In the realm of personal and business finance, the Oregon Promissory Note serves as a crucial document that outlines the terms of a loan agreement between a borrower and a lender. This form establishes the borrower's promise to repay a specified sum of money, detailing essential components such as the principal amount, interest rate, repayment schedule, and any applicable fees. It also highlights the rights and responsibilities of both parties, ensuring clarity and reducing the potential for disputes. Whether used for personal loans, real estate transactions, or business financing, this document plays a vital role in protecting the interests of the lender while providing the borrower with a clear understanding of their obligations. Additionally, the Oregon Promissory Note may include provisions for late payments and default scenarios, further safeguarding the lender's investment. Understanding the intricacies of this form is essential for anyone engaging in financial agreements in Oregon, as it lays the groundwork for a transparent and legally binding relationship.

Oregon Promissory Note Template

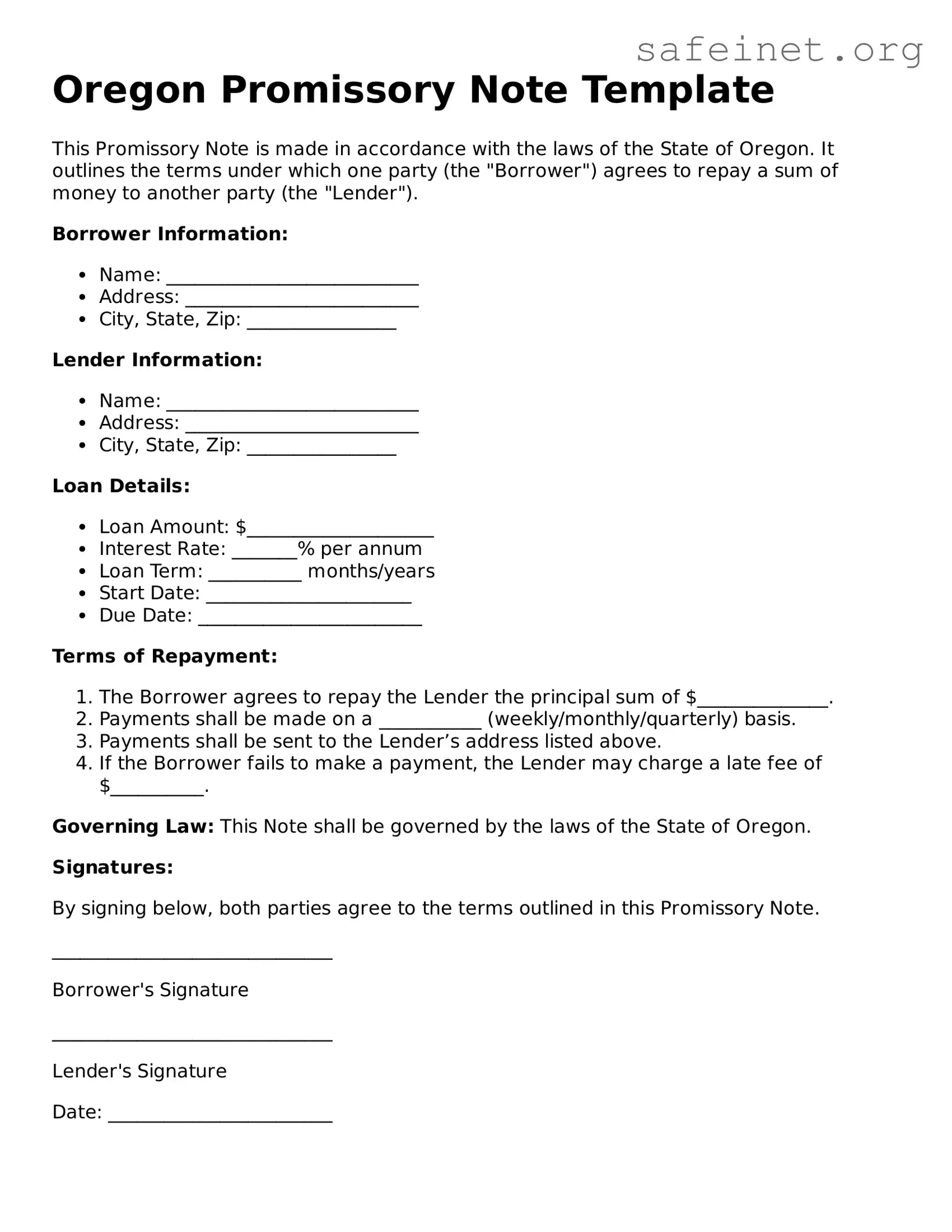

This Promissory Note is made in accordance with the laws of the State of Oregon. It outlines the terms under which one party (the "Borrower") agrees to repay a sum of money to another party (the "Lender").

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Governing Law: This Note shall be governed by the laws of the State of Oregon.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

______________________________

Borrower's Signature

______________________________

Lender's Signature

Date: ________________________

| Fact Name | Details |

|---|---|

| Definition | An Oregon Promissory Note is a written promise to pay a specific amount of money to a designated person or entity. |

| Governing Law | Oregon Revised Statutes, specifically ORS Chapter 73. |

| Parties Involved | The borrower (maker) promises to pay the lender (payee). |

| Payment Terms | The note should specify the amount to be paid, interest rate, and payment schedule. |

| Interest Rate | The interest rate can be fixed or variable, and it must comply with state usury laws. |

| Signatures | Both the borrower and lender must sign the note for it to be legally binding. |

| Enforceability | Promissory notes are legally enforceable as long as they meet certain requirements. |

| Default Terms | The note should outline what happens in case of default, including any penalties or fees. |

| Transferability | Promissory notes can be transferred or sold to another party unless otherwise stated. |

| Record Keeping | It is advisable for both parties to keep a copy of the signed note for their records. |

Once you have the Oregon Promissory Note form in hand, it’s time to fill it out carefully. Make sure you have all the necessary information ready, as this will help you complete the form accurately. Follow these steps to ensure everything is filled out correctly.

After completing the form, make sure to keep a copy for your records. You may need to present this document in the future, so having a copy on hand is essential.

What is a Promissory Note in Oregon?

A Promissory Note is a written agreement in which one party promises to pay a specific amount of money to another party under agreed-upon terms. In Oregon, this document serves as a legal instrument that outlines the borrower's obligation to repay a loan, including details such as the loan amount, interest rate, and repayment schedule.

Who can use a Promissory Note in Oregon?

Any individual or business can use a Promissory Note in Oregon. This includes personal loans between friends or family members, as well as business loans between companies. It is important that both parties understand the terms and conditions set forth in the document.

What information should be included in an Oregon Promissory Note?

An effective Promissory Note should include the names and addresses of both the borrower and lender, the principal amount of the loan, the interest rate, the repayment schedule, and any collateral involved. Additionally, it should specify the consequences of default and any applicable fees.

Is a Promissory Note legally binding in Oregon?

Yes, a Promissory Note is legally binding in Oregon as long as it meets certain requirements. Both parties must agree to the terms, and the document should be signed and dated. For added protection, it is advisable to have the document notarized.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified if both the borrower and lender agree to the changes. It is best to document any modifications in writing and have both parties sign the updated agreement to avoid misunderstandings in the future.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may involve filing a lawsuit or pursuing collection efforts. The specifics of the default consequences should be clearly outlined in the Promissory Note to prevent disputes.

Do I need a lawyer to create a Promissory Note in Oregon?

While it is not legally required to have a lawyer draft a Promissory Note, consulting with a legal professional can provide valuable guidance. A lawyer can help ensure that the document complies with Oregon laws and adequately protects your interests.

Where can I find a template for an Oregon Promissory Note?

Templates for Oregon Promissory Notes can be found online through legal form websites, or you can create your own using a reliable template as a guide. Ensure that any template used is compliant with Oregon laws and meets your specific needs.

Failing to include the correct names of the borrower and lender. It is essential that both parties are clearly identified to avoid confusion later.

Not specifying the loan amount clearly. The amount should be written in both numbers and words to prevent any discrepancies.

Omitting the interest rate. If applicable, the interest rate must be stated explicitly. This ensures both parties understand the cost of borrowing.

Neglecting to define the repayment terms. Clearly outline when payments are due and how they should be made. This helps prevent misunderstandings.

Forgetting to include any collateral details. If the loan is secured, the collateral must be described in the note to protect the lender’s interests.

Not having the document notarized. While not always required, notarization adds a layer of authenticity and can be important for legal purposes.

Failing to keep a copy of the signed note. Both parties should retain a copy of the signed document for their records to ensure clarity and accountability.

The Oregon Promissory Note form is a key document in lending transactions, outlining the borrower's promise to repay a loan under specified terms. Several other forms and documents are often used in conjunction with this note to ensure clarity and legal compliance in the lending process. Below is a list of these commonly associated documents.

These documents play a vital role in the lending process, providing necessary protections and clarifications for both borrowers and lenders. Understanding each document's purpose can facilitate smoother transactions and help avoid potential disputes.

The Oregon Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedule. While a promissory note is a simpler, more straightforward document, a loan agreement often includes additional clauses regarding collateral, default, and other legal considerations. Both serve to protect the lender's interests while providing a clear understanding of the borrower's obligations.

A Mortgage Agreement is another document that resembles the Oregon Promissory Note. While a promissory note is primarily a promise to pay, a mortgage agreement secures that promise with real property as collateral. Both documents detail the loan terms, but the mortgage agreement provides the lender with the right to foreclose on the property if the borrower defaults. This adds a layer of security for the lender beyond the promissory note itself.

The Secured Promissory Note is similar in that it also includes a promise to pay but is backed by collateral. This collateral can be any asset of value that the borrower agrees to forfeit if they fail to meet their payment obligations. The secured promissory note provides additional protection for the lender, making it a more secure option compared to an unsecured promissory note.

An Unsecured Promissory Note is another related document. Unlike a secured note, it does not involve collateral. The borrower simply promises to repay the loan amount without the backing of any asset. While both types of promissory notes outline the terms of the loan, the unsecured version carries more risk for the lender, as there is no asset to claim in the event of default.

A Personal Loan Agreement is similar to the Oregon Promissory Note in that it outlines the terms under which money is borrowed. This document typically includes information about the loan amount, interest rate, and repayment schedule. Unlike a promissory note, a personal loan agreement may also include additional terms related to the borrower's creditworthiness and responsibilities.

A Business Loan Agreement shares similarities with the Oregon Promissory Note as well. It details the terms of a loan made to a business entity rather than an individual. Both documents specify the loan amount, interest rate, and repayment terms. However, a business loan agreement may include specific conditions related to the business's financial performance and obligations.

A Lease Agreement can also be compared to a promissory note, particularly when a lease involves a payment structure similar to a loan. Both documents outline the payment terms and obligations of the parties involved. However, a lease agreement typically pertains to the rental of property, while a promissory note is focused on the repayment of borrowed funds.

Finally, a Debt Settlement Agreement is similar in that it involves the resolution of a financial obligation. This document outlines the terms under which a debtor agrees to pay a reduced amount to settle a debt. While a promissory note represents a promise to pay a specific amount, a debt settlement agreement often involves negotiation and compromise between the debtor and creditor, marking a different approach to resolving financial obligations.

When filling out the Oregon Promissory Note form, it’s essential to ensure accuracy and clarity. Here are some important dos and don’ts to keep in mind:

By following these guidelines, you can help ensure that your Promissory Note is completed accurately and effectively.

When it comes to the Oregon Promissory Note form, there are several misconceptions that can lead to confusion. Understanding these misconceptions is crucial for anyone involved in lending or borrowing money in Oregon.

Many people believe that notarization is a requirement for a promissory note to be legally binding. In Oregon, a promissory note does not need to be notarized to be enforceable. However, having it notarized can provide additional proof of authenticity.

Some individuals think that they can write vague terms in a promissory note. In reality, the note must clearly outline the terms of the loan, including the amount, interest rate, and repayment schedule, to avoid disputes later on.

While both documents relate to borrowing money, they are not identical. A promissory note is a simple promise to pay back a loan, while a loan agreement typically includes more detailed terms and conditions.

Some borrowers assume that lenders can charge any interest rate they choose. In Oregon, there are usury laws that limit the maximum interest rates that can be charged, protecting borrowers from excessively high rates.

Many people think that once a promissory note is created, it cannot be sold or transferred. In fact, promissory notes are often negotiable instruments, meaning they can be transferred to another party.

Some believe that a verbal agreement is enough to create a binding obligation. However, a written promissory note is essential for clarity and enforceability, as oral agreements can lead to misunderstandings and disputes.

Filling out and using the Oregon Promissory Note form can seem daunting, but understanding a few key points can make the process smoother. Here are some essential takeaways:

By keeping these points in mind, you can create a promissory note that serves its purpose effectively and protects your interests.