The SBA 413 form plays a crucial role in the world of small business financing, serving as an essential tool for the U.S. Small Business Administration (SBA) loan process. This form is designed to provide a comprehensive overview of individual financial information, particularly regarding personal assets and liabilities. By requiring applicants to disclose their financial standing, the SBA can better assess the creditworthiness of those seeking loans. Additionally, the SBA 413 form aids in evaluating the overall risk involved in lending, thus safeguarding both the lender and the borrower's interests. Typically, prospective borrowers must complete this form alongside their loan application, helping ensure that all relevant financial details are readily available. Not only does this form gather necessary information about an applicant's income and expenses, but it also shines a light on their personal and business resources, offering a complete picture of their fiscal responsibility. As such, understanding this form is critical for anyone looking to secure funding to support their entrepreneurial pursuits.

. .J', |

,." su81 |

20%$33529$/12 |

" |

(;3,5$7,21'$7( |

|

~ |

. |

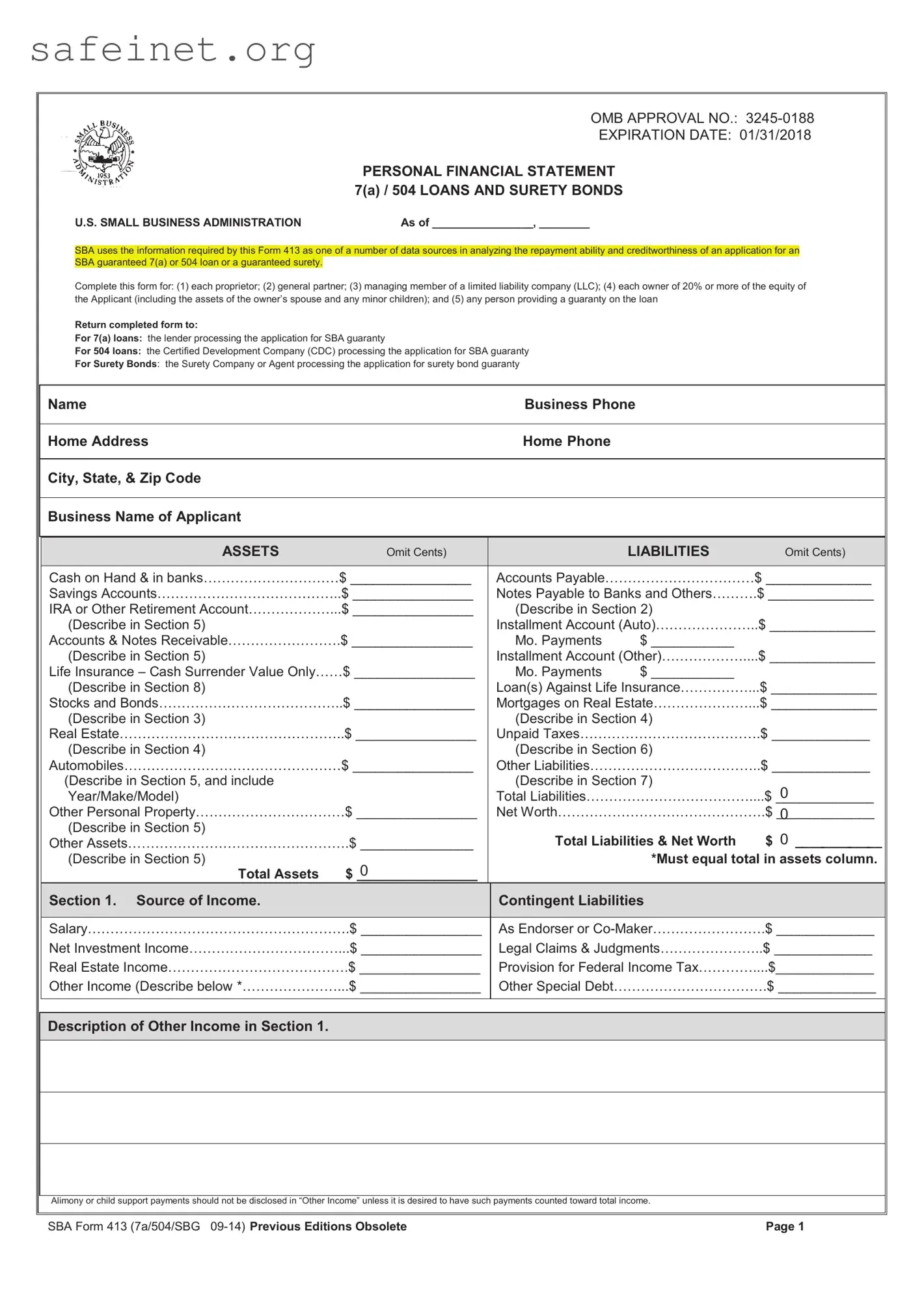

PERSONAL FINANCIAL STATEMENT |

- - |

||

|

|

7(a) / 504 LOANS AND SURETY BONDS |

U.S. SMALL BUSINESS ADMINISTRATION |

As of ________________, ________ |

|

6%$XVHVWKHLQIRUPDWLRQUHTXLUHGE\WKLV)RUPDVRQHRIDQXPEHURIGDWDVRXUFHVLQDQDO\]LQJWKHUHSD\PHQWDELOLW\DQGFUHGLWZRUWKLQHVVRIDQDSSOLFDWLRQIRUDQ 6%$JXDUDQWHHGDRUORDQRUDJXDUDQWHHGVXUHW\

|

|

|

|

|

|

|||||

|

&RPSOHWHWKLVIRUPIRUHDFKSURSULHWRUJHQHUDOSDUWQHUPDQDJLQJPHPEHURIDOLPLWHGOLDELOLW\FRPSDQ\//&HDFKRZQHURIRUPRUHRIWKHHTXLW\RI |

|||||||||

|

WKH$SSOLFDQWLQFOXGLQJWKHDVVHWVRIWKHRZQHU¶VVSRXVHDQGDQ\PLQRUFKLOGUHQDQGDQ\SHUVRQSURYLGLQJDJXDUDQW\RQWKHORDQ |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||

|

Return completed form to: |

|

|

|

|

|

|

|

|

|

|

For 7(a) loans: WKHOHQGHUSURFHVVLQJWKHDSSOLFDWLRQIRU6%$JXDUDQW\ |

|

|

|

|

|

|

|

||

|

For 504 loans:WKH&HUWLILHG'HYHORSPHQW&RPSDQ\&'&SURFHVVLQJWKHDSSOLFDWLRQIRU6%$JXDUDQW\ |

|

|

|

|

|||||

|

For Surety BondsWKH6XUHW\&RPSDQ\RU$JHQWSURFHVVLQJWKHDSSOLFDWLRQIRUVXUHW\ERQGJXDUDQW\ |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||

Name |

|

|

|

|

Business Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home Address |

|

|

|

|

Home Phone |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, State, & Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Name of Applicant |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

ASSETS2PLW&HQWV |

|

|

|

LIABILITIES |

|

2PLW&HQWV |

|

||

|

|

|

|

|

|

|

|

|

|

|

BBBBBBBBBBBBBBBB |

|

|

|

BBBBBBBBBBBBBB |

||||||

|

&DVKRQ+DQG LQEDQNV |

$FFRXQWV3D\DEOH |

|

|

||||||

|

6DYLQJV$FFRXQWV |

BBBBBBBBBBBBBBBB |

1RWHV3D\DEOHWR%DQNVDQG2WKHUV |

|

BBBBBBBBBBBBBB |

|||||

,5$RU2WKHU5HWLUHPHQW$FFRXQW |

BBBBBBBBBBBBBBBB |

'HVFULEHLQ6HFWLRQ |

|

|

|

|

||||

'HVFULEHLQ6HFWLRQ |

|

|

,QVWDOOPHQW$FFRXQW$XWR |

|

|

BBBBBBBBBBBBBB |

||||

$FFRXQWV 1RWHV5HFHLYDEOH |

BBBBBBBBBBBBBBBB |

0R3D\PHQWVBBBBBBBBBBB |

|

|

||||||

'HVFULEHLQ6HFWLRQ |

|

|

,QVWDOOPHQW$FFRXQW2WKHU |

|

|

BBBBBBBBBBBBBB |

||||

/LIH,QVXUDQFH±&DVK6XUUHQGHU9DOXH2QO\ |

BBBBBBBBBBBBBBBB |

0R3D\PHQWVBBBBBBBBBBB |

|

|

||||||

'HVFULEHLQ6HFWLRQ |

|

|

/RDQV$JDLQVW/LIH,QVXUDQFH |

|

BBBBBBBBBBBBBB |

|||||

6WRFNVDQG%RQGV |

BBBBBBBBBBBBBBBB |

0RUWJDJHVRQ5HDO(VWDWH |

|

|

BBBBBBBBBBBBBB |

|||||

'HVFULEHLQ6HFWLRQ |

|

|

|

'HVFULEHLQ6HFWLRQ |

|

|

|

|

||

5HDO(VWDWH |

BBBBBBBBBBBBBBBB |

|

8QSDLG7D[HV |

|

|

BBBBBBBBBBBBB |

||||

'HVFULEHLQ6HFWLRQ |

|

|

|

'HVFULEHLQ6HFWLRQ |

|

|

|

|

||

|

$XWRPRELOHV |

BBBBBBBBBBBBBBBB |

|

2WKHU/LDELOLWLHV |

|

|

BBBBBBBBBBBBB |

|||

|

'HVFULEHLQ6HFWLRQDQGLQFOXGH |

|

|

|

'HVFULEHLQ6HFWLRQ |

|

|

0 |

|

|

|

<HDU0DNH0RGHO |

|

|

|

7RWDO/LDELOLWLHV |

|

|

|

||

|

|

|

|

|

|

BBBBBBBBBBBBB |

||||

2WKHU3HUVRQDO3URSHUW\ |

BBBBBBBBBBBBBBBB |

1HW:RUWK |

|

|

BBBBBBBBBBBBB |

|||||

'HVFULEHLQ6HFWLRQ |

|

|

|

|

0 |

|

||||

|

|

|

|

$ 0 _____________ |

||||||

2WKHU$VVHWV |

BBBBBBBBBBBBBBB |

|

|

Total Liabilities & Net Worth |

||||||

'HVFULEHLQ6HFWLRQ |

0 |

|

|

|

*Must equal total in assets column. |

|||||

|

Total Assets |

|

|

|

|

|

|

|

|

|

|

$ ________________ |

|

|

|

|

|

|

|

|

|

|

Section 1. Source of Income. |

|

|

|

|

Contingent Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BBBBBBBBBBBBBBBB |

|

|

BBBBBBBBBBBBB |

|||||||

|

6DODU\ |

|

$V(QGRUVHURU&R0DNHU |

|

|

|||||

BBBBBBBBBBBBBBBB |

|

|

BBBBBBBBBBBBB |

|||||||

|

1HW,QYHVWPHQW,QFRPH |

|

/HJDO&ODLPV |

|

|

|||||

BBBBBBBBBBBBBBBB |

|

|

BBBBBBBBBBBBB |

|||||||

|

5HDO(VWDWH,QFRPH |

|

3URYLVLRQIRU)HGHUDO,QFRPH7D[ |

|

||||||

BBBBBBBBBBBBBBBB |

|

|

BBBBBBBBBBBBB |

|||||||

|

2WKHU,QFRPH'HVFULEHEHORZ |

|

2WKHU6SHFLDO'HEW |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Description of Other Income in Section 1.

$OLPRQ\RUFKLOGVXSSRUWSD\PHQWVVKRXOGQRWEHGLVFORVHGLQ³2WKHU,QFRPH´XQOHVVLWLVGHVLUHGWRKDYHVXFKSD\PHQWVFRXQWHGWRZDUGWRWDOLQFRPH

6%$)RUPD6%* Previous Editions Obsolete |

Page 1 |

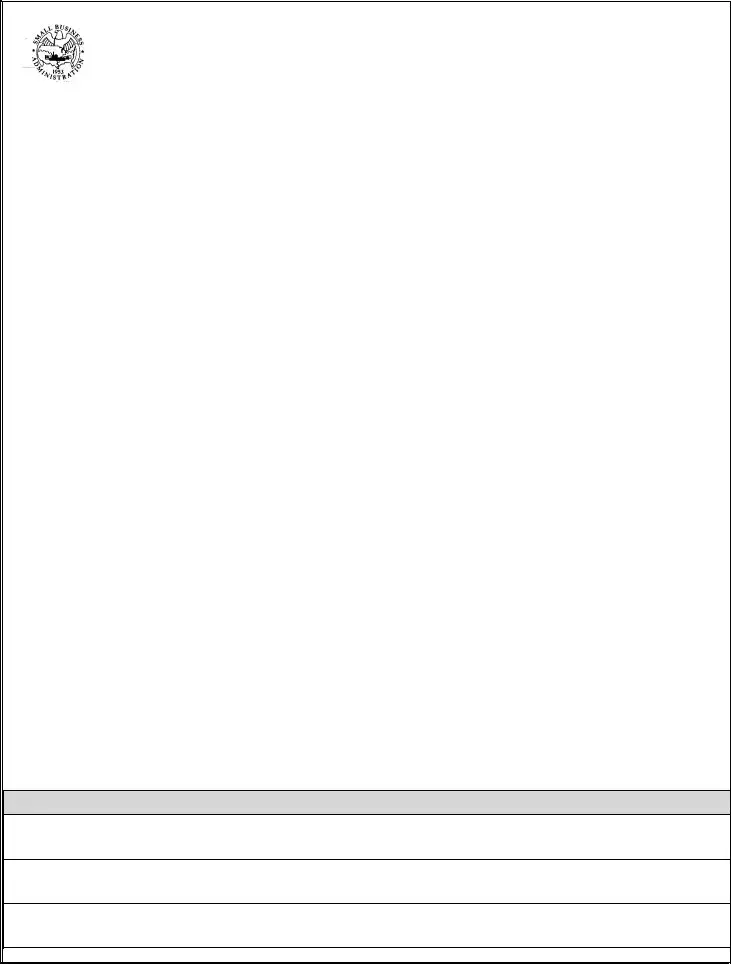

Section 2. Notes Payable to Banks and Others. 8VHDWWDFKPHQWVLIQHFHVVDU\(DFKDWWDFKPHQWPXVWEHLGHQWLILHGDVSDUWRIWKLVVWDWHPHQWDQGVLJQHG

Names and Addresses of |

Original |

Current |

Payment |

Frequency |

HoZ Secured or Endorsed |

Noteholder(s) |

Balance |

Balance |

Amount |

(monthly, etc.) |

Type of Collateral |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section 3. Stocks and Bonds. 8VHDWWDFKPHQWVLIQHFHVVDU\(DFKDWWDFKPHQWPXVWEHLGHQWLILHGDVSDUWRIWKLVVWDWHPHQWDQGVLJQHG

|

Number of Shares |

|

|

Name of Securities |

|

|

Cost |

|

|

Market Value |

|

|

Date of |

|

|

Total Value |

|

|

|

|

|

|

|

|

Quotation/Exchange |

|

|

Quotation/Exchange |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||||||||

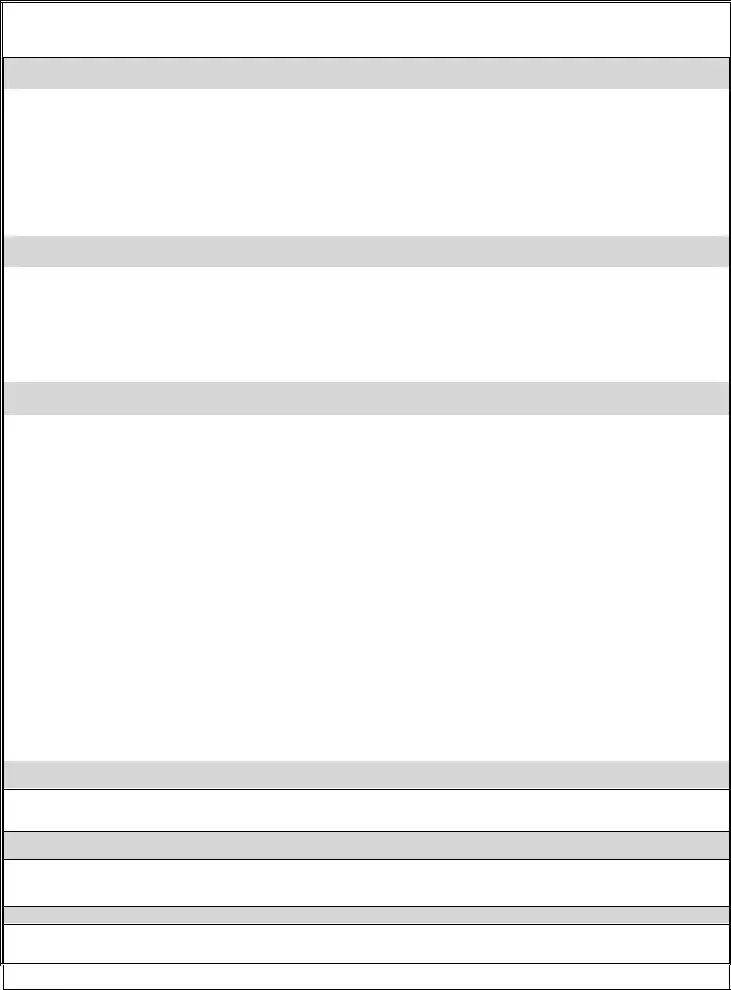

Section 4. Real Estate OZned. /LVWHDFKSDUFHOVHSDUDWHO\8VHDWWDFKPHQWLIQHFHVVDU\(DFKDWWDFKPHQWPXVWEHLGHQWLILHGDVDSDUWRIWKLVVWDWHPHQW DQGVLJQHG

|

|

Property A |

Property B |

Property C |

|

|

|

|

|

|

|

|

7\SHRI5HDO(VWDWHHJ |

|

|||

|

3ULPDU\5HVLGHQFH2WKHU |

|

|

|

|

|

5HVLGHQFH5HQWDO3URSHUW\ |

|

|

|

|

|

/DQGHWF |

|

|

|

|

|

$GGUHVV |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

'DWH3XUFKDVHG |

|

|||

|

|

|

|

|

|

|

2ULJLQDO&RVW |

|

|||

|

|

|

|

|

|

|

3UHVHQW0DUNHW9DOXH |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

1DPH $GGUHVVRI |

|

|||

|

0RUWJDJH+ROGHU |

|

|

|

|

|

|

|

|

|

|

|

0RUWJDJH$FFRXQW1XPEHU |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

0RUWJDJH%DODQFH |

|

|||

|

|

|

|

|

|

|

$PRXQWRI3D\PHQWSHU |

|

|||

|

0RQWK<HDU |

|

|

|

|

|

6WDWXVRI0RUWJDJH |

|

|||

|

|

|

|

|

|

Section 5. Other Personal Property and Other Assets. 'HVFULEHDQGLIDQ\LVSOHGJHGDVVHFXULW\VWDWHQDPHDQGDGGUHVVRIOLHQ KROGHUDPRXQWRIOLHQWHUPVRISD\PHQWDQGLIGHOLQTXHQWGHVFULEHGHOLQTXHQF\

Section 6. Unpaid Taxes. 'HVFULEHLQGHWDLODVWRW\SHWRZKRPSD\DEOHZKHQGXHDPRXQWDQGWRZKDWSURSHUW\LIDQ\DWD[ OLHQDWWDFKHV

|

|

Section 7. Other Liabilities. 'HVFULEHLQGHWDLO |

|

|

|

|

|

Page 2 |

|

6%$)RUPD6%* Previous Editions Obsolete |

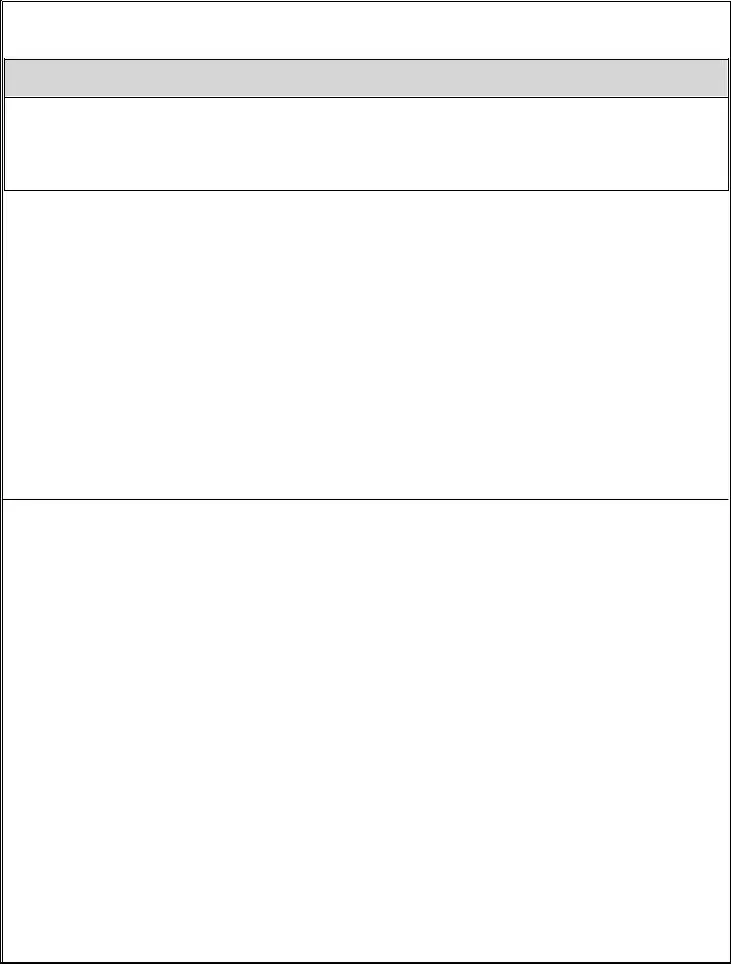

Section 8. Life Insurance Held. *LYHIDFHDPRXQWDQGFDVKVXUUHQGHUYDOXHRISROLFLHV±QDPHRILQVXUDQFHFRPSDQ\DQG %HQHILFLDULHV

,DXWKRUL]HWKH6%$/HQGHU6XUHW\&RPSDQ\WRPDNHLQTXLULHVDVQHFHVVDU\WRYHULI\WKHDFFXUDF\RIWKHVWDWHPHQWVPDGHDQGWR

GHWHUPLQHP\FUHGLWZRUWKLQHVV

CERTIFICATIONWREHFRPSOHWHGE\HDFKSHUVRQVXEPLWWLQJWKHLQIRUPDWLRQUHTXHVWHGRQWKLVIRUP

%\VLJQLQJWKLVIRUP,FHUWLI\XQGHUSHQDOW\RIFULPLQDOSURVHFXWLRQWKDWDOOLQIRUPDWLRQRQWKLVIRUPDQGDQ\DGGLWLRQDOVXSSRUWLQJ LQIRUPDWLRQVXEPLWWHGZLWKWKLVIRUPLVWUXHDQGFRPSOHWHWRWKHEHVWRIP\NQRZOHGJH,XQGHUVWDQGWKDW6%$RULWVSDUWLFLSDWLQJ /HQGHUVRU&HUWLILHG'HYHORSPHQW&RPSDQLHVRU6XUHW\&RPSDQLHVZLOOUHO\RQWKLVLQIRUPDWLRQZKHQPDNLQJGHFLVLRQVUHJDUGLQJDQ DSSOLFDWLRQIRUDORDQRUDVXUHW\ERQG,IXUWKHUFHUWLI\WKDW,KDYHUHDGWKHDWWDFKHGVWDWHPHQWVUHTXLUHGE\ODZDQGH[HFXWLYHRUGHU

6LJQDWXUHBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBB |

'DWH |

BBBBBBBBBBBBBBBBBBBB |

||

|

|

|

|

|

3ULQW1DPHBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBB |

6RFLDO6HFXULW\1RBBBBBBBBBBBBBBBBBBBB |

|||

|

|

|

|

|

|

|

|

|

|

6LJQDWXUHBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBB |

'DWH |

BBBBBBBBBBBBBBBBBBBB |

||

|

|

|

|

|

3ULQW1DPHBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBBB |

6RFLDO6HFXULW\1RBBBBBBBBBBBBBBBBBBBB |

|||

NOTICE TO LOAN AND SURETY BOND APPLICANTS: CRIMINAL PENALITIES AND ADMINISTRATIVE REMEDIES FOR FALSE STATEMENTS:

.QRZLQJO\PDNLQJDIDOVHVWDWHPHQWRQWKLVIRUPLVDYLRODWLRQRI)HGHUDOODZDQGFRXOGUHVXOWLQFULPLQDOSURVHFXWLRQVLJQLILFDQWFLYLO SHQDOWLHVDQGDGHQLDORI\RXUORDQRUVXUHW\ERQGDSSOLFDWLRQ$IDOVHVWDWHPHQWLVSXQLVKDEOHXQGHU86&DQGE\ LPSULVRQPHQWRIQRWPRUHWKDQILYH\HDUVDQGRUDILQHRIXSWRXQGHU86&E\LPSULVRQPHQWRIQRWPRUHWKDQ WZR\HDUVDQGRUDILQHRIQRWPRUHWKDQDQGLIVXEPLWWHGWRD)HGHUDOO\LQVXUHGLQVWLWXWLRQDIDOVHVWDWHPHQWLVSXQLVKDEOH XQGHU86&E\LPSULVRQPHQWRIQRWPRUHWKDQWKLUW\\HDUVDQGRUDILQHRIQRWPRUHWKDQ$GGLWLRQDOO\IDOVH VWDWHPHQWVFDQOHDGWRWUHEOHGDPDJHVDQGFLYLOSHQDOWLHVXQGHUWKH)DOVH&ODLPV$FW86&DQGRWKHUDGPLQLVWUDWLYH

UHPHGLHVLQFOXGLQJVXVSHQVLRQDQGGHEDUPHQW

3/($6(127( 7KHHVWLPDWHGDYHUDJHEXUGHQKRXUVIRUWKHFRPSOHWLRQRIWKLVIRUPLVKRXUVSHUUHVSRQVH,I\RXKDYHTXHVWLRQVRUFRPPHQWVFRQFHUQLQJWKLVHVWLPDWHRUDQ\RWKHUDVSHFWRIWKLV LQIRUPDWLRQSOHDVHFRQWDFW&KLHI$GPLQLVWUDWLYH%UDQFK866PDOO%XVLQHVV$GPLQLVWUDWLRQ:DVKLQJWRQ'&DQG&OHDUDQFHRIILFHUSDSHU5HGXFWLRQ3URMHFW2IILFH RI0DQDJHPHQWDQG%XGJHW:DVKLQJWRQ'&3/($6('21276(1')25067220%

6%$)RUPD6%* Previous Editions Obsolete |

3DJH |

PLEASE READ, DETACH, AND RETAIN FOR YOUR RECORDS

STATEMENTS REQUIRED BY LAW AND EXECUTIVE ORDER

SBA is required to withhold or limit financial assistance, to impose special conditions on approved loans, to provide special notices to applicants or borrowers and to require special reports and data from borrowers in order to comply with legislation passed by the Congress and Executive Orders issued by the President and by the provisions of various inter- agency agreements. SBA has issued regulations and procedures that implement these laws and executive orders. These are contained in Parts 112, 113, and 117 of Title 13 of the Code of Federal Regulations and in Standard Operating Procedures.

Privacy Act (5 U.S.C. 552a)

Any person can request to see or get copies of any personal information that SBA has in his or her file when that file is retrieved by individual identifiers such as name or social security numbers. Requests for information about another party may be denied unless SBA has the written permission of the individual to release the information to the requestor or unless the information is subject to disclosure under the Freedom of Information Act.

Under the provisions of the Privacy Act, you are not required to provide your social security number. Failure to provide your social security number may not affect any right, benefit or privilege to which you are entitled. Disclosures of name and other personal identifiers are, however, required for a benefit, as SBA requires an individual seeking assistance from SBA to provide it with sufficient information for it to make a character determination. In determining whether an individual is of good character, SBA considers the person’s integrity, candor, and disposition toward criminal actions. Additionally, SBA is specifically authorized to verify your criminal history, or lack thereof, pursuant to section 7(a)(1)(B), 15 USC Section 636(a)(1)(B) of the Small Business Act ( the Act). Further, for all forms of assistance, SBA is authorized to make all investigations necessary to ensure that a person has not engaged in acts that violate or will violate the Act or the Small Business Investment Act, 15 USC Sections 634(b)(11) and 687(b)(a), respectively. For these purposes, you are asked to voluntarily provide your social security number to assist SBA in making a character determination and to distinguish you from other individuals with the same or similar name or other personal identifier.

The Privacy Act authorizes SBA to make certain “routine uses” of information protected by that Act. One such routine use is the disclosure of information maintained in SBA’s investigative files system of records when this information indicates a violation or potential violation of law, whether civil, criminal, or administrative in nature. Specifically, SBA may refer the information to the appropriate agency, whether Federal, State, local or foreign, charged with responsibility for, or otherwise involved in investigation, prosecution, enforcement or prevention of such violations. Another routine use is disclosure to other Federal agencies conducting background checks; only to the extent the information is relevant to the requesting agencies' function. See, 74 F.R. 14890 (2009), and as amended from time to time for additional background and other routine uses.

Right to Financial Privacy Act of 1978 (12 U.S.C. 3401)

Freedom of Information Act (5 U.S.C. 552)

This law provides, with some exceptions, that SBA must supply information reflected in agency files and records to a person requesting it. Information about approved loans that will be automatically released includes, among other things, statistics on our loan programs (individual borrowers are not identified in the statistics) and other information such as the names of the borrowers (and their officers, directors, stockholders or partners), the collateral pledged to secure the loan, the amount of the loan, its purpose in general terms and the maturity. Proprietary data on a borrower would not routinely be made available to third parties. All requests under this Act are to be addressed to the nearest SBA office and be identified as a Freedom of Information request.

Flood Disaster Protection Act (42 U.S.C. 4011)

6%$)RUPD6%*Previous Editions Obsolete |

Page 4 |

Executive Orders

Occupational Safety and Health Act (15 U.S.C. 651 et seq.)

Civil Rights Legislation

Equal Credit Opportunity Act (15 U.S.C. 1691)

Executive Order 11738

Debt Collection Act of 1982, Deficit Reduction Act of 1984 (31 U.S.C. 3701 et seq. and other titles)

(4)suspend or debar you or your company from doing business with the Federal Government, (5) refer your loan to the Department of Justice or other attorneys for litigation, or (6) foreclose on collateral or take other action permitted in the loan instruments.

Immigration Reform and Control Act of 1986 (Pub. L.

Borrowers using SBA funds for the construction or rehabilitation of a residential structure are prohibited from using lead- based paint (as defined in SBA regulations) on all interior surfaces, whether accessible or not, and exterior surfaces, such as stairs, decks, porches, railings, windows and doors, which are readily accessible to children under 7 years of age. A "residential structure" is any home, apartment, hotel, motel, orphanage, boarding school, dormitory, day care center, extended care facility, college or other school housing, hospital, group practice or community facility and all other residential or institutional structures where persons reside.

Executive Order 12549, Debarment and Suspension 2 CFR 2700

1.The borrower or contractor certifies, by submission of its application for an SBA loan or bond guarantee, that neither it nor its principals are presently debarred, suspended, proposed for debarment, declared ineligible, or voluntarily excluded from participation in this transaction by any Federal department or agency.

2.Where the prospective lower tier participant is unable to certify to any of the statements in this certification, such prospective participants shall attach an explanation to the application.

6%$)RUPD6%*Previous Editions Obsolete |

Page 5 |

| Fact Name | Detail |

|---|---|

| Purpose | The SBA 413 form is primarily used for personal financial statements required by the Small Business Administration. |

| Impacted Business Types | This form is necessary for various types of small businesses seeking SBA loans, including sole proprietorships, partnerships, and corporations. |

| Required Information | Individuals must provide detailed information concerning assets, liabilities, and income. |

| Filing Requirement | Submission of the SBA 413 is often mandatory when applying for specific SBA loan programs. |

| Signature Requirement | Applicants must sign the form, certifying that the information provided is accurate and complete. |

| Length of Validity | The information on the form should reflect the applicant's financial status as of a recent date, typically within the last 90 days. |

| Confidentiality | Financial information submitted through this form is treated with confidentiality but may be reviewed by authorized parties. |

| Governing Law | The form is governed by federal law as it pertains to SBA financial documentation. |

After gathering the necessary information about your financial situation, you can begin filling out the SBA Form 413. This form is essential for providing the Small Business Administration with a comprehensive overview of your personal financial status. It typically requires you to provide details about your assets, liabilities, income, and other relevant financial data.

What is the SBA 413 form used for?

The SBA 413 form, also known as the Personal Financial Statement, helps individuals provide a clear picture of their financial situation. It is primarily used by the Small Business Administration (SBA) as part of the loan application process. This form allows lenders to assess your financial health and determine your eligibility for business loans.

Who needs to fill out the SBA 413 form?

If you're applying for an SBA loan, you typically need to complete the SBA 413 form. This includes anyone with a significant ownership stake in the business. Whether you are a sole proprietor, partner, or have a shareholding interest in an LLC, the SBA wants to understand your financial background.

What information is required on the SBA 413 form?

The SBA 413 form asks for various financial details, including your assets, liabilities, income, and expenses. You will need to list personal assets like cash, real estate, and investments. It's also essential to include any debts or obligations you may have. This comprehensive snapshot helps lenders evaluate your financial standing.

How do I fill out the SBA 413 form accurately?

To fill out the SBA 413 form accurately, gather all relevant financial documents beforehand. This can include bank statements, investment accounts, property appraisals, and loan statements. Take your time to fill out each section, ensuring that all numbers are correct and match your documentation. Accuracy is key to avoid delays in your loan application.

What if my financial situation changes after I submit the SBA 413 form?

If your financial situation changes after you've submitted the SBA 413 form, it’s important to communicate this to your lender as soon as possible. Major changes could include a significant increase or decrease in income, acquiring new debts, or selling assets. Keeping your lender informed helps maintain transparency and may prevent complications with your loan process.

Where can I obtain the SBA 413 form?

You can find the SBA 413 form on the U.S. Small Business Administration's official website. The form is typically available in PDF format, which you can download, print, and fill out. It's also a good idea to check the site for any updates or changes to the form and its requirements.

The SBA 413 form, also known as the Personal Financial Statement, is a crucial document when applying for loans through the Small Business Administration. Mistakes on this form can lead to delays or even denials of financing. Here are five common mistakes individuals make when completing this important form:

Many people fill out parts of the form and neglect other sections. Every section is important and contributes to the overall picture of your financial situation.

Providing inaccurate numbers can greatly affect the evaluation of your financial health. Ensure that all values are correct and reflect what you actually own or owe.

Sometimes, individuals forget to include necessary documents like bank statements or tax returns. These documents can be vital in verifying the information provided on the form.

Financial situations change, and it’s essential to keep the form current. Outdated information could misrepresent your current financial status, leading to potential issues with your application.

Every form comes with specific instructions. Not following these could lead to misinterpretations and errors that might complicate the approval process.

Taking your time to carefully fill out the SBA 413 form can help ensure accuracy and improve your chances of getting the support you need for your business.

The SBA 413 form, used primarily for reporting personal financial information for Small Business Administration (SBA) loan applications, often accompanies several other important forms and documents. Each of these documents serves a specific purpose in ensuring that the application process is thorough and accurate. Below is a list of commonly used documents alongside the SBA 413 form.

Submitting the right documents alongside the SBA 413 form not only streamlines the loan application process but also enhances the chances of approval. Ensuring that all forms are completed accurately and submitted in a timely manner is crucial for a successful application. Each item plays a vital role in painting a complete picture of the applicant’s financial status and business viability.

The SBA Form 413, often referred to as the Personal Financial Statement, serves as a crucial tool for the Small Business Administration (SBA) when assessing applicants’ financial backgrounds. Similar to the IRS Form 4506-T, this document allows applicants to request a transcript of their tax returns. Both forms require detailed financial information that the SBA can compare to the applicant’s submitted data. This similarity ensures that the lender can verify the income figures provided on the personal financial statement, leading to a more reliable portrayal of the applicant’s financial status.

Another document that holds a resemblance to the SBA 413 is the Uniform Commercial Code (UCC) Financing Statement. While the SBA 413 focuses on personal financial details, the UCC statement serves to provide lenders with insight into the assets that borrowers might use as collateral for loans. In both cases, the aim is to secure financing through transparency regarding the borrowers' financial situation and the potential risks associated with lending money.

The Personal Statement of Financial Condition is also akin to the SBA 413 form. It is typically used in the context of mortgage applications. Like the SBA 413, this document asks individuals to disclose their assets, liabilities, and overall financial health. Both documents aim to provide lenders with an up-to-date snapshot of an applicant's finances to help determine the risk associated with the financing request.

Moreover, the Credit Application form can be seen as another document similar to the SBA 413. Individuals are often required to complete a credit application when seeking loans or credit cards, listing their assets and liabilities. Like the SBA 413, this application helps lenders evaluate an individual's creditworthiness by assessing their financial condition and obligations.

The Net Worth Statement is yet another form that lines up with the SBA 413. This document allows individuals to summarize their financial status by outlining total assets and subtracting liabilities. Both the Net Worth Statement and the SBA 413 are designed to give lenders a clear picture of an individual's financial landscape to inform lending decisions.

In the realm of personal loans, a Loan Application Form is also comparable to the SBA 413. A loan application typically requests information regarding an individual’s income, assets, and debts. Just as the SBA 413 details a person's financial situation, the loan application serves to evaluate the borrower's ability to repay the debt, aiding lenders in making informed choices.

The Statement of Affairs is another document relevant to personal financial disclosure. Similar to the SBA 413, this form outlines an individual’s debts, assets, and overall financial condition, often as part of bankruptcy proceedings. Both documents aim to provide a comprehensive review of a person's financial obligations and resources for clearer financial insights.

The Financial Disclosure Statement is another key document that aligns with the SBA 413. Professionals, especially in legal contexts like divorce or bankruptcy, must provide such a statement, detailing their financial standing. Just like the SBA 413, this form is a way to ensure all financial information is disclosed to facilitate fair dealings in various financial arrangements.

The Business Loan Application is yet another form that shares similarities with the SBA 413. While this application is tailored for businesses seeking financing, it still requires detailed financial information from the owners, much like the personal financial statement. Both documents allow lenders to evaluate the financial background of applicants and make informed lending decisions.

Finally, the Business Financial Statement serves as a counterpart to the SBA 413 in the business arena. This document focuses on the financials of a business rather than an individual, but both require a detailed overview of assets and liabilities. In each instance, the goal is to assess financial stability and creditworthiness before approving financing.

When filling out the SBA 413 form, it’s essential to approach it with care. Here’s a list of what you should and shouldn’t do to ensure a smooth experience.

Taking these steps can enhance your chances of a successful application process. It’s about being prepared and informed!

The SBA 413 form is an essential document for business owners seeking financial assistance from the Small Business Administration (SBA). However, several misconceptions surround its purpose and usage. Here are five common misunderstandings about the SBA 413 form:

This is false. The SBA 413 form is relevant for businesses of all sizes, including startups. Any current or prospective business owner may need to complete it to secure financing.

While the form does involve business financials, it also requires personal financial information. This includes details about the owner's assets and liabilities, ensuring a comprehensive evaluation of both the business and its proprietor.

Unfortunately, this is not true. The SBA 413 form is just one part of the loan application process. Approval depends on multiple factors, including creditworthiness and the overall business plan.

Submitting incomplete or inaccurately filled forms can lead to delays or denials. To prevent complications, applicants should ensure that all information and supporting documents are complete and accurate.

New entrepreneurs must also file this form when seeking loans. It helps lenders assess both the personal and business financial stability of applicants, regardless of their business's maturity.

The SBA 413 form, officially known as the Personal Financial Statement, is an important tool for individuals seeking financial assistance through the Small Business Administration. Below are key takeaways to consider when filling out and using this form.

By understanding these key points, you can approach the SBA 413 form with confidence and accuracy, maximizing your chances of securing the financial assistance you need.