When it comes to lending and borrowing money, having a clear and legally binding agreement is essential. The Kentucky Promissory Note form serves as a vital tool in these transactions, ensuring that both parties understand their rights and responsibilities. This form outlines the amount borrowed, the interest rate, and the repayment schedule, providing a framework for the lender and borrower to follow. Additionally, it includes important details such as the names of the parties involved, the date of the agreement, and any collateral that may be tied to the loan. By using this form, individuals can protect themselves and foster trust in their financial dealings. Whether you are a lender looking to safeguard your investment or a borrower seeking to clarify your obligations, understanding the Kentucky Promissory Note is key to navigating the lending landscape effectively.

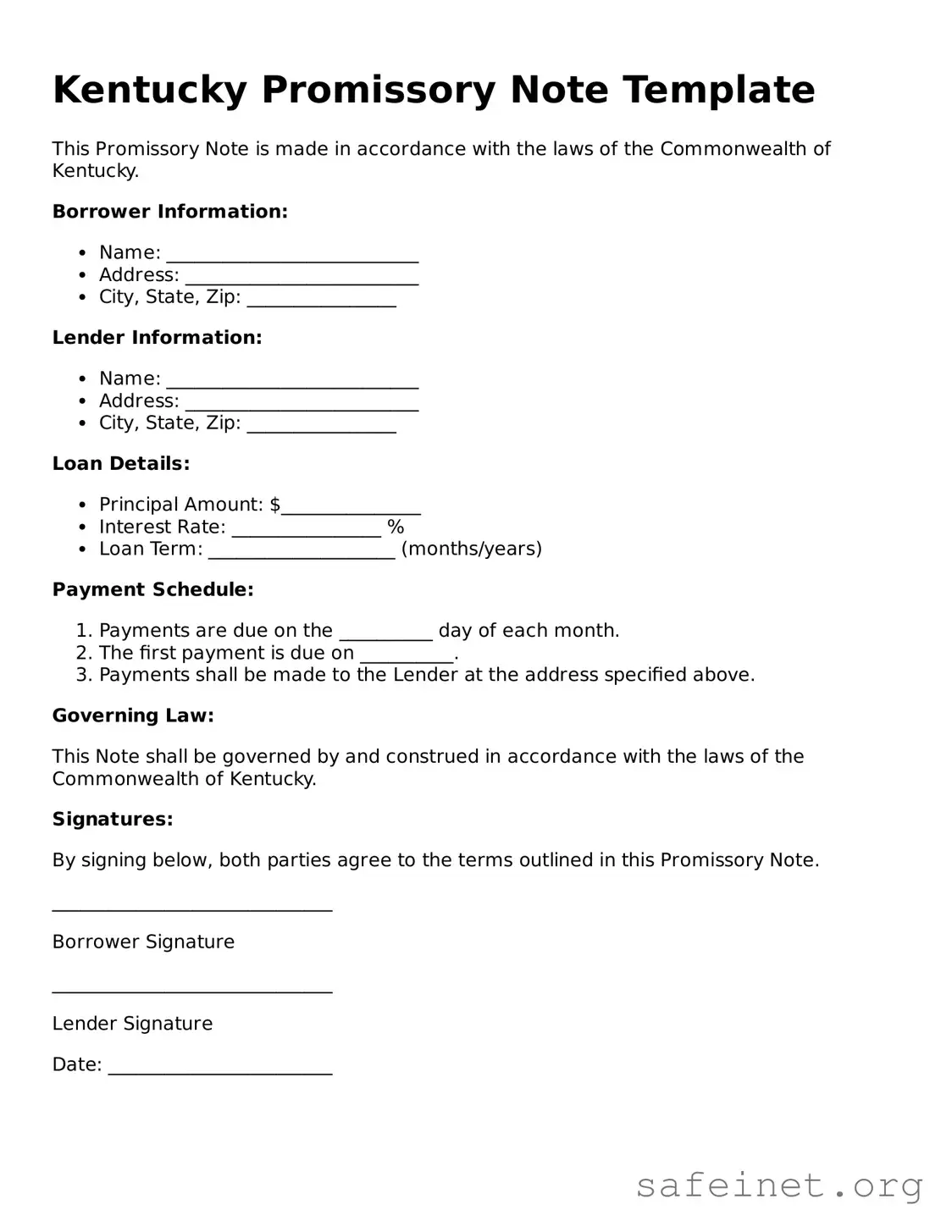

Kentucky Promissory Note Template

This Promissory Note is made in accordance with the laws of the Commonwealth of Kentucky.

Borrower Information:

Lender Information:

Loan Details:

Payment Schedule:

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the Commonwealth of Kentucky.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

______________________________

Borrower Signature

______________________________

Lender Signature

Date: ________________________

| Fact Name | Details |

|---|---|

| Definition | A Kentucky Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a defined time. |

| Governing Law | The Kentucky Promissory Note is governed by the Kentucky Revised Statutes, specifically KRS Chapter 371. |

| Requirements | The note must include the principal amount, interest rate, payment terms, and signatures of the parties involved. |

| Enforceability | To be enforceable, the note must be clear and unambiguous, with all essential terms explicitly stated. |

Once you have the Kentucky Promissory Note form in hand, you will need to fill it out accurately to ensure it meets all necessary requirements. After completing the form, you may want to review it for any errors before proceeding with signatures and any additional documentation.

What is a Kentucky Promissory Note?

A Kentucky Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender. This document includes essential details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. It serves as a written record of the agreement between the borrower and lender, ensuring both parties understand their obligations.

Who can use a Kentucky Promissory Note?

Any individual or business in Kentucky can use a Promissory Note. Whether you are a private lender, a bank, or an individual borrowing money from a friend or family member, this document can help formalize the agreement. It is particularly useful for personal loans, business loans, or any situation where money is borrowed and expected to be repaid.

What should be included in a Kentucky Promissory Note?

A well-crafted Kentucky Promissory Note should include several key components: the names and addresses of both the borrower and lender, the principal amount of the loan, the interest rate, repayment terms (including due dates), and any late fees or penalties. Additionally, it may include provisions for prepayment, default, and governing law. Clarity in these details helps prevent misunderstandings in the future.

Is a Kentucky Promissory Note legally binding?

Yes, a Kentucky Promissory Note is legally binding once both parties sign it. This means that the borrower is obligated to repay the loan according to the terms outlined in the note, and the lender has the right to enforce those terms if necessary. However, for the note to be enforceable, it must be clear, specific, and signed by both parties.

Do I need a lawyer to create a Kentucky Promissory Note?

While it is not mandatory to have a lawyer draft a Kentucky Promissory Note, it is advisable, especially for larger loans or more complex agreements. A lawyer can ensure that the document complies with state laws and adequately protects your interests. For simple loans between friends or family, using a template may suffice, but clarity and completeness are essential.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They may attempt to negotiate a new repayment plan or seek to recover the owed amount through legal means. The lender can file a lawsuit to obtain a judgment against the borrower, which may lead to wage garnishment or property liens. It is crucial for both parties to understand their rights and obligations in the event of a default.

Filling out the Kentucky Promissory Note form can be straightforward, but several common mistakes can lead to complications. Here’s a detailed list of six frequent errors:

Inaccurate Borrower Information: Many individuals fail to provide complete or correct information about the borrower. This includes the name, address, and contact details. Missing or incorrect details can create issues in the future.

Omitting Loan Amount: Some people forget to specify the total amount of the loan. This is crucial, as it defines the financial obligation. Without this information, the note may be considered incomplete.

Neglecting to Include Interest Rate: The interest rate should be clearly stated. Failing to do so can lead to misunderstandings regarding the repayment terms. It is essential to specify whether the rate is fixed or variable.

Not Specifying Repayment Terms: Individuals often overlook detailing how and when the loan will be repaid. This includes payment frequency and due dates. Clarity in this section helps prevent disputes later on.

Ignoring Signatures: Both the borrower and lender must sign the document. Some people forget to sign or fail to obtain the necessary signatures, which can render the note unenforceable.

Failure to Keep Copies: After completing the form, individuals sometimes neglect to make copies for their records. Keeping a copy is vital for both parties to have a reference in case of future disagreements.

By avoiding these common mistakes, individuals can ensure that their Kentucky Promissory Note is properly filled out and legally binding.

The Kentucky Promissory Note is a crucial document used to outline the terms of a loan agreement between a borrower and a lender. Several other forms and documents may accompany this note to ensure clarity and legal compliance in the transaction. Below is a list of commonly used forms that may be relevant in conjunction with the Kentucky Promissory Note.

These documents play a vital role in the lending process, ensuring that both parties understand their rights and responsibilities. Properly completing and executing these forms can help prevent misunderstandings and disputes in the future.

A Kentucky Promissory Note is quite similar to a Loan Agreement. Both documents serve the purpose of formalizing a loan between a borrower and a lender. They outline the terms of the loan, including the amount borrowed, interest rate, repayment schedule, and any penalties for late payments. While a promissory note is a simpler document focusing primarily on the borrower's promise to repay, a loan agreement often includes more detailed terms and conditions, as well as provisions for collateral and default scenarios.

Another document closely related to a Kentucky Promissory Note is a Secured Promissory Note. This version includes collateral to back the loan, providing the lender with additional security. If the borrower defaults, the lender has the right to claim the specified collateral. Like a standard promissory note, it details the loan amount and repayment terms, but the inclusion of collateral adds a layer of protection for the lender.

A Credit Agreement also shares similarities with a Kentucky Promissory Note. This document is typically used in larger transactions and may involve multiple parties. It outlines the terms of credit extended to the borrower, including limits on the amount borrowed, interest rates, and repayment terms. While a promissory note is a straightforward promise to pay, a credit agreement may encompass broader terms and conditions, including covenants and representations.

Another comparable document is the Personal Loan Agreement. This agreement is often used for loans between individuals, such as family or friends. It sets out the same fundamental terms as a promissory note, including the loan amount, interest rate, and repayment schedule. The primary distinction lies in the level of detail and formality; personal loan agreements may include more personalized terms based on the relationship between the parties involved.

A Business Loan Agreement is also similar to a Kentucky Promissory Note, particularly when businesses seek financing. This document outlines the terms under which a lender provides funds to a business. It includes details about the loan amount, interest rate, repayment schedule, and any specific conditions that must be met by the business. While a promissory note focuses on the borrower's promise, a business loan agreement may contain additional clauses that protect the lender's interests.

The Mortgage Note is another document that shares characteristics with a Kentucky Promissory Note. A mortgage note is a specific type of promissory note that is secured by real estate. It details the borrower's promise to repay the loan used to purchase a home or property. Like a standard promissory note, it includes the loan amount, interest rate, and repayment terms, but it also outlines the consequences of default, which can include foreclosure on the property.

Lastly, an Installment Agreement is similar in nature to a Kentucky Promissory Note. This document is used when a borrower agrees to repay a loan in fixed installments over time. It specifies the total loan amount, the number of payments, and the amount of each installment. While a promissory note may not always specify the payment structure, an installment agreement clearly lays out the repayment plan, providing both parties with a clear understanding of their obligations.

When filling out the Kentucky Promissory Note form, it’s important to be careful and thorough. Here are some key dos and don'ts to keep in mind:

By following these guidelines, you can help ensure that your Kentucky Promissory Note is filled out correctly and is legally binding.

When it comes to the Kentucky Promissory Note form, there are several misconceptions that can lead to confusion. Here’s a breakdown of some common misunderstandings:

Understanding these misconceptions can help individuals and businesses navigate the use of promissory notes more effectively. Clarity is key when it comes to financial agreements.

When filling out and using the Kentucky Promissory Note form, there are several important points to consider. Understanding these can help ensure that the document serves its intended purpose effectively.

By keeping these key takeaways in mind, individuals can navigate the process of creating a promissory note with greater confidence.