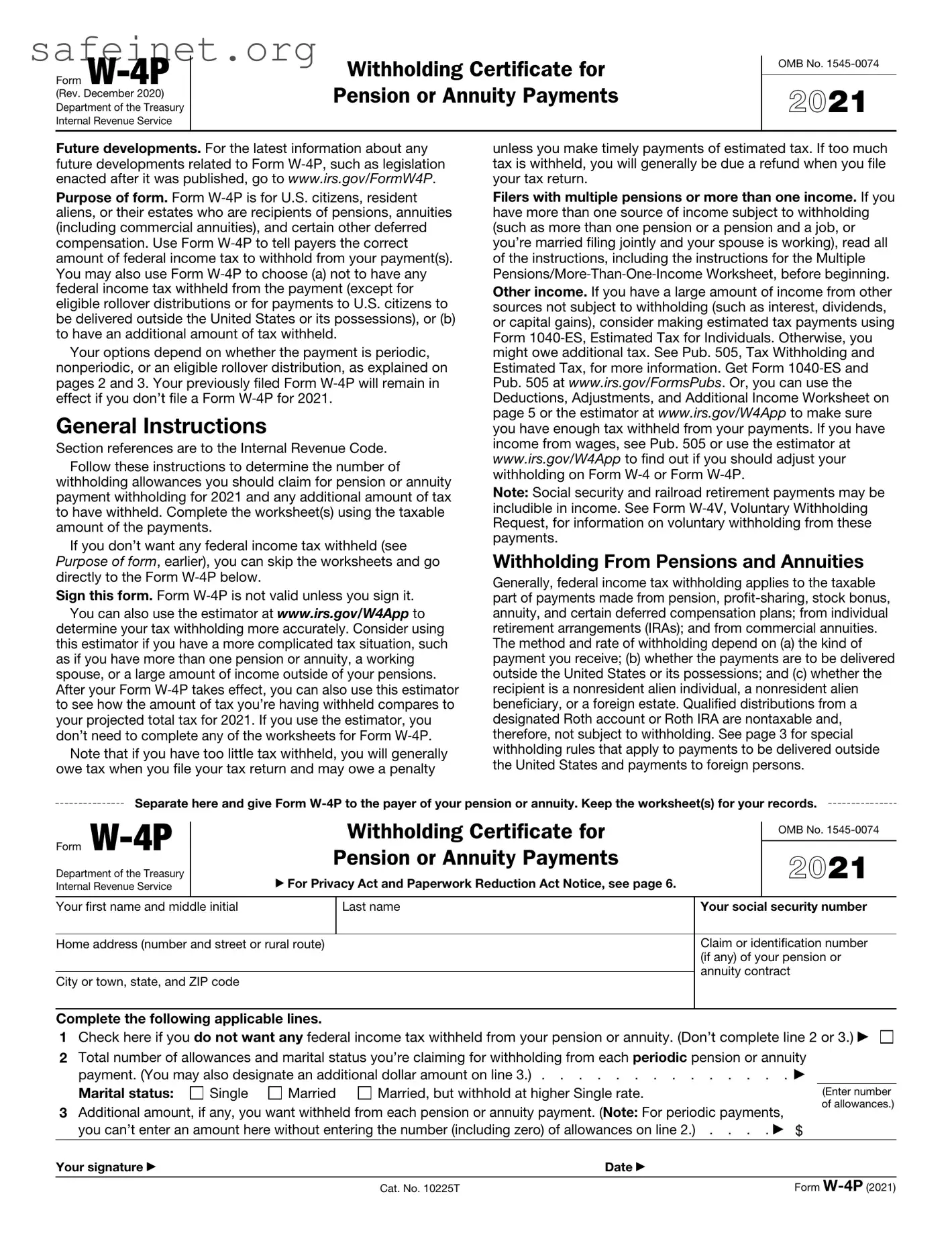

The IRS W-4P form is a crucial document for individuals receiving pensions or annuities, helping to ensure the correct amount of federal income tax is withheld from these payments. This form is used primarily by retirees and beneficiaries of pensions who wish to specify their withholding preferences to avoid underpayment or overpayment of taxes. It allows individuals to indicate their filing status and the number of allowances they are claiming, which directly impacts their tax withholding rate. Additionally, the form provides space for individuals to request additional amounts to be withheld if they anticipate needing extra withholdings due to other income sources. By understanding the major aspects of the W-4P, retirees can make informed decisions that contribute to their financial stability and tax compliance. Proper completion and submission of this form can lead to smoother transactions and fewer unexpected tax bills in the future.

Form

(Rev. December 2020)

Department of the Treasury

Internal Revenue Service

Withholding Certificate for Pension or Annuity Payments

OMB No.

2021

Future developments. For the latest information about any future developments related to Form W‐4P, such as legislation enacted after it was published, go to www.irs.gov/FormW4P.

Purpose of form. Form W‐4P is for U.S. citizens, resident aliens, or their estates who are recipients of pensions, annuities (including commercial annuities), and certain other deferred compensation. Use Form W‐4P to tell payers the correct amount of federal income tax to withhold from your payment(s). You may also use Form W‐4P to choose (a) not to have any federal income tax withheld from the payment (except for eligible rollover distributions or for payments to U.S. citizens to be delivered outside the United States or its possessions), or (b) to have an additional amount of tax withheld.

Your options depend on whether the payment is periodic, nonperiodic, or an eligible rollover distribution, as explained on pages 2 and 3. Your previously filed Form W‐4P will remain in effect if you don’t file a Form W‐4P for 2021.

General Instructions

Section references are to the Internal Revenue Code.

Follow these instructions to determine the number of withholding allowances you should claim for pension or annuity payment withholding for 2021 and any additional amount of tax to have withheld. Complete the worksheet(s) using the taxable amount of the payments.

If you don’t want any federal income tax withheld (see Purpose of form, earlier), you can skip the worksheets and go directly to the Form W‐4P below.

Sign this form. Form W‐4P is not valid unless you sign it.

You can also use the estimator at www.irs.gov/W4App to determine your tax withholding more accurately. Consider using this estimator if you have a more complicated tax situation, such as if you have more than one pension or annuity, a working spouse, or a large amount of income outside of your pensions. After your Form W‐4P takes effect, you can also use this estimator to see how the amount of tax you’re having withheld compares to your projected total tax for 2021. If you use the estimator, you don’t need to complete any of the worksheets for Form W‐4P.

Note that if you have too little tax withheld, you will generally owe tax when you file your tax return and may owe a penalty

unless you make timely payments of estimated tax. If too much tax is withheld, you will generally be due a refund when you file your tax return.

Filers with multiple pensions or more than one income. If you have more than one source of income subject to withholding (such as more than one pension or a pension and a job, or you’re married filing jointly and your spouse is working), read all of the instructions, including the instructions for the Multiple Pensions/More‐Than‐One‐Income Worksheet, before beginning.

Other income. If you have a large amount of income from other sources not subject to withholding (such as interest, dividends, or capital gains), consider making estimated tax payments using Form 1040‐ES, Estimated Tax for Individuals. Otherwise, you might owe additional tax. See Pub. 505, Tax Withholding and Estimated Tax, for more information. Get Form 1040‐ES and Pub. 505 at www.irs.gov/FormsPubs. Or, you can use the Deductions, Adjustments, and Additional Income Worksheet on page 5 or the estimator at www.irs.gov/W4App to make sure you have enough tax withheld from your payments. If you have income from wages, see Pub. 505 or use the estimator at www.irs.gov/W4App to find out if you should adjust your withholding on Form W‐4 or Form W‐4P.

Note: Social security and railroad retirement payments may be includible in income. See Form W‐4V, Voluntary Withholding Request, for information on voluntary withholding from these payments.

Withholding From Pensions and Annuities

Generally, federal income tax withholding applies to the taxable part of payments made from pension,

Separate here and give Form

Form

Department of the Treasury Internal Revenue Service

Withholding Certificate for

Pension or Annuity Payments

▶For Privacy Act and Paperwork Reduction Act Notice, see page 6.

OMB No.

2021

Your first name and middle initial |

Last name |

Your social security number |

|

|

|

Home address (number and street or rural route) |

|

Claim or identification number |

|

|

(if any) of your pension or |

|

|

annuity contract |

City or town, state, and ZIP code |

|

|

|

|

|

|

|

|

Complete the following applicable lines.

1Check here if you do not want any federal income tax withheld from your pension or annuity. (Don’t complete line 2 or 3.) ▶

2Total number of allowances and marital status you’re claiming for withholding from each periodic pension or annuity payment. (You may also designate an additional dollar amount on line 3.) . . . . . . . . . . . . . . ▶

Marital status: |

Single |

Married |

Married, but withhold at higher Single rate. |

3Additional amount, if any, you want withheld from each pension or annuity payment. (Note: For periodic payments,

you can’t enter an amount here without entering the number (including zero) of allowances on line 2.) . . . . ▶ $

(Enter number of allowances.)

Your signature ▶ |

Date ▶ |

Cat. No. 10225T |

Form |

Form |

Page 2 |

Because your tax situation may change from year to year, you may want to refigure your withholding each year. You can change the amount to be withheld by using lines 2 and 3 of Form

Choosing not to have income tax withheld. You (or in the event of death, your beneficiary or estate) can choose not to have federal income tax withheld from your payments by using line 1 of Form

You may not make this choice for eligible rollover distributions. See Eligible rollover

Caution: There are penalties for not paying enough federal income tax during the year, either through withholding or estimated tax payments. New retirees, especially, should see Pub. 505. It explains your estimated tax requirements and describes penalties in detail. You may be able to avoid quarterly estimated tax payments by having enough tax withheld from your pension or annuity using Form

Periodic payments. Withholding from periodic payments of a pension or annuity is figured using certain withholding tables that are also used to figure withholding from wages. Periodic payments are made in installments at regular intervals over a period of more than 1 year. They may be paid annually, quarterly, monthly, etc.

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

If you don’t want any federal income tax withheld from your periodic payments, check the box on line 1 of Form

Caution: If you don’t submit Form

If you submit a Form

you’re single claiming zero withholding allowances even if you checked the box on line 1 to have no federal income tax withheld.

There are some kinds of periodic payments for which you can’t use Form

For periodic payments, your Form

Nonperiodic

Caution: If you submit a Form

Eligible rollover

Form |

Page 3 |

Note: The payer won’t withhold federal income tax if the entire distribution is transferred by the plan administrator in a direct rollover to a traditional IRA or another eligible retirement plan (if allowed by the plan), such as a 401(k) plan, qualified pension plan, governmental section 457(b) plan, section 403(b) contract, or

Distributions that are (a) required by federal law, (b) one of a specified series of equal payments, or (c) qualifying “hardship” distributions are not “eligible rollover distributions” and aren’t subject to the mandatory 20% federal income tax withholding.

See Pub. 505 for details. See also Nonperiodic

Tax relief for victims of terrorist attacks. For tax years ending after September 10, 2001, disability payments for injuries incurred as a direct result of a terrorist attack directed against the United States (or its allies), whether outside or within the United States, aren’t included in income. You may check the box on line 1 of Form

Changing Your “No Withholding” Choice

Periodic payments. If you previously chose not to have federal income tax withheld and you now want withholding, complete another Form

Nonperiodic payments. If you previously chose not to have federal income tax withheld and you now want withholding, write “Revoked” next to the checkbox on line 1 and submit the Form

Payments to Foreign Persons and Payments To Be Delivered Outside the United States

Unless you’re a nonresident alien, withholding (in the manner described above) is required on any periodic or nonperiodic payments that are to be delivered to you outside the United States or its possessions. Don’t check the box on line 1 of Form

In the absence of a tax treaty exemption, nonresident aliens, nonresident alien beneficiaries, and foreign estates are generally subject to a 30% federal withholding tax under section 1441 on the taxable portion of a periodic or nonperiodic pension or annuity payment that is from U.S. sources. However, most tax treaties provide that private pensions and annuities are exempt from withholding and tax. Also, payments from certain pension plans are exempt from withholding even if no tax treaty applies. See Pub. 515, Withholding of Tax on Nonresident Aliens and Foreign Entities, and Pub. 519, U.S. Tax Guide for Aliens, for details. A foreign person should submit Form

Statement of Federal Income Tax Withheld From Your Pension or Annuity

By January 31 of next year, your payer will furnish a statement to you on Form

Specific Instructions

Personal Allowances Worksheet

Complete this worksheet on page 4 first to determine the number of withholding allowances to claim.

Line C. Head of household please note: Generally, you can claim head of household filing status on your tax return only if you’re unmarried and pay more than 50% of the costs of keeping up a home for yourself and a qualifying individual. See Pub. 501 for more information about filing status.

Line D. Child tax credit. When you file your tax return, you may be eligible to claim a child tax credit for each of your eligible children. To qualify, the child must be under age 17 as of December 31, must be your dependent who generally lives with you for more than half the year, and must have the required SSN. To learn more about this credit, see Pub. 972, Child Tax Credit and Credit for Other Dependents. To reduce the tax withheld from your payments by taking this credit into account, follow the instructions on line D of the worksheet. On the worksheet, you will be asked about your total income. For this purpose, total income includes all of your pensions, wages, and other income, including income earned by a spouse if you’re filing a joint return.

Line E. Credit for other dependents. When you file your tax return, you may be eligible to claim a credit for other dependents for whom a child tax credit can’t be claimed, such as a qualifying child who does not meet the age or SSN requirement for the child tax credit, or a qualifying relative. To learn more about this credit, see Pub. 972. To reduce the tax withheld from your payments by taking this credit into account, follow the instructions on line E of the worksheet. On the worksheet, you will be asked about your total income. For this purpose, total income includes all of your pensions, wages, and other income, including income earned by a spouse if you’re filing a joint return.

Line F. Other credits. You may be able to reduce the tax withheld from your payments if you expect to claim other tax credits, such as tax credits for education (discussed in Pub.

970). If you do so, your payments will be larger, but the amount of any refund that you receive when you file your tax return will be smaller. Follow the instructions for the worksheet for converting credits to allowances in Pub. 505 if you want to reduce your withholding by taking these credits into account. If you figure all your credits using that worksheet in Pub. 505, enter

Deductions, Adjustments, and Additional Income Worksheet

Complete this worksheet to determine if you’re able to reduce the tax withheld from your pension or annuity payments to account for your itemized deductions and other adjustments to income, such as deductible IRA contributions. If you do so, your refund at the end of the year will be smaller, but your payments will be larger. You’re not required to complete this worksheet or reduce your withholding if you don’t wish to do so.

You can also use this worksheet to figure out how much to increase the tax withheld from your payments if you have a large amount of other income not subject to withholding, such as interest, dividends, or capital gains.

Another option is to take these items into account and make your withholding more accurate by using the estimator at www.irs.gov/W4App. If you use the estimator, you don’t need to complete any of the worksheets for Form W‐4P.

Multiple Pensions/More‐Than‐One‐Income Worksheet

Complete this worksheet if you receive more than one pension, if you have a pension and a job, or if you’re married filing jointly and have a working spouse or a spouse who receives a pension. If you don’t complete this worksheet, you might have too little tax withheld. If so, you will generally owe tax when you file your tax return and may be subject to a penalty.

Form |

Page 4 |

Use the Multiple

any allowances after lines A through B in the Personal Allowances Worksheet or any allowances in the Deductions, Adjustments, and Additional Income Worksheet. However, you may need to use the Multiple

Another option is to use the estimator at www.irs.gov/W4App to figure your withholding more precisely.

Personal Allowances Worksheet (Keep for your records.)

A |

Enter “2” for yourself |

A |

B |

Enter “1” if you will file as married filing jointly |

B |

C |

Enter “1” if you will file as head of household |

C |

DChild tax credit. See Pub. 972 for more information.

•If your total income will be less than $72,351 ($105,051 if married filing jointly), enter “4” for each eligible child.

•If your total income will be from $72,351 to $181,950 ($105,051 to $351,400 if married filing jointly), enter “2” for each eligible child.

•If your total income will be from $181,951 to $200,000 ($351,401 to $400,000 if married filing jointly), enter “1” for each eligible child.

• If your total income will be higher than $200,000 ($400,000 if married filing jointly), enter

ECredit for other dependents. See Pub. 972 for more information.

•If your total income will be less than $72,351 ($105,051 if married filing jointly), enter “1” for each eligible dependent.

•If your total income will be from $72,351 to $181,950 ($105,051 to $351,400 if married filing jointly), enter “1” for every two dependents (for example,

• If your total income will be higher than $181,950 ($351,400 if married filing jointly), enter

FOther credits. If you have other credits, see the worksheet for converting credits to allowances in Pub. 505 and enter the amount from that worksheet here. If you figure all your credits using that worksheet in Pub. 505, enter

F |

|||

G Add lines A through F and enter the total here . . . . . . . . . . . . . . . . . . . . . . ▶ |

G |

||

|

{ |

• If you plan to itemize or claim adjustments to income and want to reduce your withholding, or |

|

|

|

|

|

|

|

if you have a large amount of other income not subject to withholding and want to increase your |

|

|

|

withholding, see the Deductions, Adjustments, and Additional Income Worksheet on page 5. |

|

For accuracy, |

|

• If you have more than one source of income subject to withholding or are married filing |

|

complete all |

|

jointly and you and your spouse both have income subject to withholding and your |

|

worksheets |

|

combined income from all sources exceeds $13,000 ($25,000 if married filing jointly), see the |

|

that apply. |

|

Multiple |

|

tax withheld, or use the estimator for more accuracy.

Form |

Page 5 |

Deductions, Adjustments, and Additional Income Worksheet

Note: Use this worksheet only if you plan to itemize deductions, claim certain adjustments to income, or have a large amount of other income not subject to withholding.

1

2

Enter an estimate of your 2021 itemized deductions. These include qualifying home mortgage interest, |

|

|

|

charitable contributions, state and local taxes (up to $10,000), and medical expenses in excess of 7.5% |

|

|

|

of your income. See Pub. 505 for details |

1 |

$ |

|

$25,100 if you’re married filing jointly or qualifying widow(er) |

|

|

|

Enter: { $18,800 if you’re head of household |

} |

2 |

$ |

|

|

||

3 Subtract line 2 from line 1. If zero or less, enter |

3 |

$ |

4Enter an estimate of your 2021 adjustments to income, qualified business income deduction, and any

additional standard deduction for age or blindness. See Pub. 505 for information about these items . |

4 |

$ |

5 Add lines 3 and 4 and enter the total |

5 |

$ |

6Enter an estimate of your 2021 other income not subject to withholding (such as dividends, interest, or

capital gains) |

6 |

$ |

7 Subtract line 6 from line 5. If zero, enter |

7 |

$ |

8Divide the amount on line 7 by $4,300 and enter the result here. If a negative amount, enter in

parentheses. Drop any fraction |

8 |

9 Enter the number from the Personal Allowances Worksheet, line G, on page 4 |

9 |

10Add lines 8 and 9 and enter the total here. If zero or less, enter

|

|

here and enter this total on Form |

10 |

Multiple

Note: Use this worksheet only if the instructions under line G from the Personal Allowances Worksheet direct you here. This applies if you (and your spouse if married filing jointly) have more than one source of income subject to withholding (such as more than one pension, or a pension and a job, or you have a pension and your spouse works).

1Enter the number from the Personal Allowances Worksheet, line G, on page 4 (or from line 10 above if

you used the Deductions, Adjustments, and Additional Income Worksheet) |

1 |

2Find the number in Table 1 on page 6 that applies to the LOWEST paying pension or job and enter it here. However, if you’re married filing jointly and the amount from the highest paying pension or job is $75,000 or less and the combined amounts for you and your spouse are $107,000 or less, do not enter

more than “7” |

2 |

3If line 1 is more than or equal to line 2, subtract line 2 from line 1. Enter the result here (if zero, enter

3 |

Note: If line 1 is less than line 2, enter

4 |

Enter the number from line 2 of this worksheet |

4 |

|

|

|

5 |

Enter the number from line 1 of this worksheet |

5 |

|

|

|

6 |

Subtract line 5 from line 4 |

6 |

|

||

7 |

Find the amount in Table 2 on page 6 that applies to the HIGHEST paying pension or job and enter it here |

7 |

$ |

||

8 |

Multiply line 7 by line 6 and enter the result here. This is the additional annual withholding needed . . |

8 |

$ |

||

9Divide line 8 by the number of payments remaining in 2021. For example, divide by 8 if you’re paid

every month and you complete this form in April 2021. Enter the result here and on Form |

|

|

on page 1. This is the additional amount to be withheld from each payment |

9 |

$ |

Form |

|

|

|

|

|

|

|

|

|

Page 6 |

|

|

|

|

|

Table 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Married Filing Jointly |

|

|

|

|

All Others |

|

||

|

|

|

|

|

|

|

||||

If wages from LOWEST paying |

Enter on line 2 above |

|

If wages from LOWEST paying |

|

Enter on line 2 above |

|||||

job or pension are— |

|

job or pension are— |

|

|||||||

$0 |

- |

$799 |

|

0 |

|

$0 |

- |

$799 |

|

0 |

800 |

- |

5,100 |

|

1 |

|

800 |

- |

5,100 |

|

1 |

5,101 |

- |

9,400 |

|

2 |

|

5,101 |

- |

9,400 |

|

2 |

9,401 |

- |

13,700 |

|

3 |

|

9,401 |

- |

13,700 |

|

3 |

13,701 |

- |

18,000 |

|

4 |

|

13,701 |

- |

22,000 |

|

4 |

18,001 |

- |

22,300 |

|

5 |

|

22,001 |

- |

27,500 |

|

5 |

22,301 |

- |

26,600 |

|

6 |

|

27,501 |

- |

32,000 |

|

6 |

26,601 |

- |

35,000 |

|

7 |

|

32,001 |

- |

40,000 |

|

7 |

35,001 |

- |

40,000 |

|

8 |

|

40,001 |

- |

60,000 |

|

8 |

40,001 |

- |

46,000 |

|

9 |

|

60,001 |

- |

75,000 |

|

9 |

46,001 |

- |

55,000 |

|

10 |

|

75,001 |

- |

85,000 |

|

10 |

55,001 |

- |

60,000 |

|

11 |

|

85,001 |

- |

95,000 |

|

11 |

60,001 |

- |

70,000 |

|

12 |

|

95,001 |

- 100,000 |

|

12 |

|

70,001 |

- |

75,000 |

|

13 |

|

100,001 |

- 110,000 |

|

13 |

|

75,001 |

- |

85,000 |

|

14 |

|

110,001 |

- 115,000 |

|

14 |

|

85,001 |

- |

95,000 |

|

15 |

|

115,001 |

- 125,000 |

|

15 |

|

95,001 |

- 125,000 |

|

16 |

|

125,001 |

- 135,000 |

|

16 |

||

125,001 |

- 155,000 |

|

17 |

|

135,001 |

- 145,000 |

|

17 |

||

155,001 |

- 165,000 |

|

18 |

|

145,001 |

- 160,000 |

|

18 |

||

165,001 |

- 175,000 |

|

19 |

|

160,001 |

- 180,000 |

|

19 |

||

175,001 |

- 180,000 |

|

20 |

|

180,001 and over |

|

20 |

|||

180,001 |

- 195,000 |

|

21 |

|

|

|

|

|

|

|

195,001 |

- 205,000 |

|

22 |

|

|

|

|

|

|

|

205,001 and over |

|

23 |

|

|

|

|

|

|

||

|

|

|

|

|

Table 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Married Filing Jointly |

|

|

|

|

All Others |

|

||

|

|

|

|

|

|

|||||

If wages from HIGHEST paying |

Enter on line 7 above |

|

If wages from HIGHEST paying |

|

Enter on line 7 above |

|||||

job or pension are— |

|

job or pension are— |

|

|||||||

$0 |

- $25,350 |

|

$430 |

|

$0 |

- |

$7,375 |

|

$430 |

|

25,351 |

- |

85,850 |

|

520 |

|

7,376 |

- |

37,625 |

|

520 |

85,851 |

- 176,650 |

|

950 |

|

37,626 |

- |

83,025 |

|

950 |

|

176,651 |

- |

332,200 |

|

1,030 |

|

83,026 |

- |

160,800 |

|

1,030 |

332,201 |

- 420,300 |

|

1,380 |

|

160,801 |

- 204,850 |

|

1,380 |

||

420,301 |

- 627,650 |

|

1,510 |

|

204,851 |

- 515,900 |

|

1,510 |

||

627,651 and over |

|

1,590 |

|

515,901 and over |

|

1,590 |

||||

Privacy Act and Paperwork Reduction Act Notice

We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to provide this information only if you want to (a) request federal income tax withholding from periodic pension or annuity payments based on your withholding allowances and marital status;

(b)request additional federal income tax withholding from your pension or annuity; (c) choose not to have federal income tax withheld, when permitted; or (d) change or revoke a previous Form

Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths

and possessions for use in administering their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The average time and expenses required to complete and file this form will vary depending on individual circumstances. For estimated averages, see the instructions for your income tax return.

If you have suggestions for making this form simpler, we would be happy to hear from you. See the instructions for your income tax return.

| Fact Name | Description |

|---|---|

| What is the W-4P? | The W-4P is a form used by individuals to request withholding from pension or annuity payments. |

| Who needs to file it? | Taxpayers receiving pension benefits or annuity payments should file the W-4P. |

| When to submit? | The form should be submitted to the payer before the first payment is made. |

| How to adjust withholding? | Taxpayers can adjust their withholding by completing and submitting a new W-4P at any time. |

| Frequency of updates | The IRS recommends checking the W-4P yearly or when there are changes in income or tax situation. |

| Calculating withholding | Withholding is calculated based on the information provided on the form. |

| State-specific regulations | Each state may have its own withholding requirements; state laws vary. |

| Federal vs. State Forms | The W-4P is a federal form; state-specific forms may exist based on local laws. |

| Record keeping | Keep a copy of the W-4P for your personal records and tax preparation purposes. |

Completing the IRS W-4P form requires attention to detail and a clear understanding of your tax situation. Once filled out, this form can help ensure that your withholding amounts are optimal for your financial circumstances. Carefully following the instructions below will streamline the process for you.

What is the IRS W-4P form?

The IRS W-4P form, known as the "Withholding Certificate for Pension or Annuity Payments," is a document used by individuals to indicate their tax withholding preferences on pension or annuity payments. This form helps determine how much federal income tax should be withheld from these payments, thereby allowing individuals to manage their tax liability effectively.

Who should fill out the W-4P form?

Individuals receiving pension or annuity payments should fill out the W-4P form. This includes retirees or those who receive distributions from retirement accounts. Completing this form ensures that the correct amount of taxes is withheld, which can help prevent unexpected tax bills at the end of the year.

How do I complete the W-4P form?

To complete the W-4P form, individuals need to provide personal information such as their name, Social Security number, and address. They should also indicate their marital status and specify the number of allowances they wish to claim. Instructions provided with the form will guide you on how to determine the appropriate number of allowances and any additional amount to withhold, if desired.

When should I submit the W-4P form?

The W-4P form should be submitted to your pension fund or annuity provider before receiving payments. It's advisable to submit it as early as possible to ensure that the withholding begins with your first payment. If you need to make adjustments later, you can submit a new form at any time.

Can I change my withholding amount after I submit the W-4P?

Yes, individuals can change their withholding amount on the W-4P form whenever necessary. If your financial situation changes, such as a change in income or marital status, it is important to submit a new form to reflect these changes. This helps to ensure that the correct amount of tax continues to be withheld from your payments.

What happens if I do not submit a W-4P form?

If you do not submit a W-4P form, the pension or annuity provider will typically withhold taxes at the highest rate. This may result in a larger withholding than necessary, meaning you could end up with a sizeable tax refund when you file your return. However, it also increases the risk of under-withholding if your income changes, leading to potential tax liabilities at year-end.

What factors should I consider when deciding how much to withhold?

When deciding on withholding amounts, consider your total expected annual income, other sources of income, deductions, and credits. Use the IRS withholding calculator to help determine what amount may be appropriate based on your personal tax situation. It may also be beneficial to consult with a tax professional for personalized advice.

Where can I obtain the W-4P form?

The W-4P form can be obtained directly from the IRS website or through financial institutions that offer pension or annuity plans. It is essential to ensure that you are using the most current version of the form, as tax laws and withholding guidelines may change. The IRS also provides instructions along with the form to assist you in completing it accurately.

Not Reviewing the Instructions Carefully

Many people rush through the W-4P form without thoroughly understanding the instructions. Each section serves a purpose, and skipping or misinterpreting them can lead to errors that affect withholding amounts.

Incorrectly Estimating Tax Withholding

Estimating how much tax should be withheld can be challenging. Some individuals either overestimate or underestimate their tax situation, which can result in receiving an unexpected tax bill or a smaller refund than anticipated.

Failing to Update Information

Life circumstances change. Failing to update the W-4P when there are changes in income, marital status, or deductions can lead to incorrect withholding amounts.

Neglecting to Account for Other Income

People often forget to consider additional sources of income, like interest or dividends. This oversight can impact overall tax liability and lead to insufficient withholding.

Not Signing and Dating the Form

A common oversight is submitting the form without a signature and date. This simple step is crucial, as an unsigned form is considered invalid and may lead to processing delays.

When dealing with taxes, various forms and documents can arise depending on your financial situation. The IRS W-4P form is used for withholding on pensions and other periodic income, but it often travels alongside several other important documents. Below is a list of forms that might commonly be utilized in conjunction with the W-4P.

Understanding these forms can make the tax filing process smoother and help ensure compliance with tax regulations. Each document plays a unique role in reporting your financial situation, and being organized can save you time and potential headaches in the future.

The IRS W-4P form is primarily used for tax withholding purposes from pension payments. One similar document is the IRS W-4 form, which is used by employees to indicate their tax situation to employers. Both forms require individuals to provide personal information, such as their name, address, and Social Security number. Importantly, both allow individuals to specify allowances or exemptions, which play a crucial role in determining how much tax is withheld from their payments. Essentially, while the W-4 is for regular employment income, the W-4P applies specifically to pension payments, aligning their overall purpose in managing tax withholdings.

Another related document is the IRS W-4S, which is designed for use by students receiving certain types of payments. This form, like the W-4P, provides a mechanism to indicate the preferred withholding amount from the payments being received. Similar to the W-4P, it allows individuals to clarify their tax status, ensuring appropriate tax withholding. The underlying principle remains the same: both forms are intended to facilitate better tax management based on personal financial circumstances, albeit for different types of payments.

The IRS 1099 form also shares similarities with the W-4P, especially since both pertain to income reporting and taxation. The 1099 is used to report various forms of income other than wages, salaries, or tips, including interest, dividends, and pensions. Recipients often must utilize the information from the 1099 form to complete their tax returns accurately. While the 1099 does not address withholding directly, it underscores the requirement of reporting income from which taxes might have already been withheld, creating a link between these two documents in the realm of income taxation.

Additionally, the IRS W-2 form has similarities with the W-4P. The W-2 form is used by employers to report wages, tips, and other compensation paid to employees, along with the taxes withheld. Both forms involve an employer or payee's action regarding tax withholding processes. An essential difference exists in the context: the W-2 is for employees while the W-4P deals specifically with pension recipients. Nevertheless, both documents ultimately aim to provide transparency in income reporting and facilitate correct tax filing.

Lastly, the IRS Form 1040 has common ground with the W-4P in the context of tax filing. Individuals report various sources of income, including pensions, on their Form 1040. While the W-4P specifies how much tax to withhold, the Form 1040 serves as an annual report to the IRS detailing overall income and taxes owed or refunded. Therefore, understanding how the information from the W-4P influences the figures reported on the 1040 is crucial for effective tax management and compliance.

When filling out the IRS W-4P form, consider the following dos and don'ts:

The IRS W-4P form is used by taxpayers to instruct the IRS how much federal income tax to withhold from certain types of payments. However, there are several misconceptions surrounding its use. Below is a list of common misunderstandings about the W-4P form that can impact taxpayers.

Understanding these misconceptions can help taxpayers make informed decisions regarding their tax withholding and overall financial planning.

The IRS W-4P form is used to determine federal income tax withholding on pension or annuity payments.

Completing this form accurately can help prevent over- or under-withholding, ensuring you receive the appropriate amount during tax season.

It’s important to update your W-4P if your financial situation changes, such as if you start a new job, retire, or experience any significant income change.

Keeping a copy of your completed W-4P for your records can help you track your withholding choices for future reference.