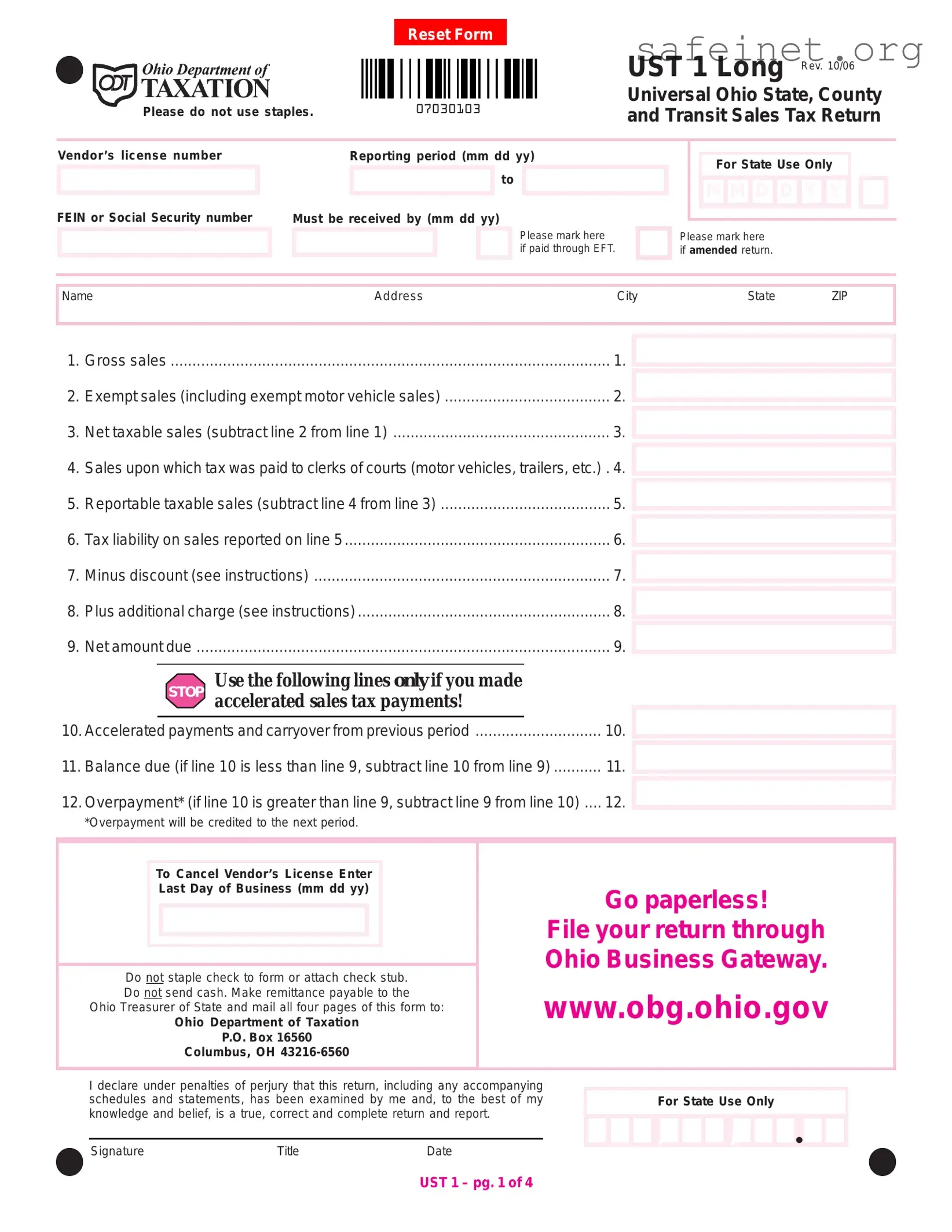

The Ohio Sales Tax UST 1 form is a critical document for vendors operating within the state, as it facilitates the accurate reporting of sales tax obligations. This form requires essential information, including the vendor's license number, FEIN or Social Security number, and the reporting period. Vendors must detail their gross sales, exempt sales, and net taxable sales, ensuring that all figures are correctly calculated to reflect their tax liability. Additional sections address sales upon which tax has already been paid, allowing for adjustments that impact the final amount due. If applicable, vendors can indicate whether the return is amended or if payment is made electronically. The form also includes a section for those who need to cancel their vendor's license, along with instructions for remittance. To streamline the process, vendors are encouraged to file electronically through the Ohio Business Gateway. Accurate completion of the UST 1 form is essential to avoid penalties and ensure compliance with state tax regulations.

|

|

|

|

|

|

|

|

|

Reset Form |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UST 1 Long Rev. 10/06 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Universal Ohio State, County |

|

07030103 |

|

|

|

|

|

|

||||||||||||||||||||||||||||

Please do not use staples. |

|

|

|

|

|

|

|

|

|

|

|

and Transit Sales Tax Return |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Vendor’s license number

FEIN or Social Security number

Reporting period (mm dd yy)

to

Must be received by (mm dd yy)

Please mark here if paid through EFT.

For State Use Only

MM D D Y Y

Please mark here if amended return.

NameAddressCityState ZIP

1. |

Gross sales |

1. |

2. |

Exempt sales (including exempt motor vehicle sales) |

2. |

3. |

Net taxable sales (subtract line 2 from line 1) |

3. |

4. |

Sales upon which tax was paid to clerks of courts (motor vehicles, trailers, etc.) . 4. |

|

5. |

Reportable taxable sales (subtract line 4 from line 3) |

5. |

6. |

Tax liability on sales reported on line 5 |

6. |

7. |

Minus discount (see instructions) |

7. |

8. |

Plus additional charge (see instructions) |

8. |

9. |

Net amount due |

9. |

|

Use the following lines only if you made |

|

|

|

STOP accelerated sales tax payments! |

|

|

10. Accelerated payments and carryover from previous period |

10. |

||

11. Balance due (if line 10 is less than line 9, subtract line 10 from line 9) |

11. |

||

12. Overpayment* (if line 10 is greater than line 9, subtract line 9 from line 10) .... |

12. |

||

*Overpayment will be credited to the next period.

To Cancel Vendor’s License Enter

Last Day of Business (mm dd yy)

Do not staple check to form or attach check stub. Do not send cash. Make remittance payable to the

Ohio Treasurer of State and mail all four pages of this form to:

Ohio Department of Taxation

P.O. Box 16560

Columbus, OH

Go paperless!

File your return through Ohio Business Gateway.

www.obg.ohio.gov

I declare under penalties of perjury that this return, including any accompanying schedules and statements, has been examined by me and, to the best of my knowledge and belief, is a true, correct and complete return and report.

Signature |

Title |

Date |

For State Use Only

, ,

UST 1 – pg. 1 of 4

Please do not use staples. Vendor’s license number

UST 1 Long Rev. 10/06

Universal Ohio State, County and Transit Sales Tax Return

Supporting schedule must be completed showing taxable sales and the combined state, county and transit authority taxes on a

County Name |

County Number |

|

|

Taxable Sales* |

|

|

Tax Liability* |

|||

*If this amount is a negative, please mark an “X” in the box provided. |

||||||||||

|

|

|||||||||

Adams |

01 |

|

|

|

|

|

|

|

|

|

Allen |

02 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Ashland |

03 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Ashtabula |

04 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Athens |

05 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Auglaize |

06 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Belmont |

07 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Brown |

08 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Butler |

09 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Carroll |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Champaign |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Clark |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Clermont |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Clinton |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Columbiana |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Coshocton |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Crawford |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Cuyahoga |

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Darke |

19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Defiance |

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Delaware |

21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Delaware (COTA) |

96 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Erie |

22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Fairfield |

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Fairfield (COTA) |

93 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Fayette |

24 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Franklin |

25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Fulton |

26 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Gallia |

27 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Geauga |

28 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Greene |

29 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Guernsey |

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Hamilton |

31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 2 subtotal

UST 1 – pg. 2 of 4

Please do not use staples. Vendor’s license number

UST 1 Long Rev. 10/06

Universal Ohio State, County and Transit Sales Tax Return

Supporting schedule must be completed showing taxable sales and the combined state, county and transit authority taxes on a

County Name |

County Number |

|

|

Taxable Sales* |

|

|

Tax Liability* |

|||

*If this amount is a negative, please mark an “X” in the box provided. |

||||||||||

|

|

|||||||||

Hancock |

32 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Hardin |

33 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Harrison |

34 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Henry |

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Highland |

36 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Hocking |

37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Holmes |

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Huron |

39 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Jackson |

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Jefferson |

41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Knox |

42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Lake |

43 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Lawrence |

44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Licking |

45 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Licking (COTA) |

94 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Logan |

46 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Lorain |

47 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Lucas |

48 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Madison |

49 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Mahoning |

50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Marion |

51 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Medina |

52 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Meigs |

53 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Mercer |

54 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Miami |

55 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Monroe |

56 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Montgomery |

57 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Morgan |

58 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Morrow |

59 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Muskingum |

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Noble |

61 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Ottawa |

62 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Paulding |

63 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Page 3 subtotal

UST 1 – pg. 3 of 4

|

|

|

|

|

|

|

|

|

|

|

Reset Form |

||||||||||||||

Please do not use staples. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

07030403 |

|

||||||||||||||||||||||||

Vendor’s license number |

Reporting period (mm dd yy) |

||||||||||||||||||||||||

to

UST 1 Long Rev. 10/06

Universal Ohio State, County and Transit Sales Tax Return

Supporting schedule must be completed showing taxable sales and the combined state, county and transit authority taxes on a

County Name |

County Number |

|

|

Taxable Sales* |

|

|

Tax Liability* |

|||

*If this amount is a negative, please mark an “X” in the box provided. |

||||||||||

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

Perry |

64 |

|

|

|

|

|

|

|

|

|

Pickaway |

65 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Pike |

66 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Portage |

67 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Preble |

68 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Putnam |

69 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Richland |

70 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Ross |

71 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Sandusky |

72 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Scioto |

73 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Seneca |

74 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Shelby |

75 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Stark |

76 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Summit |

77 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Trumbull |

78 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Tuscarawas |

79 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Union |

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Van Wert |

81 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Vinton |

82 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Warren |

83 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Washington |

84 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Wayne |

85 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Williams |

86 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Wood |

87 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Wyandot |

88 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Subtotal this page

Page 2 subtotal

Page 3 subtotal

Grand total*

*Enter totals on lines 5 and 6 on the front page of this return.

UST 1 – pg. 4 of 4

| Fact Name | Details |

|---|---|

| Form Title | Ohio Sales Tax UST 1 Form |

| Purpose | This form is used to report state, county, and transit sales tax for vendors operating in Ohio. |

| Filing Frequency | Vendors must file the UST 1 form for each reporting period, typically on a monthly or quarterly basis. |

| Governing Law | Ohio Revised Code Chapter 5739 governs sales tax reporting and compliance in Ohio. |

| Vendor Information | Vendors are required to provide their vendor license number and FEIN or Social Security number on the form. |

| Payment Options | Payments can be made electronically through the EFT option or by check, but cash is not accepted. |

| Deadline for Submission | The completed form must be received by the Ohio Department of Taxation by the specified due date for the reporting period. |

Completing the Ohio Sales Tax UST 1 form requires careful attention to detail. The form collects information about gross sales, exempt sales, and tax liabilities among other data. Properly filling out this form ensures compliance with state tax regulations and helps avoid penalties.

Once you have completed the form, ensure that all information is accurate and clear. Review the form for any potential errors before mailing it to avoid delays or complications with your tax filing.

What is the Ohio Sales Tax UST 1 form used for?

The Ohio Sales Tax UST 1 form is used by businesses to report sales tax collected during a specific reporting period. It includes details about gross sales, exempt sales, and net taxable sales. Completing this form allows businesses to calculate their tax liability and submit the appropriate payment to the Ohio Department of Taxation.

How do I fill out the UST 1 form correctly?

To fill out the UST 1 form, start by entering your vendor's license number and the reporting period. You will need to provide information on gross sales, exempt sales, and taxable sales. Make sure to subtract exempt sales from gross sales to find net taxable sales. Additionally, report any sales tax paid on specific items like motor vehicles. Follow the instructions for calculating discounts and additional charges, and ensure you sign the form before submission.

What should I do if I made an error on my UST 1 form?

If you discover an error after submitting your UST 1 form, you can file an amended return. Mark the appropriate box on the form to indicate that it is an amended return. Make sure to provide the correct information and submit it by the due date to avoid penalties. Keep in mind that any adjustments will affect your reported tax liability.

How can I submit my UST 1 form?

You can submit your UST 1 form either by mail or electronically. If you choose to mail it, send all four pages of the completed form to the Ohio Department of Taxation, along with your payment. Do not staple your check to the form. Alternatively, you can file your return online through the Ohio Business Gateway for a more streamlined process.

Incorrect Vendor License Number: Entering an incorrect vendor license number can lead to processing delays or rejections. Ensure that the number matches the one issued by the Ohio Department of Taxation.

Missing Reporting Period: Failing to fill in the reporting period can result in confusion and complications. Clearly state the start and end dates in the designated fields.

Inaccurate Calculation of Taxable Sales: Miscalculating taxable sales, especially when subtracting exempt sales from gross sales, is a common error. Double-check all figures to ensure accuracy.

Failure to Sign the Form: Not signing the form can lead to it being deemed invalid. Always ensure that you provide your signature, title, and date at the bottom of the form.

The Ohio Sales Tax UST 1 form is essential for reporting sales tax collected by vendors. Alongside this form, several other documents may be required to ensure compliance with state tax regulations. Below is a list of commonly used forms and documents that complement the UST 1 form.

Understanding and preparing these documents will help ensure accurate reporting and compliance with Ohio sales tax laws. If you have any questions about these forms, seeking assistance can provide clarity and peace of mind.

The Ohio Sales Tax UST 1 form is similar to the IRS Form 941, which is used by employers to report payroll taxes. Both forms require detailed reporting of specific financial information, including taxable amounts. Just as the UST 1 form outlines gross sales and tax liabilities, Form 941 includes wages paid and taxes withheld. Each form serves to ensure compliance with tax regulations, providing necessary information to the respective authorities for proper assessment and collection.

Another comparable document is the Ohio Employer Withholding Tax Return (Form IT-1). This form is utilized by employers to report state income tax withheld from employees' wages. Like the UST 1, it requires accurate reporting of financial data and is subject to deadlines. Both forms help state agencies track tax revenues and ensure that businesses fulfill their tax obligations in a timely manner.

The Sales and Use Tax Return (Form ST-1) is another document that shares similarities with the UST 1 form. This form is specifically for businesses that collect sales tax on goods sold or services rendered. Both forms require reporting of gross sales and exemptions, making them essential for businesses to comply with state tax laws. The ST-1 focuses on sales tax collection, while the UST 1 encompasses a broader range of sales and transit taxes.

Additionally, the Federal Excise Tax Return (Form 720) is comparable in that it requires businesses to report specific types of taxes. Both forms involve calculating tax liabilities based on sales figures. While the UST 1 is state-specific, Form 720 deals with federal excise taxes, highlighting the importance of accurate reporting at different levels of government.

The Annual Report (Form D-1) for corporations is another document that bears resemblance to the UST 1 form. Corporations use this form to report their financial performance to state authorities. Both require detailed financial disclosures and are crucial for maintaining compliance with state regulations. Each form serves as a means of transparency and accountability for businesses operating within Ohio.

The Ohio Business Tax Return (Form BTA) also aligns with the UST 1 in terms of its purpose to report business taxes. This form collects information on various business taxes, much like the UST 1 collects sales tax data. Both forms are essential for businesses to ensure they are meeting their tax responsibilities and providing accurate information to the state.

Another similar document is the Ohio Individual Income Tax Return (Form IT-1040). This form is for individuals reporting their income tax, while the UST 1 is for businesses reporting sales tax. Both require careful calculation of tax liabilities based on reported figures, emphasizing the importance of accuracy in tax reporting for compliance purposes.

The Ohio Corporate Franchise Tax Return (Form FT) shares similarities with the UST 1 form as well. This form is used to report taxes owed by corporations based on their income. Both forms require businesses to calculate their tax liabilities accurately and submit them to the state. Each serves as a critical tool for tax collection and compliance monitoring.

Lastly, the Ohio Use Tax Return is akin to the UST 1 form in that it addresses tax obligations for items purchased out of state. Both forms require businesses to report taxable transactions and calculate corresponding tax liabilities. This ensures that all sales and use taxes are accounted for, maintaining fairness in the taxation system.

When filling out the Ohio Sales Tax UST 1 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things to do and avoid:

By following these guidelines, you can help ensure that your sales tax return is processed smoothly and efficiently.

Misconception 1: The UST 1 form is only for large businesses.

This is not true. The UST 1 form is required for all vendors who sell taxable goods or services in Ohio, regardless of their size. Small businesses must also comply with sales tax regulations and submit the form to report their sales accurately.

Misconception 2: I do not need to file if I had no sales during the reporting period.

Misconception 3: I can submit my payment without filing the form.

This is incorrect. The UST 1 form must be completed and submitted along with any payment due. The form provides essential information about the sales and tax liability, which the state needs to process the payment correctly.

Misconception 4: The UST 1 form can be submitted at any time.

There are specific deadlines for submitting the UST 1 form. Vendors must ensure that their forms are received by the Ohio Department of Taxation by the due date to avoid late fees and penalties. Keeping track of these deadlines is crucial for compliance.

Filling out the Ohio Sales Tax UST 1 form is an important task for vendors. Here are some key takeaways to help ensure accuracy and compliance: