The IRS Schedule SE (Self-Employment) form is an essential tool for self-employed individuals reporting their net earnings from self-employment. This form, part of the 1040 series, enables taxpayers to calculate their Social Security and Medicare tax obligations. By considering both net earnings from self-employment and any applicable deductions, Schedule SE helps determine the self-employment tax, which is separate from income tax. It features specific sections for taxpayers to report income derived from a trade or business, farm income, and even income from sole proprietorships and partnerships. Importantly, certain income exclusions apply, such as specific amounts that may be exempt from self-employment tax. Moreover, the form guides taxpayers through the complex process of figuring out their earnings while ensuring compliance with federal tax regulations. Effectively navigating Schedule SE allows self-employed individuals to fulfill their tax responsibilities accurately and timely.

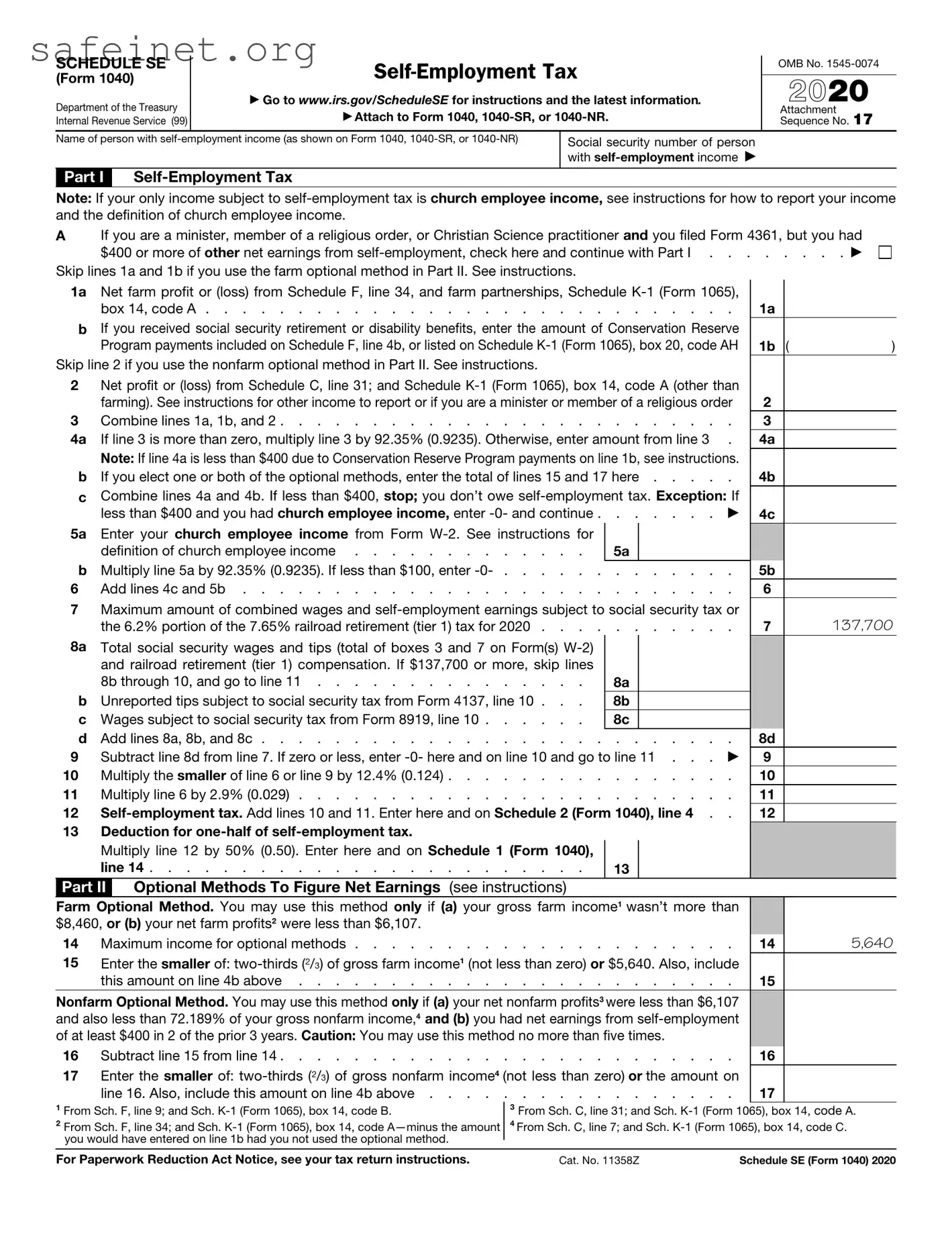

SCHEDULE SE

(Form 1040)

Department of the Treasury Internal Revenue Service (99)

▶Go to www.irs.gov/ScheduleSE for instructions and the latest information.

▶Attach to Form 1040,

OMB No.

2020

Attachment Sequence No. 17

Name of person with

Part I

Social security number of person with

Note: If your only income subject to

AIf you are a minister, member of a religious order, or Christian Science practitioner and you filed Form 4361, but you had

$400 or more of other net earnings from

1a Net farm profit or (loss) from Schedule F, line 34, and farm partnerships, Schedule

bIf you received social security retirement or disability benefits, enter the amount of Conservation Reserve Program payments included on Schedule F, line 4b, or listed on Schedule

Skip line 2 if you use the nonfarm optional method in Part II. See instructions.

2Net profit or (loss) from Schedule C, line 31; and Schedule

3 |

Combine lines 1a, 1b, and 2 |

4a |

If line 3 is more than zero, multiply line 3 by 92.35% (0.9235). Otherwise, enter amount from line 3 . |

|

Note: If line 4a is less than $400 due to Conservation Reserve Program payments on line 1b, see instructions. |

b |

If you elect one or both of the optional methods, enter the total of lines 15 and 17 here |

cCombine lines 4a and 4b. If less than $400, stop; you don’t owe

5a |

Enter your church employee income from Form |

See instructions for |

|

|

|

definition of church employee income |

. . . . . . . |

5a |

|

b |

Multiply line 5a by 92.35% (0.9235). If less than $100, enter |

|||

6 |

Add lines 4c and 5b |

|||

7Maximum amount of combined wages and

the 6.2% portion of the 7.65% railroad retirement (tier 1) tax for 2020 . . . . . . . . . . .

8a |

Total social security wages and tips (total of boxes 3 and 7 on Form(s) |

|

|

|

|

and railroad retirement (tier 1) compensation. If $137,700 or more, skip lines |

|

|

|

|

8b through 10, and go to line 11 |

8a |

|

|

b |

Unreported tips subject to social security tax from Form 4137, line 10 . . . |

8b |

|

|

c |

Wages subject to social security tax from Form 8919, line 10 |

8c |

|

|

d |

Add lines 8a, 8b, and 8c |

|||

9 |

Subtract line 8d from line 7. If zero or less, enter |

|||

10 |

Multiply the smaller of line 6 or line 9 by 12.4% (0.124) |

|||

11 |

Multiply line 6 by 2.9% (0.029) |

|||

12 |

||||

13 |

Deduction for |

|

|

|

|

Multiply line 12 by 50% (0.50). Enter here and on Schedule 1 (Form 1040), |

|

|

|

|

line 14 |

13 |

|

|

Part II |

Optional Methods To Figure Net Earnings (see instructions) |

|

|

|

1a

1b ( |

) |

2

3

4a

4b

4c

5b

6

7137,700

8d

9

10

11

12

Farm Optional Method. You may use this method only if (a) your gross farm income1 wasn’t more than |

|

|

$8,460, or (b) your net farm profits2 were less than $6,107. |

|

|

14 Maximum income for optional methods |

14 |

5,640 |

15Enter the smaller of:

this amount on line 4b above |

15 |

|

Nonfarm Optional Method. You may use this method only if (a) your net nonfarm profits3 were less than $6,107 |

|

|

and also less than 72.189% of your gross nonfarm income,4 and (b) you had net earnings from |

|

|

of at least $400 in 2 of the prior 3 years. Caution: You may use this method no more than five times. |

|

|

16 Subtract line 15 from line 14 |

16 |

|

17Enter the smaller of:

line 16. Also, include this amount on line 4b above |

17 |

1From Sch. F, line 9; and Sch.

2From Sch. F, line 34; and Sch.

3From Sch. C, line 31; and Sch.

4From Sch. C, line 7; and Sch.

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 11358Z |

Schedule SE (Form 1040) 2020 |

Schedule SE (Form 1040) 2020 |

Attachment Sequence No. 17 |

Page 2 |

|

Part III |

Maximum Deferral of |

|

|

If line 4c is zero, skip lines 18 through 20, and enter

18Enter the portion of line 3 that can be attributed to March 27, 2020, through December 31, 2020 . .

19If line 18 is more than zero, multiply line 18 by 92.35% (0.9235); otherwise, enter the amount from line 18

20Enter the portion of lines 15 and 17 that can be attributed to March 27, 2020, through December 31,

2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

21 Combine lines 19 and 20 . . . . . . . . . . . . . . . . . . . . . . . . . .

If line 5b is zero, skip line 22 and enter

22Enter the portion of line 5a that can be attributed to March 27, 2020, through December 31, 2020 . .

23 |

Multiply line 22 by 92.35% (0.9235) |

24 |

Add lines 21 and 23 |

25 |

Enter the smaller of line 9 or line 24 |

26Multiply line 25 by 6.2% (0.062). Enter here and see the instructions for line 12e of Schedule 3 (Form 1040) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

18

19

20

21

22

23

24

25

26

Schedule SE (Form 1040) 2020

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule SE (Form 1040) is used to calculate the self-employment tax owed by individuals with net earnings from self-employment. |

| Who Needs It? | Individuals who are self-employed, as well as those who earn income from a partnership or limited liability company (LLC), must file this schedule if their net earnings exceed $400. |

| Tax Rate | The self-employment tax rate is currently 15.3%, which consists of 12.4% for Social Security and 2.9% for Medicare. An additional 0.9% Medicare tax applies to higher income levels. |

| Filing Deadline | The Schedule SE must be filed along with your Form 1040 by the tax return deadline, which is usually April 15 of each year. |

| Importance of Accurate Reporting | Accurate reporting is crucial. Underreporting income can lead to penalties and interest charges from the IRS, which can increase your overall tax liability. |

Completing the IRS Schedule SE form is essential for self-employed individuals to report their income and calculate their self-employment tax. To ensure accuracy, follow these steps carefully. Gather your business revenue and expenses, as these will be necessary for filling out the form correctly.

Taking the time to fill out Schedule SE accurately helps ensure you meet your tax obligations without unexpected surprises. Double-checking your work can save you time and potential issues later.

What is the IRS Schedule SE form?

The IRS Schedule SE (Self-Employment Tax) form is used by individuals to calculate and report self-employment tax. This tax primarily consists of Social Security and Medicare taxes for self-employed individuals. It is important for freelancers, independent contractors, and business owners who earn income outside of traditional employment to file this form to ensure compliance with tax obligations.

Who needs to file Schedule SE?

Taxpayers who earned $400 or more in net self-employment income must file Schedule SE. This includes individuals who operate a business as a sole proprietor, freelancers, and those receiving income from partnerships or LLCs that are treated as partnerships for tax purposes. Even if self-employed individuals do not owe any income tax, they still need to file to pay the self-employment tax.

How do I calculate self-employment tax?

To calculate self-employment tax, total your net earnings from self-employment. This figure is then multiplied by the self-employment tax rate, which is currently 15.3%. This rate consists of 12.4% for Social Security and 2.9% for Medicare. A portion of this tax may be deducted when calculating taxable income, making the effective tax burden slightly lower.

What if my net earnings are less than $400?

If your net earnings from self-employment are below $400, you are not required to file Schedule SE or pay self-employment tax. However, if you had any income from self-employment, you might still want to report that income on your tax return, particularly if you wish to qualify for certain tax credits or benefits.

Can I deduct any expenses when calculating self-employment income?

Yes, self-employed individuals can deduct business-related expenses when calculating their net income. This includes costs for supplies, travel, equipment, and other necessary expenses incurred while operating the business. Accurate record-keeping is essential to substantiate these deductions during tax filing.

What are the deadlines for filing Schedule SE?

Schedule SE is typically due on the same date as your federal income tax return. For most taxpayers, this means the form is due on April 15. If you file for an extension, you must submit Schedule SE by the extended deadline, which is usually October 15. Be mindful of these dates to avoid penalties.

Where do I submit the Schedule SE form?

Schedule SE is submitted along with your Form 1040 when filing your tax return. If you are electronic filing, most tax software will automatically include Schedule SE with your submission. For paper filers, attach Schedule SE to your Form 1040 and mail it to the address provided in the instructions.

Is there a limit on how much self-employment tax I can pay?

While there is no overall limit on self-employment tax, there is a cap on the amount of income subject to the Social Security portion of the tax. For 2023, this cap is $160,200. Income above this threshold will not be subject to the 12.4% Social Security tax, though the 2.9% Medicare tax applies to all self-employment income, with an additional 0.9% Medicare tax for higher earners.

Incorrect Calculation of Net Earnings: One common mistake is miscalculating net earnings from self-employment. Individuals often forget to account for certain deductions that can lower their self-employment income. This oversight can lead to an inaccurate tax liability.

Failure to Use the Correct Rates: Taxpayers sometimes use the wrong self-employment tax rate. The IRS has specific tax rates that apply, and failing to check for updates or changes can result in mistakes. Using outdated rates impacts the final tax calculation.

Omitting Required Information: Schedule SE requires specific information to be filled out correctly. Many people neglect to include all necessary details, such as income sources or previously filed forms. This can lead to delays or additional requests for information from the IRS.

Rounding Errors: Simple rounding mistakes can accumulate over the various calculations on the form. Round numbers up or down incorrectly, and it can skew the final results. Precision is critical in ensuring that the file is accurate and complete.

The IRS Schedule SE (Self-Employment Tax) is a key document for individuals who earn income through self-employment. Along with this form, several other documents are often necessary for accurate reporting and compliance with tax regulations. Here is a list of related forms and documents that individuals may need to use in conjunction with Schedule SE:

Understanding these forms and documents helps individuals navigate the complexities of self-employment and tax filing. Proper use of these items ensures compliance with IRS requirements and can lead to potential savings when filing taxes. Each of these elements contributes to a comprehensive view of a taxpayer's financial situation.

The IRS Schedule C form is similar to Schedule SE in that both are used by self-employed individuals. Schedule C provides details about the income and expenses related to a business, enabling taxpayers to report profits or losses. In contrast, Schedule SE is focused on calculating and reporting self-employment tax based on that income. Together, these forms help ensure that self-employed individuals accurately report their earnings and pay the appropriate taxes on them.

Another related document is the IRS Form 1040 itself, the main individual income tax return form. While Form 1040 serves as the overall tax return where individuals report various types of income, adjustments, and credits, Schedule SE is specifically designed for calculating self-employment tax. Essentially, taxpayers showcasing self-employment income must attach Schedule SE to their Form 1040 to ensure they pay the correct amount in taxes.

The IRS Form 1099-NEC also has a close relationship with Schedule SE. This form is used to report non-employee compensation, such as income earned by freelancers and independent contractors. If you receive a Form 1099-NEC, it indicates you have self-employment income, which must be accounted for on Schedule SE. Thus, the information reported on Form 1099-NEC often becomes the basis for completing the Schedule SE calculations.

Lastly, the IRS Schedule A is another document that bears similarities. While Schedule A is used for itemizing deductions, it often includes deductions related to business expenses that self-employed individuals can claim. Although not directly related to the calculation of self-employment tax, the information from Schedule A may play a role in determining the net income to report on Schedule SE. Understanding how these deductions affect overall tax obligations can be key for self-employed individuals.

Filling out the IRS Schedule SE (Self-Employment Tax) form can seem daunting, but a few guidelines can help make the process smoother. Here is a list of things you should and shouldn't do when completing this form.

By following these simple tips, you can navigate the Schedule SE form with more confidence and accuracy. Proper preparation leads to better outcomes.

The IRS Schedule SE (Self-Employment) form may cause confusion for many individuals. Here are six common misconceptions about this form, along with clarifications to help you better understand its purpose.

Understanding these misconceptions can help you navigate your tax responsibilities more effectively. Always consider seeking guidance from a tax professional if you have questions about your specific situation.

When filling out the IRS Schedule SE (Self-Employment Tax) form, here are some important points to keep in mind:

Taking the time to understand these key points will help in accurately completing your Schedule SE form and ensuring compliance with tax regulations.