When navigating personal or business financing, understanding the essentials of a Loan Agreement form becomes crucial. This important document outlines the terms and conditions under which funds will be borrowed and repaid, serving as a safeguard for both lenders and borrowers. Key components include the loan amount, interest rates, repayment schedule, and potential penalties for late payments. Additionally, it addresses necessary clauses such as collateral, which secures the loan, and default terms, which define the repercussions if agreed-upon conditions are not met. Furthermore, a Loan Agreement form often includes spaces for signatures, ensuring all parties acknowledge and accept the terms outlined therein. Given the potential financial implications, it’s imperative to approach the Loan Agreement thoughtfully, ensuring clarity and mutual understanding among all parties involved.

Loan Agreement Template

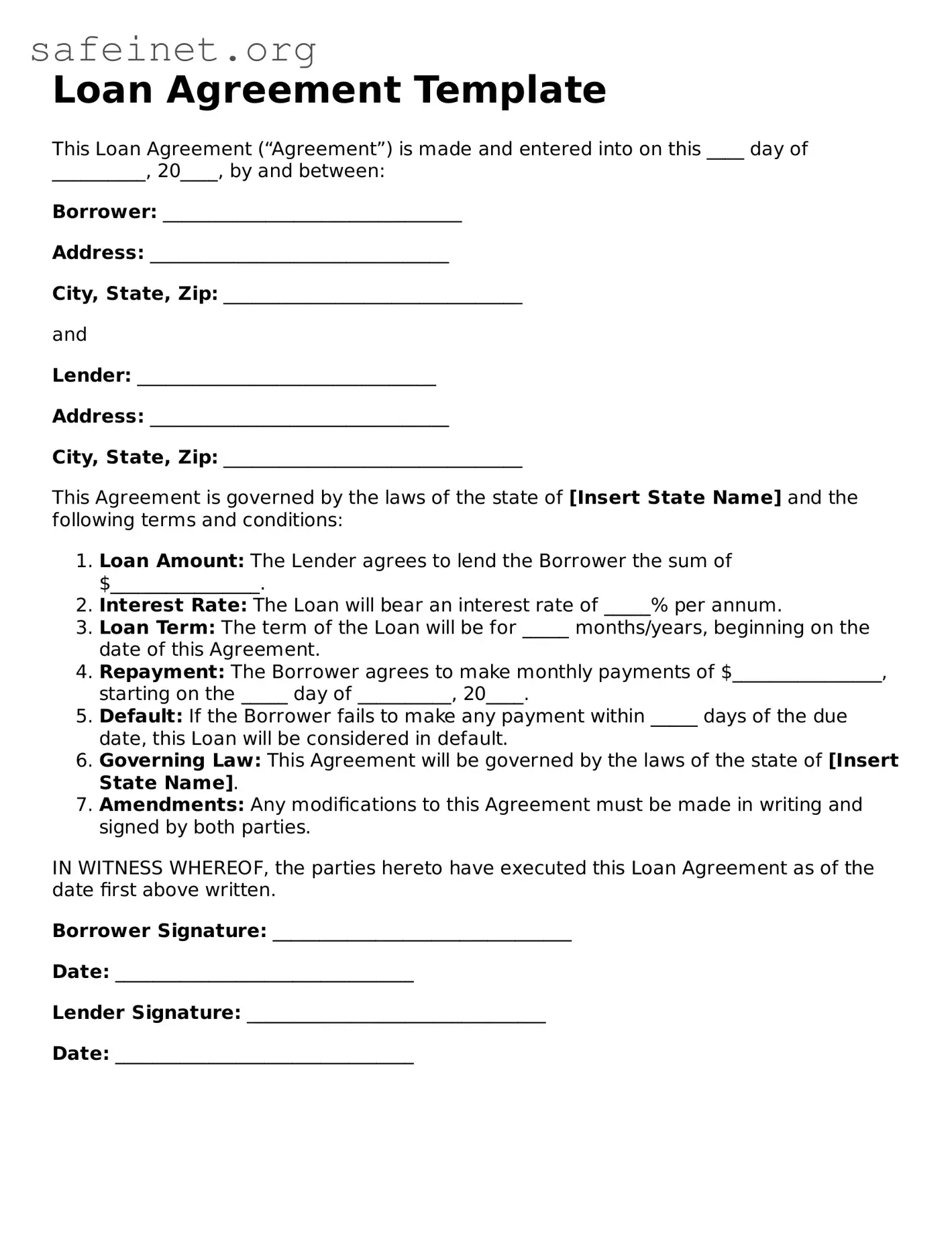

This Loan Agreement (“Agreement”) is made and entered into on this ____ day of __________, 20____, by and between:

Borrower: ________________________________

Address: ________________________________

City, State, Zip: ________________________________

and

Lender: ________________________________

Address: ________________________________

City, State, Zip: ________________________________

This Agreement is governed by the laws of the state of [Insert State Name] and the following terms and conditions:

IN WITNESS WHEREOF, the parties hereto have executed this Loan Agreement as of the date first above written.

Borrower Signature: ________________________________

Date: ________________________________

Lender Signature: ________________________________

Date: ________________________________

| Fact Name | Details |

|---|---|

| Definition | A loan agreement is a legal document that outlines the terms of a loan between a borrower and a lender. |

| Purpose | The agreement serves to protect both parties by clearly stating the loan amount, interest rate, payment schedule, and any applicable fees. |

| Governing Law | The agreement must specify the governing law, which varies by state. For instance, in California, it falls under California Civil Code. |

| Repayment Terms | Loan agreements typically include the repayment terms, outlining when payments are due and the total duration of the loan. |

| Interest Rate Types | Interest rates can be fixed or variable. The agreement should clearly define which type applies. |

| Secured vs. Unsecured | Loan agreements can be secured (backed by collateral) or unsecured (not backed by collateral). This distinction can affect terms and interest rates. |

| Default Clauses | Default clauses outline the actions taken if payments are missed or if the borrower fails to comply with the terms. |

| Amendments | The process for making amendments to the loan agreement should be outlined, ensuring both parties can agree to changes smoothly. |

| Signatures | To be legally binding, the loan agreement must be signed by both parties, typically in the presence of a witness or notary. |

Filling out the Loan Agreement form is an important step that allows both parties to clearly understand the terms and conditions of the loan. Properly completing the form ensures that everyone is on the same page and helps avoid future misunderstandings. Follow the steps below to accurately fill out the form.

Following these steps will help you complete the Loan Agreement form correctly, ensuring clarity and understanding for all involved parties.

What is a Loan Agreement form?

A Loan Agreement form is a legal document that outlines the terms and conditions under which a loan is provided. It typically includes information about the lender and borrower, the loan amount, interest rates, repayment schedule, and any applicable fees. This form serves to protect both parties by clearly stating their obligations and rights regarding the loan.

Why is it important to use a Loan Agreement form?

Using a Loan Agreement form is crucial as it provides clarity and certainty about the terms of the loan. It helps to prevent misunderstandings and disputes by documenting the agreements made between the lender and borrower. In case of a default or disagreement, having a signed form can serve as evidence in legal proceedings.

What details should be included in a Loan Agreement form?

A Loan Agreement form should include several key details: the names and addresses of the lender and borrower, the loan amount, the interest rate, the repayment terms, including the frequency of payments, and any late fees or penalties. Additionally, it should specify the consequences of default and whether any collateral is required.

Can a Loan Agreement be modified after it is signed?

Yes, a Loan Agreement can be modified after it is signed, but changes typically require the consent of both parties. It is advisable to document any modifications in writing to maintain a clear record of the new terms. Both parties should sign and date any amendments to ensure that they are enforceable.

What happens if a borrower defaults on a Loan Agreement?

If a borrower defaults on a Loan Agreement, the lender has several options. They may charge late fees, report the default to credit bureaus, or initiate legal action to recover the owed amount. The specific consequences of default are usually outlined in the Loan Agreement itself, so it is important for borrowers to understand these implications before signing.

Failing to provide complete personal information. Borrowers often leave out essential details, such as their full address or Social Security number, which can delay processing.

Incorrectly stating the loan amount requested. It is vital to ensure that the requested amount matches what is intended. Discrepancies could lead to confusion or denial.

Not reading the terms and conditions thoroughly. Many individuals skip this crucial step, which can result in misunderstandings about the repayment schedule and interest rates.

Misunderstanding the source of income. Providing vague or incomplete information about income sources is common. Clear and precise disclosures help in assessing eligibility.

Omitting or misstating financial obligations. Borrowers might forget to list existing loans or credit obligations, which can affect creditworthiness assessments.

Failing to sign or date the form. It may seem simple, but neglecting to sign can invalidate the application entirely.

Providing outdated contact information. Borrowers may list previous phone numbers or email addresses, making it difficult for lenders to reach them for follow-up.

Not double-checking for errors. Many individuals submit their forms without proofreading, leaving behind typos or inaccuracies that could complicate the approval process.

When entering into a loan agreement, it's essential to understand the documents that often accompany it. These forms help clarify terms, protect both parties, and ensure that everything is transparent. Here are four important documents that you might encounter along with your loan agreement:

Having these documents prepared and understood can help streamline the loan process and minimize misunderstandings. Make sure to read everything carefully and ask questions if anything is unclear. Clear communication is key to a successful loan experience.

A promissory note is quite similar to a loan agreement in that it serves as a legal document outlining the terms surrounding a loan. The promissory note, however, is typically a simpler document where the borrower promises to repay the lender a specific amount of money, often with interest, by a certain date. Unlike a full loan agreement, which may include detailed terms and conditions, a promissory note focuses primarily on the borrower's commitment to repay and the payment schedule. It is often considered a standalone document, making it easier and quicker to execute in some situations.

A mortgage agreement stands out as another important document related to loans, particularly for real estate transactions. This type of agreement commits the borrower to repay a loan that is secured by real property. While a loan agreement can stand alone, a mortgage agreement specifically ties the repayment of the loan to the property itself. Should the borrower fail to make payments, the lender can take legal action to foreclose on the property. This security interest sets it apart from standard loan agreements, which may not involve collateral.

An installment agreement is similar in spirit to a loan agreement but usually involves spreading payments over a defined period. These agreements specify the schedule and amount of each payment, allowing borrowers to manage their finances more effectively. Although both documents serve the purpose of outlining repayment terms, an installment agreement specifically emphasizes the frequency of payments. This can prove useful for individuals and businesses needing to budget carefully against their cash flow.

A lease agreement, while primarily associated with rental situations, shares some common ground with loan agreements. Both documents establish terms under which one party can use property owned by another. In the case of lease agreements, the focus is usually on real estate or equipment. Even though lease payments are not technically loan repayments, they can represent a form of borrowing against the value of the items being leased. This similarity lies in the structured payment terms and obligations set forth in each document.

A security agreement often accompanies loan agreements when the loan is secured by a borrower’s assets. This document describes the collateral being used to guarantee the loan, offering an added layer of protection for the lender. Like a loan agreement, it outlines responsibilities and obligations incurred by the borrower. However, the security agreement’s primary focus is on the collateral, detailing what the lender can claim if the borrower defaults. This makes it distinct from a typical loan agreement while still being closely related in terms of the overall loan arrangement.

When filling out a Loan Agreement form, there are important guidelines to follow. Here are ten things to keep in mind:

Understanding a Loan Agreement form can be challenging, and misconceptions often lead to confusion. Here are some common misunderstandings about loan agreements:

Being aware of these misconceptions can help ensure better preparation and understanding when entering into a loan agreement. It's always wise to read the fine print and seek clarification on any points that seem unclear.

Understanding the Loan Agreement form is essential for anyone engaging in borrowing or lending money. Here are some key takeaways to keep in mind:

By keeping these points in mind, both lenders and borrowers can navigate the Loan Agreement process more effectively.