The IRS W-8BEN form plays a crucial role for foreign individuals and entities engaged in financial transactions within the United States. This form is primarily used to establish foreign status and claim beneficial ownership of income that is subject to U.S. tax withholding. By completing the W-8BEN, individuals can assert their eligibility for reduced withholding tax rates under applicable tax treaties. The form requires personal information such as name, country of citizenship, and taxpayer identification number, if applicable. Additionally, it includes sections where individuals can declare their claim for tax treaty benefits, ensuring they are not subject to higher tax rates than necessary. The W-8BEN must be submitted to the withholding agent or financial institution, rather than the IRS, and it remains valid for a period of three years unless there are changes in circumstances that would affect its accuracy. Understanding the importance of this form is essential for anyone looking to navigate the complexities of U.S. tax obligations effectively.

Form |

|

|

Certificate of Foreign Status of Beneficial Owner for United |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

States Tax Withholding and Reporting (Individuals) |

|

|

|

|

|

|

(Rev. October 2021) |

|

|

▶ For use by individuals. Entities must use Form |

|

|

OMB No. |

|||

Department of the Treasury |

|

|

▶ Go to www.irs.gov/FormW8BEN for instructions and the latest information. |

|

|

|

|

|

|

Internal Revenue Service |

|

|

▶ Give this form to the withholding agent or payer. Do not send to the IRS. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Do NOT use this form if: |

|

|

|

Instead, use Form: |

|||||

• You are NOT an individual |

. |

. |

. . |

. |

|||||

• You are a U.S. citizen or other U.S. person, including a resident alien individual |

. |

. |

. . |

. |

. |

. |

|||

• You are a beneficial owner claiming that income is effectively connected with the conduct of trade or business within the United States |

|

|

|

||||||

(other than personal services) |

. |

. |

. . |

. |

. |

||||

• You are a beneficial owner who is receiving compensation for personal services performed in the United States . . . |

. |

. |

. . |

|

8233 or |

||||

• You are a person acting as an intermediary |

. |

. |

. . |

. |

. |

||||

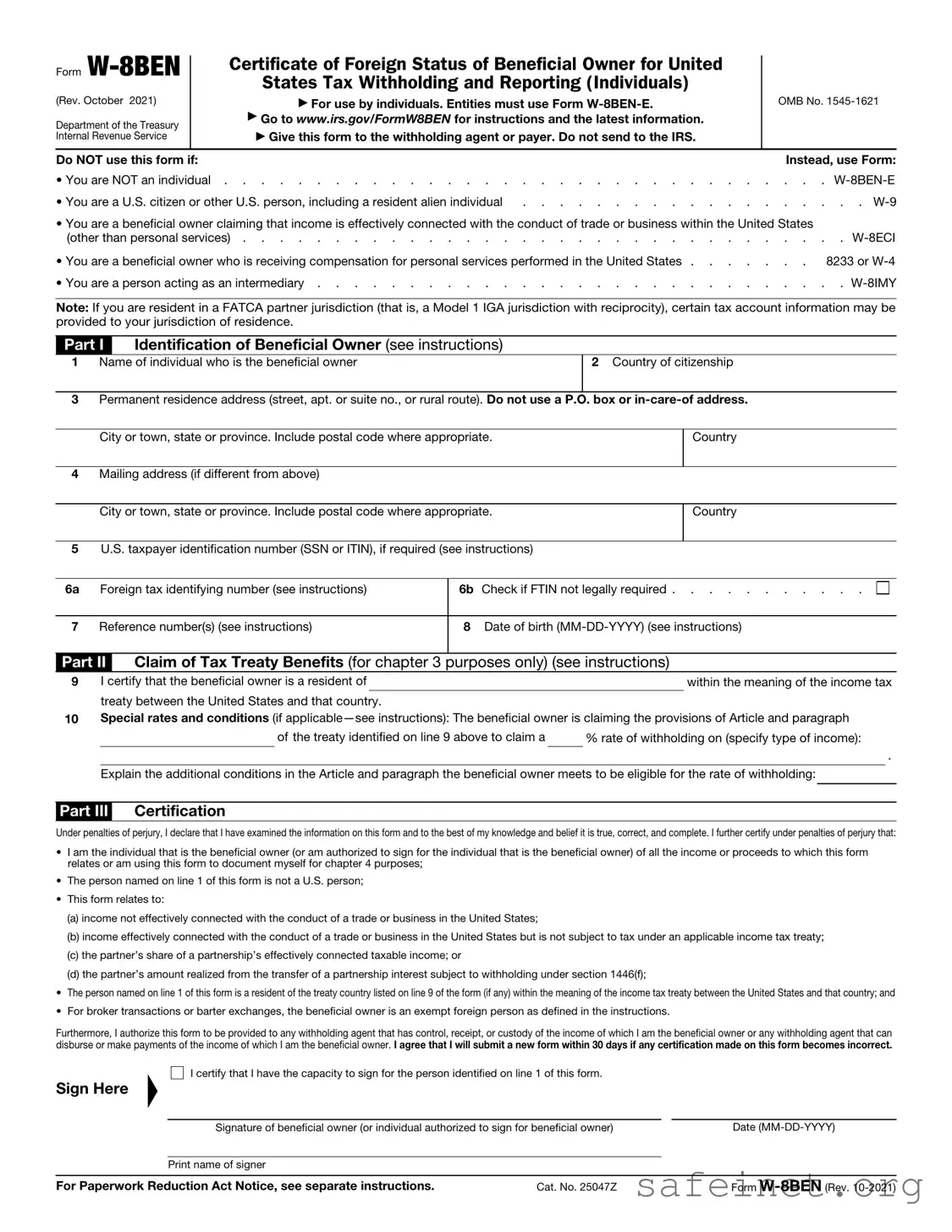

Note: If you are resident in a FATCA partner jurisdiction (that is, a Model 1 IGA jurisdiction with reciprocity), certain tax account information may be provided to your jurisdiction of residence.

Part I Identification of Beneficial Owner (see instructions)

1Name of individual who is the beneficial owner

2Country of citizenship

3Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box or

City or town, state or province. Include postal code where appropriate.

Country

4Mailing address (if different from above)

City or town, state or province. Include postal code where appropriate.

Country

5U.S. taxpayer identification number (SSN or ITIN), if required (see instructions)

6a Foreign tax identifying number (see instructions) |

6b Check if FTIN not legally required |

|

|

7 Reference number(s) (see instructions) |

8 Date of birth |

Part II Claim of Tax Treaty Benefits (for chapter 3 purposes only) (see instructions)

9 I certify that the beneficial owner is a resident of treaty between the United States and that country.

10Special rates and conditions (if

of the treaty identified on line 9 above to claim a |

% rate of withholding on (specify type of income): |

.

Explain the additional conditions in the Article and paragraph the beneficial owner meets to be eligible for the rate of withholding:

Part III Certification

Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that:

•I am the individual that is the beneficial owner (or am authorized to sign for the individual that is the beneficial owner) of all the income or proceeds to which this form relates or am using this form to document myself for chapter 4 purposes;

•The person named on line 1 of this form is not a U.S. person;

•This form relates to:

(a)income not effectively connected with the conduct of a trade or business in the United States;

(b)income effectively connected with the conduct of a trade or business in the United States but is not subject to tax under an applicable income tax treaty;

(c)the partner’s share of a partnership’s effectively connected taxable income; or

(d)the partner’s amount realized from the transfer of a partnership interest subject to withholding under section 1446(f);

•The person named on line 1 of this form is a resident of the treaty country listed on line 9 of the form (if any) within the meaning of the income tax treaty between the United States and that country; and

•For broker transactions or barter exchanges, the beneficial owner is an exempt foreign person as defined in the instructions.

Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can disburse or make payments of the income of which I am the beneficial owner. I agree that I will submit a new form within 30 days if any certification made on this form becomes incorrect.

Sign Here

▲

I certify that I have the capacity to sign for the person identified on line 1 of this form.

|

Signature of beneficial owner (or individual authorized to sign for beneficial owner) |

|

Date |

|

|

|

|

|

|

|

Print name of signer |

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 25047Z |

|

Form |

|

| Fact Name | Description |

|---|---|

| Purpose | The W-8BEN form is used by foreign individuals to certify their foreign status and claim tax treaty benefits. |

| Who Uses It | Non-U.S. residents receiving income from U.S. sources, such as interest, dividends, or royalties, typically use this form. |

| Validity Period | The form remains valid until the end of the third calendar year following the year it is signed, unless there are changes in circumstances. |

| Tax Treaty Benefits | By submitting the W-8BEN, individuals may reduce or eliminate U.S. withholding tax on certain types of income due to tax treaties. |

| Submission Process | The completed form is submitted to the U.S. withholding agent or financial institution, not the IRS directly. |

| State-Specific Considerations | Some states may have their own forms or requirements for non-residents; for example, California has specific guidelines governed by California Revenue and Taxation Code. |

| Penalties for Misuse | Providing false information on the W-8BEN can lead to penalties, including the possibility of being subject to higher withholding rates. |

After obtaining the IRS W-8BEN form, you will need to fill it out accurately to ensure compliance with tax regulations. Completing this form is essential for non-U.S. residents who receive income from U.S. sources. Follow these steps to fill out the form correctly.

Once you have filled out the form, review it for accuracy. Submit the completed W-8BEN to the appropriate U.S. entity requesting it, such as a bank or employer. Keep a copy for your records.

What is the IRS W-8BEN form?

The IRS W-8BEN form is a document used by non-U.S. persons to certify their foreign status. This form helps individuals and entities claim a reduced rate of, or exemption from, U.S. withholding tax on certain types of income. It’s particularly important for foreign investors receiving income from U.S. sources, such as dividends or royalties. By submitting this form, you can ensure that you are not subject to the standard withholding tax rates that apply to U.S. citizens and residents.

Who needs to fill out the W-8BEN form?

Non-U.S. individuals or entities that receive income from U.S. sources typically need to complete the W-8BEN form. This includes foreign investors, foreign freelancers, and anyone else who is not a U.S. citizen or resident but earns income in the United States. If you’re unsure whether you need to fill out this form, it’s wise to consult a tax professional who can provide guidance based on your specific situation.

How do I complete the W-8BEN form?

Completing the W-8BEN form involves several steps. First, you need to provide your name, country of citizenship, and address. Next, you’ll indicate your foreign tax identification number, if applicable. After that, you will need to sign and date the form, certifying that the information provided is accurate. Make sure to follow the instructions carefully to avoid any errors that could delay processing or lead to incorrect withholding rates.

Where do I send the W-8BEN form once it’s completed?

The completed W-8BEN form is generally sent to the U.S. withholding agent or financial institution that requested it. This could be a bank, brokerage, or any entity that is responsible for paying you income. Do not send the form directly to the IRS unless specifically instructed to do so. Keep a copy for your records, as it may be necessary for future transactions.

How long is the W-8BEN form valid?

The W-8BEN form is valid for a period of three years from the date you sign it. However, if your circumstances change—such as a change in your residency status or a change in the information provided on the form—you will need to submit a new form. It’s essential to keep your information up to date to ensure you continue to benefit from the appropriate tax treatment.

Failing to provide accurate personal information. It’s essential to ensure that your name, country of citizenship, and address are correct. Any discrepancies can lead to delays or rejection of the form.

Not using the correct version of the form. The IRS updates forms periodically. Using an outdated version can cause issues, so always check for the latest version on the IRS website.

Overlooking the need for a taxpayer identification number (TIN). If you have a TIN, it should be included. This number helps the IRS identify you correctly.

Incorrectly completing the certification section. This section requires you to certify that the information provided is accurate. Make sure to read the certification carefully before signing.

Neglecting to sign and date the form. A signature is crucial. Without it, the form is considered incomplete, and the IRS will not process it.

Submitting the form to the wrong entity. The W-8BEN form is meant for withholding agents or financial institutions, not the IRS. Ensure you send it to the correct recipient.

Providing inconsistent information across forms. If you are filling out multiple tax forms, ensure that the information matches. Inconsistencies can raise red flags.

Not keeping a copy for your records. After submitting the form, retain a copy for your own documentation. This will be helpful for future reference or in case of an audit.

The IRS W-8BEN form is essential for foreign individuals or entities receiving income from U.S. sources. It helps establish foreign status and claim any applicable tax treaty benefits. However, it is often accompanied by other forms and documents that further clarify the taxpayer's situation. Below is a list of additional documents that are commonly used alongside the W-8BEN.

Understanding these forms and their purposes is vital for anyone navigating the complexities of U.S. tax regulations as a foreign individual or entity. Each document plays a specific role in ensuring compliance and optimizing tax obligations, making it essential to have them in order when dealing with U.S. income sources.

The IRS W-8BEN form is often compared to the W-8BEN-E form, which is also used by foreign entities to certify their status for tax purposes. While the W-8BEN is intended for individuals, the W-8BEN-E is designed for businesses. Both forms serve to establish that the individual or entity is not a U.S. taxpayer, thus allowing them to claim a reduced rate of withholding tax on certain types of income received from U.S. sources.

Another similar document is the W-9 form, which is used by U.S. persons to provide their taxpayer identification number to payers. Unlike the W-8BEN, the W-9 certifies that the individual or entity is a U.S. taxpayer. This form is crucial for those who are subject to U.S. tax laws and need to report income to the IRS, contrasting with the W-8BEN's purpose of avoiding U.S. taxation for foreign individuals.

The 1042-S form is also related, as it is used to report income paid to foreign persons and the amount of tax withheld. When a foreign individual submits a W-8BEN, the payer may use the information to determine the appropriate withholding rate and report the income on a 1042-S. This document is essential for compliance with U.S. tax regulations regarding foreign income recipients.

Another document is the W-8IMY form, which is used by intermediaries, such as partnerships or trusts, to certify their status. This form allows intermediaries to pass on the benefits of reduced withholding rates to their foreign partners or beneficiaries. Like the W-8BEN, the W-8IMY helps clarify the tax status of the entity in question to ensure proper tax treatment.

The 8833 form, known as the Treaty-Based Return Position Disclosure, is also relevant. This form is used by foreign individuals or entities claiming a tax treaty benefit. While the W-8BEN serves to establish foreign status, the 8833 provides additional information about the specific treaty provisions being relied upon to reduce or eliminate U.S. tax withholding.

The 1040NR form is another important document for non-resident aliens. This form is used to report income earned in the U.S. by foreign individuals. While the W-8BEN is primarily for certifying foreign status and claiming benefits, the 1040NR is the actual tax return that must be filed to report any U.S. income and pay any taxes owed.

The 8832 form, which is an Entity Classification Election, is relevant for foreign entities that wish to elect how they are classified for tax purposes. While the W-8BEN-E is used to certify foreign status, the 8832 allows entities to choose whether they want to be treated as a corporation or a partnership for U.S. tax purposes, impacting their overall tax obligations.

The IRS Form 1065 is used by partnerships to report income, deductions, gains, and losses. Foreign partners in a U.S. partnership may submit a W-8BEN to certify their foreign status, while the partnership itself uses Form 1065 to report its financial activities. This interplay between the two forms ensures that tax obligations are properly managed for both U.S. and foreign partners.

Lastly, the Form 1120-F is utilized by foreign corporations to report income effectively connected with a U.S. trade or business. Similar to the W-8BEN, which certifies foreign status, the Form 1120-F is necessary for foreign corporations to report their income and claim deductions, ensuring compliance with U.S. tax laws.

When filling out the IRS W-8BEN form, it is crucial to ensure accuracy and compliance. Here is a list of things to do and avoid during the process.

Completing the IRS W-8BEN form accurately is essential for proper tax treatment. Take the time to follow these guidelines to avoid potential issues.

The IRS W-8BEN form is often misunderstood. Here are five common misconceptions about this important tax document:

Understanding these misconceptions can help individuals and entities navigate their tax obligations more effectively. It is essential to approach the W-8BEN form with accurate information and awareness of its purpose.

The IRS W-8BEN form is essential for non-U.S. residents receiving income from U.S. sources. Here are key takeaways to keep in mind:

Understanding these points will help you navigate the W-8BEN form effectively.