The Ohio Promissory Note form serves as a crucial document in financial transactions, establishing a clear agreement between a borrower and a lender. This form outlines the terms of repayment, including the principal amount borrowed, the interest rate, and the payment schedule. It typically specifies whether the loan is secured or unsecured, detailing any collateral involved. Additionally, the document may include clauses addressing late fees, default conditions, and remedies available to the lender in case of non-payment. By providing a written record of the agreement, the Ohio Promissory Note helps protect the interests of both parties, ensuring that expectations are clearly defined and legally enforceable. Understanding the structure and components of this form is essential for anyone involved in lending or borrowing money in Ohio, as it lays the groundwork for a successful financial relationship.

Ohio Promissory Note Template

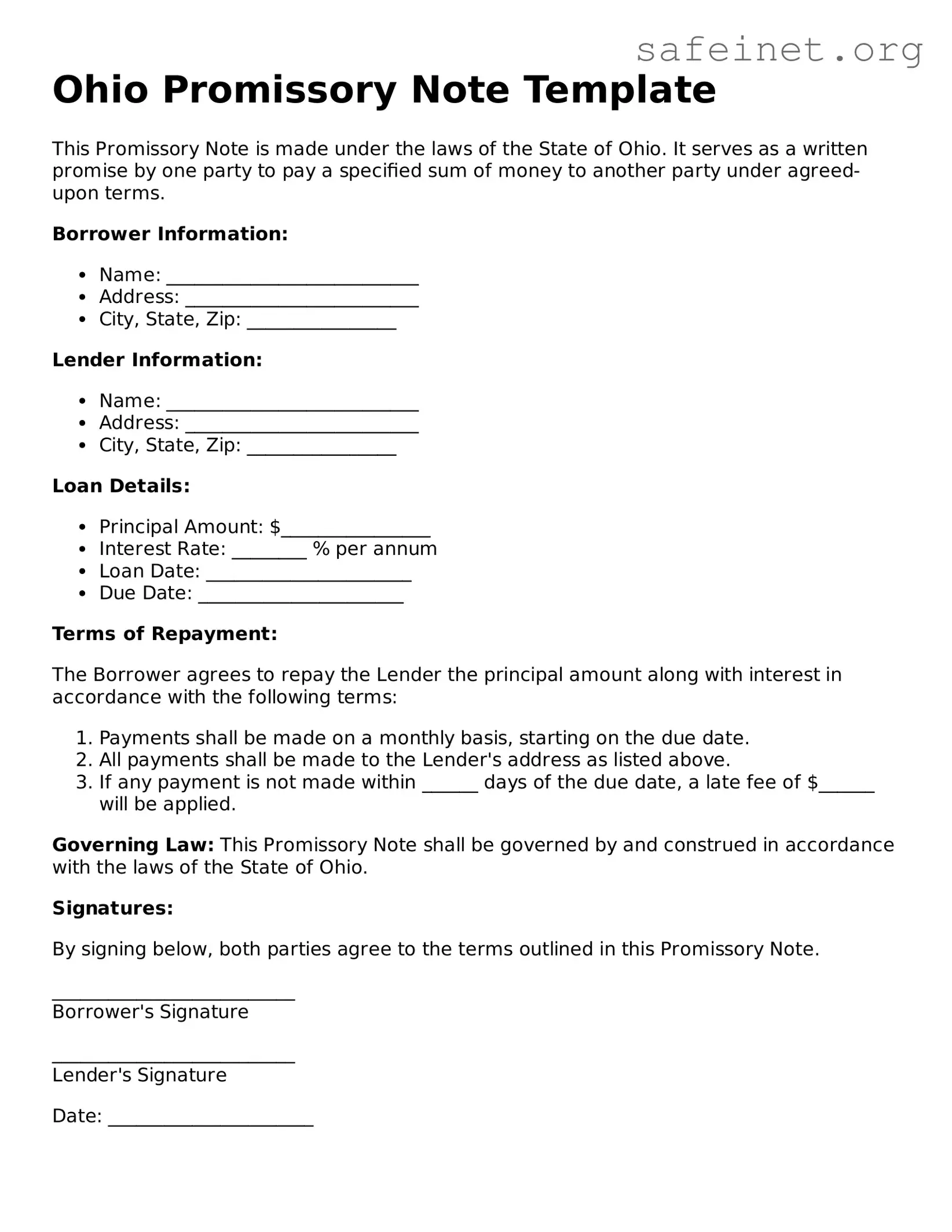

This Promissory Note is made under the laws of the State of Ohio. It serves as a written promise by one party to pay a specified sum of money to another party under agreed-upon terms.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Lender the principal amount along with interest in accordance with the following terms:

Governing Law: This Promissory Note shall be governed by and construed in accordance with the laws of the State of Ohio.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

__________________________

Borrower's Signature

__________________________

Lender's Signature

Date: ______________________

| Fact Name | Description |

|---|---|

| Definition | An Ohio promissory note is a written promise to pay a specified amount of money to a designated person or entity. |

| Governing Law | Ohio Revised Code Section 1303.01 governs promissory notes in Ohio. |

| Parties Involved | The note involves at least two parties: the maker (the person promising to pay) and the payee (the person to whom the payment is owed). |

| Consideration | A valid promissory note requires consideration, meaning something of value must be exchanged. |

| Interest Rate | The note can specify an interest rate, which must comply with Ohio law regarding maximum allowable rates. |

| Payment Terms | It should clearly outline the payment terms, including due dates and any installment plans. |

| Signatures | Both the maker and the payee should sign the note to validate it, although only the maker's signature is legally required. |

| Default Provisions | The note may include provisions outlining what happens in the event of a default, such as late fees or acceleration of payment. |

| Enforceability | Ohio courts generally enforce promissory notes as long as they meet legal requirements and are not deemed unconscionable. |

| Record Keeping | It is advisable for both parties to keep copies of the promissory note for their records in case of disputes. |

After obtaining the Ohio Promissory Note form, you will need to fill it out carefully. This document serves as a written promise to repay a specific amount of money under agreed-upon terms. Follow the steps below to complete the form accurately.

Once you have completed these steps, review the form for accuracy. Make sure all required fields are filled out correctly before finalizing the document.

What is a promissory note in Ohio?

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a certain time or on demand. In Ohio, this document serves as a legal agreement between the borrower and the lender. It outlines the terms of the loan, including the interest rate, payment schedule, and any penalties for late payments. This document is crucial for both parties to ensure that their rights and obligations are clearly defined.

How do I create a valid promissory note in Ohio?

To create a valid promissory note in Ohio, include essential elements such as the names and addresses of both the borrower and lender, the principal amount, the interest rate, the payment terms, and the maturity date. It is also advisable to sign and date the document in the presence of a witness or notary public, although notarization is not always required. Keeping a copy of the signed note for your records is important for future reference.

What happens if the borrower fails to repay the loan?

If the borrower fails to repay the loan as outlined in the promissory note, the lender has the right to take legal action. This may include filing a lawsuit to recover the owed amount. The lender may also seek to collect any accrued interest and fees associated with the late payment. It’s important for both parties to understand their rights and obligations to avoid misunderstandings and potential legal disputes.

Can a promissory note be modified after it is signed?

Yes, a promissory note can be modified after it is signed, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the borrower and lender to ensure clarity and enforceability. This helps prevent disputes over the terms of the loan in the future.

Is a promissory note enforceable in court?

Yes, a properly executed promissory note is generally enforceable in court. If a dispute arises, the note serves as evidence of the loan agreement. Courts typically uphold the terms of the note as long as they comply with Ohio law. However, factors such as fraud or duress could affect enforceability. It’s crucial to ensure that the note is clear and legally sound to protect your interests.

Failing to include the date at the top of the form. This can lead to confusion about when the agreement was made.

Not clearly stating the amount borrowed. Ambiguous figures can create disputes later on.

Omitting the interest rate. If the note involves interest, it must be specified to avoid misunderstandings.

Neglecting to identify the borrower and lender properly. Full names and addresses are essential for clarity.

Using vague language regarding repayment terms. Clear terms help prevent future conflicts.

Not including a due date for repayment. This is crucial for both parties to understand when the loan must be repaid.

Failing to sign the document. Without signatures, the note may not be enforceable.

Forgetting to have a witness or notary present. This can add an extra layer of legitimacy to the agreement.

Not keeping a copy of the signed note. Both parties should have access to the agreement for reference.

Ignoring state-specific requirements. Each state may have unique rules that must be followed.

When dealing with financial agreements in Ohio, a Promissory Note is often accompanied by other important documents. These forms help clarify the terms of the loan and provide additional legal protections for both parties involved. Below are four commonly used documents that complement the Ohio Promissory Note.

Utilizing these documents alongside the Ohio Promissory Note can enhance the clarity and security of financial transactions. Each form plays a vital role in protecting the interests of both parties and ensuring a smooth lending process.

A personal loan agreement is a document that outlines the terms and conditions under which a borrower agrees to repay a loan to a lender. Similar to a promissory note, it specifies the loan amount, interest rate, and repayment schedule. However, a personal loan agreement often includes additional clauses that cover aspects such as late fees, default conditions, and borrower rights, making it a more comprehensive document for personal loans.

A mortgage note is another document that bears similarities to a promissory note. It is used in real estate transactions where a borrower agrees to repay a loan secured by real property. Like a promissory note, a mortgage note includes details about the loan amount and repayment terms. However, it also establishes the lender's right to foreclose on the property if the borrower defaults, adding an extra layer of security for the lender.

A business loan agreement serves a similar purpose in the context of business financing. This document outlines the terms under which a business borrows money, including repayment schedules and interest rates. While it functions like a promissory note, it often contains specific provisions tailored to business operations, such as covenants that require the business to maintain certain financial ratios or operational standards.

A car loan agreement is specifically designed for financing the purchase of a vehicle. Like a promissory note, it details the loan amount, interest rate, and repayment terms. However, it also includes information about the vehicle being financed and typically allows the lender to repossess the vehicle if the borrower fails to make payments, thereby securing the loan with the collateral of the car.

A student loan agreement shares similarities with a promissory note, as it outlines the terms under which a student borrows money for educational expenses. It includes the loan amount, interest rate, and repayment schedule. However, student loans often have unique provisions, such as deferment options and income-driven repayment plans, that are specifically designed to accommodate the financial situations of students.

A lease agreement is another document that, while different in purpose, shares some characteristics with a promissory note. It outlines the terms under which a tenant agrees to pay rent to a landlord. Like a promissory note, it specifies payment amounts and due dates. However, lease agreements also include terms related to property use, maintenance responsibilities, and the duration of the lease, making them more complex than a typical promissory note.

A credit card agreement is similar in that it outlines the terms of borrowing, including interest rates and payment schedules. However, unlike a promissory note, which typically involves a single loan amount, a credit card agreement allows for ongoing borrowing up to a credit limit. This type of agreement also includes terms regarding fees, rewards, and penalties for late payments, making it distinct from a standard promissory note.

An installment loan agreement is closely related to a promissory note, as it specifies the terms of a loan that is repaid in fixed installments over time. This document includes details such as the total loan amount, interest rate, and payment schedule. However, installment loans can cover a variety of purposes, from personal loans to financing for larger purchases, and may include provisions for early repayment or penalties for missed payments.

A demand note is a type of promissory note that requires the borrower to repay the loan upon the lender's request. It shares many characteristics with a standard promissory note, such as specifying the loan amount and interest rate. However, the key difference lies in the repayment terms, as a demand note does not have a fixed repayment schedule, giving the lender more flexibility in collecting the debt.

A loan modification agreement is similar in that it alters the terms of an existing loan, often due to the borrower’s financial difficulties. While it does not serve as a new promissory note, it functions similarly by outlining the revised terms, including new payment amounts and schedules. This document is crucial for borrowers seeking to avoid default and maintain their loan in good standing.

When filling out the Ohio Promissory Note form, it's important to follow certain guidelines to ensure everything is completed correctly. Here’s a list of things you should and shouldn’t do:

By following these tips, you can help ensure that your Promissory Note is valid and enforceable. Take your time and double-check your work to avoid any mistakes.

When it comes to the Ohio Promissory Note form, several misconceptions can lead to confusion for borrowers and lenders alike. Understanding these myths can help individuals navigate the lending process more effectively. Here are eight common misconceptions:

By dispelling these myths, individuals can better understand the role and importance of the Ohio Promissory Note form in their financial transactions. Knowledge is key to making informed decisions and protecting one’s interests.

When filling out and utilizing the Ohio Promissory Note form, there are several important considerations to keep in mind. Understanding these key takeaways can help ensure that the document serves its intended purpose effectively.