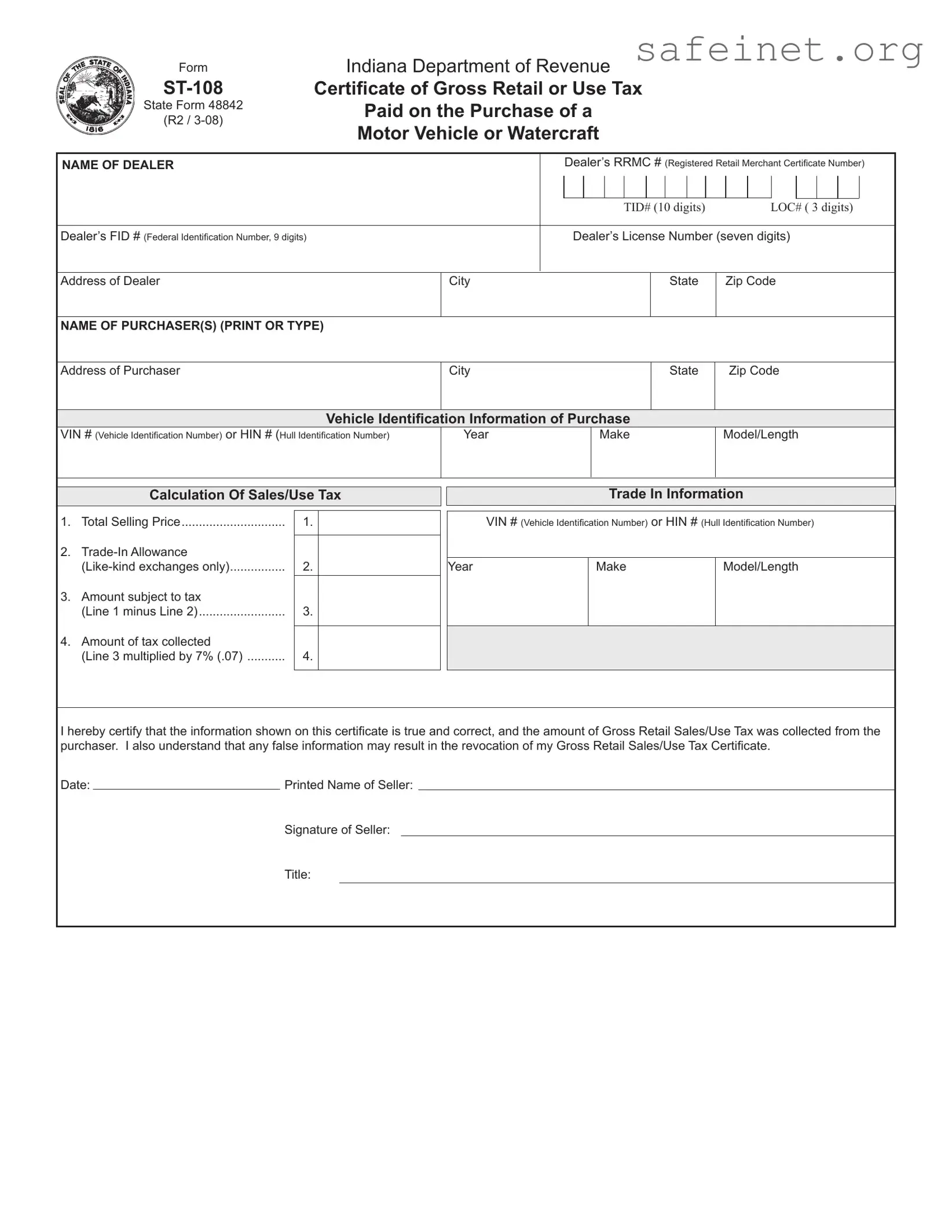

The ST-108 form is an essential document for anyone involved in the purchase of a motor vehicle or watercraft in Indiana. This certificate serves as proof that the state gross retail or use tax has been paid, a requirement set forth by Indiana law. When a buyer purchases a vehicle or watercraft from a dealer, the dealer must complete this form, detailing critical information such as the dealer’s name, identification numbers, and the purchaser’s details. The form also includes a section for vehicle identification, where the Vehicle Identification Number (VIN) or Hull Identification Number (HIN) must be recorded, along with the year, make, and model or length of the craft. Calculating the sales or use tax is another crucial aspect of the ST-108, as it requires the dealer to provide the total selling price, any trade-in allowances, and the final amount subject to tax. The tax collected is then calculated based on a rate of 7%. It’s important for both the dealer and the buyer to understand that any inaccuracies or missing information can lead to the rejection of the form, causing delays in the titling process. The seller’s signature at the end of the form confirms that the sales/use tax has been collected and will be forwarded to the Indiana Department of Revenue, ensuring compliance with state regulations.

Form

State Form 48842

(R2 /

Indiana Department of Revenue

Certificate of Gross Retail or Use Tax

Paid on the Purchase of a

Motor Vehicle or Watercraft

NAME OF DEALER |

|

|

Dealer’s RRMC # (Registered Retail Merchant Certificate Number) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TID# (10 digits) |

|

|

LOC# ( 3 digits) |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Dealer’s FID # (Federal Identification Number, 9 digits) |

|

|

Dealer’s License Number (seven digits) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Dealer |

City |

|

|

|

|

|

|

|

State |

|

Zip Code |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Purchaser(s) (pRINT OR tYPE) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Purchaser |

City |

|

|

|

|

|

|

|

State |

|

Zip Code |

||||||||

Vehicle Identification Information of Purchase

VIN # (Vehicle Identification Number) or HIN # (Hull Identification Number) |

Year |

Make |

Model/Length |

|

|

|

|

Calculation Of Sales/Use Tax

1. |

Total Selling Price |

1. |

|

2. |

|

|

|

|

2. |

|

|

3. |

Amount subject to tax |

|

|

|

(Line 1 minus Line 2) |

3. |

|

4. |

Amount of tax collected |

|

|

|

|

||

|

(Line 3 multiplied by 7% (.07) |

4. |

|

|

|

|

|

Trade In Information

VIN # (Vehicle Identification Number) or HIN # (Hull Identification Number)

Year |

Make |

Model/Length |

|

|

|

|

|

|

I hereby certify that the information shown on this certificate is true and correct, and the amount of Gross Retail Sales/Use Tax was collected from the purchaser. I also understand that any false information may result in the revocation of my Gross Retail Sales/Use Tax Certificate.

Date: |

|

Printed Name of Seller: |

|

|

|

Signature of Seller: |

|

|

|

Title: |

|

Instructions for completing Form

or Use Tax on the Purchase of a Motor Vehicle or Watercraft.

INDIANA CODE

The

If an exemption from the tax is claimed, the purchaser and the dealer must complete Form

Seller Information

NAME OF DEALER: Indicate the name of the dealer as it appears on the Registered Retail Merchant Certificate (RRMC).

FID # (Federal Identification Number): Indicate the Federal Identification Number of the dealer, if applicable.

Dealer’s License #: Indicate the Dealer’s License Number(seven digits) as it appears on the Dealer’s License Certificate.

RRMC # (same as TID # - 10 Digits + LOC # - 3 Digits): Indicate the Indiana Taxpayer Identification Number and Location Number as it appears on the Registered Retail Merchant Certificate. This number must be in the following format:

Address of Dealer: Indicate the address of the dealer as it appears on the Registered Retail Merchant Certifi- cate.

Vehicle Identification Information

VIN or HIN ID #: Enter the Vehicle ID # (VIN) or the Hull ID # (HIN).

YEAR: Indicate the year the motor vehicle or watercraft was manufactured.

MODEL # OR WATERCRAFT LENGTH: If a motor vehicle is being sold indicate the model name for the vehicle. If a watercraft is being sold indicate the length of the craft.

Calculation of Sales/Use Tax

TOTAL SELLING PRICE: When determining the total selling price include all delivery, make ready, repair, or other costs incurred prior to transfer to the buyer. Federal excise tax is NOT included.

You must also indicate the make, model, year, and ID # of the

AMOUNT SUBJECT TO TAX: Line 1 minus Line 2 results in the amount on which the sales/use tax will be calcu- lated.

AMOUNT OF TAX COLLECTED: Line 3 multiplied by 7% or .07 equals the amount to be collected by the seller.

Signature Section: The Seller must sign the

| Fact Name | Details |

|---|---|

| Purpose | The ST-108 form certifies that the gross retail or use tax has been paid on the purchase of a motor vehicle or watercraft in Indiana. |

| Governing Law | Indiana Code 6-2.5-9-6 mandates the presentation of this certification when titling a vehicle or watercraft. |

| Dealer Information | Dealers must provide their Registered Retail Merchant Certificate Number, Federal Identification Number, and License Number on the form. |

| Tax Calculation | The sales/use tax is calculated at a rate of 7% on the amount subject to tax, which is determined by subtracting any trade-in allowance from the total selling price. |

| Signature Requirement | The seller must sign the form to certify that the tax has been collected. A missing signature will lead to rejection of the form. |

| Exemption Process | If claiming an exemption, both the purchaser and dealer must complete Form ST-108E and submit it during the licensing process. |

To complete the ST-108 form, follow the steps outlined below. Ensure that all information is accurate and clearly printed or typed. After filling out the form, it should be submitted to the appropriate authority as required.

What is the purpose of the ST-108 form?

The ST-108 form is used to certify that the gross retail or use tax has been paid on the purchase of a motor vehicle or watercraft in Indiana. It must be presented when titling the vehicle or watercraft to ensure compliance with state tax laws. If this form is not provided, the purchaser will need to pay the tax directly to the Bureau of Motor Vehicles license branch.

Who is required to fill out the ST-108 form?

The dealer selling the motor vehicle or watercraft is responsible for completing the ST-108 form. The dealer must provide their information, including the Registered Retail Merchant Certificate Number, Federal Identification Number, and other relevant details. The purchaser must also provide their information and vehicle identification details.

What happens if the ST-108 form is not completed correctly?

If the ST-108 form is not filled out correctly, it may be rejected by the license branch. Common reasons for rejection include missing or incorrect identification numbers and lack of the seller's signature. If rejected, the purchaser will need to return to the dealer to obtain a valid form before they can proceed with titling the vehicle or watercraft.

What should I do if I believe I am exempt from paying the tax?

If you believe you qualify for an exemption from the sales or use tax, both you and the dealer must complete Form ST-108E. This form serves as an affidavit of exemption and lists the available exemptions. It must be submitted to the license branch at the time of licensing along with the ST-108 form.

Incorrect Dealer Information: Failing to provide the dealer's name exactly as it appears on the Registered Retail Merchant Certificate can lead to rejection.

Missing Federal Identification Number: Not including the dealer’s FID # can result in delays or issues with processing.

Improper Format for RRMC Number: The RRMC # must follow the specific format of 10 digits plus 3 digits. Errors in this format will cause the form to be rejected.

Incomplete Vehicle Identification: Omitting the Vehicle Identification Number (VIN) or Hull Identification Number (HIN) can prevent the form from being accepted.

Missing Total Selling Price: Not including all costs in the total selling price can lead to incorrect tax calculations.

Incorrect Trade-In Allowance: Providing a trade-in allowance for non-like-kind vehicles or watercraft will invalidate the exemption.

Calculation Errors: Mistakes in calculating the amount subject to tax can lead to incorrect tax amounts being reported.

Failure to Sign: Not signing the form will result in rejection by the license branch, requiring the purchaser to return for a signature.

Omitting Purchaser Information: Forgetting to fill out the name and address of the purchaser can lead to processing issues.

Not Following Instructions: Ignoring the detailed instructions provided can lead to multiple mistakes on the form.

The ST-108 form is essential for certifying that the sales or use tax has been paid on the purchase of a motor vehicle or watercraft in Indiana. Along with this form, several other documents are commonly used to facilitate the transaction and ensure compliance with state regulations. Below are four important forms that may accompany the ST-108.

Each of these documents plays a crucial role in ensuring that the transaction complies with Indiana tax laws and facilitates the smooth transfer of ownership. Understanding their purposes can help both buyers and sellers navigate the process more effectively.

Form ST-108E serves as an affidavit of exemption for purchasers claiming a tax exemption on the purchase of a vehicle or watercraft. This form must be completed by both the purchaser and the dealer at the time of licensing. It outlines the exemptions available for qualified purchases, ensuring that the necessary documentation is submitted to the Bureau of Motor Vehicles. By providing this form, the purchaser confirms their eligibility for the exemption, which helps streamline the licensing process.

Form ST-101 is a general sales tax exemption certificate used in Indiana. It allows purchasers to claim an exemption from sales tax on certain transactions, such as purchases for resale or specific exempt organizations. This form requires the purchaser to provide information about their business and the nature of the exempt purchase. Similar to the ST-108, the ST-101 facilitates the accurate collection and reporting of sales tax, ensuring compliance with state tax regulations.

Form ST-105 is a resale certificate that allows businesses to purchase goods without paying sales tax, provided those goods are intended for resale. This form requires the buyer to furnish their sales tax identification number and a description of the items being purchased. Like the ST-108, the ST-105 helps to clarify the tax obligations of both the buyer and seller, promoting transparency in transactions.

Form ST-108A is used for claiming a refund of sales tax paid on a vehicle or watercraft. This form allows purchasers to request a refund if they believe they have been overcharged or if they qualify for an exemption after the purchase. The ST-108A requires detailed information about the original purchase and the reason for the refund request. This document is essential for ensuring that taxpayers can recover funds when appropriate.

Form ST-130 is the Indiana Sales Tax Exemption Certificate for specific exempt organizations. This form is utilized by qualifying non-profit organizations to make tax-exempt purchases for their operations. It requires the organization to provide proof of its exempt status. Similar to the ST-108, the ST-130 ensures that tax exemptions are properly documented and that sellers are aware of their obligations regarding sales tax.

Form ST-140 is a tax-exempt purchase certificate that allows certain government entities to make purchases without incurring sales tax. This form is essential for ensuring that public funds are used efficiently and that government agencies can operate without the burden of sales tax on necessary purchases. The ST-140 parallels the ST-108 in its purpose of documenting tax-exempt transactions.

Form ST-102 is a form used for claiming a sales tax exemption for purchases made by certain educational institutions. This document requires the institution to provide its tax-exempt status and details about the items being purchased. Like the ST-108, the ST-102 serves to clarify the tax responsibilities of both parties in a transaction, ensuring compliance with tax laws.

Form ST-109 is utilized for reporting sales tax collected on sales of vehicles or watercraft. This form is similar to the ST-108 in that it documents the sales tax collected by the dealer from the purchaser. It requires the dealer to report the total sales and the amount of tax collected, ensuring that the appropriate funds are remitted to the state. This form plays a crucial role in maintaining accurate records for tax purposes.

When filling out the ST-108 form, it’s important to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Following these guidelines will help prevent delays and ensure a smooth transaction when purchasing a motor vehicle or watercraft in Indiana.

Understanding the ST-108 form is crucial for anyone involved in the purchase of a motor vehicle or watercraft in Indiana. Unfortunately, several misconceptions can lead to confusion and potential issues. Here are six common misunderstandings about the ST-108 form:

By dispelling these misconceptions, individuals can better navigate the process of purchasing a vehicle or watercraft in Indiana, ensuring compliance and avoiding unnecessary complications.

Here are some key takeaways about filling out and using the ST-108 form: