In the realm of financial agreements, the Kansas Promissory Note form serves as a vital tool for individuals and businesses alike, facilitating clear communication and understanding between lenders and borrowers. This legally binding document outlines the specific terms of a loan, including the principal amount, interest rate, repayment schedule, and any applicable late fees. By establishing these parameters, the form helps to prevent misunderstandings and disputes that may arise during the repayment process. Additionally, it includes essential details such as the names and addresses of both parties, the date of the agreement, and the signatures required to validate the contract. Understanding the nuances of this form is crucial, as it ensures that both parties are protected under Kansas law, allowing for a smoother transaction and fostering trust in the lending relationship. Whether you are borrowing money for personal needs or for a business venture, having a well-drafted Kansas Promissory Note can make all the difference in securing your financial future.

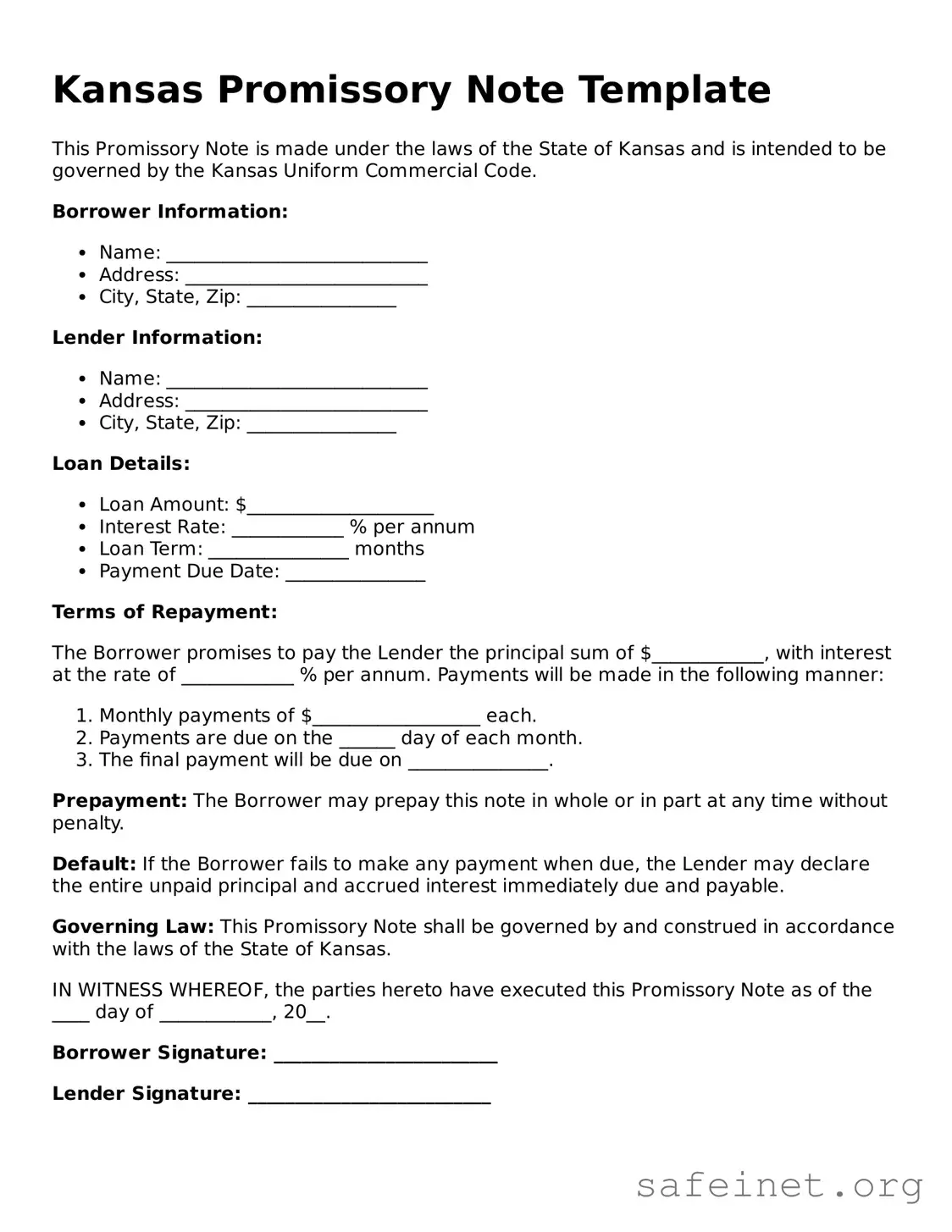

Kansas Promissory Note Template

This Promissory Note is made under the laws of the State of Kansas and is intended to be governed by the Kansas Uniform Commercial Code.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower promises to pay the Lender the principal sum of $____________, with interest at the rate of ____________ % per annum. Payments will be made in the following manner:

Prepayment: The Borrower may prepay this note in whole or in part at any time without penalty.

Default: If the Borrower fails to make any payment when due, the Lender may declare the entire unpaid principal and accrued interest immediately due and payable.

Governing Law: This Promissory Note shall be governed by and construed in accordance with the laws of the State of Kansas.

IN WITNESS WHEREOF, the parties hereto have executed this Promissory Note as of the ____ day of ____________, 20__.

Borrower Signature: ________________________

Lender Signature: __________________________

| Fact Name | Description |

|---|---|

| Definition | A Kansas Promissory Note is a written promise to pay a specified amount of money to a designated party at a predetermined time or on demand. |

| Governing Law | The Kansas Promissory Note is governed by the Uniform Commercial Code (UCC) as adopted in Kansas, specifically K.S.A. 84-3-104 et seq. |

| Parties Involved | The note typically involves two parties: the borrower (maker) who promises to pay and the lender (payee) who will receive the payment. |

| Interest Rate | The interest rate can be fixed or variable, and it must be clearly stated in the note to avoid confusion. |

| Payment Terms | Payment terms must be specified, including the due date, payment frequency, and any late fees applicable. |

| Default Conditions | Conditions under which the borrower may be considered in default should be outlined, including any grace periods or remedies available to the lender. |

| Signatures | Both parties must sign the note for it to be enforceable. Witnesses or notarization may also be recommended for additional legal protection. |

Filling out the Kansas Promissory Note form is an important step in formalizing a loan agreement between a borrower and a lender. Once you have completed the form, it is essential to ensure that both parties understand the terms outlined within it. This understanding will help prevent misunderstandings and ensure that everyone is on the same page regarding repayment expectations.

What is a Kansas Promissory Note?

A Kansas Promissory Note is a written agreement where one party promises to pay a specific amount of money to another party at a designated time or on demand. It serves as a legal document that outlines the terms of the loan, including the interest rate, repayment schedule, and any penalties for late payment.

Who can use a Kansas Promissory Note?

Any individual or business can use a Kansas Promissory Note. It is commonly used in personal loans, business transactions, and real estate deals. Both lenders and borrowers benefit from having a clear record of the agreement.

What are the key components of a Kansas Promissory Note?

A typical Kansas Promissory Note includes the names and addresses of the borrower and lender, the principal amount, the interest rate, the repayment schedule, and any collateral involved. It may also specify the consequences of default and any applicable fees.

Is a Kansas Promissory Note legally binding?

Yes, a properly executed Kansas Promissory Note is legally binding. Once signed by both parties, it can be enforced in a court of law. It is important that all terms are clear and agreed upon to avoid disputes later.

Do I need a lawyer to create a Kansas Promissory Note?

While it is not legally required to have a lawyer draft a Kansas Promissory Note, consulting with one can be beneficial. A lawyer can help ensure that the document complies with state laws and adequately protects your interests.

Can I modify a Kansas Promissory Note after it has been signed?

Yes, modifications can be made to a Kansas Promissory Note, but they must be agreed upon by both parties. It is advisable to document any changes in writing and have both parties sign the amended agreement to avoid confusion.

What happens if the borrower defaults on the Kansas Promissory Note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit or pursuing collection efforts. The specific remedies available depend on the terms outlined in the note.

Can a Kansas Promissory Note be used for business loans?

Yes, Kansas Promissory Notes are frequently used for business loans. They provide a clear framework for repayment terms and can be tailored to suit the needs of the business and the lender.

What is the difference between a secured and an unsecured Kansas Promissory Note?

A secured Kansas Promissory Note is backed by collateral, such as property or equipment. If the borrower defaults, the lender can claim the collateral. An unsecured note, on the other hand, does not have collateral backing it, making it riskier for the lender.

Where can I find a Kansas Promissory Note template?

Templates for Kansas Promissory Notes can be found online through legal document websites, local law libraries, or by consulting with a legal professional. It is essential to ensure that any template used complies with Kansas laws.

Not providing complete borrower information. Ensure that all fields, including name, address, and contact details, are filled out accurately.

Failing to specify the loan amount. Clearly state the exact amount being borrowed to avoid confusion later.

Omitting the interest rate. Specify whether the loan is interest-free or state the applicable interest rate.

Not including the repayment schedule. Clearly outline when payments are due and the total duration of the loan.

Using vague language. Be specific in all descriptions to prevent misunderstandings between parties.

Neglecting to sign and date the document. Both the borrower and lender must sign and date the form for it to be valid.

Forgetting to include any collateral details. If the loan is secured, specify the collateral to protect the lender's interests.

Not keeping a copy of the signed note. Retain a copy for your records to ensure both parties have access to the agreement.

Ignoring state-specific requirements. Familiarize yourself with Kansas laws regarding promissory notes to ensure compliance.

When dealing with a Kansas Promissory Note, several other forms and documents may be necessary to ensure a smooth transaction. Each document serves a specific purpose and helps clarify the terms of the agreement between the parties involved.

Understanding these additional documents can help both lenders and borrowers navigate the lending process more effectively. Each form plays a vital role in protecting the interests of all parties involved.

The Kansas Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms under which money is borrowed and specify the obligations of the borrower. A Loan Agreement typically includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. Like a Promissory Note, it serves as a legal record of the transaction, ensuring both parties understand their responsibilities. However, a Loan Agreement may be more comprehensive, often covering additional clauses regarding collateral or default conditions.

Another document akin to the Kansas Promissory Note is a Secured Promissory Note. This type of note is similar in that it represents a promise to pay back borrowed funds. However, it includes a security interest in an asset, which serves as collateral for the loan. If the borrower fails to repay, the lender has the right to seize the collateral. This added layer of security makes a Secured Promissory Note a more protective option for lenders, while still maintaining the basic structure of a standard Promissory Note.

A third comparable document is the IOU, or "I Owe You." An IOU is a simple acknowledgment of debt between two parties. While it lacks the formal structure and terms found in a Promissory Note, it still conveys the borrower's obligation to repay. Both documents can serve as evidence of a debt, but an IOU typically does not include interest rates or repayment schedules, making it less formal and less enforceable in legal terms.

Lastly, the Kansas Promissory Note is similar to a Personal Loan Agreement. This document, like the Promissory Note, outlines the terms of borrowing between individuals. It details the loan amount, interest rate, and repayment terms. The key difference lies in the level of detail and legal enforceability; Personal Loan Agreements often include more extensive terms and conditions, making them more formal than a simple Promissory Note. Both documents facilitate personal lending, but the Personal Loan Agreement provides a more structured approach to the borrowing process.

When filling out the Kansas Promissory Note form, it's essential to approach the process with care. Here is a list of things you should and shouldn't do:

Understanding the Kansas Promissory Note form can be challenging, and several misconceptions often arise. Below is a list of ten common misconceptions, along with clarifications to help demystify this important financial document.

By understanding these misconceptions, individuals and businesses can navigate the complexities of promissory notes more effectively and ensure that their agreements are clear and enforceable.

When filling out and using the Kansas Promissory Note form, it is essential to understand several key aspects to ensure the document is valid and enforceable.

By paying attention to these key points, you can create a solid and enforceable promissory note in Kansas.