In South Carolina, the Promissory Note serves as a vital financial instrument that outlines the agreement between a borrower and a lender. This legally binding document details the amount borrowed, the interest rate, and the repayment schedule, ensuring both parties have a clear understanding of their obligations. Additionally, it specifies the consequences of default, providing essential protections for the lender. The form can be customized to fit various loan scenarios, whether for personal loans, business financing, or real estate transactions. By including essential elements such as payment terms, maturity date, and signatures, the Promissory Note not only facilitates trust between the parties involved but also serves as a critical tool for managing financial relationships. Understanding the nuances of this form is crucial for anyone engaging in lending or borrowing in South Carolina, as it helps to prevent disputes and fosters accountability.

South Carolina Promissory Note Template

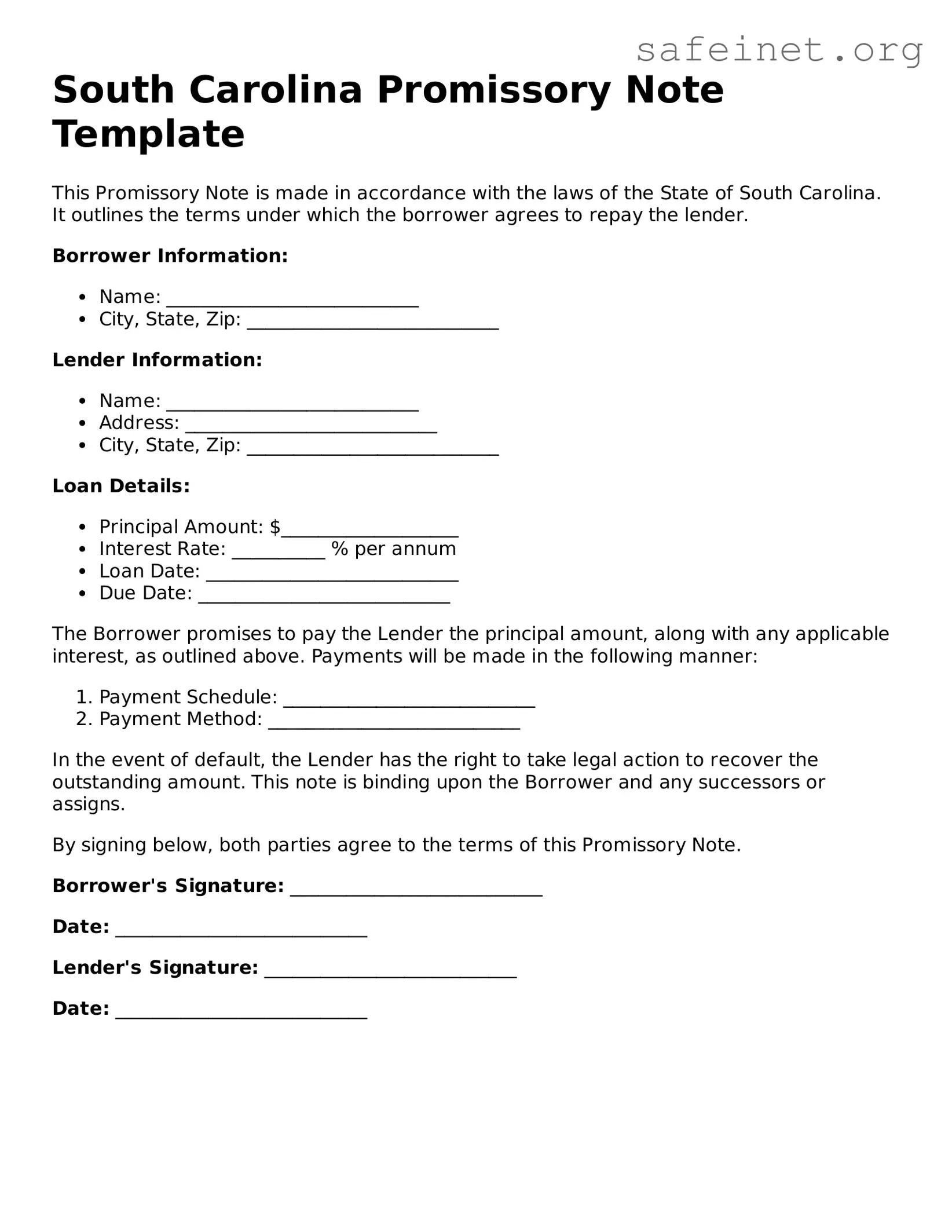

This Promissory Note is made in accordance with the laws of the State of South Carolina. It outlines the terms under which the borrower agrees to repay the lender.

Borrower Information:

Lender Information:

Loan Details:

The Borrower promises to pay the Lender the principal amount, along with any applicable interest, as outlined above. Payments will be made in the following manner:

In the event of default, the Lender has the right to take legal action to recover the outstanding amount. This note is binding upon the Borrower and any successors or assigns.

By signing below, both parties agree to the terms of this Promissory Note.

Borrower's Signature: ___________________________

Date: ___________________________

Lender's Signature: ___________________________

Date: ___________________________

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a defined time. |

| Governing Law | The South Carolina Uniform Commercial Code (UCC) governs promissory notes in South Carolina. |

| Parties Involved | The parties typically include the maker (borrower) and the payee (lender). |

| Interest Rate | The interest rate can be fixed or variable and should be clearly stated in the note. |

| Payment Terms | Payment terms should specify the due date, frequency of payments, and any grace periods. |

| Default Conditions | Conditions under which the note is considered in default must be outlined, including any applicable penalties. |

| Signatures Required | The note must be signed by the maker to be enforceable. |

| Witness or Notary | A witness or notary may be required for certain types of promissory notes to enhance enforceability. |

| Transferability | Promissory notes can typically be transferred or assigned to another party unless restricted by the terms of the note. |

| Legal Recourse | If the borrower defaults, the lender may pursue legal action to recover the owed amount. |

Filling out the South Carolina Promissory Note form is an important step in documenting a loan agreement. After completing the form, ensure that all parties involved understand their obligations and rights under the agreement. This clarity can help avoid misunderstandings in the future.

What is a South Carolina Promissory Note?

A South Carolina Promissory Note is a written agreement where one party promises to pay a specific amount of money to another party at a predetermined time or on demand. This document outlines the terms of the loan, including the interest rate, payment schedule, and any penalties for late payments.

Who uses a Promissory Note?

Individuals, businesses, and financial institutions commonly use Promissory Notes. For instance, a person borrowing money from a friend may use one to formalize the loan. Similarly, businesses may issue notes to secure financing from investors or banks.

What information is included in a South Carolina Promissory Note?

A typical Promissory Note includes the names of the borrower and lender, the loan amount, interest rate, repayment terms, and due dates. It may also specify any collateral securing the loan, as well as the consequences of default.

Is a Promissory Note legally binding?

Yes, a properly executed Promissory Note is legally binding. Both parties must agree to the terms and sign the document. This means that if the borrower fails to repay, the lender can take legal action to recover the owed amount.

Do I need a lawyer to create a Promissory Note?

While it is not required to have a lawyer, consulting one can be beneficial, especially for larger loans or complex agreements. However, many people successfully create their own Promissory Notes using templates or guides.

Can a Promissory Note be modified?

Yes, a Promissory Note can be modified if both the borrower and lender agree to the changes. It is advisable to document any modifications in writing and have both parties sign the updated agreement.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit or pursuing collections. The specific actions depend on the terms outlined in the note and state laws.

How can I ensure my Promissory Note is enforceable?

To ensure enforceability, include clear terms, have both parties sign the document, and consider having it notarized. Keeping a copy for your records is also important. Following these steps can help protect your interests in the event of a dispute.

Not including the date at the top of the form. The date is essential for establishing when the agreement takes effect.

Failing to clearly state the amount of the loan. This amount should be written both in numbers and words to avoid any confusion.

Omitting the names of the parties involved. Both the borrower and lender need to be clearly identified to ensure the agreement is enforceable.

Not specifying the interest rate. If applicable, the interest rate should be clearly stated to avoid misunderstandings later.

Ignoring the payment schedule. It is important to outline when payments are due, whether they are monthly, quarterly, or on another schedule.

Neglecting to include the consequences of default. Borrowers should be aware of what happens if they fail to make payments.

Not signing the document. Both parties must sign the Promissory Note for it to be legally binding.

Forgetting to provide witnesses or notarization, if required. Some agreements may need additional verification to be valid.

Using vague language or terms. Clear and specific language helps prevent disputes in the future.

When entering into a loan agreement in South Carolina, a Promissory Note is often accompanied by various other documents. These forms help clarify the terms of the loan, protect the interests of both parties, and ensure compliance with state laws. Below is a list of common documents that may be used alongside a South Carolina Promissory Note.

These documents play a crucial role in ensuring that both lenders and borrowers understand their rights and responsibilities. By having a comprehensive set of forms, both parties can engage in the lending process with clarity and confidence.

A South Carolina Promissory Note is closely related to a Loan Agreement. Both documents serve as a formal understanding between a borrower and a lender regarding the terms of a loan. A Loan Agreement outlines the specifics of the loan, including the amount, interest rate, and repayment schedule. While the Promissory Note focuses more on the borrower’s promise to repay, the Loan Agreement encompasses broader terms, such as collateral requirements and default provisions. Together, they provide a comprehensive view of the lending relationship.

Another document that shares similarities with a Promissory Note is a Mortgage. A Mortgage is a specific type of security agreement that involves real property. While a Promissory Note details the borrower's commitment to repay a loan, a Mortgage secures that loan with the property itself. If the borrower fails to repay, the lender can initiate foreclosure proceedings to reclaim the property. This relationship underscores the importance of both documents in real estate transactions.

A Credit Agreement also bears resemblance to a Promissory Note. This document typically outlines the terms under which a lender will extend credit to a borrower. Similar to a Promissory Note, it includes details such as loan amounts and interest rates. However, a Credit Agreement is often broader, covering various types of credit facilities, including revolving credit lines. Both documents emphasize the borrower's obligation to repay, yet the Credit Agreement may incorporate additional covenants and conditions that govern the borrower's financial conduct.

Next, consider an IOU (I Owe You). An IOU is an informal acknowledgment of a debt and shares the fundamental concept of a Promissory Note: the borrower’s promise to repay. However, unlike a Promissory Note, an IOU typically lacks detailed terms such as interest rates and repayment schedules. While both documents establish a debtor-creditor relationship, the Promissory Note is more structured and legally binding, making it a more reliable choice for formal lending situations.

A Guaranty Agreement is another document that can be compared to a Promissory Note. In a Guaranty Agreement, a third party agrees to take responsibility for the debt if the primary borrower defaults. While the Promissory Note is focused on the borrower’s promise, the Guaranty Agreement adds an extra layer of security for the lender. This relationship highlights the interconnectedness of these documents in ensuring that lenders have multiple avenues for recovery in case of default.

Lastly, a Security Agreement can be likened to a Promissory Note in that both involve a borrower’s obligation to repay a debt. A Security Agreement specifically outlines collateral that the borrower offers to secure the loan. While the Promissory Note documents the promise to repay, the Security Agreement provides the lender with rights to the collateral if the borrower fails to meet their obligations. This duality enhances the lender's protection and underscores the importance of both documents in a lending context.

When filling out the South Carolina Promissory Note form, it's important to ensure accuracy and clarity. Here are some helpful tips to consider:

By following these guidelines, you can help ensure that your Promissory Note is completed correctly and serves its intended purpose.

Understanding the South Carolina Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are nine common misconceptions about the form:

By addressing these misconceptions, individuals can better understand the role and function of the South Carolina Promissory Note form in financial transactions.

When filling out and using the South Carolina Promissory Note form, it is essential to understand several key aspects. Below are important takeaways to consider:

Understanding these points can help ensure that the promissory note serves its intended purpose and protects the interests of both the borrower and the lender.