When purchasing a car, financing options often include a promissory note, a vital document that outlines the borrower's promise to repay the loan. This form serves as a crucial agreement between the borrower and the lender, specifying important details like the loan amount, interest rate, and repayment schedule. Additionally, it indicates any collateral involved—in this case, the vehicle itself. Such a note can help protect both parties, outlining the consequences of missed payments or default while also providing a legal framework for recovering the owed amount. Understanding how to fill out this form accurately ensures that all terms are clear, fostering a stable financial relationship. As you consider signing a promissory note for a car, familiarize yourself with its key components and implications, so you can navigate your purchase with confidence.

Promissory Note for a Car

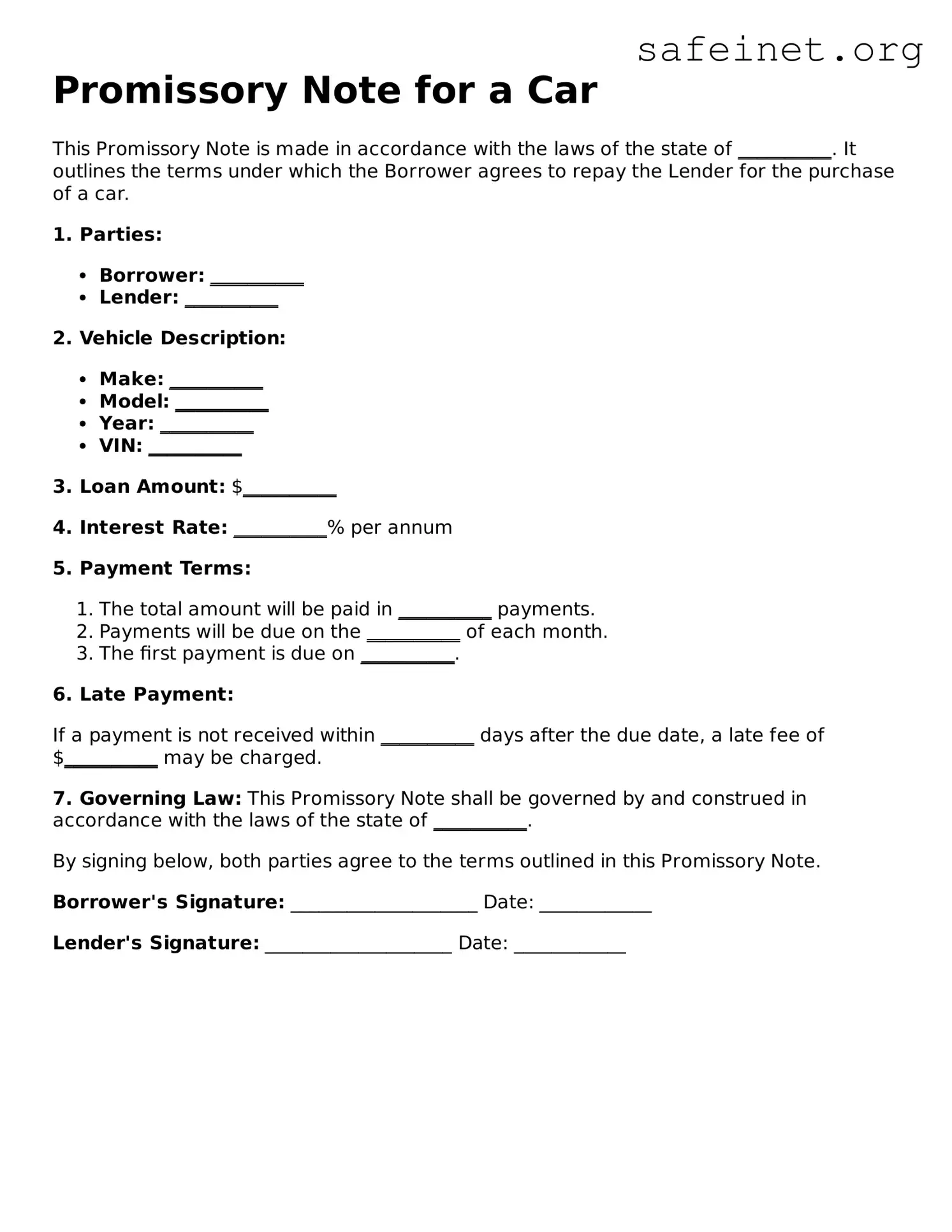

This Promissory Note is made in accordance with the laws of the state of __________. It outlines the terms under which the Borrower agrees to repay the Lender for the purchase of a car.

1. Parties:

2. Vehicle Description:

3. Loan Amount: $__________

4. Interest Rate: __________% per annum

5. Payment Terms:

6. Late Payment:

If a payment is not received within __________ days after the due date, a late fee of $__________ may be charged.

7. Governing Law: This Promissory Note shall be governed by and construed in accordance with the laws of the state of __________.

By signing below, both parties agree to the terms outlined in this Promissory Note.

Borrower's Signature: ____________________ Date: ____________

Lender's Signature: ____________________ Date: ____________

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a legal document in which one party promises to pay another party a specified amount in a given timeframe for the purchase of a vehicle. |

| Purpose | This note serves as a record of the loan agreement between the buyer and the seller, establishing the terms under which the car is financed. |

| Governing Laws | Laws governing promissory notes can vary by state. In many states, the Uniform Commercial Code (UCC) provides the framework for these agreements. |

| Essential Elements | Typically, a valid promissory note must include the date, amount, interest rate, repayment schedule, and signatures of both parties. |

| Collateral | The vehicle itself often serves as collateral in case of default, allowing the lender to reclaim it if payments are not made. |

| Enforceability | A properly executed promissory note can be enforced in court, meaning that failure to pay can lead to legal actions to recover the owed amount. |

After you have gathered your information, you can proceed to fill out the Promissory Note for a Car form. It is important to ensure that all details are accurate and clearly written. A complete and correct form helps in providing clear terms to everyone involved.

Following these steps will ensure that your Promissory Note for a Car form is filled out correctly, establishing clear terms for both the borrower and the lender.

What is a Promissory Note for a Car?

A Promissory Note for a Car is a legal document that outlines a borrower's promise to repay a loan used to purchase a vehicle. This document includes details such as the amount borrowed, the interest rate, the repayment schedule, and any consequences for failure to make payments. It serves as a written acknowledgment of the debt and can be enforced in a court of law if necessary.

Why do I need a Promissory Note for a Car?

A Promissory Note is essential for both the lender and borrower. For the lender, it provides security by clearly documenting the terms of the loan. For the borrower, it establishes a formal record of their obligation, which can help prevent misunderstandings in the future. Having this document in place can also facilitate communication regarding payments and any potential changes to the repayment plan.

What information should be included in the Promissory Note?

The Promissory Note should include the following information: the names and contact information of both parties, a detailed description of the vehicle, the loan amount, the interest rate, the repayment terms, due dates for payments, and the consequences of default. It is also wise to include any specific conditions or clauses that pertain to the agreement.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified, but any changes must be agreed upon by both parties. This typically involves creating an amendment to the original note, which should be signed and dated by both the borrower and lender. It’s crucial to ensure that all modifications are clear and legally binding to prevent any disputes in the future.

What happens if I default on the Promissory Note?

If a borrower defaults, meaning they fail to make timely payments as specified in the Promissory Note, the lender has several options. Depending on the terms outlined in the note, the lender may seek to recover the remaining balance, repossess the vehicle, or take legal action. It’s essential for borrowers to communicate with their lenders if they anticipate difficulty in making payments to find potential solutions before default occurs.

Failing to provide accurate personal information can lead to complications. Ensure your full name, address, and contact details are correct.

Not specifying the loan amount clearly is a common error. State the exact dollar amount you are borrowing.

Forgetting to include the interest rate can create confusion. State whether the rate is fixed or variable, and provide the percentage.

Omitting the repayment schedule is another mistake. Clearly outline how often payments will be made and the duration of the loan.

Neglecting to include any fees or additional costs can lead to disputes. Itemize any applicable fees as part of the total repayment.

Filling out the document without proper signatures can invalidate the agreement. Ensure all parties sign and date the note appropriately.

Not keeping a copy of the signed note for your records can result in future issues. Always retain a copy for reference.

A Promissory Note for a Car serves as a formal agreement between the borrower and lender regarding the loan taken out to purchase a vehicle. This document outlines the terms of repayment and any interest applicable. However, there are several additional forms and documents that typically accompany this agreement, providing further clarity and security for both parties involved.

Each of these documents plays a crucial role in the transaction involving a car purchase. They not only protect the interests of both the buyer and seller but also ensure that the transaction adheres to legal standards. Keeping these documents organized is advisable for a smooth and transparent car purchase process.

The Promissory Note for a Car form bears similarities to the Car Loan Agreement. Both documents serve to outline the borrower's promise to repay the borrowed money for the vehicle. These agreements usually detail the loan amount, interest rate, repayment schedule, and any penalties for late payments. By defining the terms clearly, both documents help protect the lender’s interests while informing the borrower of their obligations.

Another document that mirrors aspects of the Promissory Note is the Auto Lease Agreement. Unlike a loan, an auto lease agreement allows the borrower to use the vehicle for a specified period without the intention of ownership. However, similar to a promissory note, this agreement also specifies payment terms, including monthly lease amounts and penalties for missed payments, thus establishing a formal financial commitment.

The Retail Installment Sales Contract is another similar document. This contract is often used when purchasing a car where financing is involved. It not only lists the purchase price and down payment but also covers the payment schedule, interest rates, and personal obligations of the buyer. Like a promissory note, this document formalizes the financial relationship between the buyer and the lender.

The Secured Loan Agreement is also relevant because it involves borrowing against collateral—in this case, the car itself. This agreement, like a promissory note, details the terms of the loan, including the borrower's obligations and the lender's rights in the event of default. The security interest in the vehicle provides an extra layer of protection for the lender, paralleling the core function of the promissory note.

The Conditional Sales Contract shows another similarity, as it allows the buyer to take possession of the vehicle while making payments. In essence, though the buyer uses the car, full ownership does not transfer until the total purchase price is paid. This conditional arrangement mirrors the promise of repayment found in a promissory note, reinforcing the financial commitment made by the buyer.

Next, consider the Loan Application Form, which initiates the borrowing process. It asks for vital information such as income, credit history, and employment status, enabling the lender to assess the borrower's ability to repay. Though not a financial commitment itself, this document is the precursor to a promissory note, leading to the establishment of formal repayment terms.

Then there’s the Vehicle Title, which signifies ownership of the vehicle in question. When a promissory note is created, the title often serves as collateral for the loan, providing the lender an avenue to reclaim the vehicle if the borrower defaults. Thus, while the title itself is not a financial agreement, it underlines the obligations outlined in the promissory note.

The Bill of Sale, although more transactional, holds noteworthy similarities as it documents the sale of the vehicle and the terms agreed upon between the seller and buyer. It may include payment terms, much like a promissory note, establishing a clear mutual understanding of the financial exchange involved in acquiring the car.

Finally, the Payment Plan Agreement is akin to a promissory note as it explicitly defines the repayment terms agreed upon by both parties. This document outlines the payment amount, schedule, and any consequences for late payments, essentially guiding the borrower through their financial commitments similar to how a promissory note delineates the borrower's obligations for repaying the car loan.

When filling out a Promissory Note for a car, certain actions can ensure the process goes smoothly. Here is a list of things to do and avoid:

When it comes to understanding the Promissory Note for a Car form, some common misconceptions can lead to confusion. Let's clear up a few of them.

By understanding these misconceptions, individuals can navigate the financial side of purchasing a car with greater confidence.

Filling out and using a Promissory Note for a car is an important step when financing a vehicle purchase. Here are some key takeaways to consider:

Promissory Note Paid in Full Template - Allows both parties to move forward without lingering obligations.