Understanding the Profit and Loss form is essential for anyone involved in managing finances, whether for a small business or a larger enterprise. This form serves as a crucial tool for tracking income and expenses over a specific period, providing a clear snapshot of financial performance. It typically includes key components such as revenue, cost of goods sold, gross profit, operating expenses, and net profit or loss. By analyzing these elements, business owners and stakeholders can gain insights into profitability, identify trends, and make informed decisions about future investments or cost-cutting measures. Moreover, the Profit and Loss form plays a vital role in budgeting and forecasting, helping organizations set realistic financial goals. Ultimately, mastering this form can empower individuals to navigate the financial landscape with confidence and clarity.

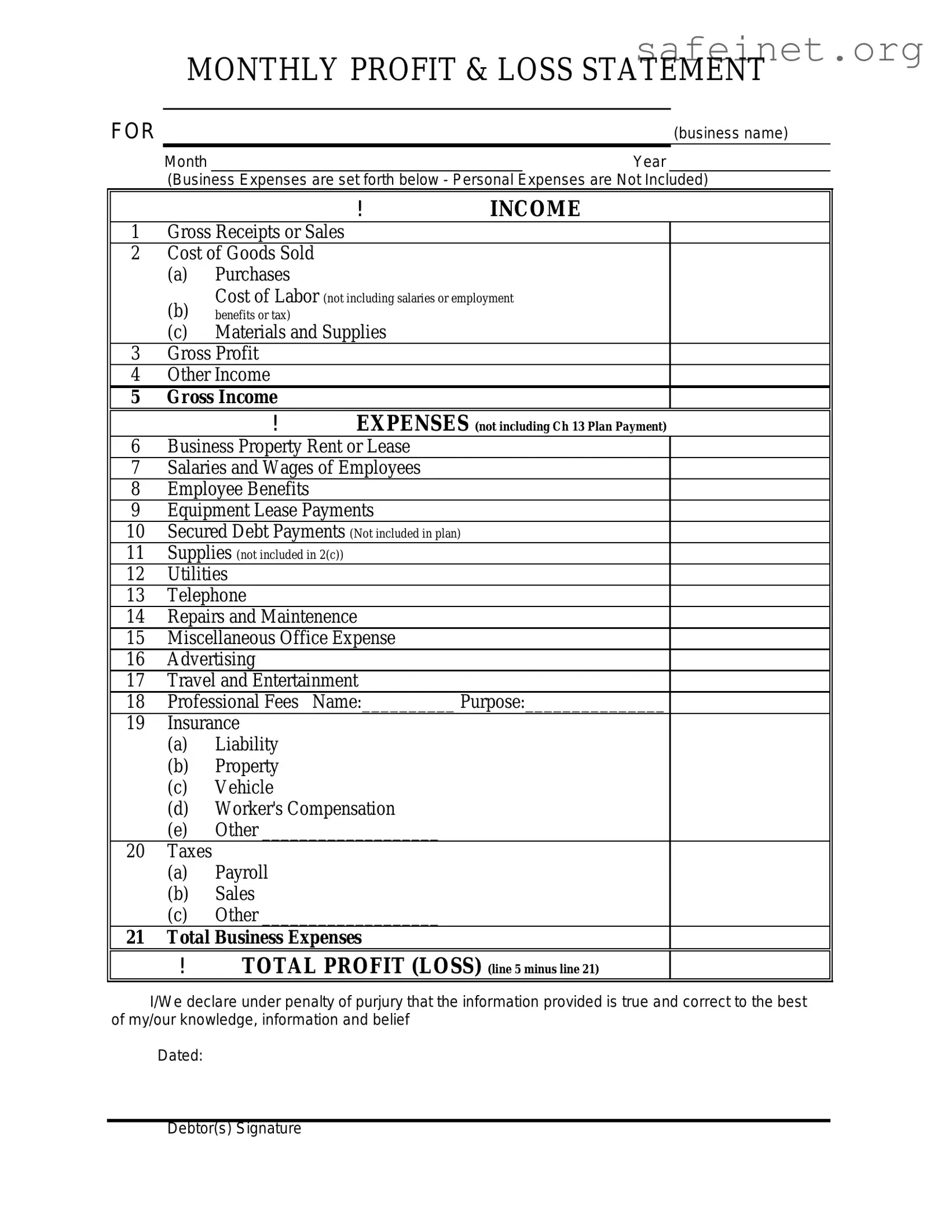

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form is used to summarize revenues, costs, and expenses over a specific period, providing insights into a business's financial performance. |

| Components | This form typically includes sections for gross revenue, cost of goods sold, operating expenses, and net profit or loss. |

| State-Specific Forms | Some states require specific Profit and Loss forms. For example, California follows the California Corporations Code, while New York adheres to the New York Business Corporation Law. |

| Filing Requirements | Businesses may be required to submit the Profit and Loss form with their annual tax returns, depending on state regulations and business structure. |

After gathering your financial information, you are ready to fill out the Profit And Loss form. This form will help you summarize your income and expenses over a specific period. Completing it accurately is crucial for understanding your business's financial health.

What is a Profit and Loss form?

A Profit and Loss form, often referred to as a P&L statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period, typically a fiscal quarter or year. It provides a clear overview of a company's financial performance, showing whether it has made a profit or incurred a loss during that time frame.

Why is the Profit and Loss form important?

This form is crucial for various stakeholders, including business owners, investors, and lenders. It helps assess the company's profitability, operational efficiency, and overall financial health. By analyzing the P&L statement, stakeholders can make informed decisions regarding investments, budgeting, and strategic planning.

What are the main components of a Profit and Loss form?

The primary components of a Profit and Loss form include revenues (or sales), cost of goods sold (COGS), gross profit, operating expenses, and net profit or loss. Revenues represent the total income generated from sales, while COGS reflects the direct costs associated with producing goods sold. Gross profit is calculated by subtracting COGS from revenues. Operating expenses include overhead costs, and net profit is derived by subtracting total expenses from total revenues.

How often should a Profit and Loss form be prepared?

Typically, businesses prepare a Profit and Loss form on a monthly, quarterly, or annual basis. Monthly reports can provide timely insights into financial performance, while quarterly and annual reports are often used for more comprehensive analysis and reporting to stakeholders.

Who prepares the Profit and Loss form?

Generally, the accounting department or a financial professional within a company prepares the Profit and Loss form. In smaller businesses, the owner may handle this task. It’s essential for the individual preparing the P&L statement to have a good understanding of accounting principles to ensure accuracy.

Can the Profit and Loss form be used for tax purposes?

Yes, the Profit and Loss form is often used for tax reporting. It provides a detailed account of income and expenses, which is necessary for calculating taxable income. However, businesses should consult with a tax professional to ensure compliance with tax regulations and to maximize deductions.

How can I analyze my Profit and Loss form?

Analyzing a Profit and Loss form involves looking at key metrics such as gross profit margin, operating profit margin, and net profit margin. Comparing these metrics over different periods can reveal trends in profitability. Additionally, benchmarking against industry standards can help assess how well the business is performing relative to competitors.

What should I do if my Profit and Loss form shows a loss?

If the Profit and Loss form indicates a loss, it’s important to investigate the underlying causes. Review expenses to identify areas where costs can be reduced. Consider strategies to increase revenue, such as enhancing marketing efforts or diversifying product offerings. Consulting with a financial advisor can also provide valuable insights on how to improve financial performance.

Failing to categorize income and expenses correctly. Proper categorization is essential for accurate reporting.

Omitting certain income sources. All revenue streams should be included to reflect the true financial position.

Not keeping receipts or documentation. Without proof of expenses, it becomes difficult to validate claims.

Using estimates instead of actual figures. Estimates can lead to inaccuracies and misrepresent the financial status.

Neglecting to update the form regularly. Regular updates ensure that the information remains current and reliable.

Forgetting to account for one-time expenses. These costs can significantly impact the overall profit and loss.

Not reviewing the completed form for errors. A thorough review can catch mistakes before submission.

Overlooking the importance of net profit calculations. Understanding net profit is crucial for assessing business performance.

Failing to consult with a financial advisor when necessary. Professional guidance can help avoid common pitfalls.

Ignoring tax implications of reported income and expenses. Awareness of tax consequences can influence financial decisions.

The Profit and Loss form is a crucial document for any business, providing a snapshot of income and expenses over a specific period. However, it is often accompanied by several other forms and documents that together offer a comprehensive view of a company's financial health. Below is a list of commonly used documents alongside the Profit and Loss form.

Together, these documents provide a holistic view of a business's financial situation. They are essential for effective management, strategic planning, and compliance with regulatory requirements.

The Profit and Loss statement, often referred to as the income statement, is similar to the balance sheet in that both documents provide crucial insights into a company's financial health. While the Profit and Loss statement focuses on revenues and expenses over a specific period, the balance sheet presents a snapshot of a company’s assets, liabilities, and equity at a single point in time. Together, these documents offer a comprehensive view of a business's financial performance and position, allowing stakeholders to assess profitability and financial stability.

The cash flow statement is another document closely related to the Profit and Loss statement. While the Profit and Loss statement summarizes income and expenses, the cash flow statement details the actual cash generated and used during a specific period. This distinction is vital; a company may report a profit but still face cash flow challenges. Understanding both documents helps stakeholders evaluate not just profitability, but also liquidity and the ability to meet obligations.

Finally, the budget variance report serves as a comparative tool against the Profit and Loss statement. While the Profit and Loss statement reflects actual performance, the budget variance report compares this performance against the budgeted figures. This analysis allows businesses to identify discrepancies, assess operational efficiency, and make informed decisions for future planning. Both documents work together to provide a clearer picture of financial performance relative to expectations.

When filling out the Profit and Loss form, it's important to keep a few key points in mind. Here’s a list of things you should and shouldn't do:

Following these guidelines can help ensure that your Profit and Loss form is filled out correctly and effectively.

The Profit and Loss (P&L) form is a critical tool for understanding a business's financial health. However, several misconceptions surround it. Let’s clarify these common misunderstandings.

In reality, the P&L outlines both revenues and expenses. It provides a complete picture of how much money a business is making or losing over a specific period.

A positive net income is a good sign, but it doesn’t tell the whole story. Cash flow, debt levels, and other factors also play crucial roles in a company's overall health.

Small businesses benefit just as much from a P&L statement. It helps them track performance and make informed decisions about growth and expenses.

Regularly updating the P&L, such as monthly or quarterly, helps businesses stay on top of their financial situation and make timely adjustments.

Expenses are categorized into operating and non-operating. Understanding these distinctions helps businesses analyze their core operations more effectively.

Depreciation is crucial as it reflects the wear and tear on assets over time. It affects net income and provides a more accurate view of profitability.

The P&L is directly tied to taxes. Net income reported on the P&L is often the basis for calculating tax liabilities.

These are distinct financial statements. While the P&L summarizes income and expenses, the balance sheet provides a snapshot of assets, liabilities, and equity at a specific point in time.

While there are differences, certain metrics like gross profit margin can be compared across industries, providing valuable insights into performance.

External parties, such as investors and lenders, also rely on P&L statements to assess a business's viability and profitability before making decisions.

Understanding these misconceptions can empower business owners and stakeholders to use the Profit and Loss form more effectively, leading to better financial decision-making.

When filling out and using the Profit and Loss form, several important points should be kept in mind to ensure accuracy and effectiveness. Here are some key takeaways: