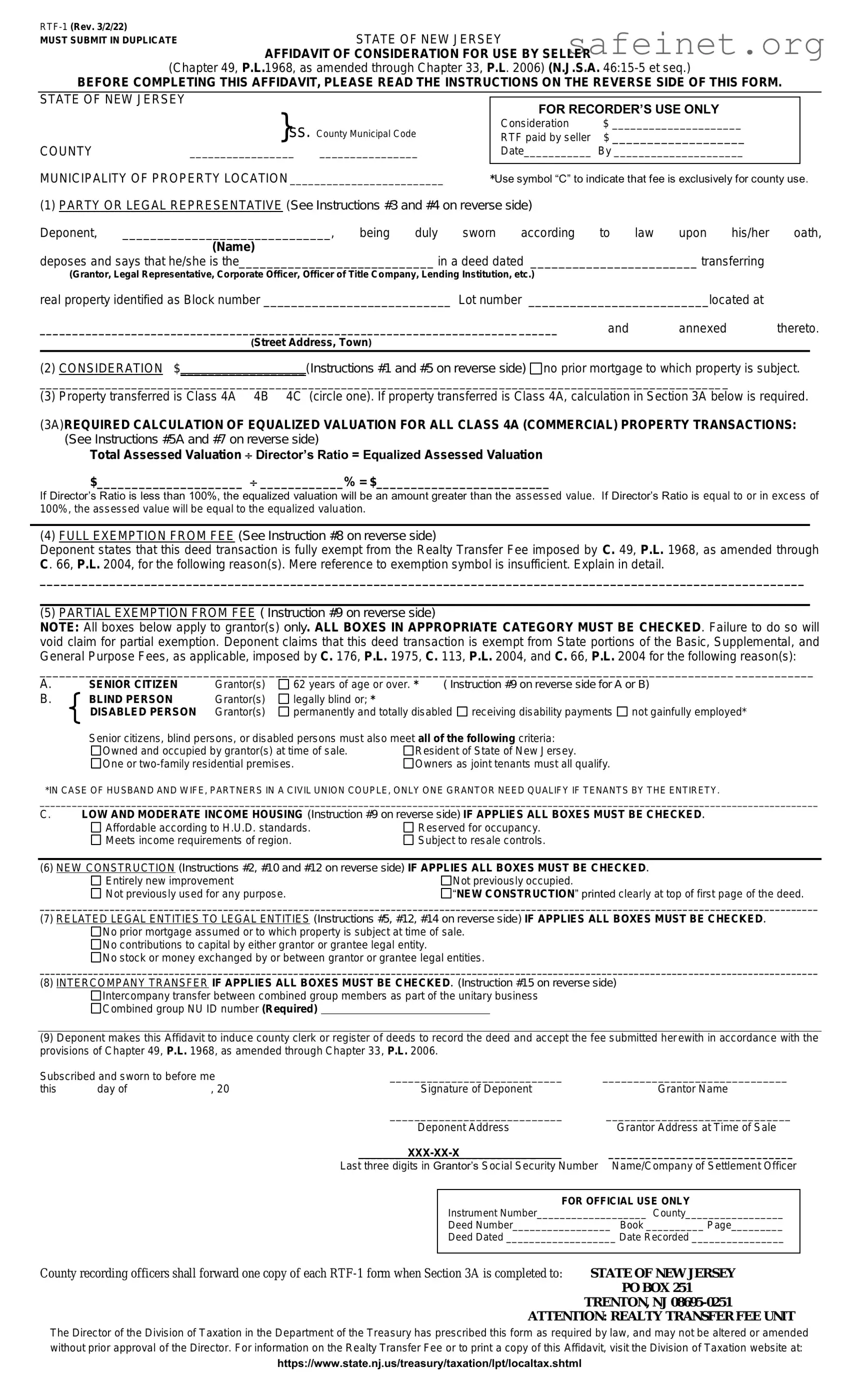

The New Jersey Affidavit of Consideration RTF-1 form serves as a crucial document in real estate transactions, particularly when it comes to the transfer of property ownership. This form is typically used to declare the consideration, or payment, involved in the sale of real estate, ensuring that all parties involved are transparent about the financial aspects of the transaction. By detailing the purchase price and any other relevant financial arrangements, the RTF-1 helps to clarify the nature of the transaction for tax purposes and assists in the proper assessment of any applicable transfer taxes. Additionally, this affidavit is often required by the county clerk’s office when recording the deed, thereby facilitating a smooth transition of ownership. Its importance cannot be overstated, as it not only provides legal protection for both buyers and sellers but also contributes to the integrity of the public record. Understanding the nuances of this form is essential for anyone engaged in real estate dealings in New Jersey, as it plays a pivotal role in ensuring compliance with state regulations.

|

|

MUST SUBMIT IN DUPLICATE |

STATE OF NEW JERSEY |

|

AFFIDAVIT OF CONSIDERATION FOR USE BY SELLER |

(Chapter 49, P.L.1968, as amended through Chapter 33, P.L. 2006) (N.J.S.A.

BEFORE COMPLETING THIS AFFIDAVIT, PLEASE READ THE INSTRUCTIONS ON THE REVERSE SIDE OF THIS FORM.

STATE OF NEW JERSEY |

|

|

|

|

}ss. County Municipal Code |

FOR RECORDER’S USE ONLY |

|

||

|

|

|||

|

Consideration |

$ _____________________ |

|

|

|

RTF paid by seller |

$ ___________________ |

|

|

COUNTY |

_________________ ________________ |

Date___________ By _____________________ |

|

|

MUNICIPALITY OF PROPERTY LOCATION _________________________ |

|

|

||

*Use symbol “C” to indicate that fee is exclusively for county use. |

||||

(1)PARTY OR LEGAL REPRESENTATIVE (See Instructions #3 and #4 on reverse side)

Deponent, ______________________________, being duly sworn according to law upon his/her oath,

(Name)

deposes and says that he/she is the____________________________ in a deed dated ________________________ transferring

(Grantor, Legal Representative, Corporate Officer, Officer of Title Company, Lending Institution, etc.)

real property identified as Block number ___________________________ Lot number |

__________________________located at |

|

|

||

_______________________________________________________________________________ |

and |

annexed |

thereto. |

||

(Street Address, Town) |

|

|

|

|

|

(2) CONSIDERATION $__________________(Instructions #1 and #5 on reverse side) |

no prior mortgage to which property is subject. |

||||

_________________________________________________________________________________________________________

(3) Property transferred is Class 4A 4B 4C (circle one). If property transferred is Class 4A, calculation in Section 3A below is required.

(3A)REQUIRED CALCULATION OF EQUALIZED VALUATION FOR ALL CLASS 4A (COMMERCIAL) PROPERTY TRANSACTIONS: (See Instructions #5A and #7 on reverse side)

Total Assessed Valuation Director’s Ratio = Equalized Assessed Valuation

$_____________________ ____________% = $_________________________

If Director’s Ratio is less than 100%, the equalized valuation will be an amount greater than the assessed value. If Director’s Ratio is equal to or in excess of 100%, the assessed value will be equal to the equalized valuation.

(4)FULL EXEMPTION FROM FEE (See Instruction #8 on reverse side)

Deponent states that this deed transaction is fully exempt from the Realty Transfer Fee imposed by C. 49, P.L. 1968, as amended through C. 66, P.L. 2004, for the following reason(s). Mere reference to exemption symbol is insufficient. Explain in detail.

______________________________________________________________________________________________________________

(5)PARTIAL EXEMPTION FROM FEE ( Instruction #9 on reverse side)

NOTE: All boxes below apply to grantor(s) only. ALL BOXES IN APPROPRIATE CATEGORY MUST BE CHECKED. Failure to do so will void claim for partial exemption. Deponent claims that this deed transaction is exempt from State portions of the Basic, Supplemental, and General Purpose Fees, as applicable, imposed by C. 176, P.L. 1975, C. 113, P.L. 2004, and C. 66, P.L. 2004 for the following reason(s):

__________________________________________________________________________________________________________ ____________

A. |

SENIOR CITIZEN |

Grantor(s) |

62 years of age or over. * |

( Instruction #9 on reverse side for A or B) |

B. |

BLIND PERSON |

Grantor(s) |

legally blind or; * |

|

|

DISABLED PERSON |

Grantor(s) |

permanently and totally disabled receiving disability payments not gainfully employed* |

|

Senior citizens, blind persons, or disabled persons must also meet all of the following criteria:

Owned and occupied by grantor(s) at time of sale. |

Resident of State of New Jersey. |

One or |

Owners as joint tenants must all qualify. |

*IN CASE OF HUSBAND AND WIFE, PARTNERS IN A CIVIL UNION COUPLE, ONLY ONE GRANTOR NEED QUALIFY IF TENANTS BY THE ENTIRETY.

________________________________________________________________________________________________________________________________________________

C.LOW AND MODERATE INCOME HOUSING (Instruction #9 on reverse side) IF APPLIES ALL BOXES MUST BE CHECKED.

Affordable according to H.U.D. standards. |

Reserved for occupancy. |

Meets income requirements of region. |

Subject to resale controls. |

(6)NEW CONSTRUCTION (Instructions #2, #10 and #12 on reverse side) IF APPLIES ALL BOXES MUST BE CHECKED.

Entirely new improvement |

Not previously occupied. |

Not previously used for any purpose. |

“NEW CONSTRUCTION” printed clearly at top of first page of the deed. |

________________________________________________________________________________________________________________________________________________

(7)RELATED LEGAL ENTITIES TO LEGAL ENTITIES (Instructions #5, #12, #14 on reverse side) IF APPLIES ALL BOXES MUST BE CHECKED.

No prior mortgage assumed or to which property is subject at time of sale.

No contributions to capital by either grantor or grantee legal entity.

No stock or money exchanged by or between grantor or grantee legal entities.

________________________________________________________________________________________________________________________________________________

(8)INTERCOMPANY TRANSFER IF APPLIES ALL BOXES MUST BE CHECKED. (Instruction #15 on reverse side)

Intercompany transfer between combined group members as part of the unitary business

Combined group NU ID number (Required)

(9)Deponent makes this Affidavit to induce county clerk or register of deeds to record the deed and accept the fee submitted her ewith in accordance with the provisions of Chapter 49, P.L. 1968, as amended through Chapter 33, P.L. 2006.

Subscribed and sworn to before me |

____________________________ |

______________________________ |

||||||

this |

day of |

, 20 |

|

Signature of Deponent |

|

Grantor Name |

||

|

|

|

____________________________ |

______________________________ |

||||

|

|

|

|

Deponent Address |

|

Grantor Address at Time of Sale |

||

|

|

|

|

_______ |

|

______________________________ |

||

|

|

|

Last three digits in Grantor’s Social Security Number |

Name/Company of Settlement Officer |

||||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

FOR OFFICIAL USE ONLY |

||

|

|

|

|

|

Instrument Number___________________ County_________________ |

|||

|

|

|

|

|

Deed Number_________________ |

Book __________ Page_________ |

||

|

|

|

|

|

Deed Dated ___________________ Date Recorded ________________ |

|||

|

|

|

||||||

County recording officers shall forward one copy of each |

STATE OF NEW JERSEY |

|||||||

|

|

|

|

|

|

|

|

PO BOX 251 |

|

|

|

|

|

|

|

TRENTON, NJ |

|

|

|

|

|

|

ATTENTION: REALTY TRANSFER FEE UNIT |

|||

The Director of the Division of Taxation in the Department of the Treasury has prescribed this form as required by law, and may not be altered or amended without prior approval of the Director. For information on the Realty Transfer Fee or to print a copy of this Affidavit, visit the Division of Taxation website at: https://www.state.nj.us/treasury/taxation/lpt/localtax.shtml

INSTRUCTIONS FOR FILING FORM

1.STATEMENT OF CONSIDERATION AND REALTY TRANSFER FEE PAYMENT ARE PREREQUISITES FOR DEED RECORDING

No county recording officer shall record any deed evidencing transfer of title to real property unless (a) the consideration is recited in the deed, or (b) an Affidavit by

one or more of the parties named in the deed or by their legal representatives declaring the consideration is annexed for rec ording with the deed, and (c) for conveyances and transfers of property for which the total consideration recited in the deed is not in excess of $350,000, a f ee is remitted at the rate of $2.00/$500 of consideration or fractional part thereof not in excess of $150,000; $3.35/$500 of consideration or fractional part thereof in excess of $150,000 but not in excess of $200,000; and $3.90/$500 of consideration or fractional part thereof in excess of $200,000. For transfers of property for which the total consideration recited in the deed is in excess of $350,000, a fee is remitted at the rate of $2.90/$500 of consideration or fractional part not in excess of $150,000; $4.25/$500 of consideration or fractional part thereof in excess of $150,000 but not in excess of $200,000; $4.80/$500 of consideration or fractional part thereof in excess of $200,000; $5.30/$500 of consideration or fractional part thereof in excess of $550,000 but not in excess of $850,000; $5.80/$500 of consideration or fractional part thereof in excess of $850,00 but not in $1,000,000; and $6.05/$500 of consideration or fractional part thereof in excess of $1,000,000, which fee shall be paid in addition to the recording fees imposed by Chapter 123, P.L. 1965, Section 2 (C.

2.WHEN AFFIDAVIT MUST BE ANNEXED TO DEED

This Affidavit must be annexed to and recorded with all deeds when entire consideration is not recited in deed or the acknowledgement or proof of the execution, when the grantor claims a total or partial exemption from the fee, Class 4 property that includes commercial, industrial, or apartment property, and for transfers of “new construction.” (See Instructions #10 and #12 below.)

3.LEGAL REPRESENTATIVE

“Legal representative” is to be interpreted broadly to include any person actively and responsibly participating in the transaction, such as, but not limited to: an attorney representing one of the parties; a closing officer of a title company or lending institution participating in the transaction; a holder of power of attorney from grantor or grantee.

4.OFFICER OF CORPORATE GRANTOR/OFFICER OF TITLE COMPANY OR LENDING INSTITUTION

Where a deponent is an officer of corporate grantor, state the name of corporation and officer’s title or where a deponent is a closing officer of a title company or

lending institution participating in the transaction, state the name of the company or institution and officer’s title.

5.CONSIDERATION

“Consideration” means in the case of any deed, the actual amount of money and the monetary value of any other thing of value constituting the entire

compensation paid or to be paid for the transfer of title to the lands, tenements or other realty, including the remaining amount of any prior mortgage to which the transfer is subject or which is assumed and agreed to be paid by the grantee and any other lien or encumbrance not paid, satisfied or removed in connection with the transfer of title. (C. 49, P.L. 1968, Section 1, as amended.)

5A. CLASS 4A “COMMERCIAL PROPERTIES” DEFINED

Class 4A “Commercial properties” as defined in N.J.A.C.

6.DIRECTOR'S RATIO

“Director’s Ratio” means the average ratio of assessed to true value of real property for each taxing district as determined by the Director, Division of Taxation, in the Table of Equalized Valuations promulgated annually on or before October 1 in each year pursuant to N.J.S.A.

7.EQUALIZED VALUE

“Equalized Value” means the assessed value of the property in the year that the transfer is made, divided by the Director’s Ratio. The Table of Equalized

Valuations is promulgated annually on or before October 1 in each year pursuant to N.J.S.A.

(Example: Assessed Value = $1,000,000; Director’s Ratio = 80%. $1,000,000 .80 = $1,250,000)

8.FULL EXEMPTION FROM THE REALTY TRANSFER FEE (GRANTOR/GRANTEE)

The fee imposed by this Act shall not apply to a deed:

(a)For consideration of less than $100; (b) By or to the United States of America, this State, or any instrumentality, agency or subdivision; (c) Solely in order to provide or release security for a debt or obligation; (d) Which confirms or corrects a deed previously recorded; (e) On a sale for delinquent taxes or assessments; (f) On partition;

(g)By a receiver, trustee in bankruptcy or liquidation, or assignee for the benefit of creditors; (h) Eligible to be recorded as an “ancient deed” pursuant to R.S.

9.PARTIAL EXEMPTION FROM THE REALTY TRANSFER FEE (C. 176, P.L. 1975; C. 113, P.L. 2003; C. 66 P.L. 2004)

The following transfers of title to real property shall be exempt from State portions of the Basic Fee, Supplemental Fee, and General Purpose Fee, as applicable: 1.

The sale of any one or

For the purposes of this Act, the following definitions shall apply:

“Blind person” means a person whose vision in his better eye with proper correction does not exceed 20/200 as measured by the Snellen chart or a person who has a field defect in his better eye with proper correction in which the peripheral field has contracted to such an extent th at the widest diameter of visual field subtends an angular distance no greater than 20º.

“Disabled person” means any resident of this State who is permanently and totally disabled, unable to engage in gainful employment, and receiving disability benefits or any other compensation under any federal or State law.

“Senior citizen” means any resident of this State of the age of 62 or over.

“Low and Moderate Income Housing” means any residential premises, or part thereof, affordable according to Federal Department of Housing and Urban Development or other recognized standards for home ownership and rental costs occupied or reserved for occupancy by households with a gross income equal to 80% or less of the median gross household income for households of the same size within the housing region in which the housing i s located, but shall include only those residential premises subject to resale controls pursuant to contractual guarantees.

“Resident of the State of New Jersey” means any claimant who is legally domiciled in this State when the transfer of the subject property is made. Domicile is what the claimant regards as the permanent home to which he intends to return after a period of absence. Proofs of domicile includ e a New Jersey voter registration, motor vehicle registration and driver’s license, and resident tax return filing.

10.TRANSFERS OF NEW CONSTRUCTION

“New construction” means any conveyance or transfer of property upon which there is an entirely new improvement not previously occupied or used for any purpose. On transfers of new construction, the words “NEW CONSTRUCTION” shall be printed clearly at the top of the first page of the deed, and an Affidavit by the grantor stating that the transfer is of property upon which there is new construction shall be appended to the deed.

11.REALTY TRANSFER FEE IS A FEE IN ADDITION TO OTHER RECORDING FEES

The county recording officer is required to collect the Realty Transfer Fee at the time the deed is offered for recording/transfer.

12.PENALTY FOR WILLFUL FALSIFICATION OF CONSIDERATION AND TRANSFERS OF NEW CONSTRUCTION

Any person who knowingly falsifies the consideration recited in a deed or in the proof or acknowledgement of the execution of a deed or i n an affidavit annexed to a

deed declaring the consideration therefor or a declaration in an affidavit that a transfer is exempt from recording fee is guilty of a crime of the fourth degree (Chapter 308, P.L. 1991, effective June 1, 1992). Grantors conveying title of new construction who fail to subscribe and append to the deed an affidavit to that effect in accordance with the provisions of subsection c. of section 2 of Chapter 49, P.L. 1968

13.COUNTY/MUNICIPAL CODES

County/Municipal codes may be found at https://www.state.nj.us/treasury/taxation/pdf/lpt/cntycode.pdf.

14.LEGAL ENTITIES TRANSFERRING NEW JERSEY REAL ESTATE TO RELATED LEGAL ENTITIES

Legal entities transferring New Jersey real estate to related legal entities are not exempt from the Realty Transfer Fee if the consideration, as defined in the law, is $100 or more. Such consideration includes the actual amount of money and/or the monetary value of any other thing of value constituting the entire compensation paid, such as the dollar value of stock included in the transaction or any enhancement to or contribution to the capital or either legal entity resulting from the transfer, or remaining balances of any prior mortgage to which the property is subject or which is assumed and agreed to be paid by the grantee and any other lien or encumbrance not paid, satisfied or removed in connection with the transfer of title.

15. INTERCOMPANY TRANSFER BETWEEN COMBINED GROUP MEMBERS THAT FILE A NEW JERSEY COMBINED RETURN

Transfers of real property that are intercompany transfers between combined group members filing a New Jersey combined return as part of the unitary business of the combined group are exempt from the grantor and grantee fees. Transfers must indicate the combined group NU identification number assigned by the Division of Taxation. If the NU number has not been assigned for any reason then the RTF must be paid and a refund may be applied for.

| Fact Name | Details |

|---|---|

| Purpose | The New Jersey Affidavit of Consideration RTF-1 form is used to disclose the consideration paid for real estate transactions in the state of New Jersey. |

| Governing Law | This form is governed by New Jersey Statutes Annotated (N.J.S.A.) 46:15-5, which mandates the reporting of consideration in property transfers. |

| Filing Requirement | The RTF-1 form must be filed with the county clerk at the time of recording the deed for the property transfer. |

| Impact on Taxes | The information provided in the affidavit can affect the calculation of realty transfer fees, which are based on the consideration amount. |

Filling out the New Jersey Affidavit of Consideration RTF-1 form requires careful attention to detail. After completing the form, you will need to submit it along with any required documents to the appropriate county office. This process is essential for ensuring compliance with local regulations.

What is the New Jersey Affidavit of Consideration RTF-1 form?

The New Jersey Affidavit of Consideration RTF-1 form is a document used in real estate transactions. It provides information about the consideration, or payment, involved in the transfer of property. This form is typically required when a property is sold or transferred, and it helps ensure that the correct amount of transfer tax is assessed based on the sale price or consideration given for the property.

Who needs to complete the RTF-1 form?

Generally, the seller or transferor of the property is responsible for completing the RTF-1 form. However, it is often prepared by the attorney or real estate agent handling the transaction. Buyers may also need to review the form to ensure that the information accurately reflects the terms of the sale. It is important for all parties involved in the transaction to understand the details outlined in the affidavit.

What information is required on the RTF-1 form?

The RTF-1 form requires specific details related to the transaction. This includes the names of the parties involved, the property address, and the total consideration or sale price of the property. Additionally, it may ask for information regarding any liens or encumbrances on the property. Accurate and complete information is crucial, as it directly affects the calculation of transfer taxes.

Where should the completed RTF-1 form be submitted?

Once the RTF-1 form is completed, it must be submitted to the county clerk's office where the property is located. This submission typically occurs during the closing process of the real estate transaction. It is important to keep a copy of the submitted form for personal records, as it serves as an official record of the transaction and the consideration provided.

Incorrect Property Description: Many individuals fail to provide a complete and accurate description of the property. This includes missing details like the block and lot numbers, which are crucial for identifying the property in question.

Omitting Signatures: It's common for people to forget to sign the form. Without a signature, the affidavit is not valid, which can lead to delays in the transaction process.

Inaccurate Consideration Amount: Some filers mistakenly enter the wrong amount for consideration. This figure should reflect the actual purchase price or value exchanged for the property. An incorrect amount can raise questions during the review process.

Not Including Required Attachments: Certain transactions may require additional documentation to be submitted along with the RTF-1 form. Failing to include these documents can result in rejection of the filing.

Using Outdated Forms: People sometimes use older versions of the form, which may no longer be accepted. Always ensure that you are using the most current version of the RTF-1 form to avoid complications.

When dealing with real estate transactions in New Jersey, the Affidavit of Consideration RTF-1 form is often accompanied by several other important documents. These documents help ensure that all parties involved have a clear understanding of the transaction and that legal requirements are met. Below are four commonly used forms that complement the RTF-1.

Understanding these documents is crucial for a smooth real estate transaction in New Jersey. Each plays a vital role in protecting the interests of all parties involved and ensuring compliance with state laws.

The New Jersey Affidavit of Consideration RTF-1 form shares similarities with the New Jersey Deed form. Both documents are essential in real estate transactions. The Deed serves as the legal instrument that conveys ownership of property from one party to another, while the Affidavit of Consideration provides a sworn statement regarding the consideration exchanged in that transaction. Essentially, the Deed transfers the title, and the Affidavit supports the legitimacy of the transaction by detailing the financial aspects involved.

Another document akin to the RTF-1 is the New Jersey Real Estate Transfer Declaration form. This form is required for all real estate transactions in New Jersey and provides information about the property being sold. Similar to the Affidavit of Consideration, it includes details about the sale price and any exemptions that may apply. Both documents help ensure transparency in property transactions and assist the state in collecting transfer taxes based on the sale price.

The New Jersey Seller's Disclosure Statement also parallels the Affidavit of Consideration. This document requires sellers to disclose known issues or defects related to the property. While the Affidavit focuses on the financial consideration of the transaction, the Seller's Disclosure Statement emphasizes the condition of the property itself. Together, they provide a fuller picture of the transaction, protecting both the buyer and seller from potential disputes after the sale.

Additionally, the New Jersey Title Insurance Policy is another document that bears resemblance to the RTF-1 form. While the Affidavit of Consideration confirms the financial terms of a transaction, the Title Insurance Policy protects the buyer against any defects in the title that may arise after the purchase. Both documents are crucial in ensuring that the buyer's interests are safeguarded during and after the transfer of ownership.

Lastly, the New Jersey Property Tax Statement can be compared to the Affidavit of Consideration. This document outlines the property taxes owed and provides a record of the property's assessed value. While the Affidavit addresses the financial consideration at the time of sale, the Property Tax Statement reflects ongoing financial obligations associated with the property. Both documents play a vital role in understanding the financial implications of property ownership in New Jersey.

When filling out the New Jersey Affidavit of Consideration RTF-1 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are some dos and don'ts to keep in mind:

The New Jersey Affidavit of Consideration RTF-1 form is often misunderstood. Here are seven common misconceptions about this important document:

Understanding these misconceptions can help ensure compliance and smooth transactions. Always consult with a professional if there are any doubts about the process.

The New Jersey Affidavit of Consideration RTF-1 form is an important document used in real estate transactions. Here are some key takeaways to keep in mind when filling out and using this form: