The Mortgage Statement form is a crucial document for homeowners, providing essential details about their mortgage account. It typically includes the servicer's name and contact information, ensuring borrowers can easily reach out for assistance. Key components of the form encompass the statement date, account number, and payment due date, all of which are vital for tracking payment schedules. The amount due is prominently displayed, along with any applicable late fees for payments received after a specified date. Homeowners will also find a breakdown of account information, including outstanding principal, interest rates, and any prepayment penalties. Detailed explanations of the amount due clarify how much is allocated to principal, interest, and escrow for taxes and insurance. Additionally, the transaction activity section records recent payments and fees, offering a transparent view of account history. Important messages highlight the implications of partial payments and delinquency, emphasizing the urgency of maintaining timely payments to avoid potential foreclosure. For those facing financial difficulties, the form directs borrowers to resources for mortgage counseling and assistance, underscoring the importance of addressing any challenges promptly.

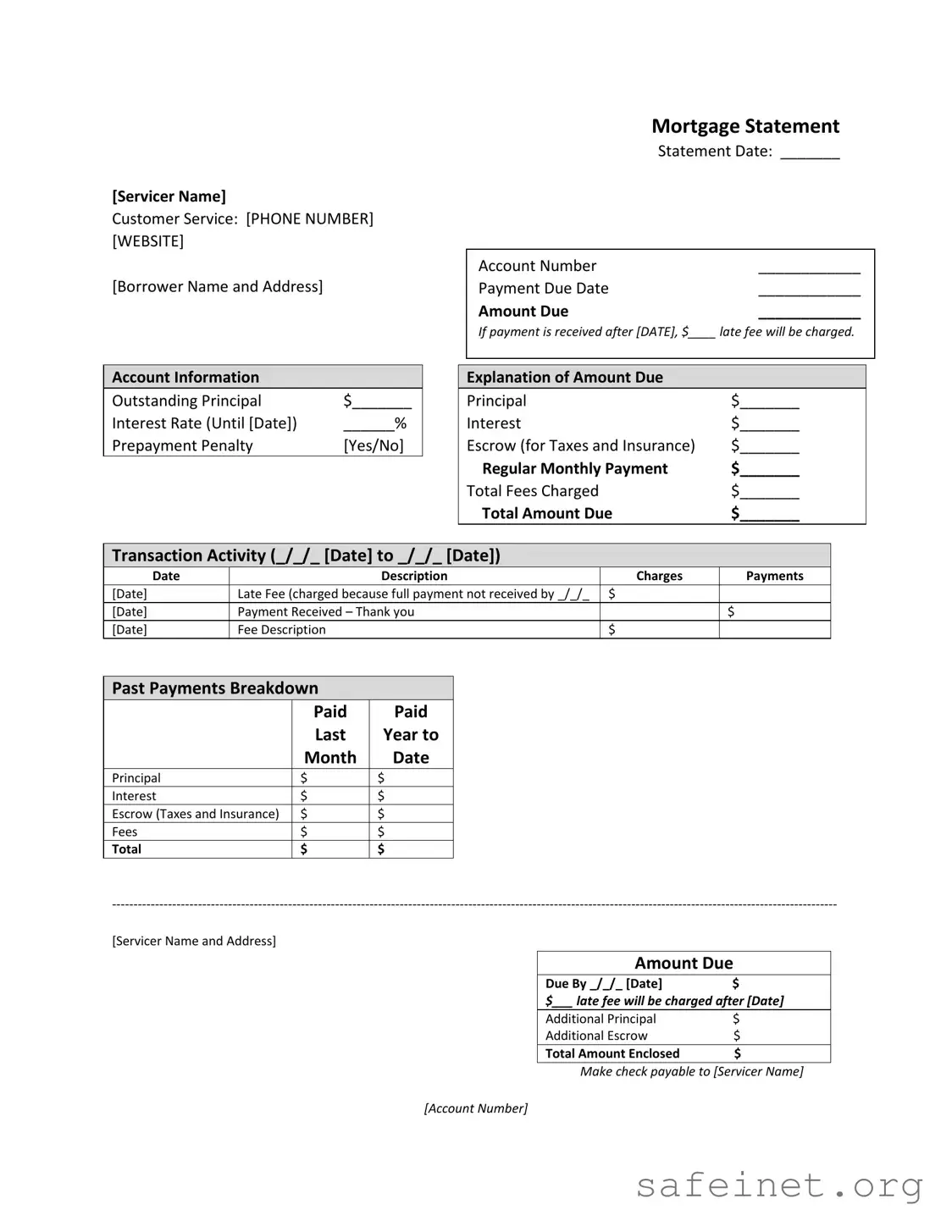

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

| Fact Name | Description |

|---|---|

| Servicer Information | The mortgage statement includes the servicer's name, customer service phone number, and website for easy contact. |

| Payment Details | It specifies the payment due date, amount due, and any late fees that may apply if the payment is not received by the specified date. |

| Account Information | The statement outlines the outstanding principal, interest rate, and whether a prepayment penalty applies. |

| Transaction Activity | A section details transaction history, showing charges and payments made within a specific date range. |

| Important Messages | It includes crucial notices about partial payments, delinquency, and resources for financial assistance if needed. |

Filling out the Mortgage Statement form is an important step in managing your mortgage. This form contains essential information about your account, payment history, and any amounts due. Follow these steps to complete the form accurately.

Once you have filled out the form, review it for accuracy. Make sure all amounts are correct and that you have included any necessary additional information. After confirming everything is accurate, you can submit the form as instructed. This will help ensure that your mortgage account remains in good standing.

What is a Mortgage Statement?

A Mortgage Statement is a document provided by your mortgage servicer. It outlines your current mortgage account status, including the amount due, payment history, and any fees that may apply. This statement helps you keep track of your mortgage payments and outstanding balance.

What information is included in the Mortgage Statement?

The Mortgage Statement includes your account number, payment due date, amount due, outstanding principal, interest rate, and any applicable fees. It also details your recent transaction activity and provides a breakdown of past payments.

What should I do if I see an error on my Mortgage Statement?

If you notice any discrepancies on your Mortgage Statement, contact your mortgage servicer immediately. They can help clarify any issues and correct mistakes if necessary. Be sure to have your statement handy when you call.

What happens if I miss a payment?

If you miss a payment, a late fee may be charged. Your Mortgage Statement will specify the amount of the late fee and the date by which payment must be received to avoid it. It's important to address missed payments promptly to avoid further penalties.

Can I make partial payments on my mortgage?

Partial payments are not applied directly to your mortgage balance. Instead, they are held in a separate suspense account. To have these funds applied to your mortgage, you must pay the remaining balance of the partial payment.

What is a prepayment penalty?

A prepayment penalty is a fee charged if you pay off your mortgage early. Your Mortgage Statement will indicate whether or not this penalty applies to your loan. If you plan to pay off your mortgage ahead of schedule, check for this information.

How can I contact customer service for questions about my Mortgage Statement?

You can reach customer service by calling the phone number listed on your Mortgage Statement or visiting their website. They are available to assist you with any questions or concerns regarding your account.

What should I do if I am experiencing financial difficulty?

If you are having trouble making your mortgage payments, seek assistance as soon as possible. Your Mortgage Statement may provide information about mortgage counseling or resources available to help you manage your financial situation.

What does it mean if I receive a delinquency notice?

A delinquency notice indicates that you are behind on your mortgage payments. This notice will specify how many days you are delinquent. It's crucial to address this situation quickly to avoid additional fees and the risk of foreclosure.

How can I make my mortgage payment?

You can make your mortgage payment by sending a check payable to your servicer, as indicated on your Mortgage Statement. Ensure to include your account number on the check to ensure proper credit to your account.

Failing to provide accurate personal information. This includes the borrower's name and address. Ensure that these details match the information on file with the mortgage servicer.

Neglecting to fill in the account number. This number is crucial for identifying the specific mortgage account. Without it, the servicer may struggle to process the statement correctly.

Forgetting to check the payment due date. It's important to be aware of when payments are due to avoid late fees. Make sure to note the date and plan accordingly.

Overlooking the amount due section. Double-check that the total amount listed matches your calculations. Errors in this area can lead to missed payments or additional fees.

Ignoring the delinquency notice. If the statement indicates that payments are late, it's essential to address this promptly. Failure to do so can result in serious consequences, including foreclosure.

When managing your mortgage, several documents often accompany the Mortgage Statement form. Understanding these forms can help you navigate your mortgage responsibilities more effectively. Here’s a list of key documents that you may encounter:

Familiarizing yourself with these documents can empower you to make informed decisions about your mortgage. Always keep them organized and accessible, as they play a crucial role in your homeownership journey.

The first document similar to a Mortgage Statement is a Credit Card Statement. Both documents serve as periodic summaries of account activity, detailing amounts owed and payment due dates. A Credit Card Statement includes information such as the outstanding balance, interest rates, and any fees incurred, much like the Mortgage Statement outlines principal, interest, and late fees. Both statements also provide a breakdown of transactions, allowing the borrower to track their payment history and understand how their payments are being applied to the overall debt.

Another comparable document is a Utility Bill. Like a Mortgage Statement, a Utility Bill provides a clear overview of what is owed for services rendered during a specific billing cycle. It typically includes the total amount due, payment due date, and any penalties for late payments. Both documents aim to inform the recipient of their financial obligations and encourage timely payment to avoid additional charges. Additionally, utility bills often contain usage details, similar to how a Mortgage Statement breaks down payments into principal and interest components.

A third document that shares similarities with a Mortgage Statement is a Loan Statement for personal loans. This document outlines the total amount owed, payment due dates, and interest rates, just as a Mortgage Statement does for mortgage loans. Both documents are designed to keep borrowers informed about their financial responsibilities and payment history. They also highlight any fees associated with late payments or missed deadlines, emphasizing the importance of timely payments to maintain good standing.

Finally, a Bank Statement can also be likened to a Mortgage Statement. A Bank Statement summarizes all transactions in a bank account over a specific period, detailing deposits, withdrawals, and any fees charged. Similar to a Mortgage Statement, it provides a snapshot of financial activity and outstanding balances. Both documents serve to keep individuals aware of their financial status, ensuring they understand what is owed and when payments are due. They also include important messages or alerts regarding account activity, which can help in managing finances effectively.

When filling out the Mortgage Statement form, attention to detail is crucial. Here’s a list of what you should and shouldn’t do:

By following these guidelines, you can help ensure that your mortgage statement is processed smoothly and efficiently.

Understanding the Mortgage Statement form can be challenging, and several misconceptions often arise. Here are four common misunderstandings:

By clarifying these misconceptions, borrowers can better understand their mortgage statements and manage their accounts more effectively.

When filling out and using the Mortgage Statement form, consider the following key takeaways:

Reviewing these key points can help ensure accurate completion and effective use of the Mortgage Statement form.